Consensus community valuation

Thanks@Wini for the nice write up on Livewire Markets: https://www.livewiremarkets.com/wires/three-asx-microcaps-taking-on-the-world

Even though I’ve had Nova Eye Medical on my watchlist since the Strawman Spotlight, I hadn’t been keeping my EYE on it! ;) I didn’t realise the share price had fallen so far since we looked at it 3 months ago. The Spotlight was a great analysis of the business and compliments @Wini’s latest write-up nicely.

Trading as low as 11 cps today, the risk reward for EYE is looking very attractive to me. There is slight possibility of a capital raise, however it is also very close to the inflexion point of profitability.

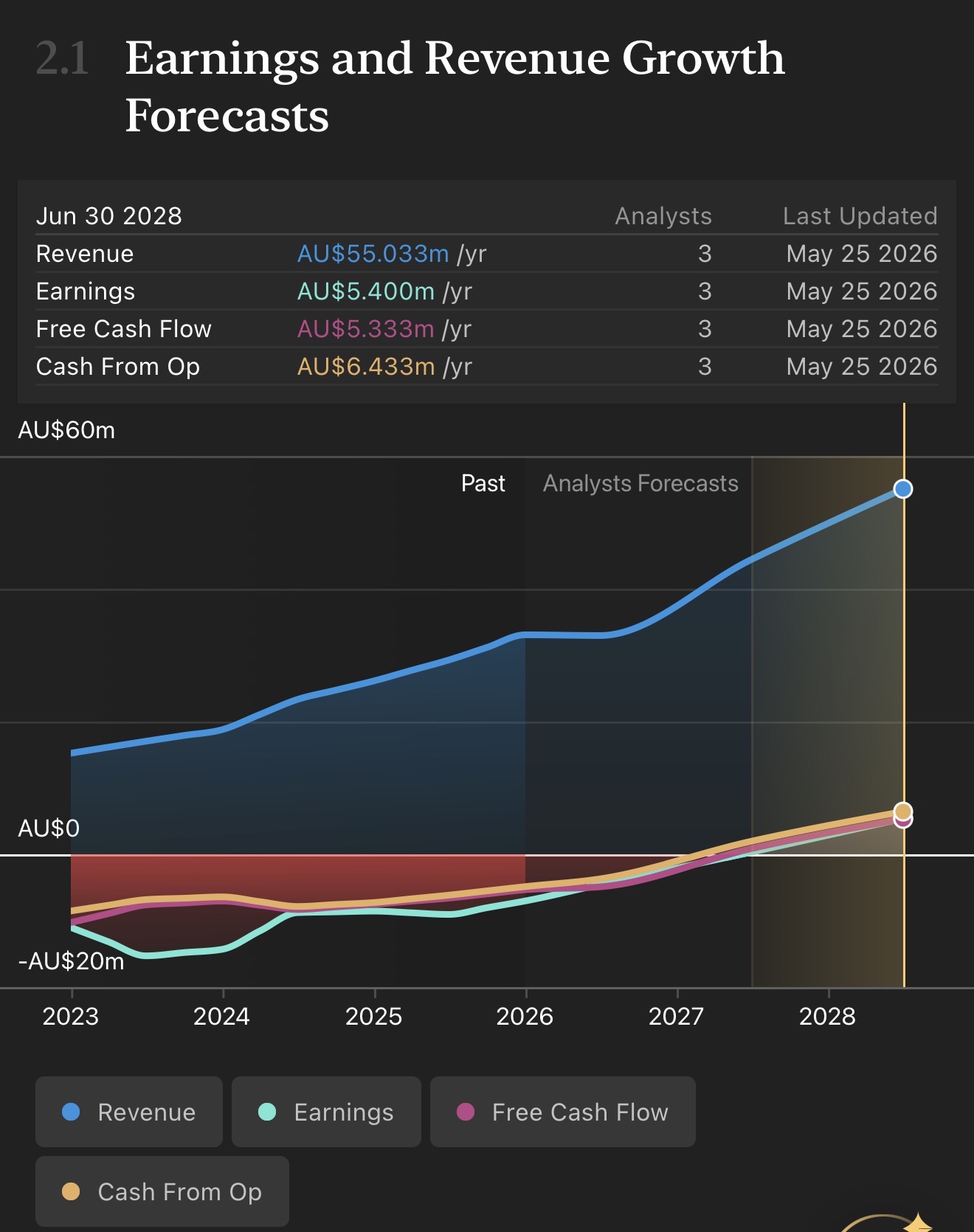

EYE is covered by a 3 analysts on Simply Wall Street; Bell Potter, MST Financial Services and Taylor Collision Limited. Two analysts have provided forecasts out to 2028.

