Consensus community valuation

Had a crack at applying @Rick's McNiven preso and spreadsheets to come up with a crude 1st attempt to value XRF following the recent 1HFY24 results.

- Using @Rick's xls as the base, I modified the xls as the means for me to internalise the McNivens formula and how it works.

- I also parameterised the xls for me to input figures from the Appendix D statements, forecast growth etc - figures in red are inputs, figures in blue are calculations.

Assumptions

- Used a 10% rate of return, about 2x what the current Term Deposit rate is - XRF is well run, conservative etc, so the risk of anything silly happening was very much on the lower end - this was applying the % used by @PortfolioPlus

- Assumed that NPAT growth for 2HFY24 was 20% - improvement in Germany, Orbis crushers, still strong mining demand etc.

- No change to dividend payout ratio in FY24 from FY23 at 59%, fully franked - there is still need for some moderate capex for facilities expansion etc but Vince has flagged no major capex, so assuming the same ratio feels about right

Still much to learn but this was a start to the valuation process and it feels "about right".

Looks like Westferry is no longer in the top 20.

The overhang that is causing the downtrend is starting to make sense

2022 Annual Report

2023 Annual Report

However, Westferry still counts XRF as one of the top holdings

As Westferry is not a substantial holder, we don't know when the sale occurred or how much they have keft

Capital IQ Pro reckons it is zero but from above I think that could be wrong.

Might be a good but pointy question to ask?

[held]

