Consensus community valuation

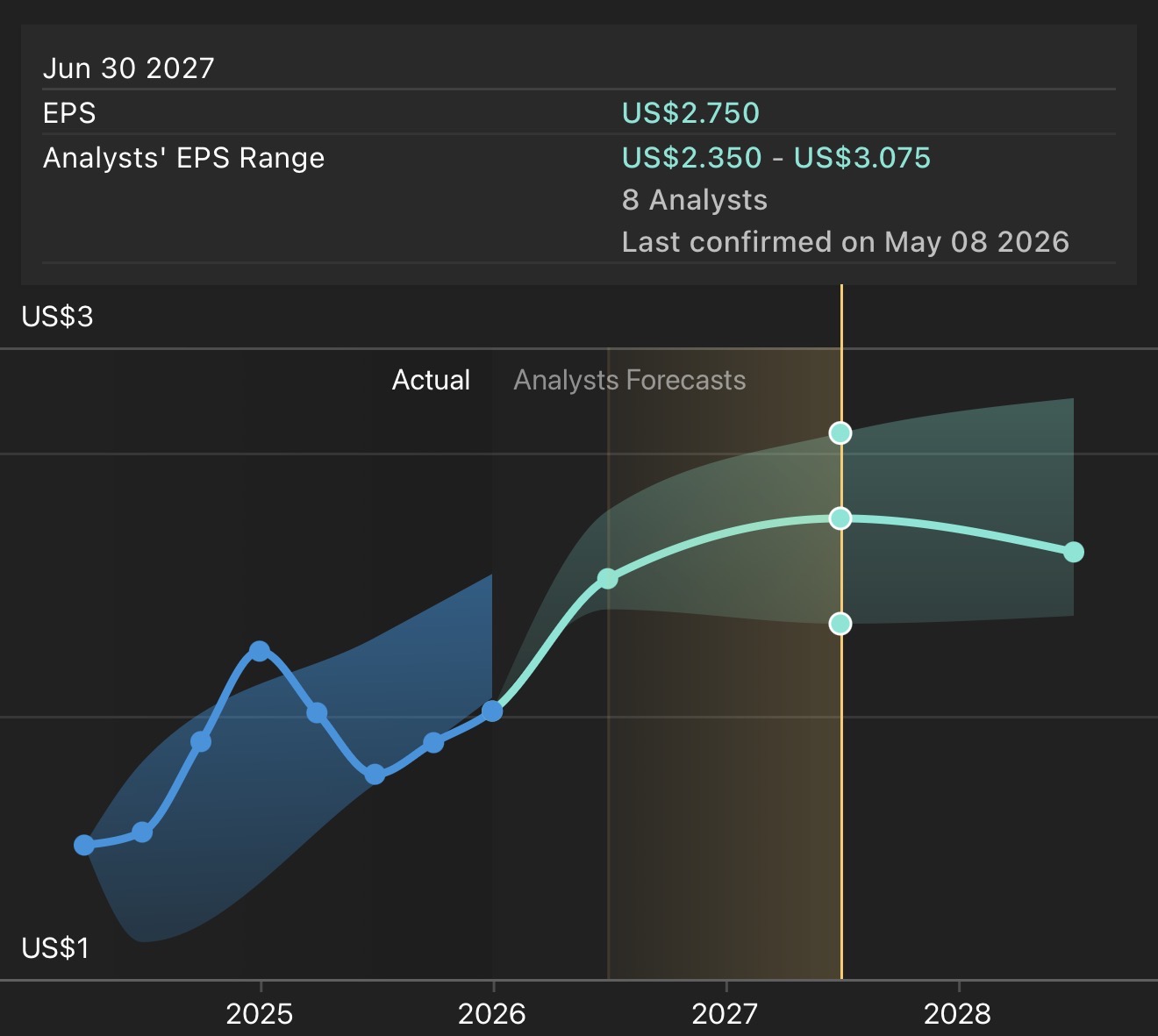

I don’t know how many Strawfolk hold BHP at the moment? It makes up about 6% of our IRL portfolio at the current share price ($62). To me BHP looks very expensive at $62 per share. I’ve been slowly taking some profits as I did last time it went above $60 per share. Analyst consensus is FY27 NPAT of US$2.75 per share. Thats A$3.80 on the current conversion rate. Thats a FY27 PE of 16 times and ROE should be approx 17.5%. BHP is a great business. It might do even better if the surge in copper prices continues and Canadian Potash starts coming on line.