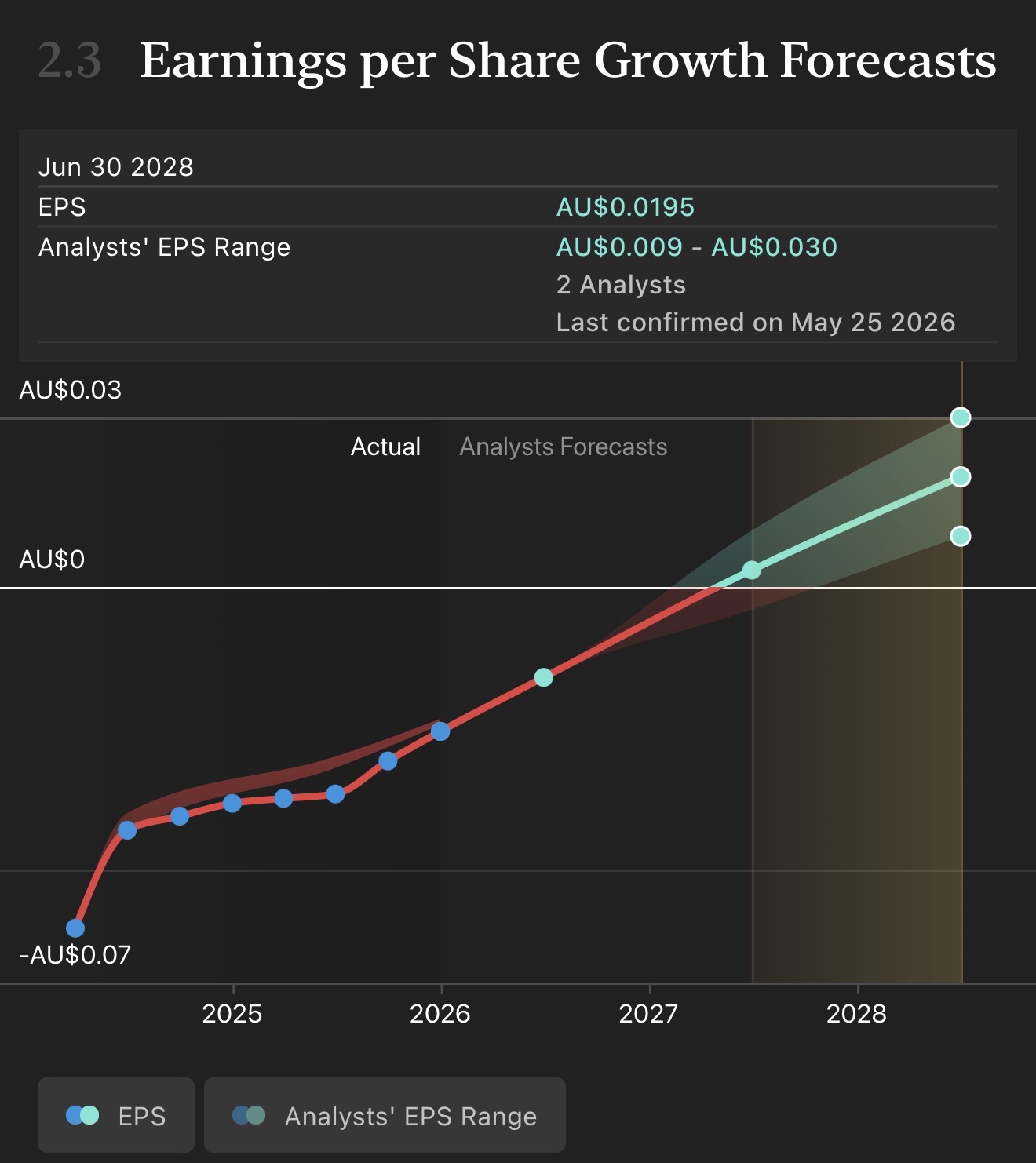

According to these analysts NPAT could be $5.4 million in FY2028, or 1.95 cps (consensus). At the rapid rate sales are currently growing at in the US I think this is entirely feasible.