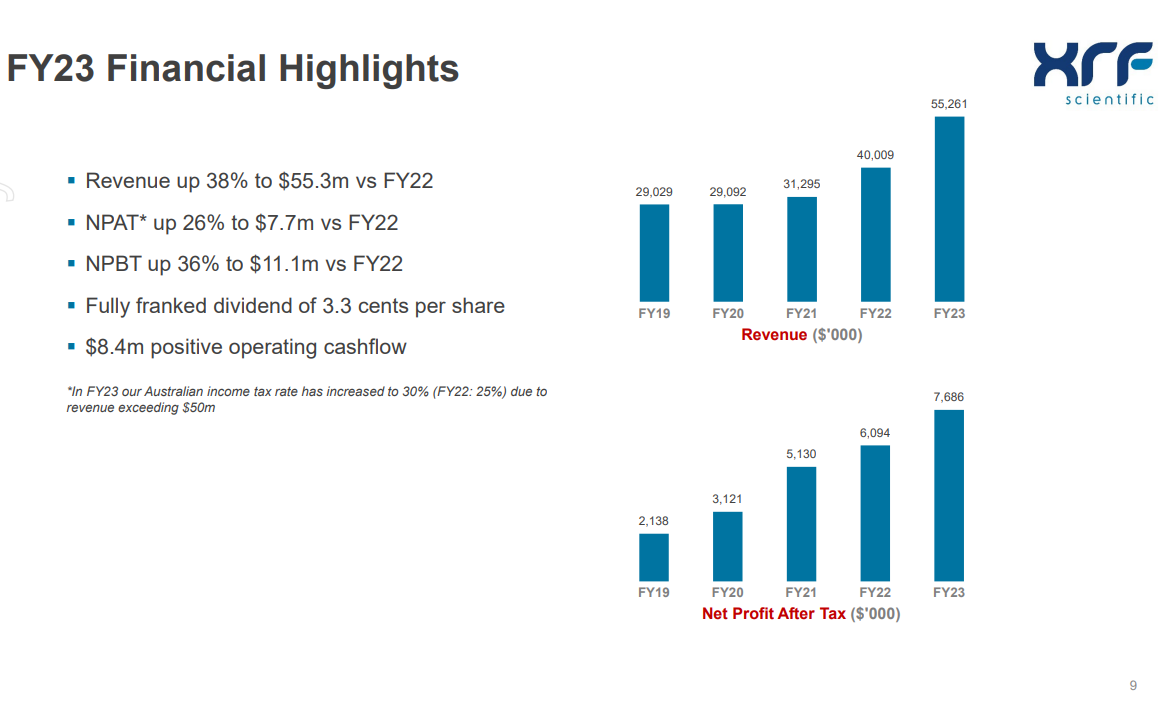

Record revenue and profit

Very strong demand from mining and industrial customers

Strong demand for capital equipment products, currently at record order levels

Launch of new product line: xrTGA thermogravimetric analyser

Continued R&D investment in new products across all divisions

Outlook: We expect the December 2023 quarter to be a positive period, with a focus on machine lead times, xrTGA sales, new product developments and international sales growth

Return (inc div) 1yr: 22.99% 3yr: 52.81% pa 5yr: 48.26% pa

Market Cap; $132M

*limited analyst coverage along with low trading liquidity holds XRF back. Reduction in mining industry generally

Combined my notes on the 30 Sep 2023 Quarterly Update and today's meeting with Vince Stazzonelli.

Discl: Held IRL and in SM, looking to top up IRL if the price falls closer to $0.90.

Built this simple revenue xls to get a better perspective of the 1QFY24 results against FY23, will add in subsequent quarters

- Solid result with PBT growing much more than Revenue

- Consumables was up 15.8%, Capital Equipment was up 27.5% but Precious Metals was down 14.9% over the PCP

- Revenue is 5.9% lower than the average FY23 quarterly revenue (average is annual revenue divided by 4)

- Not a concern given the large forward orders held for Precious Metals, but puts the 1Q result in better context, taking cue from concerns previously about the rate of growth from H-to-H

- All segments appear to be firing, with the order book for capital equipment at record levels, and production for some products is now being scheduled for the June 2024 quarter

TAKEAWAYS FROM VINCE MEETING

Industry Tests to test quality of a product which XRF Supports

- XRef Analysis - using X-Ray Fluorescence analytical technique to determine the major components of a sample

- ICP Analysis - ICP (Inductively Coupled Plasma) Spectroscopy is an analytical technique used to measure and identify elements within a sample matrix based on the ionization of the elements within the sample.

- Gold - FireAssay and PhotonAssay (C79’s technology)

- Platinum Labware - this is used in the sampling process. XRF manufactures Platinum Labware for all machines, not only XRF-specific machines

How the XRF Equipment Comes Into Play

- Orbis Mining Crushers - breaks down (crushes) big rocks to provide powder samples, which are then used as inputs to the various tests

- XRTGA Thermogravimetric Analyser - a high-temperature furnace, heats up the sample to run tests at different temperature points

- Market is dominated by key competitor: Leco

- XRF’s benefits over Leco units:

- 30 samples at a time vs 18

- Has heating and cooling cycles to speed up the process

- User friendly Touch Screen vs separate computer console

- Reputation of building reputable products

- Provides complementary data for XRF analysis

- XrTGA opens up access to new markets for XRF - Pharmaceuticals, Food, Agri-Products, Plastics etc

- Capital equipment should have at least 7-8 years of life through to 15 years

- Drives other products - spare parts, labware rework, consumables

Manufacturing Capacity

- Solved factory capacity issue for Capital Equipment this past quarter

- Can ramp up production across all 3 segments by adding more shifts - no further major spend to boost capacity is anticipated

International Expansion

- Already have presence in Europe (Germany and Belgium), North America (Montreal), Australia and parts of Asia

- Direct sales are fulfilled in Australia

- Large network of Distributors which are required to provide on-the-ground customer support

- Not in a position to open offices in many countries - driven by product line and the individual needs of the countries

Cost Pressures

- Cost pressures of the last 12-18M have eased in the last 3-6M - lead time blow outs

- Able to pass on price increases to customers who mostly pay based on the metal spot price at the time of invoice

- Employees were given good pay increases to retain them

Customer Demand

- Exploration activity mostly focused on Rare Earths, Lithium

- Exploration spend did not fall in Australia - Gold spend did fall, but Base Metals, Iron Ore continued to perform well

