Consensus community valuation

Aug 27, 2025: RRS Gold Coast 2025 - Bill Beament, Managing Director of Develop (ASX:DVP)

Plain text link: https://www.youtube.com/watch?v=zSDjwVqx5k0

Bill says it better than I can.

Further Reading:

https://www.linkedin.com/in/bill-beament-a25532134/

ASX Announcements:

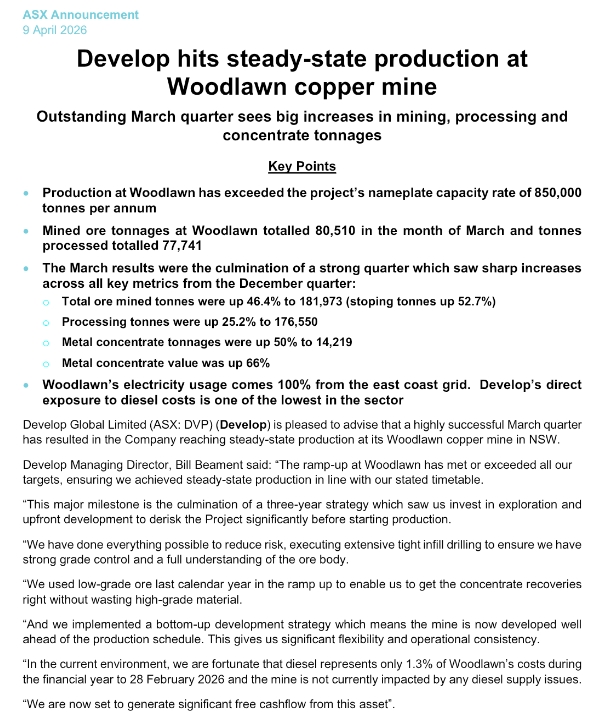

09 Apr 2026: Develop achieves steady-state production at Woodlawn

10 Mar 2026: Half Yearly Report and Accounts

28 Jan 2026: Quarterly Activities Report - December 2025

28 Jan 2026: Quarterly Appendix 5B Cash Flow Report - December 2025

Excerpt:

Blue and yellow stuff added by me; ASX mining exploration entities generally must lodge quarterly cash flow statements (Appendix 5Bs) until they transition to profitable mining producing entities. While there is no strict "number of quarters of profitability" rule, the requirement typically lasts for four consecutive profitable quarters, although this is at the discretion and assessment of the ASX.

Other DVP ASX announcements: https://www.develop.com.au/investor-centre/#asx-announcements

Disclosure: I am not currently holding DVP shares (I would like to buy them at lower levels) however I have held them in the past and intend to hold them again in the future.

Metal concentrate value up 66 percent

But metal tonnage up 50 percent

The concentrate value is something I'm having trouble understanding as this could be from anything such as the metal tonnage uplift and other factors

So more questions again

We also see if nameplate can be maintained for next quarter

Stock has done well despite all the macro. Now largest position but more downside risk at this level.

Full announcement

Goal

“At Woodlawn, the commissioning process has progressed extremely well, with both throughput and recoveries meeting or exceeding our forecasts.

“The success of the ramp-up was shown by the record throughput of 59,000t in the December. We are set to hit name-plate capacity of 850,000tpa this quarte

Reality

Going to be a long wait for DVP holders to see 850K tpa at Woodlawn.

On the plus side, lithium prices are pushing up. Pioneer Dome could be the elephant in the room for DVP.

[held]

19th December 2025: Develop Global's business strategy is two-fold, to be both a miner who owns and operates their own mines and processing plants, and to also be a mining services contractor for other companies.

I don't mind the strategy, it's the same one Chris Ellison has used at MinRes (MIN), and it has been very successful there.

However DVP's Woodlawn Mine produces mostly base metals, primarily Copper (Cu), Zinc (Zn), and Lead (Pb), along with precious metals Silver (Ag) and Gold (Au), processed into saleable concentrates that are shipped to buyers like Trafigura, with a focus on clean energy metals. The mine is ramping up from older, lower-grade zones to the high-grade Kate Lens for increased production of these key metals.