For valuation purposes I’m going to assume EPS of 1.5 cps in FY2028. Current equity is $15.8 million, or 5.6 cps. On these assumptions ROE could be c. 27% in FY2028.

Using McNiven’s formula assuming 100% of earnings are invested back into growth at 27% ROE, and requiring a ROI on investment of 15% per year, I get a valuation of 18 cps. At the current price (11.5 cps) investors could potentially return 19% per year going forward. Of course all this depends on EYE’s sales and earnings trajectory remaining on track.

My wife has glaucoma and had a bad result following a Trabeculectomy over 10 years ago. The procedure reduced her eye pressure too much causing damage to the retina and some loss of eyesight. I like this technology because it is far less invasive and restores the eyes natural drainage system. I think it has huge potential globally. Today I took a decent size nibble. Thank you to @Wini and the Strawman community for the in-depth analysis on the business. It certainly helped with my investment decision today.

Held IRL

This is my first post on Strawman, so please be gentle. As you can see from my Strawman portfolio, I am in a learning phase :)

Over the last couple of months, I have been building a workflow and toolchain to develop investment thesis documents I can understand and use.

I use a NotebookLM notebook per stock to collect data, facts, and opinions, and then use the Notebook as a BA to answer questions from my thesis Analyst, Claude AI. I do this to try to ensure that Claude does not have to compress the chat and lose context because it has too many documents and data loaded. If the thesis analyst needs some data gaps filled, it provides me with a prompt to enter into the Notebook, and I either get the answer or look for the data to get it. So I am the BA's assistant

Workflow is:

- Collect the data and load up the Notebook

- Run a data completeness check prompt that evaluates data coverage

- Run 4 prompts to get data on

- Structure, Financials & Contracts

- Management Statements, Strategy & Track Record

- Ownership, Governance & Alignment

- Analyst Views & Market Context

- Run the Claude prompt with a template to ensure a repeatable process and output. Typically 3 cycles in the prompt, sometimes more if I miss data

- No data for the first cycle

- Add 4 outputs from the Notebook next

- Add missing data if available to improve data coverage

I have a Claude Max Plan and Google AI Pro plan

The Transcript from this week's call filled a number of data gaps I had.

Keen to understand whether this is of value or whether I have confused my AI assistants and myself.

Summary

EYE is a pre-profit ASX micro-cap medtech with a differentiated surgical device (iTrack Advance) in the growing canaloplasty segment of glaucoma surgery. The company is on a clear trajectory toward profitability: 6 consecutive halves of US sales growth at ~40% CAGR, 70% gross margins, 75% spare manufacturing capacity (confirmed near-zero capex to scale), and group EBITDA breakeven guided for H2 FY26. At 1.4x EV/LTM revenue, the stock trades at a massive discount to every relevant peer. The Strawman CEO call (16 Feb 2026) strengthened the thesis by confirming: (1) US ASP ~$1,000+ with all stakeholders economically aligned, (2) capacity expansion is labour-only with no material capex, (3) VIA 360 competitor does not have a glaucoma indication, and (4) AlphaRET partner structure would be non-dilutive. The bear case is a cash crunch and dilutive raise if breakeven slips — the CEO's indirect answer on capital sufficiency means this remains the #1 risk. The probability-weighted EV of A$0.35 implies ~119% expected return from current levels.

The thesis doc is quite long but the valuation is based on scenarios as per below. I am happy to share the lot to test out my workflow but maybe better in the AI discussion.

Scenario Analysis

Bear Case 1 — "Cash Crunch & Dilution" (15%)

Sales growth decelerates to <15% in H2 FY26. Opex doesn't flex. Cash falls below A$2M → forced placement at ~A$0.10-0.12. Target: A$0.08-0.10.