Using McNiven’s Formula assuming the ROE continues at 17.5% for the foreseeable future I get an annual return of 7.5% per year at $62. I don’t know, it just looks a bit risky up here.

What do others think?

Source: Simply Wall Street

We’ve read the minutes from the last meeting… it said buy Beer.. so we did!!

23-Aug-2023: BHP's Henry responds to Dick move (MiningNews.net)

BHP's response to Queensland lease questions (australianmining.com.au)

Queensland asks BHP to invest in state or risk licence cancellation (mining-technology.com)

From the AFR article (link above - 2nd one from top):

BHP to steer clear of new investment in Queensland

BHP chief executive Mike Henry said the global miner would not make any new greenfield investment in Queensland after the state’s controversial new coal royalty regime made it too risky to invest.

While Treasurer Cameron Dick has threatened to cancel BHP’s mining leases in Queensland unless it continued to invest in the state, the BHP boss acknowledged the company would continue to expand its existing operations to take advantage of strong metallurgical coal prices.

Queensland Treasurer Cameron Dick said mining leases would be cancelled if not used. Photo credit: Jamila Toderas

The Labor government and the mining giant have been locked in a war of words since Mr Dick blindsided the resources sector when he introduced three new tiers of coal royalties in July last year.

BHP is in the process of selling two of its Queensland mines, Daunia and Blackwater, but has kept its most valuable coking coal mines, including Goonyella, Riverside, Peak Downs and Saraji.

Mr Henry said the challenge remained that Queensland’s royalty regime, which required BHP to pay another $700 million last financial year, made other states or countries a better investment destination.

“I don’t think we are saying anything particularly controversial; lower returns, higher risk means other investments become more attractive,” he said after BHP released its results on Tuesday.

“The only thing I would note is we are continuing to invest in these Queensland businesses. BMA [BHP Mitsubishi Alliance] is investing over a billion dollars a year in keeping these operations going because we do see the business as attractive.”

In its statement to the ASX, BHP said the coal royalty hikes had negatively impacted the “investment economics” of Queensland and increased sovereign risk.

“We will not be investing in any further growth in Queensland; however, we will sustain and optimise our existing operations,” it said.

Mr Dick continued his attack on the global miner on Tuesday, saying the Palaszczuk government would follow through with its threat if BHP did not complete its promised investments in Queensland.

He said BHP’s bumper profit of $13.4 billion showed the company had the resources to deliver on its mining leases.

“For all the complaints about progressive coal royalties, for coal, BHP’s underlying return on capital employed came in at a very healthy 47 per cent,” Mr Dick told state parliament.

Queensland coal royalties delivered $15 billion into state coffers last financial year. Photo credit: Glenn Hunt

“The strength of BHP’s balance sheet and the impending windfall it will make from selling the Daunia and Blackwater mines shows just what BHP can achieve when it focuses on its core business.”

Mr Dick said BHP even acknowledged the new royalty regime may push up prices, which means more profits in the future.

But he warned that the Labor government expected big miners to follow through on promised investments or they could face financial penalties or have their leases cancelled.

“We want those companies to properly develop the leases that they have been granted by the people of Queensland. If they fail to do so without legitimate commercial reason, our government has the power to act,” Mr Dick said.

The new system introduces three tiers: a royalty rate of 20 per cent for prices above $175 a tonne, 30 per cent for prices above $225 a tonne and 40 per cent for prices above $300 a tonne.

The new tiers gave Queensland the highest-taxing royalty rate in the world and delivered a staggering $15 billion in coal royalties last financial year.