- Have not seen anything impacted by a slowing of Chinese demand

Capex Management Approach

- Dividend payout ratio is around 60% - this level of dividends is able to provide required capital for R&D, Inventory and Working Capital

- On the lookout for bolt on acquisitions - generally like to issue script to fund these acquisitions to incentivise vendors

- Ideal targets are (1) lab products which have business synergies with XRF’s products (2) used by existing customers (3) are under-developed in market potential

- Not interested in building business scale as XRF is at “about the right size” - focus is on value adding acquisitions

Key Investor Misunderstanding on XRF

- Investors misunderstand where XRF sits in the laboratory process

- High quality products

- Strong IP

- Essential in providing data to mines, industrials

- Critical to customers processes

Well it appears that my days as a valued member of Capital IQ pro are numbered

I've been blocked from looking at the most recent estimates

But I still managed to find that XRF had received a downgrade from an unknown broker. My guess it is Euroz

Revenue downgrade of 9%

Sentiment changed to hold

Price target maintained at 1.22

Since Aug 2023, XRF has dropped more than 9%

[held]

Scroll down - latest updates are the end...

23-July-2021: I do not follow this one closely enough to add much value here unfortunately. They're in my Strawman.com virtual portfolio, but I've been selling down and taking profits there. The wind has come out of the sails a little in the past couple of weeks, and I think they need to have a ripper of a report next month to get them to resume that upward trajectory once again. My gut feel is that 40 cps is reasonable knowing what we know now, and anything above that is probably pricing in future growth that is not guaranteed to happen, but well might. In that light, they do look a little overbought above 45 cps, and if they have a poor report or even an ordinary report, I can see further downside. That said, I'm obviously wishing they do shoot the lights out, for the sake of all of the XRF shareholder we have here on Strawman.com.

25-Oct-2021: Update: ...And they did shoot the lights out, great report, and here they are testing all-time highs once again around 66 to 68 cps. Wish I still held them in real life. Not only has their share price been flying, they've also upped their dividend every 6 months since 2017, including through Covid.

At least I still have some XRF in my SM portfolio...

Upgrading my PT to 77cps.

03-Nov-2022: Update: Raising my Price Target (PT) from 77 cents to 90 cents because the company is now trading at 80c, i.e. above my previous 77c/share PT. The company continues to perform well and surprise the doubters, however I think it will take a fair bit to push through $1, so they might hang around 90c/share or thereabouts for a while before having a few goes at $1 and beyond.

I'm not going to talk about the company's fundamentals because it's not a company I follow closely now, and not one I currently hold IRL (although I have previously, and I did follow them a lot more closely then). They're in my Strawman.com virtual portfolio however, and they've performed well for me, albeit it's a relatively small position, as many of my positions here are. I was just looking through and noticed that this "valuation" was stale, so thought I'd "refresh" it. So I did.

10-Sep-2023: Updating this one again: Once again, I have to move my price target (not a valuation, just a price target) up, because the SP has overtaken my old one yet again and the business has outperformed even my lofty expectations.

I'll target $1.48 this time, and I know that's not particularly brave, since XRF closed at $1.41 on August 1st this year and were as high as $1.435 in intraday trading back then, however I'm happy to keep raising the bar and watch them sail over it again with apparent ease. There's not much of a negative nature you can say about XRF. They have good management, a good business model, they have products and services that companies and organisations need, they are very well positioned within their industry, and they keep moving in the right direction.

Occasionally they look over-valued by the market, i.e. not cheap, but then they never seem to put a foot wrong, and they don't take too much time to grow into those lofty valuations. Quality company. Quality products and services. One of the few companies who are able to increase their ROE as they grow:

Source (above bar graphs): Commsec.

Below sourced from FNArena.com:

While FNArena is showing some NPM decline over the past two years, their Net Profit Margin is still higher than it was FY18, FY19 and FY20, and still above 10%, which is a good NPM for a business of their type. Everything else (Book Value/share, Cashflow, Sales Revenue, Earnings, Dividends/share, ROE and EPS) are all continuing to rise at a good clip.