CEO gave an indirect answer on capital sufficiency during the Strawman call — cited ASX formula compliance rather than expressing direct confidence. This remains the #1 thesis risk.

Bear Case 2 — "US Growth Stalls" (15%)

RPR peaks. New surgeon acquisition slows. Competitors respond. Revenue grows but margin leverage doesn't materialise. Target: A$0.12-0.14.

Reduced from 20% post Strawman call: VIA 360 confirmed not indicated for glaucoma; capacity expansion confirmed near-zero capex; reimbursement economics confirmed healthy for all stakeholders.

Bear Case 3 — "Reimbursement / Regulatory" (5%)

Medicare cuts reimbursement for canaloplasty; or EU MDR blocks European access. Target: A$0.06-0.10.

Reimbursement economics (doctor/facility/device) are healthy and aligned for all parties, which provides some political protection against cuts.

Base Case — "Execution on Guidance" (42%)

FY26 revenue A$35-36M. EBITDA breakeven H2 FY26. FY27 revenue ~A$45M at 25% growth. No capital raise required. Target: A$0.35-0.45 at 2.5-3.0x P/S.

Base case logic: EV at 2.75x A$45M = A$124M → ~A$0.44/share.

Bull Case 1 — "Profitability Inflection + Re-Rate" (17%)

FY27 revenue >A$50M. EBITDA A$5-8M positive. Analyst coverage expands. Target: A$0.55-0.75 at 3.5-4.5x.

Strengthened by confirmed near-zero capex scaling; AlphaRET non-dilutive structure; 7% US share = A$60M as management aspiration.

Bull Case 2 — "China Upside" (10%)

iTrack Advance drives US$5-10M annual in China (3.6M cataract surgeries/year TAM). Target: A$0.60-0.80.

Bull Case 3 — "Drug Delivery / M&A" (5%)

Licensing deal or takeover. At ~A$46M EV for A$32M revenue at 70% GM with 100+ patents — objectively cheap on a take-private basis. AlphaRET partner structure confirmed as subsidiary-level equity (non-dilutive to EYE shareholders). Target: A$0.80-1.50+ (speculative).

Data Gaps and open Questions

Kill Switches (what breaks the thesis)

- Dilutive capital raise at >20% discount — placement below A$0.13 signals cash crisis

- US quarterly revenue turns negative YoY — core thesis is US growth

- Medicare reimbursement rate cut for canaloplasty — structural demand impairment

- MD or Exec Chairman sells on-market — insider signal of thesis failure

In prep for tonight's session on Nova Eye, I used Google Gemini's NotebookLM to create this 7 minute video summary.

This only uses material posted on Strawman and does not reference any external content, such as company reports, announcements or broker reports.

Of course, like most AI generated stuff, it's not perfect. But it does a reasonable job of capturing the general vibe of what members have said.

Let us know what you think.

Click the image to watch:

As I’m a bit over getting bullied by spec resources investors (*cough* @BkrDzn), I thought it might be worthwhile to filter out the gold price for a while and focus on an interesting microcap idea.

Like most microcaps that that have been listed for a while, Nova Eye Medical (EYE) comes with a rocky history. I won’t go too deeply into it given our friendly LLM junior analysts can do a pretty good job of summarising. But long story short EYE is the old Ellex Medical Lasers, who after selling their laser business to a French company in 2020, used the proceeds to fund the development and commercialisation of iTrack, a microcatheter used in canaloplasties of the eye to treat glaucoma. Messy history aside, EYE now appears to be a one product company and a much cleaner investment story.

The treatment of glaucoma is a big industry but is dominated by eye drops which make up 85-90% of the market. That said, minimally invasive glaucoma surgeries (MIGS) are growing, largely because a lot of patients are non-compliant with eye drops and glaucoma is a progressive disease where they eventually require surgical intervention. Improvements in MIGS technologies is also leading to many ophthalmologists to prefer surgical intervention sooner.

Within the smaller but growing MIGS segment the dominant solution is bypass stents to reduce the build-up of pressure in the eye. Stents have historically been 60-70% of the MIGS market, but with improvements in products and a preference for ophthalmologists to not leave hardware behind in the eye, canaloplasties are taking market share.

