Metal concentrate value up 66 percent

But metal tonnage up 50 percent

The concentrate value is something I'm having trouble understanding as this could be from anything such as the metal tonnage uplift and other factors

So more questions again

We also see if nameplate can be maintained for next quarter

Stock has done well despite all the macro. Now largest position but more downside risk at this level.

Full announcement

Goal

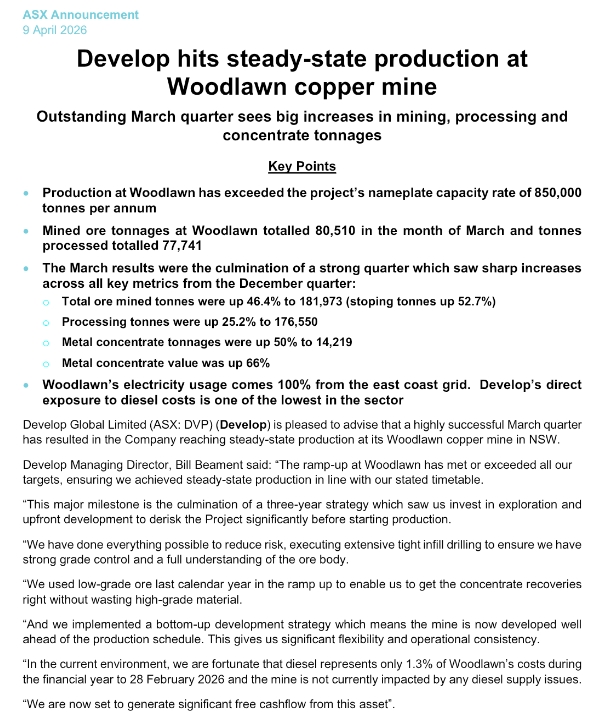

“At Woodlawn, the commissioning process has progressed extremely well, with both throughput and recoveries meeting or exceeding our forecasts.

“The success of the ramp-up was shown by the record throughput of 59,000t in the December. We are set to hit name-plate capacity of 850,000tpa this quarte

Reality

Going to be a long wait for DVP holders to see 850K tpa at Woodlawn.

On the plus side, lithium prices are pushing up. Pioneer Dome could be the elephant in the room for DVP.

[held]

First maiden profit for the group

Driven by none other than deferred tax assets from prior years

Without this DVP still made a loss although it has narrowed

Meanwhile it will be a pivotal year for DVP. Some aspirational numbers being quoted

These are the last quarterly numbers from Woodlawn which is still low

Let's see if DVP delivers and lives up to its hype.

[held]

Barry Fitzgerald article on DVP at RRS conference

I have to disagree that there was a 1100% return on my investment though!

It's more like only 1 bag. We should note that Bill and others threw a whole bunch of equity as part of the refinancing package to transform VXR into DVP.

[held]

Been a bit slow on updates here while I catch up

These pics of Sulphur Springs progress few days back was not what I was expecting - in a good way!

I thought it would be more rugged like the Grand Canyon. Shorts must be nervous right now seeing these photos if there are any.

It is good to see progress here as Sulphur Springs was the main reason why I invested in VXR/Develop.

[held]

Bill on the front foot today quashing rumours about any bad news about the BGL trading halt on work for DVP

Reassuring to know there is no reputational or business damage as I alluded to earlier but better to wait and see what BGL will release after the TH.

[held]

I prefer not posting on Develop as it does not appeal to anyone's radar here.

I guess it's because it is resources which appear to be rallying hard at the moment and people here are probably double dipping on tech and market faves lately.

Personally I don't see the volumes that encourage me to dip into any market darlings. Examples include AMZN, WES and BVS.

Anyway, Develop seems to have shifted back toward base metals which is a good sign as I originally invested for Sulphur Springs even though we know transport infrastructure will be a challenge. Key date will be June 2025. If nothing happens by then it will probably be a sell.

