It’s been a bit quiet on Strawman since Easter. My two lovely granddaughters have kept me busy playing Sequence, drafts, checkers, chess amongst other things. I don’t even get the chance to knock out a straw before breakfast because they’re in our bed from 6am! :)

It hasn’t stopped me from adding a few shares though. I notice there’s been a lack of interest in Lycopodium shares by the market since it went ex-dividend on 25 March 2024. When a business paying a 7% fully franked dividend goes ex-div you might expect a decent pull back. However, yesterday Lycopodium traded at $11.00, and at that price I think it’s a BUY.

I maintain my valuation of $15.00 for Lycopodium shares, and I am even more bullish on the business than a month ago. I’ve been adding more shares at just over $11.00. Buying at today’s share price I think you could expect an annual return of 18% per year. The share price only needs to grow at 8% per year to achieve that.

Gold is trading at record prices and most of Lycopodium’s projects are in servicing gold miners in Africa.

With a strong pipeline of studies and projects in delivery, the Company remains on track to achieve the previously advised full year guidance of approximately $345 million in revenue and NPAT in the range of $46 to $50 million. The total value of capital projects currently in delivery is in the order of A$4 billion.

Bell Potter Unearthed Conference Presentation

Assuming mid-range NPAT of $48 million ($1.21 per share) Lycopodium is trading at 9 x FY24 earnings. I think Lycopodium’s guidance is very conservative and I expect guidance might be upgraded toward the top end in the next month or two.

What I really like about this business is the ROE has been increasing for several years and now sits on c. 40%. it has achieved this with zero debt and increasing cash reserves. The balance sheet is impeccable! While it is paying out a massive dividend of c. 7% fully franked, it continues to reinvest 30% of its earnings back into growth at a 40% internal rate of return. You get all this for a low PE of just 9 times NPAT. It’s a bargain in my eyes, even at an historically lofty share price of $11.00.

Source: Commsec Website

It’s important to remember that Lycopodium is a cyclical stock, and it will follow the fortunes of the resource industries, particularly gold. I think the outlook for the business should remain strong while the gold price is near record highs.

Held IRL (4.8%) and adding

Friday 10-Nov-2023: Firstly, I've written plenty on LYL previously - which you can read here: https://strawman.com/reports/LYL/Bear77 including a straw titled, "Income, Growth, Both?" - which you can probably find towards the top of the pile here: https://strawman.com/reports/LYL/all

Having failed to highlight the insider ownership with EGL in my recent straw on them (and a few other things that Harley Grosser pointed out in his own recent Livewire Markets "wire" on EGL: https://www.livewiremarkets.com/wires/an-undervalued-small-cap-growth-story), I thought I'd kick off this LYL update with that insider ownership data, before I forget again:

Lycopodium (LYL) has HEAPS of insider ownership, so plenty of shareholder alignment:

Source: Commsec data plus Lycopodium's FY23 Annual Report and their FY23 Shareholder Report.

The Board and Management own 36% of the shares on issue, which reduces the "free float" and is a factor in why it has taken LYL so long to be included in the All Ords Index (XAO) - they were only added in March this year. They are still not in the ASX300 index.

They also don't like issuing new shares very often - in fact the shares on issuee have been stable for the past decade - as highlighted by me in green below:

As highlighted by me in blue at the bottom of that Commsec screenshot above, LYL are trading at a reasonably low PE compared with their average PE over the previous decade. Their PE Ratio was 6.5 on June 30, and it's just over 8 currently. They are NOT expensive.

However, they are relatively small, and they can be quite illiquid at times, with usually less offers on the SELL side and more bids on the BUY side, which I assume is because the majority of LYL shareholders aren't looking to sell their shares. As a result of the low liquidity and the gaps between the bids and between the offers, their share price can bounce around quite a bit on relatively small volume (of shares traded).

Screenshots taken from Commsec and added to by me.

They do pay excellent fully franked dividends, with their trailing dividend yield being over 8% (plus the value of their franking credits, so over 12% grossed up to include the full value of those FCs).

Their dividends rise along with their earnings, and their earnings have been rising - see the top of the previous screenshot above - the Earnings chart - and now take a gander at the ROE chart beside it - how's that for a services company that is involved in engineering and construction - an ROE of over 40% - and rising!!

Now - while their shares on issue haven't changed for a decade (it's been 39.7m shares every year, as shown above), they are going to be issuing a small amount of extra shares to management as share-based payments and so forth, as explained here:

Source: Page 74 of Lycopodium's FY23 Annual Report.

The company has been ASX-listed for almost two decades, mostly with the same management and Board who include the company's founders, so they have been doing this for some time, and they know what they're doing.

I found some good stuff in their recent Shareholder Report (released with their FY23 Full Year Results in August):

Above, we see that they have become diversified across Infrastructure and Industrial Processes, in addition to their traditional core sector, Resources.

Below we also see that they have diversified across geographies (Regions), however it's worth noting that Africa remains a large part of their revenue, and they remain very active in West Africa in particular.

West Africa has plenty of risks, and LYL have become impressively proficient at managing those risks, which is why they continue to specialise in West Africa, where many other industry players (who do similar work to LYL) would prefer not to work. This also means that LYL can and do charge a premium to compensate them for taking on those risks, so as long as they continue to manage those risks as they have done to date, that work will remain very profitable for them.

LYL work for some very big players like Barrick Gold Corporation - the world's second largest gold producer - LYL-Award-of-Reko-Diq-Copper-Gold-Contract.PDF [12-June-2023] as well as some very small players like the tiny (A$14.7m) Toubani Resources Inc. (TRE.asx), which is an ASX-listed and Canadian-listed gold exploration and development company primarily focused on the development of the Kobada Gold Project in Southern Mali (Toubani are HQ'd in Canada, not Australia, despite being ASX-listed) - Lycopodium-Appointed-as-Lead-Engineer-for-Kobada-DFS-Update.PDF

Lycopodium's Office Locations Globally:

Here's some of the projects they were involved in during FY23:

As you can see, most were in the Resources sector, but there were also some in Infrastructure and some in Industrial Processes. That is page 26 of their FY23 Shareholder Report, and they provide details of all of those projects on the pages listed above. I'll give you just one example - the CSL Seqirus "Banksia Flu Cell Culture Manufacturing Facility" Project - which is on page 40 of the report (as indicated above):

For details of the other projects, click on the link above to access the full report.

That'll probably do for tonight.

Pacific National, another LYL client.

