01-Aug-2018: I meant to add the following to my last straw (in #Industry/Competitors):

Some of Downer's Competitors:

Cimic (CIM) and their various divisions are generally regarded as direct competitors of Downer, as are LendLease (LLC)..

RCR Tomlinson (RCR) in solar farms, railway signalling and electrical systems, minerals processing facility construction and operation, infrastructure construction, maintenance and operation, and various other areas.

All of the miriad of mining services companies compete directly against Downer's mining services division.

Hansen Yuncken, John Holland (which was purchased in 2015 by China Communications Construction Company International Holding Limited - CCCI), Watpac (ASX: WTC), Cimic (ASX: CIM, the old Leighton's, who also own Thiess), BGC Group, Fulton Hogan, CPB Contractors, Multiplex (owned by Brookfield, a Canadian private equity group), Laing O’Rourke Australia, Probuild, Nexus Infrastructure, ADCO Constructions, LendLease(ASX:LLC) and plenty of others - in non-residential construction.

Monadelphous (ASX: MND) in mining and engineering construction services, solar and wind farm construction, maintenance and operations, and especially in water infrastructure, oil & gas, and many other areas in which Downer operate.

There are plenty more.

One of Downer EDI's strongest areas is transport infrastructure construction, and they have a lot of competition there from both big, medium and small companies, including Lendlease (LLC), Probuild Civil, Abigroup, Fulton Hogan, Seymour Whyte, York Civil, Civil Mining and Construction (CMC), Ertech, Georgiou Group, VEC Civil, Guideline, John Holland, Burton Contractors, Golding (owned by NWH), CIM (Cimic), Boral (BLD) and a couple of overseas-based companies that operate here.

It's not easy to identify Downer's enduring competive advantages, if they have any. However Downer look like a reasonable sector play to me. Their issues with Spotless Group, and prior issues with the Waratah Trains contract in NSW are just two reasons why investors might still be a little hesitant to dip their toes back in this particular pond.

While LLC (LendLease) have been moving NE at a good clip for 6 months now, CIM and DOW have just begun to be positively re-rated by the market in the past month. There is likely more upside from here.

And I prefer DOW to CIM.

01-Aug-2018: Downer EDI are a $4.4 billion market-cap S&P/ASX-100 company that I think is going to report well this month, although I did think that about RCR Tomlinson (RCR) and I got that very wrong. Downer do the following:

- Road, rail & bridge construction and other transport infrastructure;

- Renewables, including solar farms;

- Mining Services, with a number of mining contracts with miners of various sizes, including BHP Mitsubishi Alliance, Glencore, Idemitsu Australia Resources, Karara Mining, Milmerran Power Partners, Newmarket Gold, Newmont, Rio Tinto, Roy Hill Iron Ore, New Century Zinc, Stanwell Corporation and Yancoal Australia;

- Infrastructure construction, maintenance and operations, the latter two providing recurring revenue which is good to see with a contractor;

- Industrial plant construction, maintenance and operations;

- Facilities Management;

- Power and Gas;

- Communications;

- Minerals Processing;

- Non-residential Building;

- Light Rail, Buses and other Transport Solutions;

- Airports and Ports;

- Water Infrastructure;

- Oil and Gas; and

- Defence.

http://www.downergroup.com/about-us

They've had a history of problems, including with Spotless Group, a recent acquisition, and with the NSW Waratah Trains in prior years:

I think that 2018/2019 is likely to be the year they get things right for a change, on the back of a massive increase in transport infrastructure spending, especially on the east coast.

Disclosure: I hold DOW shares.

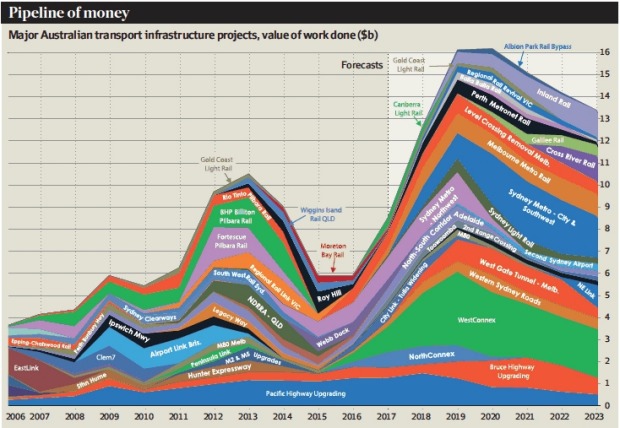

I've posted a more up-to-date "Major Australian Transport Infrastructure Projects" chart here in a different straw (under the same hash tag - #Industry/competitors). It was below (but they do move around a bit). The other chart shows more projects that have been added since the one above was created and just how busy 2019 and 2020 are shaping up to be. The bigger companies (like DOW, CIM, LLC) tend to dominate the larger contracts, but there will be plenty for everyone, and as the pendulum swings from too-many-companies-and-not-enough-work towards the other extreme (where there is a LOT more work, and companies can once again include some decent profit-margin in their quotes and tenders), we should see rates rise and profitability increase for companies like Downer.

Here's a more up-to-date Australian Transport Infrastructure Construction Project chart:

Source: Macromonitor construction materials forecast, February 2018 estimates. Presented at May 2018 Boral Investor Day.

http://www.livewiremarkets.com/wires/key-beneficiaries-of-the-24bn-infrastructure-pipeline