We tend to lump stocks into two camps: small and risky, but with tantalising upside, or big and boring, plodding along with dependable (but modest) returns. But that’s a false binary; there is, of course, a vast and often fertile patch between these two extremes.

Not that this is news to Strawman members. But Corey Leung from WCM Investment Management makes a compelling case for the middle ground in his recent piece, The Goldilocks Years: A Case for SMID.

Leung sees SMIDs — short for Small and MID-cap companies — as inhabiting a sort of no man’s land in markets. Too large for the micro-cap crowd chasing moonshots, too small for institutional giants who care more about liquidity and benchmarking. The result is a blind spot where price and value often drift far apart.

For those willing to do the work, that spells opportunity.

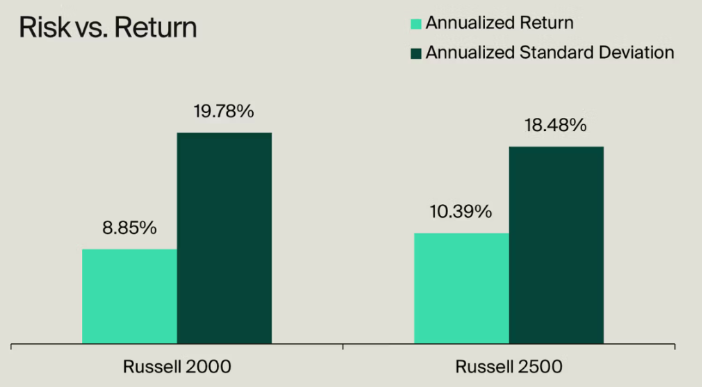

WCM’s data makes the case: using the Russell 2500 as a proxy, SMIDs returned 10.4% annually between 1985 and 2025 — beating small caps (Russell 2000) at 8.9%, and with less volatility. That kind of edge, held long enough, compounds into something serious.

But the real prize lies in what Leung calls “financial adolescence”; that awkward, but glorious transition from promising small fry to durable mid-cap compounder. It’s where moats expand, management matures, and the market starts to catch on. Spot the next blue-chip before the crowd does, and the payoff can be huge.

So why haven’t these inefficiencies been arbitraged away? Mostly because of how the system is set up. Institutional investors often get boxed in by rigid mandates. Once a company grows out of its small cap label, it has to be sold, regardless of merit.

Then there is the lack of coverage, especially in Australia, where many SMIDs operate under the radar and those who do cover them can have conflicting interests. Add to that the market’s obsession with short-term sizzle over long-term substance, and you have a recipe for neglect.

And let us not forget liquidity. Big funds struggle to build meaningful positions without moving the price. All of this makes the ASX’s middle-ground a surprisingly rich hunting ground for mispriced, high-quality businesses.

And that’s the key word: quality. Leung isn’t advocating simply for “cheap” stocks (although value definitely matters); he’s hunting for businesses with durable competitive advantages and stakeholder-aligned management. Think:

- Clear competitive edge: pricing power, sticky customers, scale, or IP.

- Savvy capital allocators: with discipline, transparency, and skin in the game.

- Reinvestment runway: ample room to grow, via established offerings and backed by internal cash flows.

- Businesses scaling up: from niche to national (or global). And with clear evidence of traction.

- Structural tailwinds: industries with secular growth or ripe for disruption.

The hard part is patience. It takes time for a business to realise its full potential. Sure, you can (in theory) make a decent buck betting early and exiting once the market wakes up. But the real money is in sticking around for the compounding.

Don’t bail just because a stock doubles or triples. If the fundamentals are improving, the business is reinvesting wisely, and the moat’s getting deeper, your best returns may still be ahead.

Conviction takes time. So does value realisation.

Anyway, all of this is to say that the recipe for outsized returns is simple (though far from easy): steer clear of the crowded, well-trodden corners of the market, back companies that have shown they’re more than just hype and hope but whose success and opportunity are not yet widely appreciated, and then get out of the way as they compound quietly over the years.

Turns out you don’t have to choose between growth and safety — or at least, it’s less of a trade-off than the style guides would have you believe. That’s what SMIDs offer: startup-like upside with blue-chip-esque resilience.

Strawman is Australia’s premier online investment club.

Members share research & recommendations on ASX-listed stocks by managing Virtual Portfolios and building Company Reports. By ranking content according to performance and community endorsement, Strawman provides accountable and peer-reviewed investment insights.

Disclaimer– Strawman is not a broker and you cannot purchase shares through the platform. All trades on Strawman use play money and are intended only as a tool to gain experience and have fun. No content on Strawman should be considered an inducement to buy or sell real world financial securities, and you should seek professional advice before making any investment decisions.

© 2025 Strawman Pty Ltd. All rights reserved.