That's their slide deck pitch however my concern is that Woodlawn is predicted to produce about three times as much zinc as copper, so it should really be viewed as a zinc mine that also produces copper plus smaller quantities of those other metals. And I'm not particularly bullish on zinc, and whenever I have briefly been bullish on zinc in prior years, I've always been wrong. Usually zinc stinks.

They have other projects sure, but Woodlawn is their only producing asset at this point in time.

And their mining services business has only one client, plus Woodlawn which they own themselves, and that one external client is Bellevue Gold which has done alright recently from a share price perspective, but has had a rough time of it with multiple production downgrades since they started producing, all with DVP as their mining contractor during that time. Bellevue's problems have been mostly grade control issues, dilution, and stope underperformance, however there have also been previous issues with development stopes taking longer to drill than anticipated because of both the rock being very hard and also a lack of basic infrastructure at times, like water supply, drainage and adequate ventilation.

In one "Hole Truth" interview that I watched a few months back Bill described the huge improvements that Bellevue (BGL, the company) had made in that area (underground infrastructure) which he said meant that there should be nothing now holding DVP back from getting on with the underground drilling at Bellevue (the underground mine; both the company and the mine are called Bellevue), which suggests that there had been plenty holding them back in prior quarters.

They also previously had a mining services contract at the high-grade Beta Hunt gold mine, which is now owned by Westgold (WGX) but was owned by TSX-listed Karora Resources Inc. (formerly RNC Minerals) when DVP were awarded that contract in 2024, then Westgold acquired Karora after outbidding Ramelius Resources (RMS) for the company, then DVP's contract at Beta Hunt finished in late November 2024. The official spin by DVP on that was:

DVP's mining services contract at Westgold's Beta Hunt Mine concluded in late November 2024, finishing as planned because the development scope was completed ahead of schedule, allowing DVP to redeploy its teams and equipment to other high-value projects like Bellevue Gold and Woodlawn.

Some additional facts are that Westgold (WGX) acquired Karora in August 2024 and Westgold tends to use their own teams and equipment for mining, so they have an owner/operator model, same as what Bill Beament himself established at Northern Star during his time building that company up from nothing to become Australia's largest gold miner. Ral Finlayson's Genesis Minerals (GMD) also employ an owner/operator model at all of their mines. Additionally, Westgold do use MLG Oz (MLG) for road haulage between some of their mines and their processing plants, but in terms of the actual mining at Beta Hunt, Westgold do that themselves, so it makes sense that DVP finished up at Beta Hunt 3 months after Westgold took ownership of the mine.

I asked Google, "How many mining services contracts have Develop Global had during their history and how many do they have right now?" and Google answered with:

Develop Global's Mining Services division has rapidly grown, achieving its 5-year plan target in 18 months and currently holding three major contracts, generating significant revenue, with projections for even more in FY2025, showing strong historical growth in contract numbers and revenue. While the total number of contracts throughout their entire history isn't specified, their recent performance highlights rapid expansion from fewer contracts to a strong portfolio.

That's not actually true today - the reference for that spiel was this: https://www.listcorp.com/asx/dvp/develop-global-limited/news/mining-services-set-to-generate-c-175m-revenue-3010001.html which was from March 2024.

DVP's own website (https://www.develop.com.au/) does not list their mining services contracts either current or historic, however my understanding is that they are only currently active on two sites, being Bellevue Gold (BGL) and DVP's own Woodlawn Zinc-Copper mine.

Until today's news:

Source: Develop-awarded-A$200m-contract-with-OceanaGold.PDF [19-Dec-2025]

While the market did appear to like this announcement, sending DVP's SP up +4% to $4.36 today, they remain below their $5.19 year-high achieved mid-year (in July).

DVP's chart has been choppy, and while this new mining services contract announcement is welcome news, the project is in New Zealand and is only a one-off mine development project rather than an ongoing mining contract. It's a A$200 million underground development contract to establish access tunnels at OceanaGold’s (OG's) Waihi North Project in NZ.