Queensland Resources Council chief executive Ian Macfarlane, who has vowed to fight the state’s coal royalty regime up to next year’s election, said Mr Dick’s latest threat to cancel BHP’s leases would further shake investor confidence in the state.

“We shouldn’t take for granted that Queensland will always have a strong resources sector to rely on if policies are introduced which make us less competitive and less attractive to investors,” Mr Macfarlane said.

“All Queenslanders will lose out if resources companies move their focus to mining projects in other states and countries because of growing uncertainty about the Queensland government’s attitude towards the mining sector.”

--- end of excerpt ---

Further Reading: BHP looks past China’s property woes to mining’s brave new world (afr.com)

Disclosure: I do not currently hold any BHP shares, however I do hold South32 (S32) shares IRL and they own the Cannington Silver/Lead/Zinc mine in Queensland. Interesting that the Qld Government chose to have a barney with BHP and not S32 (which was spun out of BHP a few years ago). However, this is all about coal, and BHP are still into coal, whereas S32 is moving away from coal and have already divested all of their thermal coal assets. The only coal that S32 have now is the Illawarra Metallurgical Coal mine in NSW, and the NSW Government has a far more collaborative approach to mining and mining investment than the combative approach that Queensland appears to be taking, particularly on coal.

18-Jan-2021: I think BHP's SP will continue to rise on the back of a global economic recovery and recovering commodity prices, although I expect the iron ore price to go lower once Vale resume full production in Brazil. I also think that BHP might bounce off that $50 level a few times before finally pushing through with conviction, and that might take some time to play out, so I'm going to pick a PT (price target) a little below $50 for January 2022 (12 months from today), although it could well be above $50 if things go better than expected. I do not currently hold BHP because I see better opportunities in other companies at this point, like S32 (South32), which I do hold in my superannuation portfolio.

In summary, I think there's long term upside in BHP - no doubt - however there will likely be SP volatility associated with a correcting iron ore price in the medium term. I am therefore of the opinion that BHP is not one of the best opportunities in the market at this point in time (so do not hold them), even though I think there IS upside.

19-July-2021: In the past 6 months BHP have poked their nose above my $49.77 price target a few times, and they're currently at $50.50, so just above it. I don't see a major catalyst that is going to push BHP up to $60 yet, and the iron ore price will come down once Vale are back in full production in Brazil. There is also the rumour that China are trying to source as much as they can from countries OTHER than Australia, and so far Iron Ore has been their biggest headache because we're the biggest supplier, and the next biggest supplier (Brazil) still have issues at this point, however when they are able to, I expect China to buy more iron ore from Brazil and other countries, and less from Australia. Apparently we haven't learned our lesson and we need to be punished further. Which is all to say that it's not ALL blue skies for BHP from here, and perhaps around the $50/share mark is as good as it gets for a while.

I am not holding BHP shares. I do hold South32 (S32) shares however, the "non-core" assets that were spun out of BHP a few years ago, and I think S32 still have further upside from here. S32 do not produce iron ore. S32 produce bauxite, from which they extract alumina, which they smelt into Aluminium, plus silver, nickel, zinc, manganese, lead and metallurgical coal, having recently completed the sale of their thermal/energy coal assets. BHP still has thermal/energy coal mines.

17-Jan-2022: Update: My $50 valuation for BHP has flagged as stale, so I'm updating it, and raising my PT (price target) to $53. Nothing new to say about BHP at this time (that I haven't already said above) except that I think they will have some tailwinds on the back of rising copper and nickel prices, however I think the outlook for iron ore and met coal are more uncertain. BHP are very low cost producers however, so they can absorb lower prices and still remain very profitable. Their potash assets could do very well over the next decade.

I am not currently holding BHP here or in RL.

19-July-2022: Still not holding BHP, although I do currently hold S32 and FMG shares. I'm lowering my price target for BHP to $42 today. They did briefly tag my previous $53/share price target (a couple of months ago, in April/May 2022) however there have been changes, not least of which is that they have spun out their Petroleum (oil and gas) assets via a merger of that division of BHP with Woodside Petroleum to create a new company called Woodside Energy Group (WDS).

