Consensus community valuation

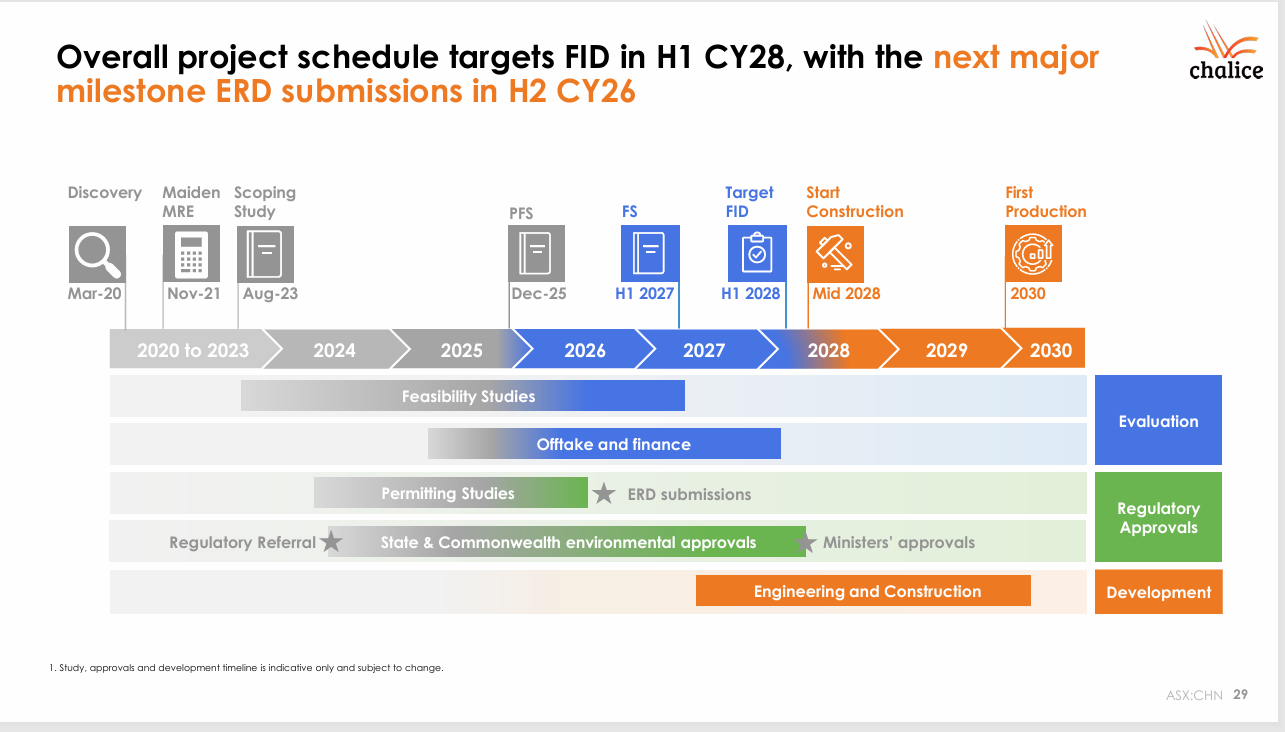

Funded to Targeted FID in H1 2028

/presentation-macquarie-australia-conference

2026-quarterly-activities-cashflow-report

some receipts from customers shown:

Funded to Targeted FID in H1 2028

some recent share price slippage:

