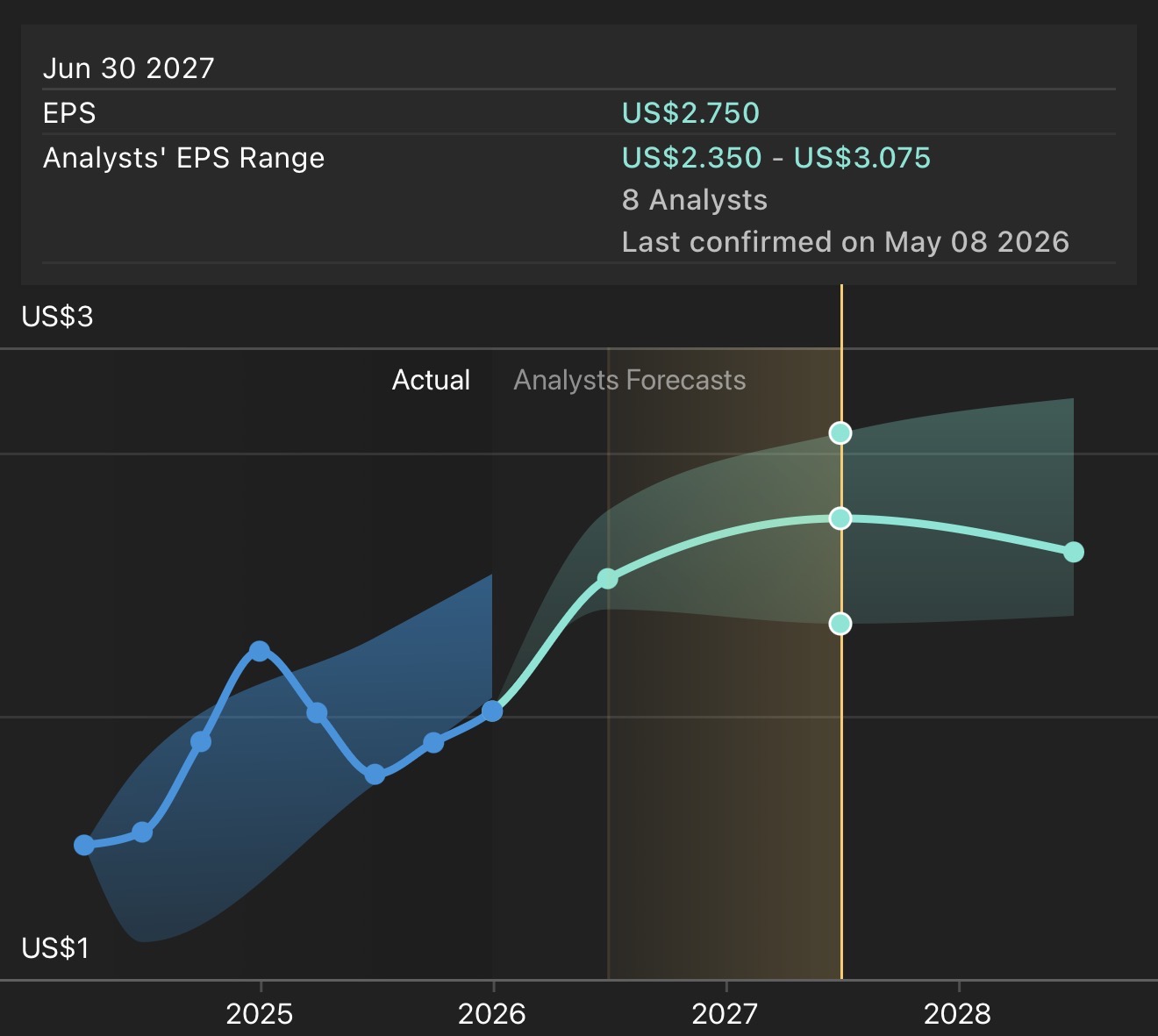

I don’t know how many Strawfolk hold BHP at the moment? It makes up about 6% of our IRL portfolio at the current share price ($62). To me BHP looks very expensive at $62 per share. I’ve been slowly taking some profits as I did last time it went above $60 per share. Analyst consensus is FY27 NPAT of US$2.75 per share. Thats A$3.80 on the current conversion rate. Thats a FY27 PE of 16 times and ROE should be approx 17.5%. BHP is a great business. It might do even better if the surge in copper prices continues and Canadian Potash starts coming on line.

