Interesting write up on changes to Macquarie’s lending practices arising from the removal of negative gearing:

Might be a tough time ahead in the short term for borrowers with LVRs greater than 90%, especially those who are paying the bare minimum repayments.

I think Chris Kohler nailed it with his recent post

https://www.facebook.com/share/r/1CiWDrSzwZ/?mibextid=wwXIfr

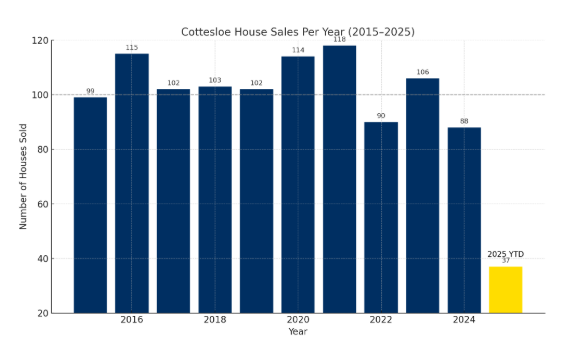

Something interesting I've come across looking at some property stats recently.

Annual house sales in Cottesloe over the last 10 years, annual Long Term Average is 100 and change. Currently, year to date is 37.

Tight tight tight

Cottesloe often is one of the suburbs which leads the pack up and down and is the canary in the mine for many movements.

In the absence of any world changing black swan events, the media are going to be having a field day in the coming months about growth...

Another monthly contribution in an industry I work in. Hopefully some analysis from my side assists someone with their decisions...

Contributing to the conversation with what I can!

After what’s felt like a stop-start few months, the Perth property market is finally getting a bit of clear air. The school holidays are done, public holidays are out of the way, and the Federal election is behind us. With those distractions easing off, we’re seeing momentum return to the market, and the general sentiment right now is pretty simple: just get on with it.

This week’s 0.25% rate cut from the RBA, the second in this current easing cycle, is a welcome sign. While it won’t have an immediate, dramatic impact on borrowing power, it signals that inflation is softening and the economy’s cooling just enough to give the RBA confidence to ease the pressure. For property investors, that’s key, because confidence and clarity are the fuel for decision-making.

In practical terms, we’re already seeing increased activity, especially around well-priced, well-presented homes. Perth continues to offer a compelling value proposition compared to the eastern states, and with rental vacancy rates still sitting incredibly low, yields remain strong. That combination of affordability and return continues to draw interest from both local and interstate investors.

From the conversations I’ve been having with clients, the shift in sentiment is clear. We’ve moved from a “wait and see” mindset to a “let’s make it happen” one. Buyers and sellers are becoming more realistic and more decisive.

The truth is, while the market isn’t running hot like it was a couple of years ago, it’s steady, active, and full of opportunity. There’s less panic, less noise, and more room for strategic moves.