Preprofit phase ( hopeful for profit 2030) Towards 2030

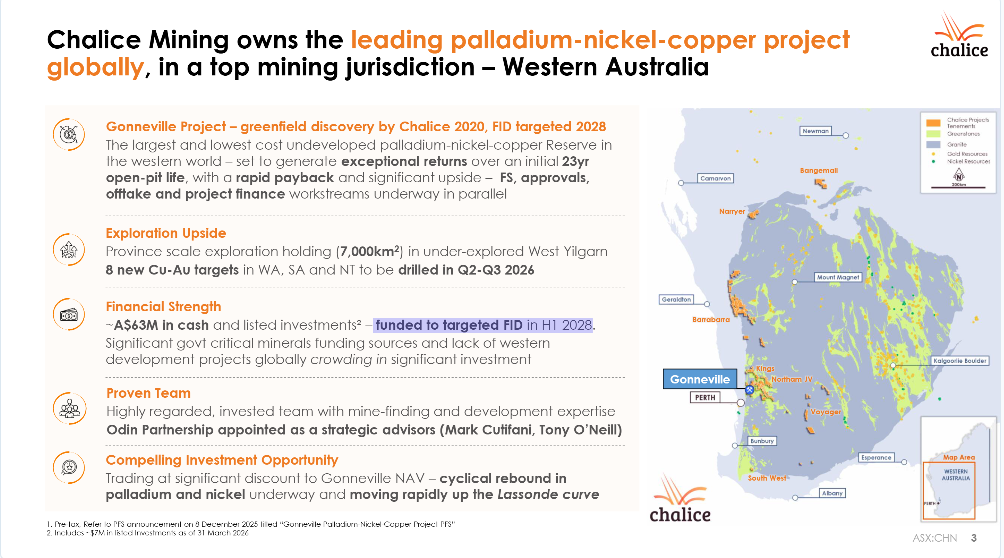

Chalice owns the leading palladium-nickel-copper development project in the western world – one of the standout critical minerals projects globally, funded to FID in H1 CY28

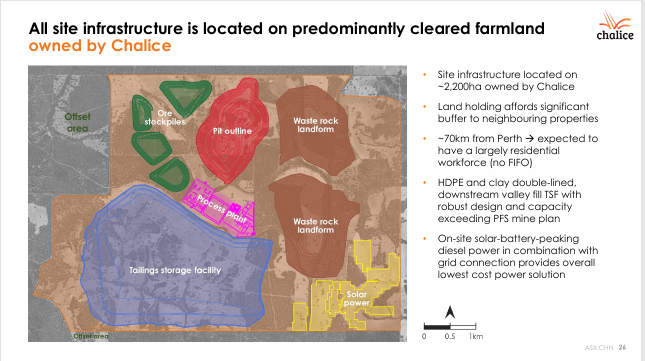

70km form Perth should be cheaper

..But the local council could install metered parking and that could bugger the whole project ..lol .. joke