Comp table to really "sell the story". I don't pay much attention to these

Also the ASX comp has started and I recently bought in below 2.80 along with ALQ, mainly because no one talks about these here in Strawman so I'm going opposite of this site at the moment. Now both up which is good.

Market trend looks encouraging too.

[held]

Bill Beaumont's Develop popped 9% yesterday and one stage was up 11%.

Wonder why? Linkedin may be the answer.

At 600m market cap now with all those shares. My holding has been heavily diluted

[held]

Perhaps a positive development in Woodlawn for Beament's DVP

Not that I care much what happens. This is still a "challenging" project no matter which way you look

Would things be different if MIN still had a holding in DVP?

[held]

Develop announced their results indirectly via their Annual report with EBITDA 10.4m (-11.8+22.2)

Develop has the right commodities with copper, zinc and especially silver which is going up but the sellers still come out at the closing auction when I observe the recent price action.

[held]

Material enough for a trading halt?

Trying not to hope for too much here given the fall yesterday

(Held)

Did DVP post their final year results unannounced?

From Yahoo Finance

Apparently EBITDA positive of nearly 9m which was a bit unexpected.

Meanwhile DVP put up their latest presentation showing Pioneer Dome will be developed before Sulphur Springs

Probably why the share price fell given Lithium is now in a bear market.

Might be too late to walk back the presentation

[held]

Maybe another reason for the poor share price are the share options outstanding

A few days ago Blackiston excised his 1.4m 75c options DVPAY

But there's still a heap left and DVPAA expired last week

Wonder if the weird trading is from all these options floating around?

[held]

New addition on Develop website

Also a big thank you to whoever moved the shares down to $2.78 at the open as my order finally got filled after sitting there for months (bot trading??).

Time will tell if that seller made the right decision as it looks like there is clearly lots happening at Develop

[held]

Some unusual trading today with DVP shares which started down significantly at 3.15 before finishing up 3.36

Could be a bit of re-balancing going on for some funds.

[held]

Nero Resources Fund cuts DVP - 27 Sept (3.20)

Not sure what the thesis is behind the exit. It is not cap related as they hold Gensis Minderals which has a market cap of over $1bn so maybe simply thinks DVP is overvalued.

Bit of background:

Nero resources fund team - http://www.nerofund.com.au/team

Money of Mine podcast from the Nero Director Russell Delroy

https://youtu.be/do8JPnDI9VA?si=SHARU-32WHgf__7r

[held]

Develop has achieved its first quarter of operating free cashflow.

Which brings some much needed stability and trust in the business given there has been lots happening in DVP from the Woodlawn restart down to the merger with Essential.

But I'm also thinking costs may increase due to upcoming development work at Pioneer Dome and Woodlawn. So unless we see another contract, this performance could be a one-off.

I also feel there is still a great degree in skepticism about whether Beament can succeed in the same way he did with Northern Star which is totally understandable.

[held]

As expected. Woodlawn resource increases to 10 year+

Bill showing us that it is important to have the right people and not just the right product to execute.

Still waiting on reserve estimate before we can dig into financials

For those into hard figures, I believe Sulphur Springs has a NPV reserve of around $200m although it looks like Woodlawn is where we will see first revenues.

So DVP Market cap of $640m is overvalued if you believe BDO and strip out the org and people.

Resource details

Size comparison.

[held]

I'm sure lots of people would like to see a lower share price below $2 as mentioned by the BDO Independent Expert Report

Below is the reason why BDO still feels the merger is not fair due to their valuation of $1.73 published a few weeks ago.

Response from Bill Beament.

BDO’s recommendation, however, is based on a preferred post-deal value for Develop Global of just $1.73 a share, well under Friday’s closing price of $3.20.

Mr Beament, Develop Global’s managing director and an 18.3 per cent shareholder, unleashed on BDO, questioning the gap between its valuation and the market price.

“Please tell me where I can buy Develop shares at $1.73,” he said.