The merger was completed in June with the new company (WDS) owned approximately 52 per cent by the old Woodside (WPL) shareholders and 48 per cent by BHP shareholders (who were on the share register prior to the merger). BHP received 914,768,948 Woodside shares as consideration for the sale of BHP Petroleum and BHP distributed those Woodside shares in the form of an in-specie dividend to their own shareholders.

This means that BHP is now worth less because some of that value that WAS there prior to June now resides within a different company, Woodside Energy Group (WDS) who are travelling OK at the minute.

BHP, not so much...

There are positives, like BHP deciding to sell off some of their thermal coal assets, while retaining their met coal assets (metallurgical coal is used for steel production, not burned to create electricity in coal-fired power stations), and negatives, such as BHP deciding to keep some of their thermal/energy coal assets (BHP-to-retain-New-South-Wales-Energy-Coal.PDF) and an iron ore price that finished FY22 at over $100/tonne LOWER than where it finished FY21, and has gone even lower since June 30th.

BHP's revenue is primarily derived from iron ore, copper, coal and nickel now, with some lesser production of zinc and uranium which are really byproducts from their Olympic Dam mine in northern South Australia. They are also continuing to develop their Potash arm.

However they do not expect to be producing Potash before 2027 according to that.

Source: BHP-Quarterly-Activities-Report-Q4-FY22.PDF

So BHP is becoming cleaner, or more streamlined with the oil and gas assets gone and the thermal coal assets being reduced (although not entirely eliminated because they are still continuing to stubbornly hold on to their high margin NSW energy coal assets). But still diversified. If you can stomach the iron ore price volatility, BHP remains a solid exposure to both copper and nickel, but especially copper.

I currently hold S32 and FMG, but not BHP or RIO.

BHP is starting to look interesting, but I would be unlikely to get seriously interested in them again while they continue to retain those thermal/energy coal assets in NSW. One of the things I liked about S32 is that they said they would sell off their thermal coal assets, and then they did. BHP say they will, then they change their mind. I'm sure that's being driven by the higher coal prices and big profits available in coal at this point in the cycle, but I prefer a company like S32 that is looking further ahead and positioning themselves for that future.

BHP's Potash arm is a plus, and a big differentiator for them, but it's still 5 years away from production and they might end up changing their minds and selling it before then. Who Knows? They don't always follow through on what they say they're going to do.

On the other hand the board at S32 and Twiggy Forrest at FMG DO tend to do exactly what they say they're going to do, so you know what you're getting into a lot more with those two I think.

19-July-2022: BHP-Quarterly-Activities-Report-Q4-FY22.PDF

Commentary: Strong BHP performance undermined by Qld coal royalties - Australian Mining

Plain text link: https://www.australianmining.com.au/news/strong-bhp-performance-undermined-by-qld-coal-royalties/

Strong BHP performance undermined by Qld coal royalties

July 19th, 2022. By Ray Chan, AustralianMining.com.au

BHP's Olympic Dam operation in South Australia.

A strong fourth quarter has capped off a year of significant progress for BHP, with iron ore leading the way, generating record sales volumes for the 2021–22 financial period.

BHP sold 284 million tonnes of iron ore across the 12 months, as South Flank’s ramp-up to full production capacity (80mt per annum) tracks ahead of schedule.

An average rate of 67mtpa was achieved at South Flank in the June 2022 quarter, contributing to record production from the Mining Area C (MAC) hub and record lump sales.

BHP produced 253mt of iron ore in FY22, with the Western Australia Iron Ore (WAIO) operations making up 249Mt of that and Samarco the remaining 4mt, in line with BHP’s iron ore production from the 2020–21 financial year.

The company said the performance had been underpinned by safe, reliable operations and firm demand for its commodities.

Chief Executive Officer Mike Henry said the year was once again fatality-free and BHP continued to improve safety issues, which included addressing sexual assault and harassment, racism and bullying.