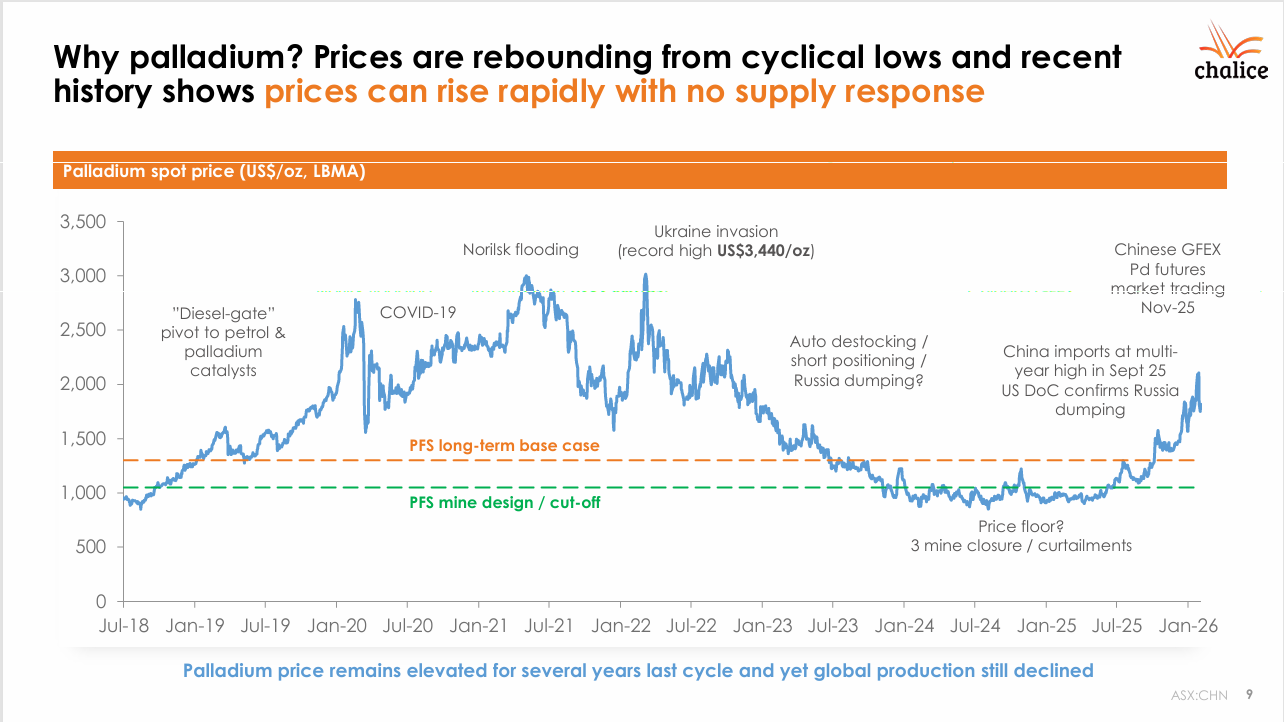

Palladium price holding up. Can depend on international Diplomacy .. someone rippon someone off!

Towards 2030 execution .. Can the Board deliver?

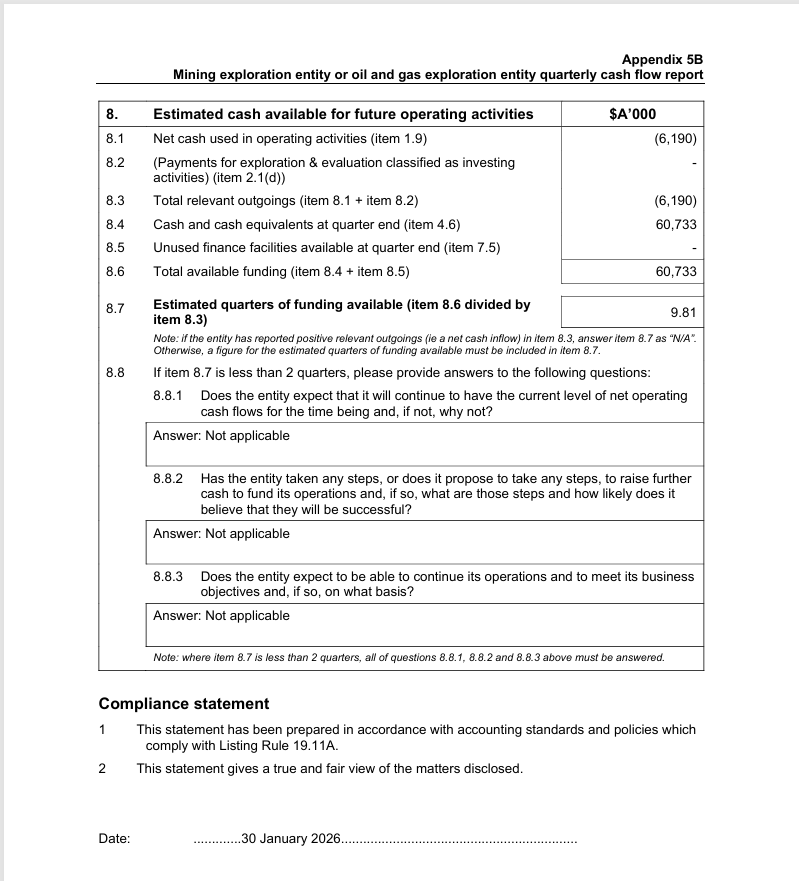

At December 2025 Quarterly activities Report

The Bank account has cash available ..Tick

Copilot research Below:

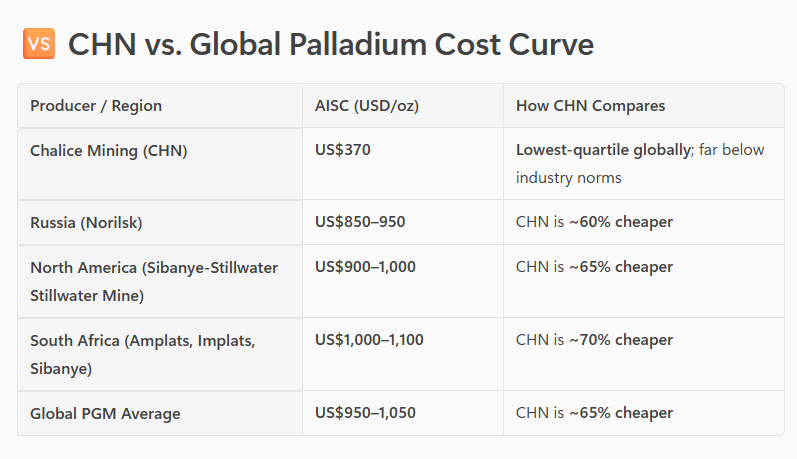

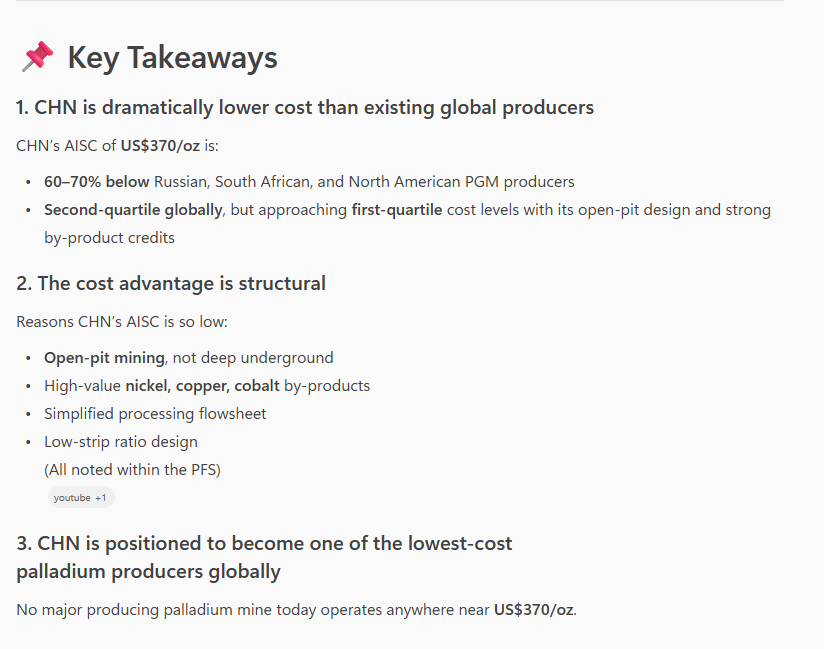

CHN AISC/oz is anticipated to be World low cost operation as per the list below:

Mkt cap $716.6M

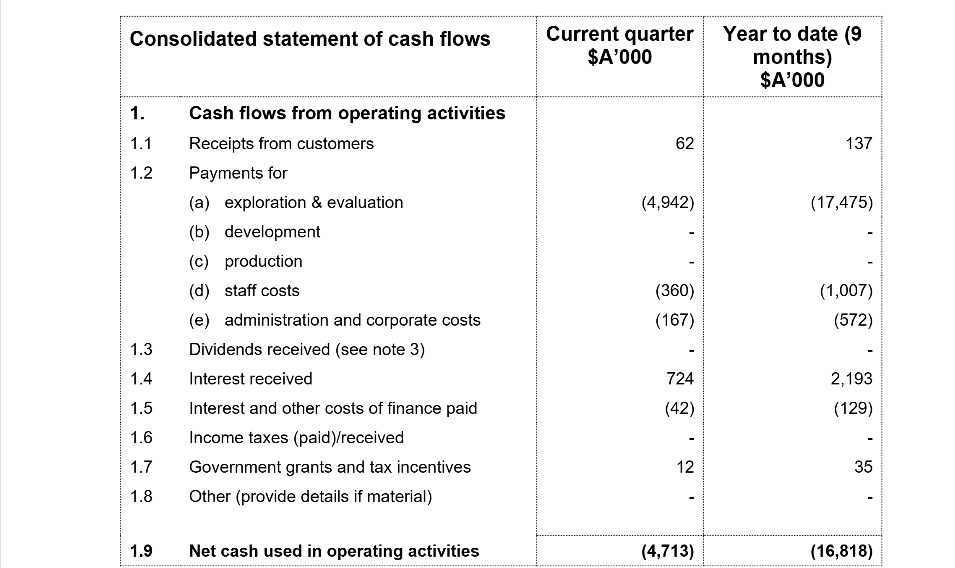

Statement of Cash Flows Cash and cash equivalents at 30 June 2025 were $70.8 million (2024: $88.9 million). Cash used in operating activities reduced from $44.1 million to $17.8 million, primarily due to a reduction in cash flows associated with exploration and evaluation expenses of $23.9 million and a reduction in cash paid to suppliers and employees of $1.6 million.

Net cash used in investing activities decreased significantly during the financial year, predominantly due to the acquisition of a private property and financial assets in the prior financial year.