Using McNiven’s Formula assuming the ROE continues at 17.5% for the foreseeable future I get an annual return of 7.5% per year at $62. I don’t know, it just looks a bit risky up here.

What do others think?

Source: Simply Wall Street

Is it possible that the biggest short in the history of BHP was a big mistake? In hindsight it certainly seems that way?

On the 28 January BHP was the most shorted stock on the ASX with a whopping 17.63% of shares shorted. The shorts spiked by an incredible 7.18% in just one day on the 28 January 2022 (www.shortman.com.au). Why?

Stephen Bartholomeusz explained why BHP was sold short prior to the unification (The Sydney Morning Herald, 19/01/2022).

‘For most of the two decades since the formation of the dual-listed structure (although not always) the Plc shares have traded at a material discount to Ltd’s, generally in the mid-teens although it has been as much as 20 per cent.’

Following the LSE delisting a Plc share had exactly the same rights and entitlements to earnings and dividends as a Ltd share – providing a windfall to Plc shareholders as the historic discount is wiped out by unification.

That largely happened early on. From the moment unification was announced Ltd shares have fallen and Plc shares risen.

What was a Plc discount of 21 per cent immediately ahead of the unification announcement has been closed to less than 3 per cent as arbitrageurs sold BHP shares short and bought Plc shares that they will use to cover their positions, at tidy profits, once the unification is complete.

Ltd shares have fallen about 10 per cent and Plc shares have risen about 3 per cent since the corporate restructure was announced.

BHP’s independent expert, Grant Samuel thought there could be as many as 450 million shares sold as British and other foreign shareholders exit the register.

Against that, BHP’s weighting in the ASX has increased materially, from about 6.2 per cent to about 10 per cent. Australian index investors and those funds benchmarked against the ASX indices have been be buyers.

Now the register has settled, the unified BHP is trading on its performance and prospects. Unification has had no material impact on either.

What happened on the 28 January?

The BHP Plc Scheme (Unification) became effective on 28 January 2022. Plc Shareholders (BHP shares listed on the LSE) received one New Limited Share for each Plc Share they held.

Despite the 7.18% jump in short positions on the 28 January coinciding with the unification, the BHP share price increased by 2.7% to $46.92. It would seem the impact of short activity on the 28 January was outweighed by a BHP buying spree.

Normal trading in New Limited Shares on the ASX as a result of the unification under the ticker “BHP” commenced on 2 February 2022. The BHP share price closed at $45.64, again it was up on the previous day.

After 3 days of normal trading (Friday, 4th Feb 2022) the BHP share price closed at $46.81. There were still no signs of a collapse in the share price as a result of the unification. Why?

In my view the 21% discrepancy between the BHP Plc share price (LSE) and the BHP LTD (ASX) immediately prior to the unification announcement share price has already closed. Funds were quick off the mark in discovering there were huge profits (20% in fact) to be made by selling down BHP Ltd shares and buying BHP Plc shares.

This all happened very quickly after the announcement. In less than a week after the announcement the BHP Ltd share price had dropped from $52.81 to $44.46.

What happen with the Short Positions?

The unification of BHP did not collapse the share price as shorters were hoping for and this did not provide the opportunity to close positions at a profit.

Then on the 15 February BHP released an incredible 1H22 result with NPAT up 144% pcp.

Iron ore prices are trending up again and the future prospects are looking good.

The BHP share price is now climbing toward $50.

Since the unification of BHP Shorters have been scrambling to close positions, now almost non existent (0.56% on the 11 Feb).

To some extent I think shorters have helped to drive up the share price! Ouch, that must have hurt! :)

So in hindsight was the Big BHP Short just one Big Mistake?

There's nothing investors hate more than confusion and uncertainty! Over the last 24 hours BHP served up a smorgasbord of confusion...and hey presto, look what's happened to the share price!

Only 2 weeks ago the BHP share price was an all time high of $54.06 and today it closed at $47.70, down 12% in just 14 days. What happened? Tristan Harrison from TMF posted a great Outlook Summary following the FY21 results announcement.

So, where do you start to make sense of it all? There are four big items in the mix right now:

- FY21 financial results

- US$5.7 billion capital expenditure approved for the Jansen Potash Mine

- Woodside Petroleum Business Merger

- Dividend declared, US$2.00 (AU$2.76), fully franked.