Disclosure: Yep, I sure do hold LYL shares.

21/02/2024

Lycopodium (LYL) released another great 1H24 result today. This is a very high quality business operating in a cyclical industry. It is diversified and is starting to grow revenue in some less cyclical sectors, for instance: “Transformation of the global energy sector from fossil-based to zero-carbon sources represents a period of innovation and opportunity in the development of new systems that can operate on low carbon energy sources, whilst maximising waste recovery and reuse” (1H24 Presentation). However revenues are heavily skewed towards resources in Africa.

It’s a high quality business because currently it has a very high return on equity (38%). If you look at the presentation LYL say their ROE is 25.5%.

Here they are calculating their ROE as the 1H24 NPAT/ Equity. I questioned this in their previous results meeting and they agreed it was only calculated on the half. It needs to be calculated using full year NPAT. LYL reaffirmed guidance for FY24 to be $46 - $50 million. That looks a tad conservative too, given they’ve already achieved $30 million of that. @Bear77 would agree (since it will be in the top 3 companies on Strawman today) that LYL is just one of those quiet achievers that just plugs away doing marvellous things with your equity without crowing before the eggs are laid!

My calculation of ROE based on equity at the end of Dec 2023 ($127.1 million) and mid-guidance of $48million is 38%. This might not hold up through a depressed cycle so we need to keep a close eye on it. LYL generally pay out approx 70% (50% for this half) of their earnings in dividends, and the dividends are fully franked.

For FY24 I am expecting a fully franked dividend of 84cps (70% of guidance EPS, $1.21cps). That’s a forecast yield of over 6% fully franked, or 8.5% including franking credits.

Valuation

Turning to the valuation using McNiven Formula assuming ROE 38%, Equity $3.07 (Dec 2023) 30% of earnings reinvested, and requiring a return (RR) of 15% I get a valuation of c.$15 per share, the same as my previous valuation but now I feel the valuation is slightly more conservative. While the cycle is strong LYL should continue to do well.

Held IRL (3%)

14/11/2023

My valuation and justification remains unchanged from 3 months ago (see valuations at LYL). The last three months have panned out even better than I expected and today’s FY24 guidance confirms LYL is expecting continued growth which puts ROE to remain in excess of 40% over the next 12 months. The business is virtually debt free with $82.4 million of shareholders total equity of $113 million sitting in cash. Investors could expect dividends in FY24 to be between 9% and 10% fully franked (over 13% gross yield including franking credits). This is while it continues to reinvest 30% of earnings back into growth.

01/08/2023

Lycopodium said in its guidance update on the 11th April that in the final quarter it is “continuing to see a high level of activity across all operating sectors, delivering a robust order book of projects and feasibility studies across a broad geographic footprint. We are also seeing a strong study pipeline which bodes well for the future. This significant level of activity across all sectors of operation continues to translate into healthy financial performance. The Company now provides an updated guidance for the full financial year, with forecast revenue of $320 million and forecast net profit after tax (NPAT) of $45 million.”

What to expect for FY23:

- FY2023 NPAT of $45 million represents a 45% ROE, and is 67% up on last year (FY22 of NPAT $27 million)

- FY23 Net Profit Margin 14%

- FY2023 EPS $1.13 (80 cps FY22). FY23 PE 8.9 based on the current share price of $10.06

- Debt free

- $2.40 per share held in cash ($95 million cash, 39.7 million shares)

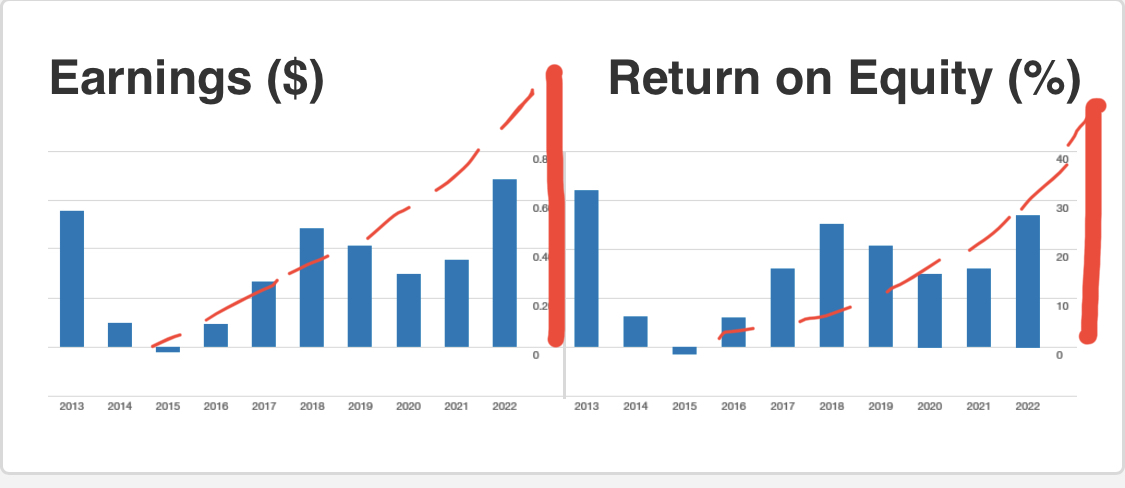

At 45%, Lycopodium’s ROE will be the highest in over a decade, and this is the seventh successive year where ROE has been higher than 15%.

FY23 Earnings and ROE represented in red (Adapted from Commsec data)

I don’t know of any other business which has zero debt, holds 24% of its market capital in cash, and at the same time is expecting ROE of 45%.

Source: Simply Wall Street

Shareholder equity is $2.60 per share of which $2.38 is held in cash and equivalents.

At $9.70, Lycopodium’s shares are trading close to their all time high of $10.60. In January 2016 shares were trading for $1.16, so along with it’s fully franked dividends it has realised excellent returns for shareholders over 7 years.

Dividends

At a historic payout ratio of 70%, the final dividend is likely to be over 40 cps, fully franked. The interim dividend paid was 36 cps, fully franked. Shareholders can expect a grossed up annual yield of circa 11% (including franking credits). There is plenty of cash sitting on the balance sheet, so there is also the possibility of a special dividend, a share buy back or an acquisition some time in the future.

Valuation

Over the last 4 years the average PE ratio has been 12.5 (calculated from Commsec annual average PE data). The current PE ratio based on FY23 earnings is 8.6, well below the historical average. Given business performance has vastly improved over 4 years (ROE has more than doubled), I think it is reasonably conservative to use an average PE of 12.5 for valuation. This makes Lycopodium worth over $14.00 per share.