On the corporate front, disciplined financial management saw FY25 operating cash outflows reduced to $18 million – the lowest level in six years

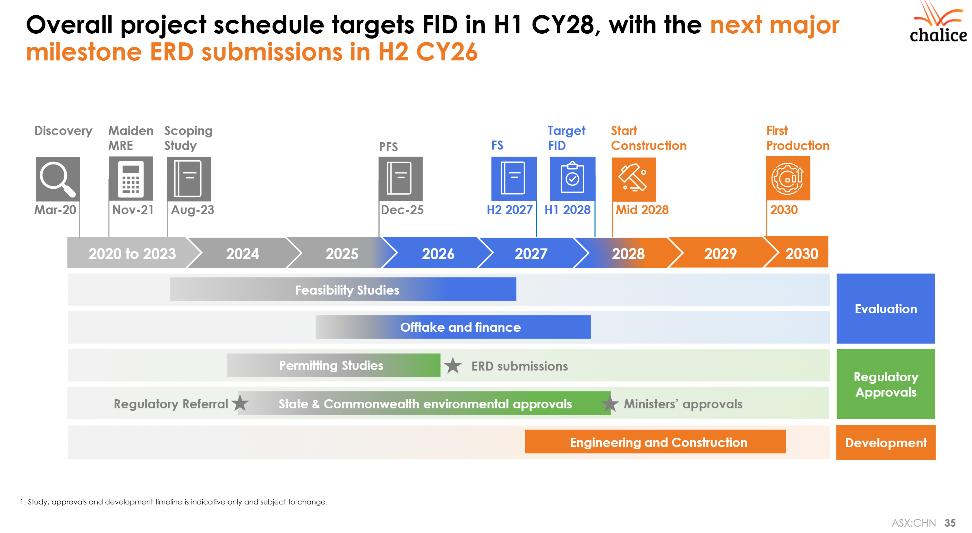

– adapting to lower commodity prices and preserving our strong cash and listed investment balance of $78 million. This strong position ensures we are well funded through to a Gonneville Final Investment Decision targeted for late CY27.

Gonneville is forecast to generate ~45-50% of its revenue from palladium,

The outlook for Chalice With a strong balance sheet, Chalice is well funded to advance Gonneville to a Final Investment Decision in late 2027, while continuing to explore priority targets. Anticipated milestones in FY26 include completion of the PFS, commencement of financing discussions, progression of offtake negotiations and submission of the Environmental Review Documents to regulators for major environmental approvals.

Return (inc div) 1yr: 71.07% 3yr: -14.19% pa 5yr: 0.90% pa

CHN liquidity average traded daily : $3,000,000

Palladium

Gonneville is the largest palladium-nickel-copper resource in the Western world, a 17Moz 3E PGE, 960kt Ni, 540kt Cu, and 96kt Co open-pit project .

Early indications of price recovery but spot price still well below marginal cost of supply (~US$1450/oz)

https://hotcopper.com.au/threads/ann-presentation-diggers-and-dealers-mining-forum-2025.8696626/

The resource so supply and Demand:

Palladium fell to 1,187.50 USD/t.oz on August 5, 2025, down 2.10% from the previous day. Over the past month, Palladium's price has risen 5.74%, and is up 40.70% compared to the same time last year, according to trading on a contract for difference (CFD) that tracks the benchmark market for this commodity.

about:

Palladium is a soft silver-white metal used mostly in the production of catalytic converters for petrol cars, electronics, dentistry, medicine, hydrogen purification, chemical applications, groundwater treatment and jewelry. The biggest producers of palladium are by far Russia and South Africa (70-80% of world output) followed by United States, Canada and Zimbabwe. Palladium Futures are available for trading in London Platinum and Palladium Market and on the New York Mercantile Exchange. The standard contact weights 100 troy ounces.