“We delivered record full-year sales volumes at our iron ore business in Western Australia as a result of reliable operational performance and the South Flank project,” he said.

“In copper, Escondida in Chile had record material mined and near-record concentrator throughput, while Olympic Dam in South Australia performed strongly in the fourth quarter after planned smelter maintenance.”

Henry said Queensland metallurgical coal delivered strong underlying performance for the quarter in the face of significant wet weather.

As well, BHP is assessing the impacts on BMA economic reserves and mine lives as a result of the increase in coal royalties by the Queensland Government.

“The near tripling of top end royalties has worsened what was already one of the world’s highest coal royalty regimes, threatening investment and jobs in the state,” he said.

“Also during the year, we merged our petroleum business with Woodside, completed the sales of BMC and Cerrejón, and decided to retain New South Wales Energy Coal until the cessation of mining in 2030 subject to relevant approvals.

“We also unified our corporate structure, and added to our global options in copper and nickel.

“Broader market volatility continues and we expect the lag effect of inflationary pressures to continue through the 2023 financial year, along with labour market tightness and supply chain constraints.

“Over the year ahead, China is expected to contribute positively to growth as stimulus policies take effect, however, the continuing conflict in the Ukraine, the unfolding energy crisis in Europe and policy tightening globally is expected to result in an overall slowing of global growth. Our strong focus on safety, operational reliability, cost control and social value will help us navigate these challenges and continue to deliver for all of our stakeholders.”

--- ends ---

About Ray Chan

Editor of industrial titles and mastheads with Prime Creative Media. Publications include Rail Express and Australian Mining (web content). View all posts by Ray Chan →

-----

Disclosure: From Bear77: I don't currently hold BHP shares, although I do sometimes hold them. I currently prefer FMG for iron ore exposure and S32 (which was spun out of BHP) for base metals and silver exposure.

Increase in QLD coal mine royalties could be a risk for BHP as they have met coal assets in Bowen Basin.

Is it possible that the biggest short in the history of BHP was a big mistake? In hindsight it certainly seems that way?

On the 28 January BHP was the most shorted stock on the ASX with a whopping 17.63% of shares shorted. The shorts spiked by an incredible 7.18% in just one day on the 28 January 2022 (www.shortman.com.au). Why?

Stephen Bartholomeusz explained why BHP was sold short prior to the unification (The Sydney Morning Herald, 19/01/2022).

‘For most of the two decades since the formation of the dual-listed structure (although not always) the Plc shares have traded at a material discount to Ltd’s, generally in the mid-teens although it has been as much as 20 per cent.’

Following the LSE delisting a Plc share had exactly the same rights and entitlements to earnings and dividends as a Ltd share – providing a windfall to Plc shareholders as the historic discount is wiped out by unification.

That largely happened early on. From the moment unification was announced Ltd shares have fallen and Plc shares risen.

What was a Plc discount of 21 per cent immediately ahead of the unification announcement has been closed to less than 3 per cent as arbitrageurs sold BHP shares short and bought Plc shares that they will use to cover their positions, at tidy profits, once the unification is complete.

Ltd shares have fallen about 10 per cent and Plc shares have risen about 3 per cent since the corporate restructure was announced.

BHP’s independent expert, Grant Samuel thought there could be as many as 450 million shares sold as British and other foreign shareholders exit the register.

Against that, BHP’s weighting in the ASX has increased materially, from about 6.2 per cent to about 10 per cent. Australian index investors and those funds benchmarked against the ASX indices have been be buyers.

Now the register has settled, the unified BHP is trading on its performance and prospects. Unification has had no material impact on either.

What happened on the 28 January?

The BHP Plc Scheme (Unification) became effective on 28 January 2022. Plc Shareholders (BHP shares listed on the LSE) received one New Limited Share for each Plc Share they held.

Despite the 7.18% jump in short positions on the 28 January coinciding with the unification, the BHP share price increased by 2.7% to $46.92. It would seem the impact of short activity on the 28 January was outweighed by a BHP buying spree.