Given the improving business performance I would prefer to use McNiven’s StockVal Formula for valuation. Assuming ROE continues at 40%, reinvested earnings 30%, equity $2.60, you could pay up to $12.50 and still get a 15% annual return (including franking credits).

Even though Lycopodium is trading near all time highs, I think it is excellent value at the current share price. At $9.72, you could expect an annual return of c. 18% including franking credits.

You could pay up to $17 and still receive an annual return of 12% (including franking credits).

I think Lycopodium is currently one of the best (if not the best) mining services businesses on the ASX. I’ve been adding shares below $10 and have lifted my valuation to $15 per share.

Disc: Held IRL (0.8%).

17/04/23

The Lycopodium share price has shot past my previous valuation of $10.00. Is it now overvalued? Not if you base your valuation on the updated guidance with NPAT expected to be $45 million for FY23. That will put FY23 ROE at 43% ($45 million NPAT / $103.5 million equity). That’s the highest ROE in 10 years, and possibly the highest on record for LYL.

Source: Commsec

Source: Commsec

Lycopodium is definitely in a sweet spot at the moment with ‘a high level of activity across all operating sectors, delivering a robust order book of projects and feasibility studies across a broad geographic footprint.’ The increased activity is driven by battery minerals, gold and copper. While we continue to see strong activity in these sectors we can expect LYL to thrive. I think we will see this across the board in other mining service companies also.

My previous valuation was based on a ROE of 35% and a required return of 15% p.a. I feel comfortable bumping the ROE for LYL up to 40% for an updated valuation. Still requiring a 15% p.a. return on my investment my updated valuation jumps to $12 (McNiven’s StockVal Formula). If you were happy with a 12% p.a. return you could pay up to $16 while ROE remains over 40%.

A caution though, this is a cyclical industry and at these share price levels it’s important to keep a close eye on future guidance and the health of the miners.

Disc: Held IRL (0.6%)

Feb 2023

Thanks @Scott for your 1H22 results straw and valuation. This is an excellent result for Lycopodium, and their best return on equity (ROE) in a decade (39%). Unfortunately, they did themselves a disservice in the presentation:

I asked MD Peter de Leo on the conference call this morning if this was based on the return for just 6 months rather than an annual ROE, which he confirmed.

Those who follow my straws would know that ROE is the first metric that gets my attention. I’m looking for businesses with a track record of consistently strong and preferably growing ROE. I try to find businesses with a minimum of 15% ROE and preferably higher than 20%. There are plenty of businesses with ROE higher than 20%, but most trade on high multiples of PE and PB.

Lycopodium is a quality business and has averaged ROE of between 15% and 25% over the past 6 years. This year ROE will be close to 40%. That’s the best ROE in a decade.

However, Lycopodium is also a cyclical business with over 90% of its revenues coming from resource companies. Earnings can fall away rapidly when the shine goes off mining.

None the less, it has a track record of high ROE, and I expect ROE to be in excess of 30% for a few years to come. With NPAT guidance of $40 million, or $1.00 per share, that puts LYL on a FY23 PE of 8.3X. How many businesses can you buy with a PE of 8 and a ROE of 40%. Not many!

If I use McNiven’s StockVal formula, assuming normalised ROE of 35%, a dividend payout ratio of 70%, franking of 100%, and a required annual return of 15%, I get a valuation of $10.04, say $10.00.

I don’t think this is a business you buy and hold for ever. Having said that I have held LYL for several years. The time to sell is when the pipeline of work with resource companies starts to dry up. The project pipeline for Lycopodium still very strong so it’s a strong hold for me.

Disc: Held IRL (0.6%)

LYL reported today.

No commentary but the +50% NPAT lift must be how some payments fell. Full year NPAT guidance is NPAT~$46 to $50 million which will be up from $47M for FY23. They have a history of under promising. Don't be surprised for it to come in at $55M which would be 14% growth. Current P/E is 10 before today's release. Share price is up 10% today at time of writing.

August 2018: LYL has already overtaken my previous price target. This ($5.45) is my new 6 month price target. They continue to perform well. . . .

Feb 2019: 12 month price target will depend on new contracts and commodity prices (esp. gold) which will in turn depend on what's happening in the world. Very hard to predict. . . .

Update: 31-Aug-19: Overtaken my updated PT. New PT = $6.77, based on quality management, quality company, and tailwind of higher gold price. . . .

29-Feb-2020: Update: Due to delays experienced across the industry with the timing of contract starts and new contract awards, it may take a bit longer for LYL to hit my latest $6.77 PT, so faced with new information, I'm reducing it back down to $5.80, which is a level I think they can reach over the next 6 months (by early September 2020) with a couple of reasonably sized new contract wins, and their usual outstanding performance on existing contracts.

29-Aug-2020: $5.80 is still fine for a 12-month PT. They went over $6 in Jan/Feb this year, and would have probably maintained those levels if it wasn't for the pandemic. LYL specialise in designing, building and optimising gold processing plants, and that's a great space to be at the minute. The downside is that they have traditionally done a lot of their work in Africa, South America, and other risky places to operate. Back here in Australia, GR Engineering (GNG) seem to get most of that work. Ideally I'd like to see the two companies merge, or LYL acquire GNG, but that may never happen. Would be good if it did tho... I hold both. GNG is a long term hold for me. LYL is a company I tend to buy when they look undervalued and sell when they look expensive. They look undervalued here (below $5) so I'm holding them.

LYL do a lot of other stuff also - not just gold plants. Have a look at their website for more on that.

They were originally (many moons ago) the engineering arm of Monadelphous (MND), which was spun out, and in recent years the two companies have formed a JV called Mondium which has been gaining traction, winning larger contracts each year. I also hold MND shares.

Update: 01-Mar-2021: This is another company that seems to be happy to sit at or around the price target that I set 12 months ago - $5.80 in this case, but I should acknowledge that prior to that it was $6.77 and I reduced it to $5.80. The $6.77 PT (in 2019) did not get taken out. $5.80 seems to be around the mark, and I would be raising it if gold was on a tear, but it ain't, so I won't. I think LYL will likely bounce around this level for a while, probably falling away on no news, then coming back up when new contracts are announced. I still hold LYL shares - and GNG shares. GNG had a corker of a day today, up another +5.84% to $1.45. Of the two, you'd have to say GNG has the far superior chart at this point - it's exactly what you want to see - all bottom left to top right at a very good clip. LYL is bouncing around their 12-month high but they don't have the same north-bound momentum that GNG currently do. I'm happy to be holding both, particularly GNG with their recently declared 5 cps fully franked interim dividend.