“I have spent more than $10 million buying Develop shares in recent months and I paid up to $3.20 a share. And I certainly believe that I got more than fair value. It was great value.”

Market was switf to respond to the latest repeat announcement today, sending shares up $3.46 ( 10%)!

Was good accumulation under $3 while it lasted. My post valuation merger still stands at 3.25.

[held]

Recent application grants to Develop at Sulphur Springs marked in light blue (E 4506033, E 4506034)

Purple dots are Lithium occurences which happens to be Pilgangoora. Dark yellow is copper. Bright yellow is gold.

Don't know what the filled shapes represent but I know they are different types of bedrock.

[held]

Have stayed quiet on Develop recently because it is literally too quiet here!

The Woodlawn SS is out and reads well. Could be mining soon once FID approval is passed next year.

7 year mine life with project still open at depth. Still hopeful this can go to 10 years.

More importantly, Reserves statement due in March 2024 which will form part of FID.

Not much has changed on Sulphur Springs. I think Woodlawn will be developed first even though I invested in VXR for Sulphur Springs because of wrongly assuming the Capex was lower than Khoemacau and not factoring Khoemacau has a much much longer mine life!

Dropping the word "Lithium" to stir a bit of excitement in Sulphur springs and make up for the lack of change above as well.

In other news, the Federal Court has granted DVP progress the Scheme of arrangement iwith ESS

Develop is also doing a few presentations. I may attend the Sydney one.

[held]

DVP released their quarterly and have decided to withdraw from the Liontown tender.

Looks like DVP could not provide enough boots on the ground for the project or needed men for other work including the Pioneer Dome asset that will be acquired after the ESS takeover.

[held]

Attempted short attack on DVP shares this morning which got gobbled up at my fair value estimate.

Not surprising this happened at the post cap / acquisition valuation (as opposed to the pro forma valuation)

[held]

Although Bill is taking up the accelerated rights issue (1 for 29 @ 3.20), I may give it a pass. Not sure if it is good value after doing my post acquisition calculations. Might be better to keep an eye on the share price and buy on market when it falls around that level.

Presentation slide with all the details of the takeover including shares on issue. Matches up with calcs on what I got including the assumption that rights and option holder convert to shares and in turn convert to DVP shares.

Interesting that DVP is using 3.20 CR price as the "Pro Forma Market Cap" and using the current price to compare. ESS is also trading around the equivalent DVP CR price.

With MIN giving approval with their 20% blocking stake, the takeover will most likely go throught. IGO had tried before and failed because MIN rejected that proposal using their blocking stake. Somehow you get the feeling that MIN was paving the way for DVP to make the move.

Fun and games

Also below is an article from AFR about the takeover which is currently behind the paywall:

[held]

Left field acquisition. ESS. DVP in trading halt

Held

DFS update.

Was hoping a better update but not as strong as hoped. Sold off first thing in the morning before staging a remarkable turnaround!

Someone selling at the lows (tax loss selling?) had a bad day. But as I say one day up doesn't make a trend if you take Nufarm as an example.

NPV5 is also used which I think is too low. Or Bill is sending a signal that he is really confident of getting the funds without tapping shareholders.

It will take time to go through the DFS so below is a summary and the original figures in 2019 for comparison. Overall it is not much different if you apply NPV8, it will probably work out to be equal the 2019 study. FCF is down from 818m to 745m so I think those that sold had the right idea but probably did not expect that price to run back up to positive territory.

Looks like inflation has impacted the figures. But bear in mind the original DFS was for OP (Open Pit) first while this update is for underground first (similar to Cannington) so it is more like comparing an apple to a pear.

VXR DFS as reference for comparison (5aug2019):

----------------------------- --- ---- --------------------------------------------------------------------------------------------------------------------

[held]

Spot the difference which copped a "Please explain" from the ASX

After the trading halt

A minor transgression I guess. Nevertheless another good drill result at the bottom. Anything at around 20m is good in my book Also remember CHN discovery hole was 20m worth of PGE.