1. FY2021 Financial Result

What an incredible result! (see attachment):

- Underlying EBITDA US$37.4 billion (up 69%)

- Underlying EBITDA margin of 64%

- Underlying attributable profit of US$17.1 billion

- Attributable profit of US$11.3 billion

- Record FY dividend of US$3.01 cps

BHP reported that its attributable profit grew 42% to US$11.3 billion. That number included an exceptional loss of US$5.8 billion predominately related to impairments of potash and energy coal assets, and the current year impact on the Samarco dam failure.

BHP said that all divisions met earnings guidance.

Tristan Harrison (TMF) said the result was in line with what most analysts were expecting. Macquarie Group Ltd and UBS said the dividend was bigger than expected.

Based on the forecast 2022 earnings brokers had varying opinions according to Tristan. Macquarie has a price target of $58. It reckons BHP is valued at 11x FY22’s estimated earnings with a forward grossed-up dividend yield of 10.6%.

However, UBS says BHP is a hold with a price target of $42, even though it reckons the BHP share price is valued at under 10x FY22’s estimated earnings. UBS is expecting a higher FY22 profit than Macquarie.

If we averaged broker opinions the 2022 target price would be around $50 per share. This doesn't explain the closing price of $47.70 today.

2. Jansen Potash Capital Expenditure

BHP announced that it has approved US$5.7 billion of capital expenditure for the Jansen Stage 1 of the Potash Project in the province of Saskatchewan, Canada.

BHP believes Jansen will create value for shareholders for generations. Jansen is located in the world’s best potash basin and is expected to operate up to 100 years.

Potash provides BHP with increased leverage to key global mega-trends, including rising population, changing diets, decarbonisation and improving environmental stewardship.

Jansen S1 is expected to produce approximately 4.35 million tonnes of potash per annum, and has a basin position with the potential for further expansions. First ore is targeted in the 2027 calendar year, with construction expected to take approximately six years, followed by a ramp up period of two years.

At consensus prices, the go-forward investment on Jansen is expected to generate an internal rate of return of 12 to 14 per cent, an expected payback period of seven years from first production and an underlying EBITDA margin of approximately 70 per cent given its expected first quartile cost position.

Potassium is a future facing commodity with attractive long term fundamentals from multiple angles:

- The environmental footprint of potash is considerably more attractive than other major chemical fertilisers

- Conventional mining with flotation is more energy and water efficient than other production routes

- Traditional demand drivers of population and diet are reliable and slow moving

- Attractive upside over basic drivers exists due to the rising potash intensity-of-use needed to support higher yields and offset depleting soil fertility

- On top of the already compelling case, decarbonisation could amplify demand upside

- The industry’s 4th wave is underway: demand to catch-up over the course of the 2020s

- Demand is catching up to excess supply, and major supply basins are mature

- Price formation regime accordingly expected to transition from current SRMC to durable inducement pricing, with Canada well placed to meet market growth longer term at LRMC in the mid $300s

3. Woodside Petroleum Business Merger

I believe investors are most concerned about the Woodside-BHP Petroleum merger news.

Under the proposed transaction, Woodside will acquire 100 per cent of the issued share capital of BHP Petroleum International Pty Ltd in exchange for shares in Woodside which will deliver 48 per cent to BHP shareholders on completion. Woodside shares will be immediately distributed to BHP shareholders. Woodside will remain listed on the ASX with listings on additional exchanges being considered.

The merger is expected to be completed in the second quarter of the 2022 calendar year with an effective date of 1 July 2021.

Morgans notes that the Woodside merger removes growth opportunities for BHP. Though, it acknowledges that its balance sheet strength gives it mergers and acquisitions (M&A) optionality.

I think BHPs long term strategy to move away from fossil fuels and focus more on the key global mega trends including copper, nickel, potassium and iron ore is a positive step for the company.

4. Record Final Dividend

BHP has declared a record final dividend of US$2.00 per share fully franked, or AU$2.76. If you consider the value of the franking credits, this equates to AU$3.59. BHP trades ex dividend on 2nd September 2021.

The upcoming dividend is significant in the current value proposition for BHP. If you subtract the dividend value including franking credits ($3.59) from the current share price of $47.70 you are potentially buying BHP for $44.11 per share. Yes, the share price will drop when BHP goes ex-div on the 2nd September, but I think the share price will gravitate towards the consensus target price of $50 per share over time.

My take

I think BHP is worth considering at $47.70 with the upcoming dividend taken into account, and the move away from fossil fuels towards global mega trends is considered.

Disc: Held SM and IRL