asx CHN Return (inc div) 1yr: 53.85% 3yr: -30.66% pa 5yr: 8.50% pa

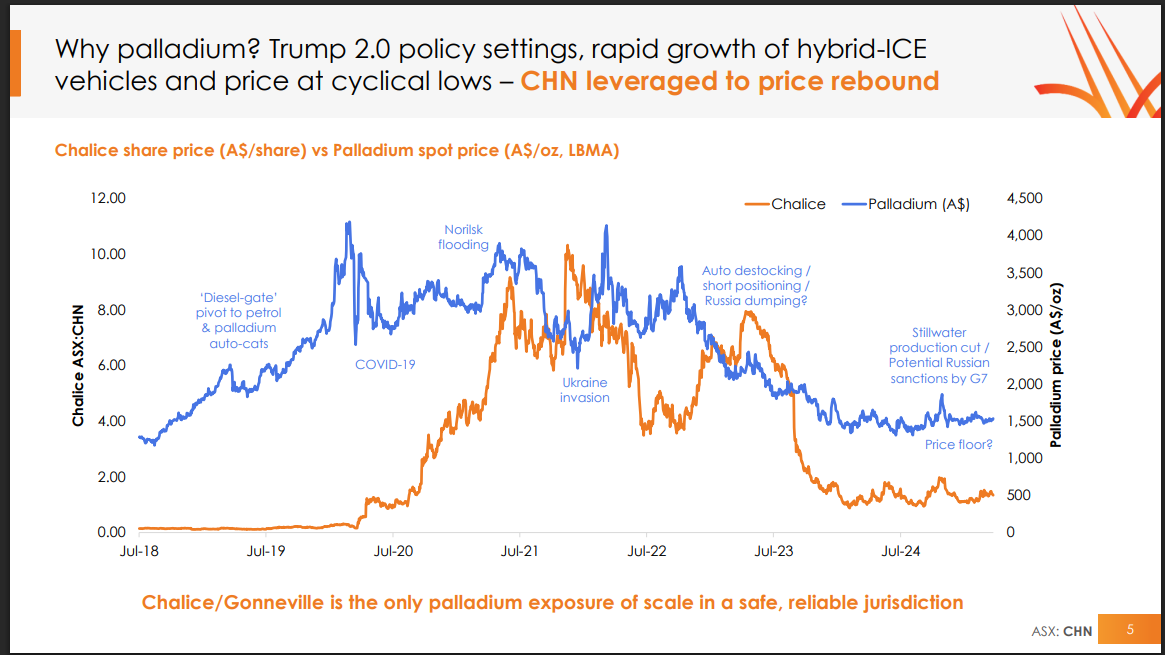

*The Charts - Palladium chart and the CHN have both declined

Cost of supply has a cost gap of (not profitable!) 23% = 1450 / 1182

$1450 IS COST OF SUPPLY AS ABOVE

30/07/25 08:25

This had a great run... on the back of the palladium price

CHN. Return (inc div) 1yr: 39.74% 3yr: -30.86% pa 5yr: 10.02% pa

Held RL

Palladium just needs to break through the year-long $1065 resistance level.

chart below at 7/6/2025:

Tuesday 10th market price up at open.

Last

$1.43

Change

0.150(11.8%)

Mkt cap !