They weren't always heading northeast at a good clip, but they have been since 2018 (so for the past 5 years), and the company has never looked stronger.

Disclosure: I do hold XRF here in my SM virtual portfolio and I have held them on and off in real life also. Currently not holding IRL, but wishing I was. This is one of those companies that is high enough quality that I should just hold them through and not try to sell in and out and time them so much.

Adding further info to my comment on why the share price fell. I won't worry about drawing the graph as the numbers show the trend well enough.

My last comment mentioned margins fell, but it was only minor about 2% 2H2022 versus 2H2023

However of most concern is the revenue growth. It was only 4% from end of 1H2023 to 2H2023 versus 16% from end of 1H2022 to 2H2022.

Also earnings between 1H2023 and 2H2023 was only 5% growth versus 22% growth between 1H2022 to 2H2022

In summary it seems both revenue and growth stalled from the beginning of the 1st half to the end of June 2023 down to single digits.

The market reacted as expected, even though the numbers looked good,because the growth from previous period was not as much as opposed to the corresponding period. I think market wanted consistent double digit growth but unless I did something wrong above, it looks like growth is becoming marginal.

[held]

- Summary: August 2023 Investor Presentation

3 x Segments Below:

Return (inc div) 1yr: 98.03% 3yr: 67.98% pa 5yr: 52.85% pa

Shares in Value have just emailed their thoughts on XRF, here they are:

Our high-conviction pick for this month is XRF Scientific (ASX: XRF), a significant player in the mining industry, providing essential gas and electric fusion equipment for mineral sample preparation, a prerequisite for X-ray fluorescence analysis. This indispensable process plays a pivotal role in shaping the strategies of industry heavyweights like BHP, Glencore, Vale, South 32, and Alcoa, who depend on it for assessing the grade, reducing waste rock, and formulating drilling plans. The role of sample preparation cannot be understated—it serves as the vital initial step in deciphering a sample's chemical purity and composition.

We recommended XRF to our members in January at $0.84, and it has grown 58% in the last 6 months to a princely $1.33 (effective 27 July 2023).

So why do we remain so bullish on XRF?

XRF's unique non-cyclical attribute offers uncommon stability in the volatile mining industry. Further, the company follows a Gillette-style business model, providing high-margin chemical agents essential for each sample preparation.

Over the years, the company has been undervalued as a mining services supplier rather than being recognised for its inherent value as a premium international equipment provider, a reputation reinforced by 28% and 19% revenues and profits growth in 2022. It also maintained a 60% dividend payout ratio, delivering a yield of over 3%, a beneficial attribute for those pursuing dividend returns. The company's record-breaking order book indicates there is potential for further growth.

With the increasing demand for low-emission technologies driving commodity growth, XRF, central to mining activities, stands to benefit. Looking forward, XRF's ambitious 2023 expansion plan is noteworthy. With strategies targeting geographical diversification, new product launches, and a particular emphasis on precious metals, XRF offers a blend of steady cash flows with a balance of growth and dividends.

A substantial amount of credit for XRF's success is due to the tenacious leadership of CEO Vance Stazzonelli. He embodies the ideal qualities that we at Shares in Value believe are crucial in an effective leader: honesty, accuracy, and a refreshing lack of pretentious adjustments in the financial results. His straight-shooting approach, especially in the small caps realm, sets him apart.

Under Vance's steady helm, XRF continues to deliver exceptional results. Despite the considerable recent surge in its share price, we are confident in our recommendation of XRF, believing in its long-term potential.

Competitive Advantages: Large sample carousel with 30 positions for greater throughput Higher maximum temperature range up to 1100°C Highly automated and user-friendly interface Fast heating and cooling cycle times Fully integrated PC without the need for an external unit

Had a mighty run -up Return (inc div) 1yr: 104.89% 3yr: 72.11% pa 5yr: 53.00% pa

20/5/2023: A look at NPAT.