I'm leaving my PT for LYL at $5.80 for now, but will raise it if they break through $6 with any conviction. If they do that I think they're heading for around $6.70 by this time next year.

Update: 30-Aug-2021: Still happy with $5.80 for a PT for LYL, but that other former $6.70 PT for March 2022 might be a bridge too far from here (currently $4.75). LYL reported on 23-Aug-2021 and rose +4% on the day - from $4.61 to $4.80, but they haven't shot the lights out. GNG is looking better than LYL at this stage, and I do have significantly more invested in GNG than in LYL at this point. I have maintained a small RL position in LYL, but have a much larger one in GNG for their dividend - latest one is 7 cps (FF) for GNG, so their dividend yield is almost 6%, plus franking credits (12c/year FF). LYL have declared a 15 cps final div, so when added to their 10 cps interim dividend, they are on a 5.26% yield, plus franking, and LYL fully frank their divs also. Both do very similar work, however most of LYL's work is outside of Australia, and most of GNG's work is at home - within Australia, although not all. Both have liquidity issues due to being microcaps (LYL is < $200m, GNG is < $300m market cap) and having very high insider ownership. Holders are usually not interested in selling, so there can be precious little available to buy.

Their results can also be lumpy due to the shorter term nature of their EPC work, although GNG also have recurring revenue from their Upstream PS division - but check out GNG for further details on that - this is supposed to be about LYL. Both LYL and GNG have high quality management with heaps of skin in the game, both companies avoid debt and always maintain net cash on the balance sheet, both have excellent risk management strategies in place which clearly work, even when their clients get into financial difficulty occasionally and have trouble paying their bills. GNG & LYL have good track records of being conservative with their accounting and with their guidance, and collecting on their bad and doubtful debts more often than not.

LYL often work for larger companies on average than GNG do, although that is a generalisation and isn't always the case. I like them both, Two of my favourite engineering and construction companies. My other favourite in the space is MND - Monadelphous - but Mono's do other types of E&C to what Lycopodium and GR Engineering Services do. Mono's also have a variety of different divisions so they are much bigger with many more sources of revenue, including recurring revenue from multi-year operations and maintenance contracts. Of the three, currently GNG is performing the best, and MND is the safest, but LYL will have their day in the sun again one day. If they get back down to $4, I'll probably load up.

$7 is probably a good 5 year PT for LYL, so $7 by September 2026.

Update: 24-Aug-2022: LYL reported for FY22 today, and it was very good. All covered in various straws. They are now on a 9% dividend yield, or a 12.6% grossed-up yield (that includes the full value of their franking credits). Their FY22 dividends are more than double what they paid in FY21.

I am updating my valuation to $7.40 to reflect the significant growth the business has achieved in FY22 and the positive outlook they have for FY23.

Update: 23-Feb-2023: Six months on, and LYL have released one of the best half year reports I've seen this year, perhaps THE best one. I won't talk about it too much because it's been well covered in the straws and valuations by @Scott (see here) and @Rick (see here). However, this latest half year report by Lycopodium is a cracker. Particularly given the industry headwinds, especially around the pandemic and the associated recruitment and staff retention challenges experienced across the sector.

FY2023 H1 Results Announcement

FY2023 H1 Results Presentation

That's from page 1 of their announcement (link above) but I've added the percentage increases (in the green boxes, plus the green arrow) because they seem too shy and bashful to point out how well they've done. They're not big on blowing their own trumpet, this mob!

Their full year guidance of approx. $320m in revenue and $40m NPAT is simply double what they managed in the first half ($159.9m and $20m), so I have no doubt they will exceed those numbers, as they usually do. Underpromise and overdeliver. That's their MO. I hold LYL both here and in real life, and I always have high expectations of both LYL and GNG (who do the same stuff but with a more Australian focus, LYL specialise in West Africa and other risky places and they are very, very good at risk management), but LYL even beat my own high expectations sometimes. They are THAT good!

LYL closed at $7.64 on the 21-Feb-2023 (Tuesday), the day before they released these results, comfortably meeting my previous price target (set six months ago) of $7.40.

On Wednesday, on the back of these results, they rose +76 cents (+10%) to close at $8.40. Today (Thursday) they rose another 7 cents to close at $8.47. Based on their most recent full year dividend of 36 cps plus this one (another 36 cps), that's 72 cents per share per year now, which means their dividend yield is 8.5%pa based on today's price, and 9.4%pa based on Tuesday's closing price. Based on my average buy price (IRL) of $6.05 (yes, I've averaged up on this one), they're on an 11.9% yield, and that's not taking any of the franking credits into account. And their dividends are all fully franked. To get the grossed up yields (to include the full value of the franking credits, you can take those yields and multiply them by 1.42857 - or just add 43% more on.

That's a handy tip for anybody that wants to work out the franking credits they're going to get on a dividend. Work out the total amount you're going to get in the bank, and if that dividend is fully (100%) franked at the 30% corporate tax rate, you can use the following formula:

30 / 70 x X

where X is the full amount you're going to receive in the bank, "/" means "divided by" and "x" (the small x) means "multiplied by".

If the dividend is coming from a small LIC (like SNC) or any smaller company who qualifies for the lower 25% tax rate, you would use this formula:

25 / 75 x X

The first two numbers in the formula always need to add up to 100 for the formula to work. The first number is the corporate tax rate that applies and the second number is 100 minus the first number. The reason you can't just add 30% to the amount you're going to receive is that a fully franked dividend includes the tax payable on the entire value of the dividend and the franking credits, because the franking credits count as both income and a tax credit, so they have to cover the tax payable on the franking credits plus the amount you're going to get in the bank, which usually works out to 42.857142857% or 30 / 70.

That formula gives you the dollar value of the franking credits you're going to receive. If the dividend is only 85% franked, you would add "x 0.85" to the end of the formula, so for MFG's latest dividend the franking credits would be:

30 / 70 x X x 0.85

For Altium's latest dividend, which is 40% franked, you would change the 0.85 to 0.40 (or just 0.4 or even .4, as the extra zeroes in this case are superfluous).