So not recurring revenue and I would suggest while it is certainly material, it isn't a game changer for them. It could be if it leads to ongoing work in NZ, but that is by no means guaranteed.

So for now, DVP have a number of irons in the fire, but they only have one advanced development project (Sulpher Springs, zinc, copper and silver) plus one producing mine (Woodlawn, zinc, copper, lead, silver and a little gold) where they are owner/operators, plus one external mining services contract (Bellevue Gold) and one external mine development contract (OceanaGold's Waihi North in NZ).

I like Bill Beament and greatly respect everything he achieved at Northern Star Resources (NST), but this isn't gold, and it hasn't got those gold tailwinds - except for Bellevue and the jury is still out on whether Bellevue has further production guidance downgrades or upgrades to come from here - it could go either way, except it doesn't really impact DVP either way because they are on a fixed price rates schedule there as I understand it, so as long as Bellevue keeps operating the mine and mill, there is still going to be contract mining work for DVP there, but DVP don't share in the higher gold price upside there because they're just the mining contractors, not the project owners.

OG's Waihi North is also a gold mine, but again, it's not owned by DVP, they're just providing $200m worth of services there during 2026 and probably into 2027 - until those access tunnels are completed. No gold price upside there for DVP.

Sure, DVP certainly do have copper exposure, but what concerns me is that both Woodlawn and Sulpher Springs are going to produce far more zinc than copper so the outlook for zinc does impact DVP, and in my opinion it probably matters more to them than price movements with copper or any other metal.

Disclosure: I have held DVP in the past. I do not hold them today. I look at them regularly, but I'm not sure they're worth over $4/share with what they've got right now in terms of their business, their assets and their direct commodity exposures.

If track records are important, and they are, Bill Beament has one of the best track records you could ever come across over at NST. But that was gold, and DVP is primarily a zinc producer right now. (IMO)

So they remain on my watchlist for now.

First maiden profit for the group

Driven by none other than deferred tax assets from prior years

Without this DVP still made a loss although it has narrowed

Meanwhile it will be a pivotal year for DVP. Some aspirational numbers being quoted

These are the last quarterly numbers from Woodlawn which is still low

Let's see if DVP delivers and lives up to its hype.

[held]

I prefer not posting on Develop as it does not appeal to anyone's radar here.

I guess it's because it is resources which appear to be rallying hard at the moment and people here are probably double dipping on tech and market faves lately.

Personally I don't see the volumes that encourage me to dip into any market darlings. Examples include AMZN, WES and BVS.

Anyway, Develop seems to have shifted back toward base metals which is a good sign as I originally invested for Sulphur Springs even though we know transport infrastructure will be a challenge. Key date will be June 2025. If nothing happens by then it will probably be a sell.

Comp table to really "sell the story". I don't pay much attention to these

Also the ASX comp has started and I recently bought in below 2.80 along with ALQ, mainly because no one talks about these here in Strawman so I'm going opposite of this site at the moment. Now both up which is good.

Market trend looks encouraging too.

[held]

Monday 13th May 2024: Having a look at Bill Beament's Develop Global (DVP) again today, which I do hold (both here and IRL) and they are making steady progress towards their objectives. Cornerstone shareholder MinRes (MIN) sold their 14% stake in DVP around this time last month, and Bill Beament has increased his own stake in DVP to 15.08% (held through his company Precision Opportunities Fund). Chris Ellison's MinRes was under pressure to reduce MIN's debt levels, so there have been some "non-core asset" sales, including having 49% of MIN's dedicated 150-kilometre private haul road corridor in the Pilbara up for sale - the road connects MinRes’ Onslow Iron project at Ken’s Bore mine to the Port of Ashburton on the northern WA coast.