Below from the Feb 2023 Report:

2023 shares on Issue: 135,8

June 2022 NPAT actual reported: $6,084Mill

Forecast June 2023: NPAT $7,909Mill = 6,084 x 1.3 ( say NPAT growth is 30%pa )

Find EPS for June 2023: 5.82cps = 7,909 / 135,8

so Valuation Range $1 to $1.35

1st Guess Pe ratio 23% = 135cps / 5.82cps ( Bull )

Vs

2nd Guess Pe ratio 17.18% = 100cps / 5.82cps ( Bear )

Market cap:$88Mill

ROE: growth has been good

ROE future: some pundants thinking lower in 2023.

EPS growth likely to tail off in 2023 Free cash flow ok

Free cash flow: current 3.25c out -look 4.47cp

PE ratio 18% then future pe taper off to 15 times earnings

Revenue stream or silo's of cash from Australia , Canada, Europe.

A solid performance will the buyers get excited again..

Return (inc div) 1yr: 38.08% 3yr: 55.22% pa 5yr: 35.49% pa

David Brown: Consideration $60,180

Securities b) 3,059,163 Securities held after the change b) 3,110,163

Good 1yr Price trend here

I’ve been watching XRF but still don’t own it unfortunately. Congratulations to those who jumped on board.

@Winiwas spot on in forecasting the incremental growth rate in ROE. Generally other analysts didn’t see this coming so I should have taken more notice of Wini’s forecast!

Assuming FY23 NPAT of c. $11 million and current equity of $49 million, that puts XRF on FY23 ROE of over 24% (even higher than Wini’s forecast of 22.5%). The ROE chart is likely to look something like this for FY23. That’s a significant jump and supports Wini’s view that XRF is a capital light business.

@edgescape put forward a valuation of $1.58 based on historical PE ratios x forecast FY23 earnings. If I use McNiven’s Formula assuming a forward ROE of 24% and a 10% required return on investment I get a similar valuation to Edgescape. If you were requiring a higher return on your investment, say 12%, the current valuation would be $1.20 or about the current share price. If the incremental growth in ROE continues into the future this will push the valuations higher still. Wini might have a view on what the future looks like from here.

My guess is that share price will now be influenced more by share price trends and the chartists in the short term, so I wouldn’t be surprised if the share price reached $1.80 or higher. If I owned XRF I wouldn’t be selling it in a hurry while the green candles continue and MACD sits in positive territory.

However, ignoring the charts and considering a ROE based valuation with a required return on investment of 15%, I won’t be buying at the current share price of $1.20 either. Good luck to those who are holding.

Not held

Sales of capital equipment products have been robust at $3.9m compared to $2.8m in the PCP. The demand is being driven globally by both the mining and industrial sectors. Geographical growth is adding to revenue, and certain markets have been reactivated post COVID‐19 impacts. For some core products our order book remains at record levels, with production now being scheduled into the December 2023 quarter. We are working to reduce our lead times through the addition of new labour and inventory resources.

- Summary:Summary: March 2023 Quarterly Trading Report

- Price Sensitive: Yes

27-Aug-2021: Click here to watch Luke "Wini" Winchester from Merewether Capital talking on Ausbiz on Friday (27-Aug-2021) about the recent (24th Aug) full year results from XRF Scientific (from the 3:30 mark of the video), Kip McGrath Education and Austco Healthcare. Wini was the Emerging Companies Portfolio Manager at Oracle Investment Management (and might still be according to his LinkedIn profile), and is now the CIO of Newcastle-based Merewether Capital, which ARC have just bought 40% of. Luke discloses that he owns all three of those companies (XRF, KME and AHC) and he's bullish on them clearly, and when Wini is bullish on a company it's worth noting!

Disclosure: I do not hold any of those companies in RL, but XRF is in my SM portfolio (and ARC is on my watchlist).