Bear case from none other than Respeculator. Commenting on where NextDC can find the energy supply to provide the GW

I only follow him mainly because of his mathematical mind.

https://twitter.com/respeculator/status/1762713738296414378

I'm not sure how correct this is as I don't know enough about the energy marketplace.

I'm sure NextDC can find some source by constructing a few solar panels/wind turbines near their Data Centres? :)

Some interesting observations recently.

At 31st December 2022 ---> NextDC contracted Utilisation was 84.2MW ( It took 10 years for NextDC to sell 84.2MW)

From 31st December to 12th April ( NextDC sold another 35.9MW in 4 months, Remember it took 10 years to sell 84.2MW)

From 12th April to 23rd August ( NextDC sold another 25MW in 4.5 months)

What has changed? in just 8 months, NextDC almost sold 61MW capacity.

The following article resonates with me. Have a read

NextDC is raising equity for global expansion into the Asia Pacific.

Not surprisingly the share price has held up quite well despite the discount (10.80)

Thought I'd start the discussion as no one else had discussed it.

So is the share price expensive?

Using the Real option method by Damodaran and assigning a higher prob of success versus failure because of better management and also being a top ASX listed firm.

Think this might be a good raise and maybe better than AMI. Again not advice and my figures could be wrong. Personally I'm waiting till the entitlement raise is over and see how the share price behaves.

For anyone who is interested and has time and love maths and probability, you can read the paper by Damodaran here

NextDC reported it that the company's contracted utilisation has increased by 35.9MW to 120MW since 31 December 2022. That is massive number for half year and explains that they must have been chasing this big customer win since last 2 years.

To compare the scale of this number have a look at this graph

Now, Amazon have said that it plans to invest in its AWS business in Sydney and Melbourne from 2023 and 2027

https://www.manmonthly.com.au/aws-invest-13-2-billion-australian-cloud-infrastructure/

So you can guess who the customer may be. ( its just a speculation on my part )

This is going to be short squeeze in my opinion

Let's see what happens in the next few weeks.

$NXT reported results yesterday that were broadly well-received by the market. Expansions, site acquisitions for new data centres, and expectations of material new contracts supported this long term growth story. Analysts reactions are broadly positive, with no major moves to SP targets based on the updates so far. (Although GS tweaked down their 12m TP from $13.60 to $13.30)

I've had exposure to the data-centre theme IRL for several years ($NXT, $MP1) and continue to see it as a long term growth theme.

However, I have recently switched my RL position from $NXT to $MAQ, and I'll briefly explain here.

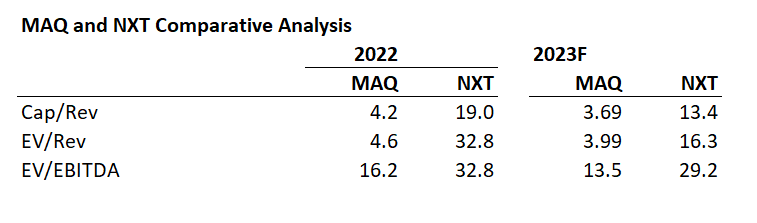

$NXT is a more agressive growth play, with 3-year revenue CAGR to end FY22 of 18% vs. 8% for $MAQ, and a 3-yr EBITDA CAGR of 26% vs, 19% at $MAQ. However, this is at the cost of significant debt, with long-term borrowings now reaching $1.26bn and interest for the last 6 months now up to $62m (annualised).

On a comparative basis $NXT is spending 32% of EBITDA on interest, compared with a more conservative 12% at $MAQ.

Furthermore, $NXT have recently signalled an intention to expand internationally, although we are yet to see what this means in practice. This further increases the risk profile.

Looking at valuation multiples, $MAQ is looking favourable, and I have initiated my RL position recently at $55.50 (2.75%). (I will follow today in SM, because strictly speaking these companies are "yet to prove themselves", which is my criterion for holding in SM.)

Table 1: Comparative Valuation Multiples

Source: www.marketscreener.com; Company Accounts

Overall, with interest rates still rising (and the real chance that peak forecasts will go up further) and with tech companies reducing investment in new storage, this sector may move from a focus on expansion to a greater focus on utilisation and profitability, with consequence implications for pricing.

Overall, while I like both $NXT and $MAQ, I consider that $MAQ is more defensively positioned given these risks. I have been watching it for several years, and with the SP below $60 I feel now is the time to switch horses.

$MAQ brings some other differences to $NXT as follows:

- It is founder-led, managed and majority owned

- The limited free-float means that it is not as easily accessible to institutions; however, liquidity is fine for a retail investor

- Its capital structure is different with a higher proportion of capital leases vs. owning real estate.

I don't often switch horses within a sector and, while I think BOTH companies will generate long-term shareholder value, I now prefer the risk-reward profile of $MAQ. So, out with $NXT and in with $MAQ.

Disc: $NXT - not held; $MAQ - held IRL (and later today on SM)

P.S. For those who follow Gaurav Sodhi, you'll recognise I have adopted his rationale. I have been aware of his perspective for well over a year, and on this occasion my analysis aligns with that story. You can look it up by watching back issues on "The Call" - just search for $NXT and $MAQ and pick the days when he the "talking head".

Mega trends

Macroeconomics conditions

Move to Cloud has just begun

Data

SC1 is live and ready to welcome customers

S3 is open now

M3 is close to complete now

US Hyperscalers have reported mouthwatering growth in Cloud business and the growth forecast for cloud computing isn't slowing anytime soon. that bodes well for NextDC.

Few questions - is NextDC in a position to pass on inflation to these hyperscalers or suffering margin squeezed? Is there any signed contract NextDC holds for all these new capacities it is about to open for customers? Has overseas expansion on the card? What's the plan for going free cash flow and future investment?

NextDC is a data center services company. There is definitely a tailwind for its services. All Cloud migration, business digital transformation, and abundant data that everyone generates need home.

There is a number of players already exist in the market e.g. Equinix, Airtrunk, Rackspace, MAcquire Telecom etc

NextDC is well placed and ahead in the Australian market compare to other providers - It's financial is sorted - last November it renewed its debt facility.

If you ignore new investments, NextDC is already cash-flow positive at the operation level. The following graph illustrates how much operating cash it generated from FY2015.

Currently, NextDC has 98 MW capacity and current investment is to increase its capacity 4 times i.e 400 MW

Each 1 MW currently generates 4m in revenue.

The following two case studies were done during the FY21 presentation, which illustrates How a single DC generates ~75% EBITDA at a mature stage.

Now Do you think that there will be enough demand for data centers in the next 5 to 10 years? Wou7ld NextDC be able to capture that demand? Would NextDC will be able to fully utilize it's 400 MW capacity in the future? If answers to these questions are yes or highly likely then NextDC is too cheap currently - as at that stage it will be gushing cash like a machine.