But back to DVP: Here are their latest announcements and presentations:

08/05/2024 8:23 am: DVP-Investor-Presentation-Pathway-to-Positive-Cashflow-May-2024.PDF(11 pages, market sensitive)

07/05/2024 8:24 am: Updated-Pioneer-Dome-Scoping-Study-(DVP).PDF (38 pages, market sensitive)

24/04/2024 8:24 am: DVP-March-2024-Quarterly-Activities-Report.PDF (18 pages, market sensitive)

24/04/2024 8:23 am: DVP-Quarterly-Appendix-5B-Cash-Flow-Report-March-2024-Qtr.PDF (5 pages, market sensitive)

From the Investor Presentation:

If you're not into Mining Services, copper, zinc and to a lesser extent lithium, then this one won't be for you, but with Bill Beament running this company, there's every reason to expect the company to be highly successful in future years, and he's done a reasonable job so far, since he left NST to head up Venturex, renamed the company ("Develop Global") and built up this portfolio of mining services clients and base metals and lithium projects.

I rarely buy into early stage companies like this - i.e. at this point in their history - however I'm happy to make an exception when we've got Bill Beament running the show. He has a truly exceptional track record.

Further Reading:

MinRes sells Develop Global stake; Bell Potter on the ticket (afr.com) [08-April-2024]

First-round offers in for MinRes $1b pit-to-port haul road sale (afr.com) [06-March-2024]

(25) DEVELOP: Overview | LinkedIn

Q+A: Aussie mining legend Bill Beament talks stonker copper hits and facing the future - Stockhead [17-May-2023]

Bellevue Gold Develops $400m contract - Australian Mining [14-April-2022]

MinRes awards Mount Marion decline contract - InvestMETS [01-Dec-2023]

Develop achieves five-year business plan - Australian Mining [22-March-2024]

Mining Services set to generate c.$175m Revenue - Develop Global Limited (ASX:DVP) - Listcorp. [21-March-2024]

09-April-2024: MinRes sells Develop Global stake; Bell Potter on the ticket (afr.com)

Disclosure: I hold MIN and DVP shares. I think that this does remove an overhang, and if zinc, copper and lithium prices rebound, DVP's share price will likely rise significantly from current levels. It may not happen overnight...

From March 18th, 2024, Develop Global (DVP) and the 13 other companies listed in the table below will all be added to the ASX300 Index - which is important for people such as myself who have their SMSF within an industry fund (CBUS, AustralianSuper, HostPlus, etc) or for any other SMSF where the rules only allow the additions of ASX300 Companies, so they prohibit the inclusion of any company that is not in the ASX300 or above (ASX200, ASX100, etc.). This restriction generally does NOT apply to fully self managed SMSFs where you arrange the auditing of the fund yourself, but does apply to those within industry super funds and a few other low-cost SMSF providers/facillitators that have the same restrictions.

Full announcement: SP-DJI-Announces-March-2024-Quarterly-Rebalance.PDF

I've been waiting for GNG, LYL and XRF to be added to the ASX300, but I'll have to wait longer clearly. The criteria isn't just based on the company's market capitalisation (m/cap), it's also based on the "free float", so the amount of shares that is nominally available to trade excluding shares held by insiders (Board and Management, Founders) and long-term institutional (insto) shareholders. This means that companies like GNG & LYL, where the Board, Management and Founders own 55% and 36% of the company respectively, and insto's own another 15% and 26% respectively (leaving a "free float" of just 30% of their SOI [shares on issue] for GNG and 38% of their SOI for LYL), will have to grow their market caps further than most other companies before being considered for inclusion in these indicies - due to their relatively small "free floats".

It will be good to be able to add DVP to my SMSF from March 18th anyway.

29-Jan-2024: I was talking over the weekend about quarterly reports over in the gold forum - see here - and today we got DVP's FY24 Q2 Reports: DVP-December-Quarterly-Activities-Report-29Jan2024.PDF and DVP-Quarterly-Appendix-5B-Cash-Flow-Report-December2023-29Jan2024.PDF

Firstly - here's the first page of their activities report:

I like that Bill is calling out the opportunity that he sees in "the softness in some parts of this market" - Agreed - there's nothing like buying at or near the bottom, if indeed this is at or near the bottom. Let's hope it doesn't turn out to be "nothing like" the bottom.