$496.0M

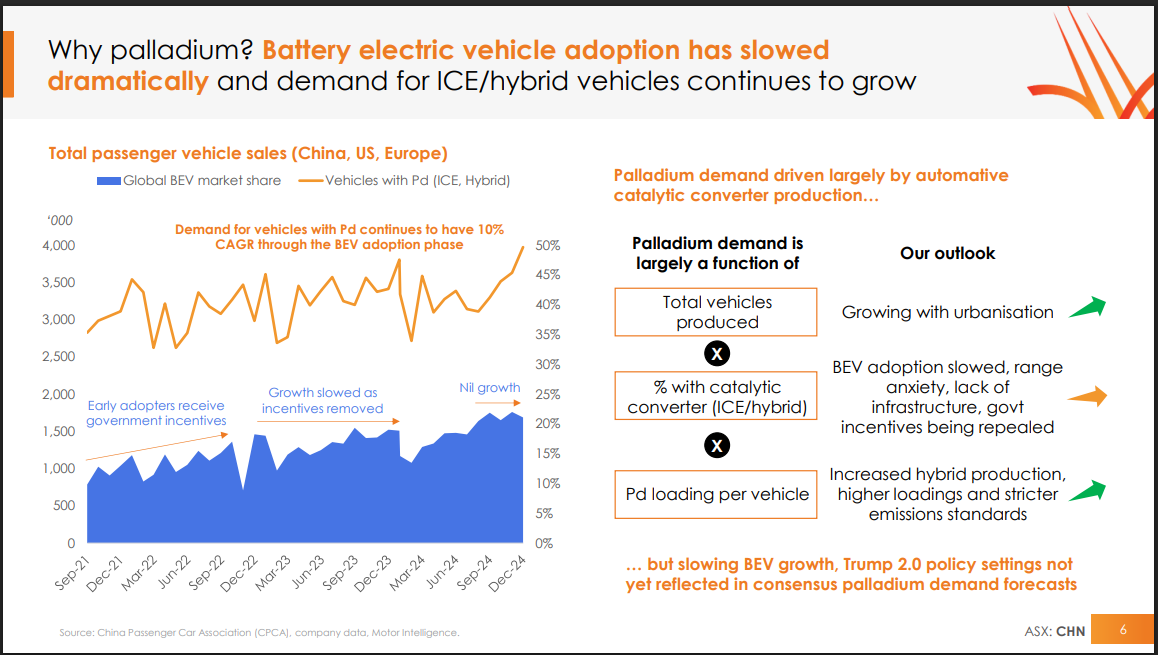

And the 'bias' is that hybrids (PHEV) are the go to now vs Battery (BEV), Gov policy 'belief' ..

..............We need cars still !!! .. though Amazon deliverers our parcels ..jejeje

https://hotcopper.com.au/threads/ann-presentation-macquarie-australia-conference.8569029/

at 06/05/25 08:34

- Presentation - Macquarie Australia Conference

https://hotcopper.com.au/threads/ann-promising-early-stage-gold-results-in-the-west-yilgarn.8598987/

significant suture of the South West and Youanmi terranes, including 1m @ 6.6g/t Au:

Gold-copper focused exploration in the Province remains at an early stage, with targeting for goldcopper systems continuing, drawing upon all available datasets including high-quality airborne magnetics, gravity and EM survey data acquired by Chalice from 2021 to 2023 following the discovery of the tier-1 scale Gonneville PGE-Ni-Cu-Co deposit.

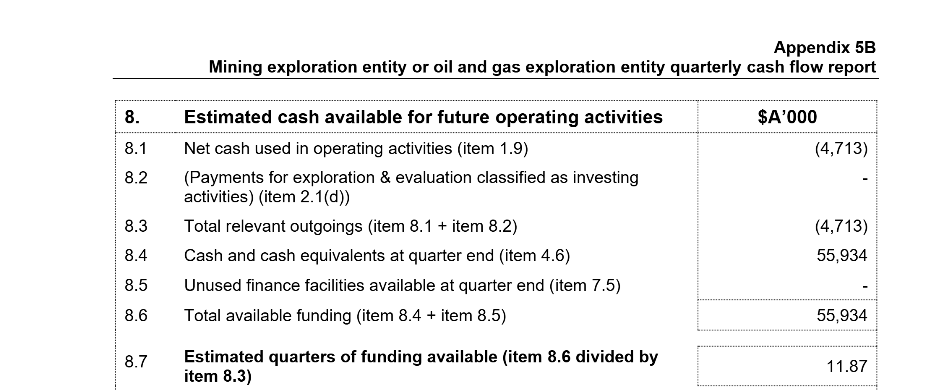

is there any cash in the bank? 18.24 quarters..

- March 2025 Quarterly Activities & Cashflow Report

Last

$1.21

Change

-0.035(2.82%)

Mkt cap !

$466.8M

Suitors Reportedly Prepare to Lob Bids for Chalice

Suitors lining up for $2.3 billion nickel explorer and developer Chalice Mining Limited (ASX:CHN) are preparing to lob their final offers by August 21, sources say. The company's main project is its Julimar nickel and copper project in Western Australia's Avon region, 70km northeast of Perth. The group's Gonneville deposit is one of the world's nickel sulphide discoveries. It reported a net loss of $33.7 million for the six months to December and is looking for a backer to fund its development through Standard Chartered. But some believe the process could result in an acquisition of the company as a whole. Sources say Chalice is open to several options including a partial sale of about 20% of the group, or 100%. The king maker is Founding Chairman Tim Goyder, who owns just over 8% of the business. He has proved a tough negotiator on price, based on the experience of Albemarle, which has been courting Liontown. Mr. Goyder, who stepped down as the Chairman of Chalice Mining in 2021, also owns 15% of Liontown. Albemarle, the world's lithium producer, offered $5.5 billion for that company, currently worth $6 billion, but that was rejected. Anglo American plc (LSE:AAL), South32 Limited (ASX:S32), BHP Group Limited (ASX:BHP) and Rio Tinto Limited are expected to be lining up for Chalice's platinum metals assets. Some experts say the big players will be obliged to look at the asset, simply given the size of the resource, but the project is not yet in production and will take a long time from an environment point of view. The world's platinum producer, Sibanye Stillwater Limited (JSE:SSW), could also be in the mix.

