I fired chatgpt, and hired claude (for $0). I fed it my rules for investing file, the quarterly report, and my RKT thesis, research details, and this is the short version of what popped out.

What Happened This Quarter

Revenue was $2.47 million, flat on Q4 but up 49% year-on-year. Flat sequential revenue is worth examining: the increase in recurring xBot revenue (up 73% QoQ) was offset by lower one-off hardware and project revenue, which the company characterises as normal volatility in the hardware sales cycle. This explanation is credible — the underlying recurring base is growing, and one-off hardware timing is structurally unpredictable regardless of platform health.

The most significant financial event is the first positive operating cash flow in company history: $62k for the quarter, a $345k swing from Q4's -$283k burn. This is a genuine inflection point. At a $2.47 million quarterly revenue run-rate with positive operating cash flow, the company has demonstrated that its model generates operating leverage. This directly addresses the exit trigger language in the thesis — "repeated dilutive capital raises to fund operations" — which was the primary financial risk. That risk has materially reduced.

Monthly recurring revenue reached $602k in March 2026, up from $533k in February. The MRR trajectory within the quarter (not just the quarterly average) is an important signal — it means the company exits Q1 with momentum into Q2 rather than having front-loaded the quarter.

Cash balance of $2.97 million with $822k in total financing facilities fully drawn. The $894k cash decline was driven by $641k in capital expenditure on xBot fleet hardware and $118k in Skylink software development — growth investment, not operating burn. The distinction matters: a company spending cash on income-generating assets is not the same as burning through a runway.

Risks and So-Whats

The cash balance of $2.97 million with all facilities fully drawn and no unused financing capacity is the most important near-term risk. While positive operating cash flow reduces dilution risk, the margin of safety is thin. A single quarter of revenue disappointment — one deferred hardware order, one delayed contract commencement — could push the company back into operating burn with limited buffer. The so-what is not to exit the position but to monitor Q2 receipts closely. The Sibanye 24/7 contracts commencing in Q2 provide some revenue visibility but are not yet contracted at reported run-rate.

Related party payments of $233k in the quarter, including a $50k bonus to the CEO and $5k to a related party, are within what might be expected for a company of this scale but represent a meaningful proportion of operating receipts. The so-what is to note this as a cost discipline flag — not an exit trigger, but a variable to watch as the company scales.

WAIO trial cessation introduces the question of whether BHP's broader enterprise appetite for RocketDNA's platform is narrower than previously assumed. BMA remains a strong anchor relationship but the WAIO withdrawal suggests site-specific evaluation rather than enterprise-wide rollout is the current BHP posture. The so-what is to calibrate expectations for the pace of BHP expansion — more conservative than the thesis may have assumed.

The debt facilities — equipment loans, vehicle leasing, insurance premium funding, and equipment leasing at rates up to 13.9% — are all fully drawn. As the company grows, refinancing these facilities at better rates would improve the operating margin. The current cost of capital is a drag on net cash generation.

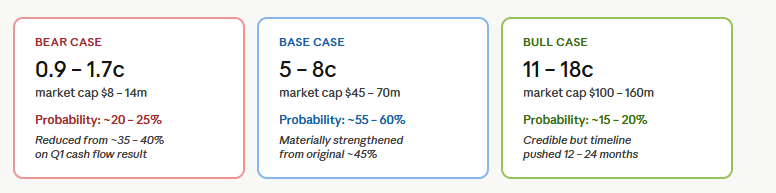

Proposed Bear/Base/Bull.

These numbers are all up 2-3c based on the new quarterly data. I enjoyed seeing a probability, despite it being AI generated... another bias to add to the list. hahaha "probability that AI is full of sh*t ... 100%"