After all, Bill did make a name for himself by buying decent gold projects with plenty of turnaround potential at low points in the market (at NST) and then turning those projects around - increasing their profitability by reducing their costs while increasing productivity. It was his background in mining services - before he got into gold mine management - that enabled him to be able to think like that and allowed NST to achieve the success that they enjoyed while he was at the helm.

Speaking of bottoms, it would be good if last Tuesday was the bottom for the DVP share price, but you know what they say about trying to pick bottoms...

Technically they're probably still in a downtrend despite that +11.4% bounce today after rising +10.3% on Thursday - the DVP share price is up by just over +23% since last Tuesday - in 3 trading days - but their chart (above) still looks nasty...

I also liked this:

Note they "only" have 22 quarters (5.5 years) of available funding ($32.5m cash/cash equivalents plus $41.7m in unused finance facilities = $74.2m) based on their December Quarter cash burn (of $3.35m).

Yeah, I can see why the market MAY have considered today that DVP appeared to be oversold and was due for a minor positive re-rate; but... will they go on with it, or fall back and resume that downtrend... ? That is the question...

From The Helm - With Bill Beament, Managing Director of Develop - YouTube [19-Dec-2023]

Bill Beament, Managing Director of Develop - YouTube [24-May-2022]

Bill Beament, Can He Do It Again? | DVP.asx | Mining News - YouTube [27-April-2023]

Yes, I believe he can!

Disclosure: Yes, of course I hold DVP shares! It's Bill Beament!

01-Dec-2023: Develop-Awarded-Mt-Marion-Lithium-Underground-Development-Contract.PDF

Develop Global Limited (DVP.asx) is pleased to announce that it has been awarded a A$46 million underground development contract to establish and develop an exploration decline at the Mt Marion lithium mine in WA.

Mt Marion, which is a joint venture between Mineral Resources Limited (MinRes, MIN.asx) and Ganfeng Lithium Co. Ltd, is located 40km south-west of Kalgoorlie. It is also 95km from Develop’s Pioneer Dome Lithium Project.

The contract has a term of 18 months and is expected to start in early 2024.

The key works to be completed by Develop under the contract include:

- Surface facilities to support underground mining activities

- Portal Establishment

- Installation of underground mine infrastructure

- Excavate underground capital development and exploration drill platforms

- Develop through the orebody underground to obtain important geological and operational data for future mining activities

- Set up the underground for an extensive diamond drilling campaign to grow the maiden underground resource of 9.5Mt at 1.52% Li2O (see MIN ASX release 22 September 2023)

Develop Managing Director Bill Beament said, “The award of this contract to Develop is a significant vote of confidence in our world-class underground mining team.

“We have built a world-class underground mining team with immense experience in developing and operating underground operations, especially in WA.

“The strength of this team is shown by the outstanding results we are generating at the Bellevue gold mine, where the project is running on time and on budget.

“The Mt Marion contract is consistent with our stated strategy of securing two to three contracts within our mining services division.

“Our team is eager to make a significant contribution to the Mt Marion project by applying its extensive skills and experience to the underground development”.

--- ends ---

This contract award was widely expected - as the MoM (Money of Mine) podcast boys discussed earlier today - see below, so it didn't move the share price - in fact DVP closed -4.58% lower (14 cps down) at $2.92/share this arvo, and MinRes (MIN) closed down -0.93% (-57 cps) at $60.60/share as lithium names continued to slide - along with lithium prices.

Source: MarcusToday.com.au [MT don't include DVP in that graphic, but MIN is there in the "Lithium" section as well as in the "Mining Services" section, but not under "Iron Ore" despite Iron Ore being MIN's second largest revenue earner, behind Mining Services (mostly iron ore crushing, loading & hauling); MIN do not currently earn any revenue from lithium as their lithium mines are not producing anything yet - Wodgina was, but it's been on C&M - Care & Maintenance - so hasn't produced any spod for a couple of years now due to low spodumene prices. MIN has substantial lithium assets, they're just not producing assets at this point. Their revenue right now comes from mining services, iron ore, and probably a little from energy/gas as well.]

In Today's "Money of Mine" Podcast...