Normal trading in New Limited Shares on the ASX as a result of the unification under the ticker “BHP” commenced on 2 February 2022. The BHP share price closed at $45.64, again it was up on the previous day.

After 3 days of normal trading (Friday, 4th Feb 2022) the BHP share price closed at $46.81. There were still no signs of a collapse in the share price as a result of the unification. Why?

In my view the 21% discrepancy between the BHP Plc share price (LSE) and the BHP LTD (ASX) immediately prior to the unification announcement share price has already closed. Funds were quick off the mark in discovering there were huge profits (20% in fact) to be made by selling down BHP Ltd shares and buying BHP Plc shares.

This all happened very quickly after the announcement. In less than a week after the announcement the BHP Ltd share price had dropped from $52.81 to $44.46.

What happen with the Short Positions?

The unification of BHP did not collapse the share price as shorters were hoping for and this did not provide the opportunity to close positions at a profit.

Then on the 15 February BHP released an incredible 1H22 result with NPAT up 144% pcp.

Iron ore prices are trending up again and the future prospects are looking good.

The BHP share price is now climbing toward $50.

Since the unification of BHP Shorters have been scrambling to close positions, now almost non existent (0.56% on the 11 Feb).

To some extent I think shorters have helped to drive up the share price! Ouch, that must have hurt! :)

So in hindsight was the Big BHP Short just one Big Mistake?

1:24pm, 01-Feb-2022: There have been some isolated cases of Covid-19 in WA's mining industry, and BHP is one of the companies that has been affected.

COVID cases isolate dozens of WA mine staff - Australian Mining

At this stage, the management of all of the affected mines are saying there have been no material impacts to production. It does however feed into the skilled worker shortage that WA is experiencing. There are now even ads on Adelaide buses spruiking WA as a place with PLENTY of work, so worth considering a move over there. Seems out of step with their refusal to open their border and allow people in though.

I'm thinking that these conditions are very positive for a company like Mader Group (ASX: MAD) as long as they can keep their own workers Covid-free. Mader provide fitters and other skilled workers - especially heavy duty mobile and fixed plant mechanics - to various industries, but the mining industry is their bread and butter, with earth-moving/construction also providing MAD with plenty of work. My brother is one of those (HD plant mechanic) and he's working at S32's Worsley Alumina refinery (which was majority owned by BHP before the South32 spin-out/demerger). He doesn't work for Mader - he works for another labour hire company that also provides workers to the mining and minerals processing industries. Those labour hire companies are doing very well at the moment, especially in WA, and remember that WA only has a small fraction of people with Covid-19 compared to the eastern states and SA. If the Covid problem gets worse there, I reckon the labour hire companies are only going to get busier. They already have rising metals/materials prices as a tailwind, which is resulting in further activity in the sectors they operate in. I think Mader provides the purest exposure to that and I do hold Mader shares, and S32 shares - but not BHP at this point.

There's nothing investors hate more than confusion and uncertainty! Over the last 24 hours BHP served up a smorgasbord of confusion...and hey presto, look what's happened to the share price!

Only 2 weeks ago the BHP share price was an all time high of $54.06 and today it closed at $47.70, down 12% in just 14 days. What happened? Tristan Harrison from TMF posted a great Outlook Summary following the FY21 results announcement.

So, where do you start to make sense of it all? There are four big items in the mix right now:

- FY21 financial results

- US$5.7 billion capital expenditure approved for the Jansen Potash Mine

- Woodside Petroleum Business Merger

- Dividend declared, US$2.00 (AU$2.76), fully franked.

1. FY2021 Financial Result

What an incredible result! (see attachment):

- Underlying EBITDA US$37.4 billion (up 69%)

- Underlying EBITDA margin of 64%

- Underlying attributable profit of US$17.1 billion

- Attributable profit of US$11.3 billion

- Record FY dividend of US$3.01 cps

BHP reported that its attributable profit grew 42% to US$11.3 billion. That number included an exceptional loss of US$5.8 billion predominately related to impairments of potash and energy coal assets, and the current year impact on the Samarco dam failure.