Surprised IGO isn't on the list. Anglo seems a logical fit given their ground is nearby.

[held]

Continually impressed by Capital IQ Pro. Only found out tonight how to overlay claims between 2 companies Western Yilgarn and Chalice which is very useful.

Bit of competition here. Chalice in Red. Western Yilgarn in Blue

While Western Yilgarn has applied for E70/5111, Chalice has applied for E70/6255 which overlaps the former when I remove Western.

Western Yilgarn claims that E70/5111 has some lithium but won't know until they drill also implying E70/6255 has that too. Even then the application is still pending so a risk there for Western Yilgarn than Chalice.

Another note is I think Chalice is delaying the study because they know the resource can only get bigger. I think releasing a study now will undervalue the project. On the other hand it is disappointing we don't know the economics yet.

[held]

Capital raising for retail fell short of target.

But good to see directors including the CEO Alex Dorsch putting some money into the raising. That is better than some of the other recent raisings where the CEO did not subscribe to any shares (but will not mention any names here for now).

Source: marketindex

On another note, UBS put a sell rating on CHN citing concerns on palladium demand forecasts

[held]

After an anticlimax with environmental groups, Chalice secured approvals for drilling of Hartog in the Julimar State forest

https://www.afr.com/companies/mining/chalice-wins-permission-to-drill-in-wa-state-forest-20220519-p5amvy

Shares rallied 19%

For those that want background information on the opposition groups and a map of Hartog, there is a great article in AFR (behind a paywall)

https://www.afr.com/companies/mining/chalice-asks-opponents-to-see-the-forest-for-the-trees-20220502-p5ahop

Further drilling on the farmland since November has suggested the resource contains even more platinum, palladium, nickel and copper than was understood in November.

But the big hope for Chalice shareholders – and the big concern for opponents such as Kinsella – lies in what a helicopter found just six kilometres north of Gonneville in September 2020.

As it surveyed terrain inside the forest boundary for the type of magnetic signals that bounce off underground metal deposits, the helicopter received signals from several spots inside the forest boundary.

One of those signals was “significantly stronger” than Gonneville had produced when it was the subject of aerial surveys, and the location of that signal has since been dubbed “Hartog”.

The magnetic signals picked up by aerial surveys do not guarantee the presence of valuable minerals, but where there is smoke there is often fire, and Hartog is now one of Australia’s most eagerly anticipated exploration targets.

The investment community swiftly formed the view that if Chalice could get inside the forest to drill Hartog, it would likely prove that Gonneville was the tip of an iceberg whose richest parts were buried inside the forest boundary.

It’s a hypothesis that has turned pre-revenue Chalice into a $2.5 billion company and elevated its managing director Alex Dorsch onto the Financial Review Young Rich List.

But it’s also a hypothesis that will remain unproven until Hartog is drilled.

“We don’t know if anything is there yet.” stressed Dorsch, when asked about Hartog.

“I know the public is quick to associate exploration effort with mining and typically the mind goes straight to big, open-cut type of mining.

“We are many years away from knowing what sort of mineralisation is there, if any, as well as what style of mining it would be.”

The WA government has given Chalice permission to drill on the existing dirt tracks that firefighters and recreational users have carved through the forest.

But those tracks are nowhere near Hartog, nor the other targets identified by the helicopter surveys.

Permission to leave the tracks and push through the forest vegetation to drill the centre of the Hartog target looked to have been secured by Chalice in January, but the WA government permit has since been held up by five appeals from members of the public.

Community appeals

One of those five appeals was lodged by the Avon and Hills Mining Awareness Group, a community activist group that was formed to fight bauxite mining proponents in the region long before Chalice found Gonneville.

Kinsella was not one of the five, preferring to fight the project through other means.

Dorsch says it is not yet possible to judge whether the economic and environmental benefits of mining within the forest would justify the environmental impacts of the project, because the size and contents of the geology remains a mystery.

Held