Who’s Failing AGM Season? + Don’t Believe the “Substantial” Hype | Daily Mining Show - YouTube

... the boys did discuss this contract award, at the end...

0:00:00 Preview

0:02:04 The key link in TG6 History

0:04:38 How is mesh made?

0:08:30 AGM strikes

0:11:32 Euro Manganese funding announcement

0:16:19 Ballarat Gold Mine swallowed up by Acheron Capital

0:18:19 Aus Super buying PLS

0:21:35 Orecorp deal update

0:24:45 Wild Magnus AGM scenes

0:27:29 Develop get Mt Marion contract

Click on that image above of the lads discussing Develop and MinRes to go straight to that part of today's podcast.

And if you're into lithium, they have discussed lithium every day over the past week, except for Monday - which was all about West African Gold.

Friday 24th November 2023:

Inside the AVZ’s Shareholder Meeting | Daily Mining Show - YouTube

0:00:00 Introduction

0:01:58 Turning shit ground into good enough ground

0:06:58 AVZ shareholder's day in the sun

0:23:24 Which ASX companies don't like management's pay?

0:28:04 Does the Raw Materials Act impact ASX companies?

0:31:45 We share the Bald Hill acquisition details (as MinRes won't)

0:39:00 What's the latest from Cobre Panama?

Monday 27th November 2023:

African Gold M&A is all GO! | Daily Mining Show - YouTube

0:00:00 Preview

0:00:30 Introduction

0:01:05 How Junior Miners can get more bang for their buck

0:05:17 Perseus go substantial on OreCorp, getting in SilverCorps way

0:11:02 IER deems Zhaojin's bid for Tietto not fair & not reasonable

0:18:31 Turaco do a deal with Endeavour

0:20:05 Aeris rattling the tin for 30 bucks

Tuesday 28th November 2023:

The Koala on why Lithium is Iron Ore 20 yrs ago & the Mining M&A evolution - YouTube

(No relation)

0:00:00 Preview

0:02:39 Gina needs help breaking Iron Ore

0:07:53 Why Trav and the Koala like Twitter

0:24:54 M&A at the big end of town

0:37:44 Why was Freeport sold?

0:43:05 Reconciling views on trough EBIDTA

0:46:29 WA Lithium

Wednesday 29th November 2023:

(no, not me, another Koala)

0:00:00 Preview

0:01:35 Underground Mining Trivia

0:04:34 How real is DLE?

0:09:58 Metal Price Bifurcation

0:18:03 Shareholder Activism

0:23:44 Whitehaven alignment

0:34:23 BHP growth

0:47:03 Is the Copper boom going to happen?

0:48:22 The Koala on the Banking hampster wheel

1:05:02 Over Rated - Under Rated

Thursday 30th November 2023:

All You Need to Know About Lithium Brines with Joe Lowry - YouTube

0:00:00 Introduction

0:00:08 Preview to Mr Lithium

0:01:18 Recap of the Delta Lithium AGM

0:03:48 Flying with Brooks to South America

0:06:02 Jobs on offer at JP Search

0:08:20 Joe Lowry back on Money of Mine!

0:12:20 The 101 on lithium brines

0:17:06 Is water going to be an issue for DLE?

0:26:45 What is the waste product for a brine project?

0:31:15 What are the most misunderstood aspects of brine projects?

0:34:08 is SQM slowing down or ramping up?

0:36:55 Why is the Atacama special for brines

0:43:58 Where is China going to source its product?

0:47:38 What makes a good brine development project

0:51:58 Summing up Direct Lithium Extraction (DLE)

0:56:00 Who are the DLE tech players

0:57:47 Prelude to part 2!

Plenty on lithium and lithium miners in that lot!

And Friday's (today's) podcast is discussed and linked to further up (above all the others).

Disclosure: I hold MIN and DVP shares and I topped up both today on the SP weakness and the confirmation of this contract award. BTW, MinRes recently increased their stake in DVP to a bee's whisker under 14% (13.97%) - see here: Change-in-substantial-holding-from-MIN.PDF so nobody is taking over Develop Global without Bill Beament and Chris Ellison being onboard - as both of them have their own blocking stakes. I believe that the two companies will merge (MIN will aquire DVP) at some point in the future, and that Bill B will end up running MinRes when Chris is ready to step back or retire from frontline management. No guarantees, but that's what I reckon might be on the cards.