BHP said that all divisions met earnings guidance.

Tristan Harrison (TMF) said the result was in line with what most analysts were expecting. Macquarie Group Ltd and UBS said the dividend was bigger than expected.

Based on the forecast 2022 earnings brokers had varying opinions according to Tristan. Macquarie has a price target of $58. It reckons BHP is valued at 11x FY22’s estimated earnings with a forward grossed-up dividend yield of 10.6%.

However, UBS says BHP is a hold with a price target of $42, even though it reckons the BHP share price is valued at under 10x FY22’s estimated earnings. UBS is expecting a higher FY22 profit than Macquarie.

If we averaged broker opinions the 2022 target price would be around $50 per share. This doesn't explain the closing price of $47.70 today.

2. Jansen Potash Capital Expenditure

BHP announced that it has approved US$5.7 billion of capital expenditure for the Jansen Stage 1 of the Potash Project in the province of Saskatchewan, Canada.

BHP believes Jansen will create value for shareholders for generations. Jansen is located in the world’s best potash basin and is expected to operate up to 100 years.

Potash provides BHP with increased leverage to key global mega-trends, including rising population, changing diets, decarbonisation and improving environmental stewardship.

Jansen S1 is expected to produce approximately 4.35 million tonnes of potash per annum, and has a basin position with the potential for further expansions. First ore is targeted in the 2027 calendar year, with construction expected to take approximately six years, followed by a ramp up period of two years.

At consensus prices, the go-forward investment on Jansen is expected to generate an internal rate of return of 12 to 14 per cent, an expected payback period of seven years from first production and an underlying EBITDA margin of approximately 70 per cent given its expected first quartile cost position.

Potassium is a future facing commodity with attractive long term fundamentals from multiple angles:

- The environmental footprint of potash is considerably more attractive than other major chemical fertilisers

- Conventional mining with flotation is more energy and water efficient than other production routes

- Traditional demand drivers of population and diet are reliable and slow moving

- Attractive upside over basic drivers exists due to the rising potash intensity-of-use needed to support higher yields and offset depleting soil fertility

- On top of the already compelling case, decarbonisation could amplify demand upside

- The industry’s 4th wave is underway: demand to catch-up over the course of the 2020s

- Demand is catching up to excess supply, and major supply basins are mature

- Price formation regime accordingly expected to transition from current SRMC to durable inducement pricing, with Canada well placed to meet market growth longer term at LRMC in the mid $300s

3. Woodside Petroleum Business Merger

I believe investors are most concerned about the Woodside-BHP Petroleum merger news.

Under the proposed transaction, Woodside will acquire 100 per cent of the issued share capital of BHP Petroleum International Pty Ltd in exchange for shares in Woodside which will deliver 48 per cent to BHP shareholders on completion. Woodside shares will be immediately distributed to BHP shareholders. Woodside will remain listed on the ASX with listings on additional exchanges being considered.

The merger is expected to be completed in the second quarter of the 2022 calendar year with an effective date of 1 July 2021.

Morgans notes that the Woodside merger removes growth opportunities for BHP. Though, it acknowledges that its balance sheet strength gives it mergers and acquisitions (M&A) optionality.

I think BHPs long term strategy to move away from fossil fuels and focus more on the key global mega trends including copper, nickel, potassium and iron ore is a positive step for the company.

4. Record Final Dividend

BHP has declared a record final dividend of US$2.00 per share fully franked, or AU$2.76. If you consider the value of the franking credits, this equates to AU$3.59. BHP trades ex dividend on 2nd September 2021.

The upcoming dividend is significant in the current value proposition for BHP. If you subtract the dividend value including franking credits ($3.59) from the current share price of $47.70 you are potentially buying BHP for $44.11 per share. Yes, the share price will drop when BHP goes ex-div on the 2nd September, but I think the share price will gravitate towards the consensus target price of $50 per share over time.

My take

I think BHP is worth considering at $47.70 with the upcoming dividend taken into account, and the move away from fossil fuels towards global mega trends is considered.

Disc: Held SM and IRL