22-Sep-18: This is just an update regarding the gold producers list I wrote about in another "Company Presentations" straw here.

Tribune (TBR) and Rand (RND) have announced during the past week that they have sold a large portion of the gold bullion that they had stored at The Perth Mint, and are returning that money to shareholders via massive fully franked special dividends. This has resulted in the share price of TBR rising 50% on Thursday and holding those gains on Friday, and RND rising almost 60% on Thursday and another 6% on Friday. I have full details of those dividends and the implications of them (and the risk that they may not proceed) in 3 "ASX Announcement" straws under Tribune Resources.

While our top 10 ASX-listed pure-play gold producers list hasn't changed, it has now grown to 11 (all with market values, a.k.a. market capitalisations, or market caps, or m/caps, of over $500 million), and the order of the next 7 (#12 to #18, all with m/caps between $200m & $500m) has certainly changed.

The main movers have been TBR (up 2 spots from #13 to #11) and RND (up from #22 to now be at #16). The list as of Friday's close, in market cap order, from biggest to smallest, of our seven $200m to $500m market cap gold gold producers is: WGX ($439m), PRU ($373m), SLR ($290m), RMS ($264m), RND ($242m), AGG ($231m), and AQG ($225m).

TBR has left those 7 behind for now - they should come back to the fold shortly as their proposed huge $3.50/share special dividend goes ex-div on Tuesday (25-Sep-18) which will undoubtedly result in a substantial share price fall - and the div might also be blocked or postponed by the Takeovers Panel; TBR have moved up into the $500m+ group for now, which was 10 companies but is now 11.

TBR is now #11 with a m/cap of $525m, nipping at the heels of DCN (Dacian Gold) which closed yesterday with a m/cap of $526m. Aurelia (AMI) has powered further ahead of DCN now and has a market value of $662m.

Those top 11 (all with m/caps of over $500m) are NCM, NST, EVN, OGC, RRL, SBM, SAR, RSG, AMI, DCN & TBR. The only change is the addition of TBR.

As I said, I would expect TBR to be back in the sub-$500m club soon enough, most likely Tuesday (25-Sep-18) when they are due to go ex-div for that $3.50 special dividend.

Back to DCN: To keep up to date with Dacian's latest presentations, you can check their website: http://www.daciangold.com.au/site/content/

Scroll down for their latest news and presentations.

Dacian released this today (6th July 2018) and rose 6.9%:

http://www.daciangold.com.au/site/PDF/1570_0/OperationalUpdate

Their most recent investor presentation was:

http://www.daciangold.com.au/site/PDF/1545_0/InvestorPresentationJune2018

Their homepage:

http://www.daciangold.com.au/site/content/

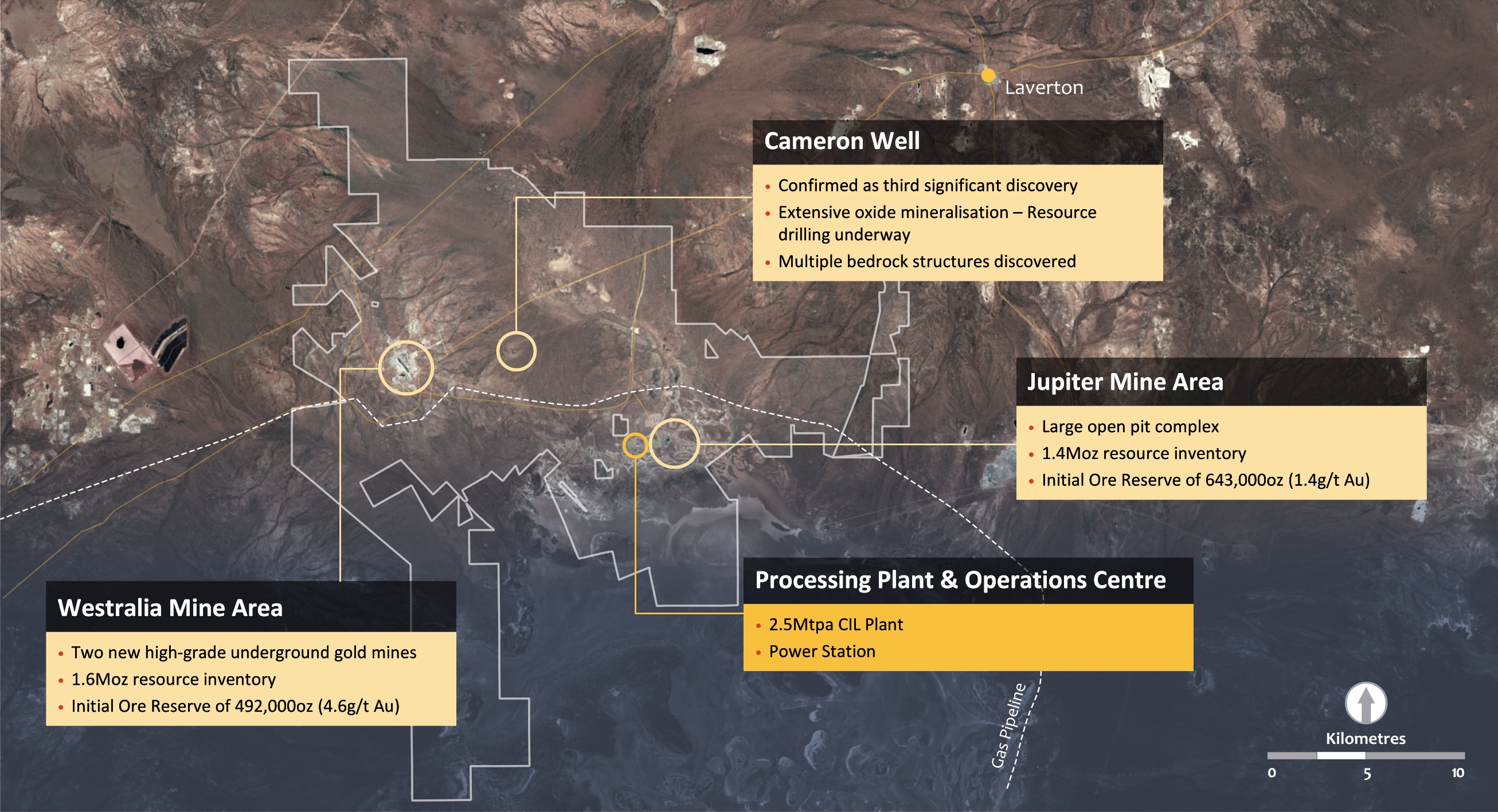

Their gold plant at Mt Morgans is operating as expected, and they're on track to declare commercial production next quarter (in the December 2018 quarter).

They are also busy looking for more gold.

6th January 2018: Additional: DCN spent 2018 mostly falling - from over $3 (in March/April) to under $2 in December. They are on the rise again now, already back to $2.72 and the NE trajectory looks very good. They kept saying that they would achieve MMGO (Mt Morgans Gold Operation) Commercial Production in December, but they haven't declared it yet - that announcement is due any day now. However, there has been plenty of good news, including the following as disclosed on December 18th:

MT MORGANS ORE RESERVE INCREASES 16% TO 1.4MOZ - see here

Extends Westralia Ore Reserve life to FY2025 and includes maiden 45koz Ore Reserve for Cameron Well as 3.5Moz Mt Morgans Project remains on track to establish 10-year life at +200,000oz pa

Key Highlights

- Total Ore Reserve for the Mt Morgans Gold Operation (MMGO) increases by 16% to 1.39Moz (net of mining depletion), increasing current production visibility to at least FY2025

- Westralia Ore Reserve increased by 17% to 575,000 ounces (net of 28,000 ounces mining depletion), extending Westralia’s current Ore Reserve life to 7 years (FY2025)

- Jupiter Ore Reserve of 611,000 ounces, maintaining Jupiter’s current Ore Reserve life to FY2025

- Maiden oxide Ore Reserve for Cameron Well of 45,000 ounces forms the basis for mine planning activities – paving the way for further expansion and production growth from Dacian Gold’s third production centre

- Numerous initiatives underway to continue growing Ore Reserves and Mineral Resources at Westralia including... see announcement for details (link above or click here)

Also, it is worth noting that MAH (Macmahon) have the mining contract for Dacian at Mt Morgans - see here and here. MAH are very experienced at gold mining. They do the mining at Telfer for NCM and at Tropicana for AGG & IGO.

Disclosure: I hold DCN and MAH shares.