Not sure about that chart. I'm no technical analyst, but you could make an argument about a shorter term rally within a longer term downtrend, or you could say it's starting to form a pennant and could breakout either up or down from within that pennant as it gets closer to the pointy end. Or you could look at what Bill achieved at NST and just back the man and his new company. His track record of shareholder value creation is enviable.

Some unusual trading today with DVP shares which started down significantly at 3.15 before finishing up 3.36

Could be a bit of re-balancing going on for some funds.

[held]

Nero Resources Fund cuts DVP - 27 Sept (3.20)

Not sure what the thesis is behind the exit. It is not cap related as they hold Gensis Minderals which has a market cap of over $1bn so maybe simply thinks DVP is overvalued.

Bit of background:

Nero resources fund team - http://www.nerofund.com.au/team

Money of Mine podcast from the Nero Director Russell Delroy

https://youtu.be/do8JPnDI9VA?si=SHARU-32WHgf__7r

[held]

Recent application grants to Develop at Sulphur Springs marked in light blue (E 4506033, E 4506034)

Purple dots are Lithium occurences which happens to be Pilgangoora. Dark yellow is copper. Bright yellow is gold.

Don't know what the filled shapes represent but I know they are different types of bedrock.

[held]

06-Aug-2023: Update on DVP from Euroz Hartleys here: dvp-040823.pdf It was published on July 28th and distributed by the ASX on Friday (4th August). I've reproduced the first page below:

Disclosure: I do not hold DVP shares at this point in time, but I probably should...

Wednesday 26th July 2023: INSIDER MAGAZINE: Bill Beament on life outside of mining and Develop Global | The West Australian

Plain Text Link: https://thewest.com.au/business/insider/insider-magazine-bill-beament-on-life-outside-of-mining-and-develop-global--c-10894035

We put Develop Global’s managing director Bill Beament in the hot seat to ask ...

What’s the best financial advice you’ve ever been given?

My old man was very adamant on this one. If you’re paying tax then you’re making money, and you’re making a contribution to everything else in society too. I’m paying a fair bit of that (tax) right now.

How do you manage a work-life balance?

I really do believe this is a hard one. I don’t think I’ve come across anyone in similar type roles in the past 15 years that gets the balance right.

A very wise, old and extremely successful entrepreneur told me last year at lunch: in your career you have spurts and steady periods, and in those steady periods, get that time with your loved ones.

What’s something that others have underestimated about you?

I think my energy, it catches people out. Those that have worked with me get it ... I’m like the Energiser bunny, I never say die. I’ve got a pretty big battery, that’s what my fiance says to me — she can’t keep up.

What drives you to succeed?

I just love the mining industry and I love the people in it, and I love seeing them develop and also succeed in all areas of life that goes with it. That’s been a big driver in the last seven or eight years of my career — watching the next generation of CEOs and entrepreneurs come through. For me, it’s never been about money.

I also love challenging the status quo and making a difference in the industry ... I love it when someone says I can’t do something, it’s like, I’ll find a way.

Beament with his Dad’s personal number plates. Credit: Ross Swanborough/The West Australian

Favourite holiday destination?

Being with my family and my loved ones is first and foremost and then it has to be the Duke of Orleans caravan park east of Esperance, where I grew up. I love that place.

I took my kids seven years ago on a big fancy holiday around America and Europe — it was an expensive bloody holiday, and a year later I said, ‘What’s your favourite holiday?’ and they said, ‘Out the Duke, Dad’.

Chocolate or cheese?

Both, and with a nice Italian red.

What are you binge-watching right now?

I’m watching Below Deck and I reckon it’s the best trash TV I’ve seen in a while. You can miss an episode and pick up where you left off, it’s fantastic.

Read any good books lately?

I failed English in high school so I actually hate books and don’t read them.

If you were to invite three dinner guests, dead or alive, who would they be?