[held]

Presenting at RRS

Fully funded by debt

Latest Woodlawn drill results at 75m @2.1% CU 3.1% Zn and 8.9g/t Ag

Aiming first revenue from Woodlawn stockpiles end of this year.

And I like this part - "Sorry for brokers/ fund managers in the room who want a cheap ticket you are not going to get it from us"

Still no revenue until end of the CY23 but a very slick presentation from Bill

[held]

Woodlawn drilling results.

9.9% at 5.6m looks quite good on face value. I haven't interpreted the true width yet. Maybe some geo/mining engineer can comment as I don't want to get too excited on the result.

In the meantime I better go back and check my high school trigonometry

[held]

There's been lots of speculation for the last 6 months Develop could be in the running for another underground mining contract this time with Liontown Resources.

Maybe this article from Stockhead triggered the rumour with Bill sporting a Liontown resources cap.

So I suppose when LTR rejected the takeover offer, DVP shares rallied on likelihood they will win the contract if Kathleen Valley remained under control of LTR?

[held]

Adding further to my theory of labour shortages in my South32 straw on Cannington Underground Mine.

Develop made a couple of key appointments who were former employees of Northern Star and Barminco back in November 2021.

Also it is already probable Northern Star experienced labour shortages as a result of the above key appointments of former NST employees.

While there's no proof key staff at Cannington or Golden Grove (29Metals) got headhunted by Develop, it is hard not to ignore the correlation of Develop having hardly any report of labour shortage and other underground mines being short staffed.

[held]

Selling has dried up from Endurance RP

This may explain why the shares have been trending upwards and bucking the wider market.

Their ETF-like sells seem to have not been properly timed which means there is probably something fundamentally wrong with this Venture Capital firm.

https://www.endurancerp.com/ICMServlet/download/13-2629-4273/eAnn_Disposal%20of%20DVP%20Shares.pdf

There are still some more shares to sell after they excised some options, so it is possible the downtrend could happen again soon.

[Held]

Michelle Woolhouse buys more shares.

But the big twist is she resigned her directorship in October

If this isn't confidence then I don't know what is...

[held]

Beament and a few other directors acquires more shares from placement

Also need to learn a bit more about how estates work as I thought usually estates get closed after a period when the person is deceased?

Looking back on my history, I may have also bought this for the Strawman Classic when it was still Venturex Resources (Oct 2020). As usual, it did nothing during the competition until the year after when Beament took over.

[Held]

Woodlawn details and plan - Develop Strategy Day

Develop outlining the issues and revised plan for Woodlawn as expected in their strategy day. The key is that there is lots of work to do including a new box cut that may require lots of resources, time and money which may be why price is underperforming.

On the flipside, Beaumont is acknowledging the challenges faced in developing the asset and appears to be very upfront about starting from a clean slate.

In summary, this will be a long marathon, but one Bill feels he is confident in winning.

And the work ahead.

Strategy going forward - exploration drive

The next 5 years - New box cut.

https://wcsecure.weblink.com.au/pdf/DVP/02564895.pdf

[Held]

Significant selling by former sub Endurance RP HK (formerly Regent Pacific HK)

Endurance RP HK is headed by Jamie Gibson and James Mellon who were formerly non-executive directors of Venturex resources in 2013. At that time they had a significant holding in Venturex.

Since the name change from Regent Pacific to Endurance RP, the company is transitioning their investments from resources to health and life sciences. Also it appears they have a tax settlement to pay with the ATO. Hence the share sales which started from 2019.

What is strange is that they took their option entitlement when Bill came on board.

Endurance RP may not be the only one selling and driving down the price. A possible candidate could be major creditor of Woodlawn, Orion Capital. But will have to do more digging

May be opportunistic time to start accumulating.

[H]

Map of the Woodlawn site from NSW Planning Portal submitted by Heron Resources.

