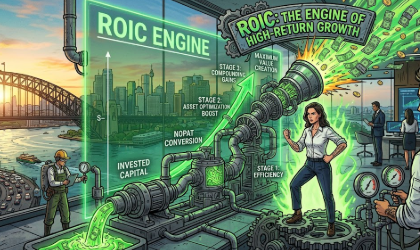

Successful investing is ultimately about identifying activities that deliver a positive return on invested capital (ROIC). The more money you generate, and the sooner you generate it relative to every dollar put at risk, the better.

Period. Full stop. End of story.

This fundamental truth holds steady whether you are a business, an individual, or a government. While it is certainly possible to get lucky when market sentiment swings your way, luck is not a strategy. If you aren’t clawing back a significant return for every dollar invested — or worse, getting back less than you put in — you have Buckleys chance of long-term success.

Even a high total return can be a trap if it takes thirty years to materialise. The time value of money means a significantly delayed win is usually indistinguishable from a loss.

I have previously argued that earnings growth is the North Star of investing; that per-share earnings are the ultimate attractor for share prices. That is definitely true. It’s just that ROIC is the underlying engine that enables that growth. Mathematically, you simply cannot sustain strong earnings per share (EPS) growth without a healthy return on investment. Without it, growth is just an expensive treadmill that leads nowhere.

(As a quick aside, related concepts like return on equity, return on assets, and return on capital employed are really just different flavours of the same idea. While they each offer unique nuances and no single metric tells the whole story, the underlying principle remains identical: the higher, the better.)

All this begs the question: how do you find a company primed to achieve great ROIC?

While history is never a guarantee of the future, past form sure as hell counts for something. It requires a bit of number crunching (or some savvy AI prompting paired with a careful human review) to look at the profits generated over a meaningful period and contrast them against retained earnings, raised equity, and debt. For the spreadsheet jockeys among us, this exercise is both a bit of fun and incredibly illuminating.

But like most backward-looking data, it only tells you what has already happened, not what will happen in the future. Still, you can sharpen your intuition by spotting early encouraging signs and determining if a business has the momentum to drive its ROIC higher.

This is why I find companies transitioning past the break-even inflection point so compelling. In these cases, much of the heavy lifting is often done: the capital has been raised, the infrastructure has been assembled, and a product is already gaining traction. If sales can be sustained or grown without requiring massive additional infusions of cash, the true ROIC is finally revealed and acts to drive per-share earnings higher.

The market quite often misses these opportunities because it remains fixated on a history of losses. It forgets the natural sequence of value creation: investment must always precede production, and production must always precede profit.

Amazon is a well worn example, but a good one. For years, the bears screamed that it was a black hole for money because it only ever seemed to suck it in, without ever giving any back. But under the hood, Jeff Bezos was achieving a massive return on invested capital in his established warehouses; he was simply choosing to reinvest every cent of that return (and then some) into new warehouses and AWS. The “losses” weren’t a sign of a bad business; they were the necessary precursor to a profit machine that eventually became unstoppable once the heavy lifting of the infrastructure build was complete.

Of course, there are never any guarantees. History is littered with companies that achieved early success only to be undone by hubris. When management starts reinvesting inappropriately or chasing growth for growth’s sake at the expense of efficiency, they usually just end up killing the golden goose.

Ultimately, growth is vanity, but return is sanity. If the maths on the capital doesn’t work, the investment won’t either.

Strawman is Australia’s premier online investment club.

Members share research & recommendations on ASX-listed stocks by managing Virtual Portfolios and building Company Reports. By ranking content according to performance and community endorsement, Strawman provides accountable and peer-reviewed investment insights.

Disclaimer– Strawman is not a broker and you cannot purchase shares through the platform. All trades on Strawman use play money and are intended only as a tool to gain experience and have fun. No content on Strawman should be considered an inducement to buy or sell real world financial securities, and you should seek professional advice before making any investment decisions.

© 2026 Strawman Pty Ltd. All rights reserved.