30 / 70 x X x 0.40

So - if you held 8,000 LYL shares, you would get $2,880 (being 8000 x 0.36) in the bank on the 6th April, plus $1,234.28 in franking credits (or $1,234.29 if they round to the nearest cent instead of ignoring everything after the second decimal place). That $1,234.28 is:

30 / 70 x 2880

Anyway, sorry about the excruciating level of detail (helpful no doubt to some, very obvious to others), but that is all to say that LYL were on a VERY good dividend yield before these results, and they still are, even with the share price rise we've seen this week.

And while they are certainly a good income stock, they are also a growth stock. Their core revenue is lumpy by nature - being one off engineering, procurement and construction (EPC) contracts, often with an "M" tacked on - meaning that they manage the projects as well, but they keep winning more and more work. Some of their more recent work has not included the "C" - it's been "EPM" work, so Engineering, Procurement and Management of projects, especially some in West Africa. That, no doubt, is also part of their risk management. They will often let others do the actual boots-on-the-ground construction in these higher-risk areas of the world, and get paid very well for designing the plant, procuring all the parts and equipment and material required to build it, and managing the whole process.

But that better belongs in a Bull Case straw I suppose. Superior management who are exceptional at risk management in some of the more risky parts of the world to build gold plants.

However, as their presso points out, they are active in a number of industries, they have more than one string (gold plants) to their bow, and they just keep on delivering for their shareholders. I plan to buy more soon once one or two of my other companies goes ex-div.

And they do a lot more than just gold plants of course, like Lithium...

https://www.lycopodium.com/case-studies/

https://www.lycopodium.com/what-we-do/

https://www.lycopodium.com/about-us/our-story/

27-Aug-2023: Update: After FY23 full year results in August:

Raising my price target for LYL to $11.88 (from $9.70 - which they've already reached and passed).

Source: LYL-FY2023-Full-Year-Results-Announcement-22-Aug-2023.PDF

See also: LYL-Investor-Presentation-FY2023-22-Aug-2023.PDF

Souurce: Commsec (trend lines added by me).

Not growing in a straight line all of the time, there are pullbacks, but the overall trend is up and the growth has been substantial.

Current 12m trailing dividend yield is 7.9% plus franking, and all of their dividends have been fully franked. That's a grossed-up trailing yield of 11.2% (including the full value of the franking credits).

And we have share price growth as well:

Source: Commsec (as at Friday 25th August 2023, showing Friday's price movement (-1.72%) at the top.

Disclosure: I continue to hold LYL shares (both here and IRL). Liquidity is still an issue, however it's a great place to park some patient money and watch it grow and produce income at the same time.

03-March-2024: Update: Raising my PT for LYL from $11.88 to $14.25, as they've already shot past my previous price target. They keep on underpromising and overdelivering. Here's their H1 of FY2024 results summary table:

As usual, they did NOT provide any percentages - I've added those (above) on the right side of the table. The cash fluctuates depending on progress payments, completion payments, and so forth, so I'm not fussed about the cash levels - they move up and down a lot, but they always have plenty of spare cash - they are, after all, a small company with a sub-$500m market cap, so $69m of net cash is plenty.

Here's page 1 of that results announcement:

And here's a link to the full announcement: Lycopodium-Half-Year-Results-Announcement.PDF

And to their results presentation for the half: 1HFY2024-Investor-Presentation(LYL).PDF

And below is a share price comparison of LYL, GNG and MND against the S&P/ASX200 TR (total return) Index (XJO) - Lycopodium, GR Engineering and Monadelphous all being quality ASX-listed engineering and construction companies that I hold in real money portfolios (and I also hold two of them here on Strawman.com):

GNG has done OK, but LYL is powering ahead now. Happy to be holding. They're growing at a good clip, they are very profitable, they pay excellent fully franked dividends, they have high insider ownership (great alignment of interests between management and ordinary shareholders), they have superb industry position, they are very well run, and the management like to underpromise and then overdeliver. Not very much NOT to like! And LOTS to like!

Lycopodium released its FY23 AGM Presentation this morning. Sandwiched in the middle of the presentation was a slide titled “Current Snapshot” which contained FY24 Guidance:

How does this compare to FY23?

Management expect FY24 Revenue to be $345 million which would be up 6.5% on FY23 revenue of $324 million.

Management expect FY24 NPAT to be flat to 7% higher than FY23 NPAT of $46.8 million

Importantly, FY24 ROE should remain between 40% and 44% which is exceptional, particularly when you consider LYL has a lazy $82.4 million of the $113 million in total shareholder equity sitting in cash.

LYL is obviously building some sort of ‘moat’ around their expertise to be increasing ROE every year to this level without the need for leverage and with so much lazy cash sitting almost idle on the balance sheet. Since 2020 LYL has definitely landed in a sweet spot, and this looks set to continue into the near future.

I also like that LYL management are very forward thinking and try to seperate themselves by focusing on a unique suite of specialised engineering and professional services rather than trying to compete in the mainstream. The slide below is an example of how management is always thinking forward to stay ahead of the pack.

As @Bear77 has already mentioned LYL is also diversifying away from their heavy reliance on expertise to the Western African gold mimers, which @Bear77 pointed out is an area where they are also specialists in the field of electrical engineering.

As @Bear77 has already mentioned LYL is also diversifying away from their heavy reliance on expertise to the Western African gold mimers, which @Bear77 pointed out is an area where they are also specialists in the field of electrical engineering.

This slide demonstrates LYL have several irons in the fire, and are are carving out a unique niche in each. I’m liking this business more each year, and have continued to add more shares to our portfolio.

Better leave something for @Bear77 to talk about!

Disc: Held IRL (2.6%)

Today (Friday 22nd December 2023): TWO New Contract Awards:

[Award of the Engineering, Procurement and Construction Management (EPCM) Services and reimbursable Supply contract for the process plant and associated non-process infrastructure for FG Gold Limited’s (FG Gold) Baomahun Gold Project in Sierra Leone, advancement of the project subject to FG Gold attaining financial close. The contract includes detailed engineering, procurement of equipment and materials, construction management, preoperational testing, and commissioning. This EPCM Services and Supply contract is valued at approximately A$100 million, with work anticipated to commence in Q1 2024.]

[Award of the Engineering, Procurement and Construction Management (EPCM) services contract for the Yanqul Copper Gold Project in the Sultanate of Oman, being developed by Mazoon Mining LLC (MMC), a subsidiary of Minerals Development Oman SAOC (MDO), the flagship mining group in the Sultanate of Oman. This EPCM services contract is valued at approximately A$45 million. It is anticipated works will commence in Q1 2024 and conclude in Q2 2026.]