Richard Branson first, I’ve always followed him — I just think he’s an amazing entrepreneur. I’d throw Kerry Packer in there and Margaret Thatcher.

What was the last band you paid to see?

Eskimo Joe.

Childhood hero?

My Dad and my Mum. Dad was a mechanic by trade and Mum was a house mum and housewife, but Dad ended up being a bit of an entrepreneur with his mechanical side and the rest is history.

Dad took great care to buy the best ute available at the time for his purposes, which I took out of the estate. It has personal number plates from the small region where I grew up (Condingup), just east of Esperance.

Who would play you in the movie of your life story?

Probably Tom Hanks; I grew up watching him. He can do any role and looks to be a genuine, nice guy.

--- end of excerpt ---

Here's a link to Google Maps showing Condingup (where Bill grew up) and his favourite holiday destination - the Duke of Orleans Caravan Park.

Duke of Orleans Bay Caravan Park - Google Maps

Nice part of the world!

Could be a bit chilly on the South Coast at this time of year, but a fair destination for a summer holiday for sure!

Interesting insight into the man who built up Northern Star Resources from scratch to become Australia's second largest gold mining company and is now back in Mining Services (where he started before NST) - building up Develop Global (DVP).

Adding further to my theory of labour shortages in my South32 straw on Cannington Underground Mine.

Develop made a couple of key appointments who were former employees of Northern Star and Barminco back in November 2021.

Also it is already probable Northern Star experienced labour shortages as a result of the above key appointments of former NST employees.

While there's no proof key staff at Cannington or Golden Grove (29Metals) got headhunted by Develop, it is hard not to ignore the correlation of Develop having hardly any report of labour shortage and other underground mines being short staffed.

[held]

Map of the Woodlawn site from NSW Planning Portal submitted by Heron Resources.

Now the suspicions from Keith et al. that were spread during the Diggers conference seem justified that parts of the underground workings crosses the void and hence might not be good mining conditions.

From the presentation can see the mine void and lenses although quite small:

Close up (bit hard to see where the void is where Veolia is tipping the waste)

New drill drive (perhaps to get around the void)

So from the above slides, I believe Bill is aware of the problems faced (in my opinion). DVP will conduct a tour of the site with major investors and hopefully have a more detailed plan on addressing the "rumours"

Also note the project was acquired for 34m but a total of 340m was spent by previous owners.

As usual I could be wrong and Keith, TTC and Datt could be correct. In which case myself and Beament take the loss and eat humble pie.

DYOR.

[held]

On face value, the Woodlawn mine acquisition appears to be a bargain for Develop which includes significant pieces of infrastructure including 1Mtpa plant and a state of the art ISAMill developed by Glencore for extracting ore from tailings (mentioned many times during the Heron conferences). Initial payment of $30m to be made through cash and equity raising.

For some that do not know, Heron Resources went into administration after trying to ramp up production operations at the Woodline zinc-copper mine. Heron's haphazard approach to extract Zinc/Copper from both development ore and tailings as they worked towards the high grade lens to generate cashflow combined with mismanagement within the company and with their subcontractor Sedgman/CIMIC was all part of Heron's undoing. Heron spent $300m in total developing the project

Bill is coming into this project with a totally new approach. This includes more drilling in depth to find the extent of the orebody which was not done properly by Heron. More importantly, he is continuing to put the mine in care and maintenance and has not set a date to restart production to try and preserve capital until he can expand the deposit further.

If Bill is right and the deposit expands, Develop needs to make upfront payments of 12.5m for 550Kt of ZnEq and 5.5m for 750Kt of ZnEq contained resources. Then further payments will be made for final investment decision (20m) and continuous production for 18 months (30m).

Overall it looks like the deal is fair as Bill is making payments only if milestones are achieved. And if things don't turn out as planned, then the upfront payment payment is written off at the minimum.

Webcast link - https://webcast1.boardroom.media/watch_broadcast.php?id=620c9a0e1c785

Disc: Held (on the fence with taking my entitlement)

FYI: thanks for putting me back as premium member, will try and type a bit more now :)