Now the suspicions from Keith et al. that were spread during the Diggers conference seem justified that parts of the underground workings crosses the void and hence might not be good mining conditions.

From the presentation can see the mine void and lenses although quite small:

Close up (bit hard to see where the void is where Veolia is tipping the waste)

New drill drive (perhaps to get around the void)

So from the above slides, I believe Bill is aware of the problems faced (in my opinion). DVP will conduct a tour of the site with major investors and hopefully have a more detailed plan on addressing the "rumours"

Also note the project was acquired for 34m but a total of 340m was spent by previous owners.

As usual I could be wrong and Keith, TTC and Datt could be correct. In which case myself and Beament take the loss and eat humble pie.

DYOR.

[held]

Appears there are some who are critical about the Woodlawn Project particularly after the recent announcement confirming the resource estimate.

Can agree that Woodlawn has had a chequered past including some environmental issues regarding rehab of the site (I'm still doing my own research into this and found a detailed map of the site which I may link later).

The above tweet does not mention of the recent announcement of the updated resource estimate (it's slightly lower grade than before but within expectations). Also Keith was really hyping up Chalice at the ATH (and got me at one stage when really I should have sold or trim down my holding). So he does get things wrong sometimes.

At the end of the day, what matters is if Beament can prove the critics wrong by doing the work needed to improve confidence in Woodlawn. I'm not sure what that is - only Beament has the solution.

The other important point is Beament does have skin in the game, tipping in his own equity after the last capital raise for Woodlawn and the initial raising when he took over Venturex.

This is just my opinion and I'm trying to be objective with the views. Maybe Keith and the other commenters above could be correct and the ground rehab issues means Woodlawn does end up being a dud.

Held

Good exploration update update from Beament's Develop

Seems like there are some good widths from the infill drilling of over 20m and some extensions which could upgrade the size of the resource.

Market liked the update, up 9%

But bad timing as always with the current selloff happening. We are also now trading at around 50c pre-split and in addition a capital raising done at $3.20. Not including the contract as I don't know how to value that project especially given we are in a inflationary environment.

Perhaps some value around here???

Held

On face value, the Woodlawn mine acquisition appears to be a bargain for Develop which includes significant pieces of infrastructure including 1Mtpa plant and a state of the art ISAMill developed by Glencore for extracting ore from tailings (mentioned many times during the Heron conferences). Initial payment of $30m to be made through cash and equity raising.

For some that do not know, Heron Resources went into administration after trying to ramp up production operations at the Woodline zinc-copper mine. Heron's haphazard approach to extract Zinc/Copper from both development ore and tailings as they worked towards the high grade lens to generate cashflow combined with mismanagement within the company and with their subcontractor Sedgman/CIMIC was all part of Heron's undoing. Heron spent $300m in total developing the project

Bill is coming into this project with a totally new approach. This includes more drilling in depth to find the extent of the orebody which was not done properly by Heron. More importantly, he is continuing to put the mine in care and maintenance and has not set a date to restart production to try and preserve capital until he can expand the deposit further.

If Bill is right and the deposit expands, Develop needs to make upfront payments of 12.5m for 550Kt of ZnEq and 5.5m for 750Kt of ZnEq contained resources. Then further payments will be made for final investment decision (20m) and continuous production for 18 months (30m).

Overall it looks like the deal is fair as Bill is making payments only if milestones are achieved. And if things don't turn out as planned, then the upfront payment payment is written off at the minimum.

Webcast link - https://webcast1.boardroom.media/watch_broadcast.php?id=620c9a0e1c785

Disc: Held (on the fence with taking my entitlement)

FYI: thanks for putting me back as premium member, will try and type a bit more now :)

Substantial shareholder notice - Mineral resources

Seems MIN (Mineral resources) has been busy buying up VXR shares in the past couple of weeks before the cross trade happened to become substantial holder.

Interesting times.

_Ann_Becoming_a_substantial_holder_from_MIN.png?1616065761)