Friday 11th December 2023:

[LYL were awarded a Contract from Barrick Lumwana for the Feasibility Study and Basic Engineering for the expansion of Barrick’s Lumwana Copper Mine in Zambia, valued at approximately A$19 million, with the project having a capital cost investment of almost US$2 billion. Work has commenced, with the accelerated development program targeting completion of the Feasibility Study by the end of 2024 and expanded process plant production anticipated in 2028. It pays to note that studies like this FS (feasibility study) and basic engineering contracts often lead to larger EPCM contracts like the ones above announced today.]

Further Reading: 14th November 2023 AGM Presentation: PowerPoint Presentation (lycopodium.com)

Disclosure: I hold LYL in three of the four real money portfolios that I manage and I also hold them here in my Strawman.com virtual portfolio. They are a high conviction holding. The only reason they are not in my fourth real money portfolio (my SMSF) is because they are not yet in the ASX300 Index, which is a prerequisite of the industry super fund (CBUS) that I use for my SMSF. If I could add them to that portfolio, they'd be in there as well.

See also: https://strawman.com/reports/LYL/all

And:

https://fggoldmining.com/projects/baomahun-gold-project/

And:

https://www.omanobserver.om/article/1139784/business/economy/revenues-of-ro-500myear-seen-from-key-oman-copper-gold-mining-project [08-July-2023]

And:

https://www.lusakatimes.com/2022/10/31/barrick-hoping-to-extend-lumwana-mine-to-2042/ [31-Oct-2022]

Source: Facebook

Source: BARRICK GOLD TO EXPAND LIFE OF LUMWANA MINE ~ (znbc.co.zm) [8-July-2023]

Source: Mining Weekly - Lumwana copper mine expansion, Zambia – update [15-Dec-2023]

https://www.reuters.com/markets/commodities/barrick-ceo-says-zambias-lumwana-mine-life-could-be-extended-2060-2022-10-26/ [27-Oct-2022]

Barrick to spend $2B on Lumwana expansion - Mining Magazine [04-Oct-2023]

Lycopodium just released a very pleasing FY22 results announcement. I couldn’t find the percentage improvements over last year, so I made a few quick calculations below the table:

Revenue +43%

EBITDA +71%

NPAT +92%

EPS + 92%

Cash +31%

…and a nice juicy ROE of 29% which puts LYC back on track with the good ol’ days of 2013!

Outlook:

Given the general outlook and level of committed work, we expect our financial performance in FY2023 to be broadly in line with that achieved in FY2022. We do however undertake to provide further revenue and profit guidance as part of our Annual General Meeting update in November.

A quick valuation on my StockVal spreadsheet puts the valuation up to approx $12 after lifting ROE from 20% to 29%. This was quick and dirty as I still need to rework 2022 equity values, payout ratios etc. I’m just after a ball park for when the market opens.

Disc: Small holding IRL (0.4%)

24-Aug-2022: As I said in my "Strategy & Outlook" straw for Macmahon (MAH) early this morning (about 2am), the Lycopodium (LYL) result was going to be good. It was. You can view the "#Great FY22 Result" straw by @Rick here: https://strawman.com/reports/LYL/Rick?view-straw=19458 and a "#Management" straw by @Scott here: https://strawman.com/reports/LYL/Scott?view-straw=19464

@Scott has also updated his valuation for LYL: https://strawman.com/reports/LYL/Scott

I think their dividend increase was well hidden in their announcements and presentations, it was certainly not highlighted by them, but it's definitely one of the major positives, and there were a lot of positives.

As I said last night (or early this morning), I hold LYL in a portfolio that is structured partly to provide a decent income stream, and LYL are certainly contributing to that. A dividend yield of 9%, and a grossed up yield (including the full value of the franking credits) of 12.6%. And there's capital growth as well, because the company is growing revenue, profits, EPS, etc. at a very decent clip. There's a LOT to like about Lycopodium. $100m cash in the bank. 29% ROE. 39% of the company is owned by their Board and Management. Lots of skin in the game and terrific results.

Investor Presentation - Full Year Results FY2022

FY2022 Annual Financial Report

FY2022 Full Year Results Announcement

Investor Relations | Lycopodium

Lycopodium Limited | The Science of Engineering, Maximising Commercial Value

They are the quiet achievers. They just get on with the job and deliver. No promotion, no blowing their own trumpet, no fanfare, just brilliant management and a wonderful company that does everything right.

Disclosure: I hold LYL shares.

asx:LYL

asx:LYL24-Feb-2021: 1HFY2021 Half Year Results Announcement plus Interim Financial Report 31 December 2020

and: 1HFY2021 Investor Presentation

Lycopodium Records Solid Start for FY2021

Lycopodium Limited (ASX: LYL) has delivered a solid result for the first half of 2021, with net profit margin remaining strong, at 8.8%.

For the six-months ended 31 December 2020 (“1H FY2021”), the Company generated revenue of $71.0 million and net profit after tax (NPAT) of $6.3 million.

The company Directors have approved a fully franked interim dividend of 10 cents per share, payable on 8 April 2021.

Lycopodium’s Managing Director, Peter De Leo, said: “The first half of this financial year has been very positive, with the successful completion of Perseus’ Yaouré Gold Project in Côte d’Ivoire in December, ahead of schedule and under budget despite the challenges presented by COVID-19, and the recent award of two substantial African resource projects.”

In December, the Company was awarded the contract to provide Engineering and Procurement (EP) services for Sandfire Resources’ Motheo Project (T3 Copper-Silver Project), located in Botswana’s Kalahari Copper Belt, one of the world’s most exciting and emerging copper producing regions. This followed the earlier completion of the Definitive Feasibility Study (DFS) and Front End Engineering and Design (FEED) for the project.

In early January, Orezone Gold Corporation awarded the Company the contract to provide Engineering, Procurement and Construction Management (EPCM) services for the delivery of its Stage 1 Oxide Process Plant for the Bomboré Gold Project in Burkina Faso. Again, this award comes on the back of earlier works completed on the project, including the initial study work and FEED, undertaken out of Lycopodium’s Toronto office.

“Our ability to convert initial study and engineering works into project delivery is testament to the strong client relationships we have established and our clients’ confidence in us,” said Mr De Leo.

Having successfully completed its largest EP(C) contract to-date in 2020, being the Yaouré project, the Company has maintained its strong safety performance, with a Lost Time Injury Frequency Rate (LTIFR) of zero for the rolling 12 month period to January 2021, against 2.5 million manhours controlled.

“Delivering projects safely for our clients remains a fundamental metric of success and our excellent safety performance is a credit to our delivery teams on the ground,” said Mr De Leo.

While COVID-19 continues to influence economic confidence globally, impacting project commencements, the forward outlook is considered positive, with a strong pipeline of opportunities identified. Based on the anticipated timing of new projects commencing, the Company provides guidance for the full year of approximately $160 million in revenue and NPAT in the order of $12 million.

“Our focus will continue to be on working in partnership with our clients to enable them to progress their projects to completion, on time and budget,” Mr De Leo said.

--- end ---

[I hold LYL shares. 71% of their H1 revenue came from Africa, and particularly West Africa, and 24% from Australia. In the pcp (prior corresponding period, being the 6 months to 31-Dec-2019) it was 79% from Africa and 16% from Australia. They do the same stuff that GR Engineering Service (GNG) do, except usually on a larger scale and for larger companies, and mostly overseas. Both GNG and LYL are WA companies based out of Perth and both specialise in designing and building gold processing plants, after doing the studies (PFSs, DFSs and BFSs, being Pre-Feasibility, Definitive Feasibility and Bankable Feasibility Studies). Both also work for other industries, meaning other miners and in other industries outside of the resources industry, but with both LYL and GNG it is working for gold miners that provide their main source of revenue. I like them both for a pick-and-shovel-play on gold. When they are flying, as GNG are starting to again now, their dividends can also be quite good, market-beating in fact, i.e. above average, although revenue and therefore dividends can be quite lumpy at various times.]

19-Nov-2021: Lycopodium, once the engineering arm of Monadelphous many moons ago, and involved in a JV with Mono's again now (called Mondium) have seen a decent share price move since they held their AGM yesterday. They closed up +7.4% today at $5.21, after having risen +1.8% yesterday. They closed at $4.44/share on Wednesday, but have finished the week at $5.21, some +17.3% higher. I do hold LYL shares (and MND shares). I also hold GNG shares. GR Engineering (GNG) and Lycopodium (LYL) both specialise in designing and building gold processing plants. That's their specialty, although both also work with other commodities and in other industries. GNG do most of their work in Australia, and LYL do most of theirs in Africa. The following shows LYL's breakdown of revenue by sector and geography:

With 90% of their work coming from the Resources sector in FY2020 and 87% in FY21, it is certainly the main game for Lycopodium:

However, I believe their infrastructure division is underappreciated and has plenty of potential:

And they also do other stuff, like working for CSL, on facilities for base vaccine component production, and on plasma and blood product production facilities...

LYL ticks a LOT of boxes for me. Firstly, they are a company that is solving a problem, i.e. providing services that are clearly needed and are in demand, and what they do is something that I understand - i.e. engineering, design, procurement, construction, and management (including construction management) - so EPC/EP(C)/EPCM work.

They work in sectors that I understand, and sectors with good tailwinds for the most part too. And they are GOOD at what they do, hence they win a lot of repeat work from clients.

They have a top notch Board and Management team, with plenty of skin in the game, so their interests are aligned well with ordinary retail shareholders.

41% of the company's shares are held by their Board and Management. 30% is held by Insto's, leaving only 29% for the rest of us (retail investors). They can go nowhere for months and then have quite big moves (like today), on relatively low volume often, because of that lack of liquidity. They are a microcap (currently just under $200m market cap) company with a small free float, so they can be very thinly traded. On the 2nd and 4th of this month (November 2021), less than 1,000 LYL shares traded over the entire day. The volume for those two days was 299 and 573 shares respectively. While they did move up +7.4% today, that was on volume of only 32,886 shares. That's 32 thousand shares, not 32 million shares. They are very illiquid. And I do like that as well. It means you can quite often pick up shares at low prices when there is no good news and people aren't interested in buying them.

I also like their solid balance sheet, with minimal debt, and the reasonable ROE.

They have their "Mondium" JV (joint venture) with MND (Monadelphous Group) which tackles some fairly large projects, like this one for RIO:

But what they do best, in my opinion, is design and build gold processing plants, on time, and on budget, even during a global pandemic, like this one:

That's the Yaouré Gold Project in Côte d'Ivoire that Lycopodium have just delivered for Perseus Mining (PRU). They won that project award after successfully delivering the Sissingue gold project for PRU, and then completing the definitive feasibility study (DFS) and the front-end engineering and design (FEED) for Yaouré. I don't like investing in gold miners who work only in or predominantly in Africa or some of the other less stable and less predictable parts of the globe, however I do admire Lycopodium's track record of successful project delivery of gold processing plants in Africa. I guess their involvement is usually at the front end of a project's life cycle, and the "sovereign risk" issues tend to pop up further down the track, after the gold plant has been in production for a year or three and the local government wants a larger slice of the pie. When the excrement does hit the air blower, LYL are usually elsewhere working for someone else. Such is the nature of shorter-term contracting work. And that is clearly a risk worth mentioning. It can be a long time between drinks - in terms of very large projects, however I have found that both LYL and GNG have managed to diversify their revenue away from purely gold miners in recent years and have navigated through a variety of different operating conditions with aplomb, i.e. apparent ease. It hasn't stopped them being sold down on occasion, but GNG is now flying, and LYL are just taking off it seems.

But then, with their liquidity issues, it can be hard to tell. Probably need to wait until LYL get over $6 with conviction to call an uptrend. Those charts are over 5 years, and over 10 years the picture looks different, as LYL were trading at over $6 (and up to $7.31) in 2012. Still, as a gold bug myself, and a holder of both GNG and LYL shares in one of my real life portfolios (my income portfolio) - and also here in my SM portfolio - It's good to see the positive SP movement. And the great dividends continue as well. Based on their closing share prices today, the trailing yields for GNG and LYL are 6% (5.97%) and 4.8% respectively, PLUS franking, and both are paying fully franked dividends, so the grossed up yields are even higher. If you can handle the lack of liquidity, and the lumpy nature of a large part of their annual revenue, there is a lot to like about these two little engineering companies. I'm not sure I'd be buying much more GNG up here, but LYL could well have further to run.

Disclosure: I hold LYL, GNG and MND shares.

Further Reading (source of graphics/images used in this straw, other than the Commsec charts): Lycopodium 2021 AGM (18-Nov-2021) Presentation

Further Presso's: Presentations | Lycopodium

Case Studies: Case Studies (lycopodium.com)

Website: Lycopodium Limited | The Science of Engineering, Maximising Commercial Value

27-Aug-2023: Yesterday I highlighted GR Engineering Services (GRES, GNG.asx) and their income and growth history and future prospects. Today it's Lycopodium (LYL.asx).

So there's the income - LYL's current 12m trailing dividend yield is 7.9% plus franking, and all of their dividends have been fully franked. That's a grossed-up trailing yield of 11.2% (including the full value of the franking credits). The trend here is also your friend. Their dividends are increasing along with their revenue and earnings. Their revenue and earnings can be lumpy due to the one-off nature of much of their project work, however their downtrends don't seem to last long, and the overall trend is up.

Here's their interim results summary released in Feb for the 6 months ending Dec 31st, 2022:

And here's their full year results published last week for the 12 months ending June 30, 2023:

Source: LYL-FY2023-Full-Year-Results-Announcement-22-Aug-2023.PDF

See also: LYL-Investor-Presentation-FY2023-22-Aug-2023.PDF

And we have share price growth as well:

And here's that graph I showed yesterday in the straw on GNG that highlights the return from the same amount invested in GNG, LYL and the All Ords Index 10 years ago:

GNG has returned 6.6 x the All Ords Accumulation index, just in share price appreciation, with all the fully franked dividends on top of that. LYL has returned 3 x the All Ords return, plus dividends (dividends are already included in the green line coz the XAO is the All Ords Accumulation index which assumes all dividends are reinvested back into the underlying companies whereas the Blue and Orange lines for GNG and LYL do NOT include dividends).

The thing to note however is that LYL are really hitting their straps at this point in time, with rapid revenue and earnings growth, big dividend rises, and big share price movement to boot. GNG have done it more consistently, however LYL are catching up now.

Both companies do similar work, with both specialising in the design and construction of gold processing plants (mills) and both also do other commodities as well as gold, and both have other divisions as well with their Mineral Processing Engineering & Construction division being their main revenue driver. That project work is lumpy, but they're both very good at it and they are usually busy. Both companies have very high insider ownership as well.

In LYL's case, it's 36% Board and Management ownership, and a notional 39% free float, but they're just as illiquid as GNG are, so selling a heap of shares in a hurry will almost certainly move the share price, and it could be by quite a bit, depending on how many you need to sell and how fast. Once again, suitable for patient money.

You can see there that their market cap is very similar to GNG and they actually have a similar amount of cash in the bank ($82.4m vs GNG's $86m at June 30th), however LYL, unlike GNG, do actually have some debt, and it's a trade-off, because while they have manageable debt, they are also growing faster and have a higher ROE (44%). They are more profitable than GNG are.

They are also more global, with more full-time employees than GNG and with more offices that they work out of. They do a lot of work overseas, especially in Africa, and particularly West Africa, where there are more risk factors to consider, but LYL have become very good at that. More on that in a minute.

OK, now to their revenue sources, first by sector and then by geography:

The first slide shows little change from FY22 to FY23, however the "...by Geography" slide shows that they are relying less on Africa (in FY23 vs FY22) even though over half of their revenue is still derived from work done in Africa. Another way of looking at it is that they (Lycopodium) are now getting more work here in Australia.

The majority of GNG's revenue is derived from work here in Australia, although they do work overseas as well, just less than LYL do. Most of LYL's work is done overseas or else for clients who have mines/processing plants located overseas, and that's mostly still in Africa, and in West Africa in particular.

The next slide slows you the status of their major projects, and also gives you a fair idea of what commodities they are into; it's mostly lithium, gold and copper to a lesser extent, as well as mineral sands.

The next slide shows you the total of all projects and studies that LYL are working on currently, split into commodities, and we see that Diamonds/Gems feature now as well (below), although not in the previous slide - which was just their "Major" projects - so we can assume that those Diamonds/Gems Projects and Studies are smaller in nature. I do note that "De Beers Group" is listed as one of LYL's clients (two slides up from here).

Finally, the Outlook and Strategy slide:

OK, so that's just 12 slides from the deck of 26 - you can view the entire deck here: LYL-Investor-Presentation-FY2023-22-Aug-2023.PDF

I recommend having a look at slides 16 through 18 on "Business Improvements" and "Innovative Thinking", and also slides 12 through 14 on Lycopodium's FY23 Operational Highlights Details.

If you're interested.

Summary: Lycopodium (LYL) is a microcap that has low liquidity (not too many buyers or sellers much of the time and often substantial gaps between the price points of both the bids and the offers, and more often than not a reasonable gap between the highest bid and the lowest offer) that is suitable for patient money that is looking for income plus growth. The company is highly profitable (ROE of 44%), paying very good dividends (which are growing), and the business is growing at a good clip, and is well managed by a Board and Management who own 36% of the company - which provides good shareholder alignment which usually results in positive shareholder-friendly outcomes (such as good total shareholder returns).

Their revenue is diversified across commodities and across geographies, and they are expanding their offering beyond traditional engineering and construction project work.

One feature I have noticed is that a couple of recent contracts (in the past year) have been EPM contracts rather than the traditional EPC or EPCM contracts. E=Engineering. P=Procurement (sourcing everything needed for the project to be constructed and commissioned). C=Construction. M or PM=(Project) Management. So with an EPM contract (sometimes called an EP and PM contract), LYL do the design (E), procurement (P) and they manage (M) the project, but another company does the actual construction work, usually a local company that is based (HQ'd) in the country where the project is being constructed. This is likely another form of risk management. Use a local company to do the actual construction work, employing locals, and LYL manage the whole process and clip the ticket on everything. One example of where they have done this is with the Goulamina Lithium Project in Mali - see here: Award-of-Contract-for-the-Goulamina-Lithium-Project.PDF [14-Nov-2022]

Anyway, while a lot of their work is one-off project work, so their revenue and earnings will be lumpy at times, they are very good at what they do, and the industries that they work in recognise that, so I have good reason to think they'll stay busy and keep growing.

They don't overpromise and then undeliver; they give conservative guidance and then try to beat it, often positively upgrading their guidance as the year progresses and then still beating it on at least one metric.

Disclosure: Of course I do hold LYL (and GNG) in my real life portfolios as well as here on SM.

Further Reading:

Our Story | Lycopodium Limited

What We Do | Lycopodium Limited

Our Engineering and Project Management Principles | Lycopodium

Where We Work | Lycopodium Limited

Investor Relations | Lycopodium