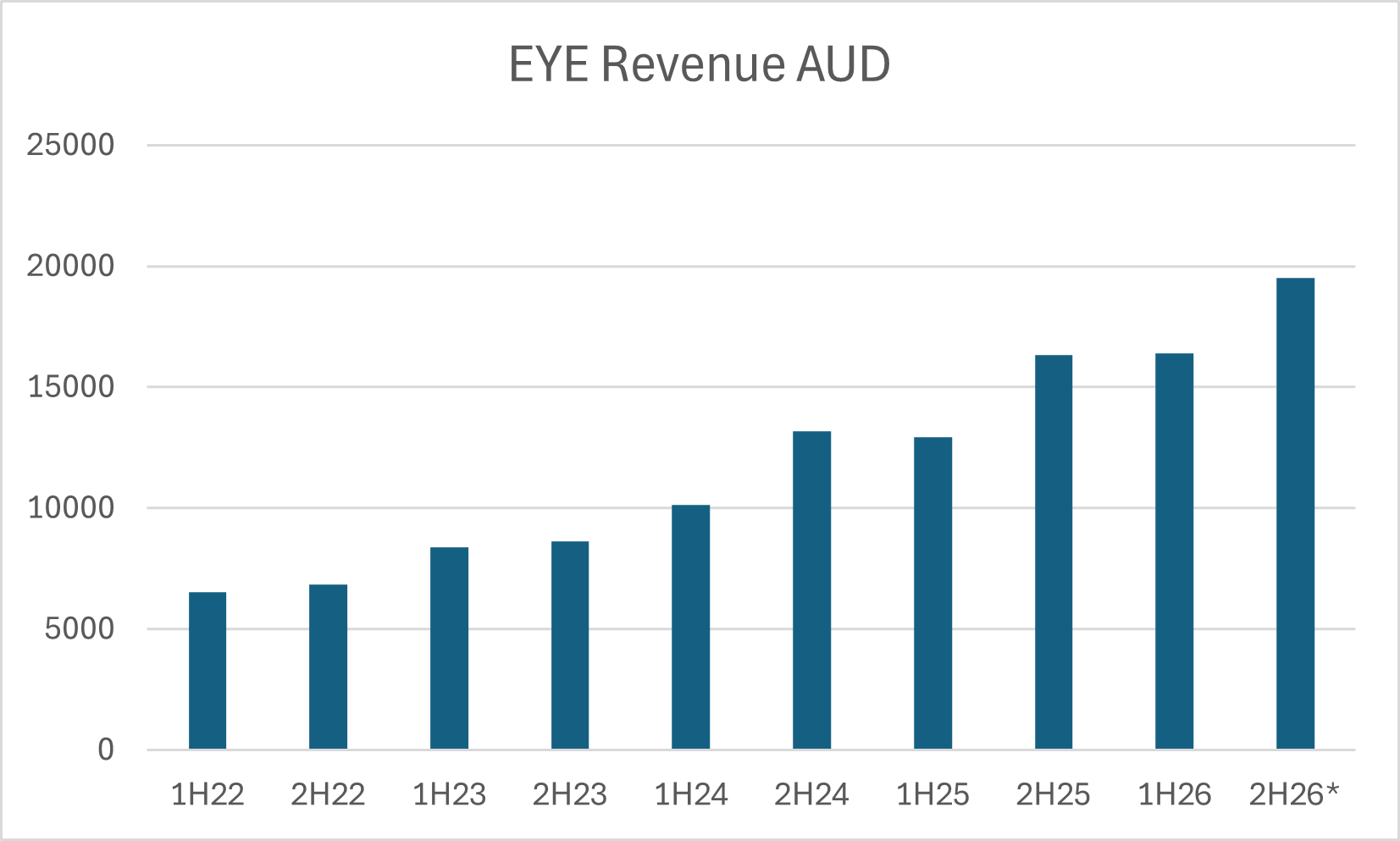

EYE’s original iTrack device had FDA approvals since 2008, but it wasn’t until the approval and commercialisation of the second generation iTrack Advance in 2023 where we started to see good sales traction, particularly in the US:

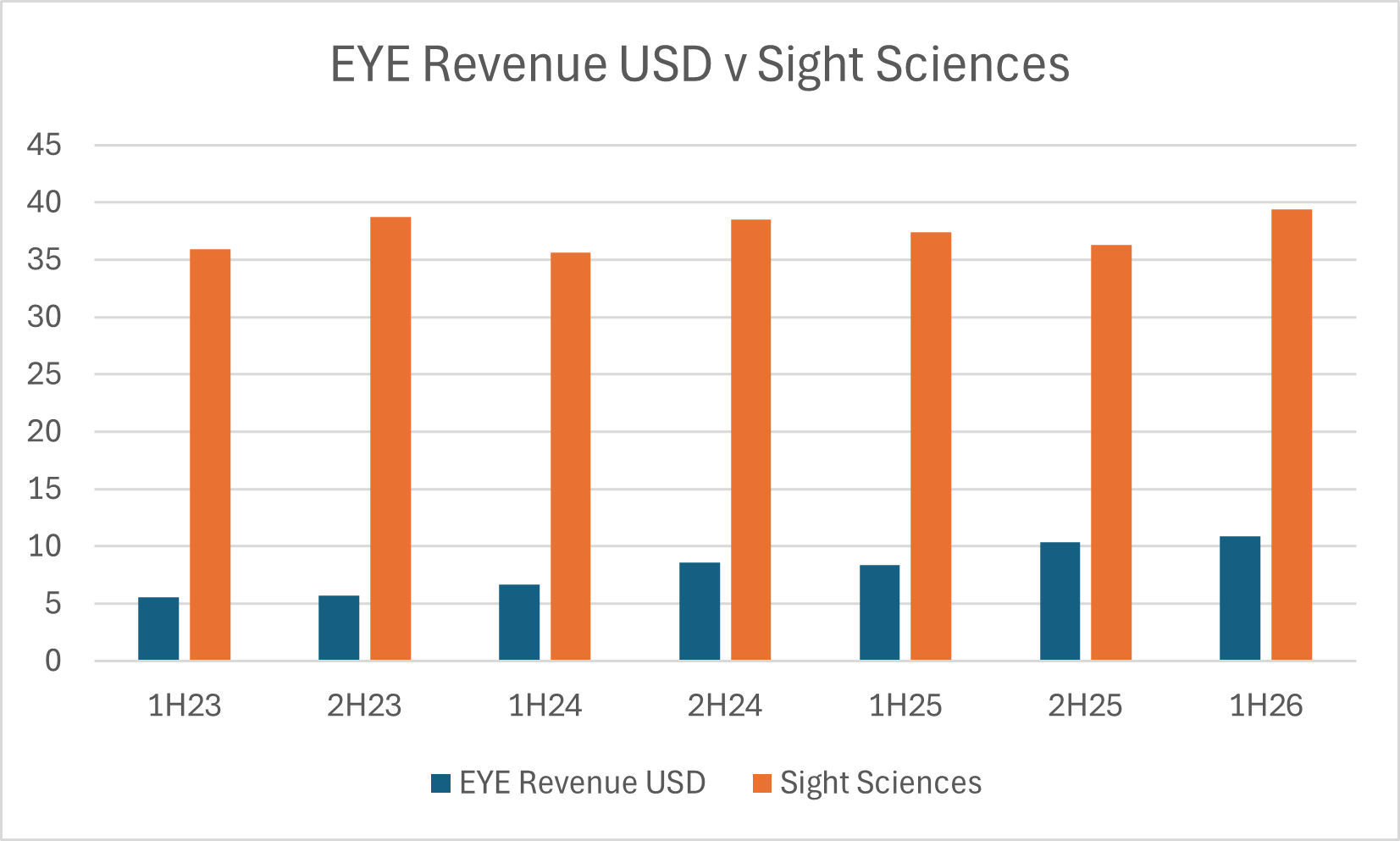

In the canaloplasty niche EYE effectively has just one competitor which is the Omni system produced by US based Sight Sciences. Fortunately, Sight Sciences is a listed business and we can track their glaucoma treatment segment over time and see how it compares to EYE:

Yes, it’s off a low base, but nonetheless it’s impressive to see EYE ~2x its revenue while Sight Sciences has largely been flat at the same time. It also supports EYE’s claim to be growing 3x faster than the broader glaucoma market.

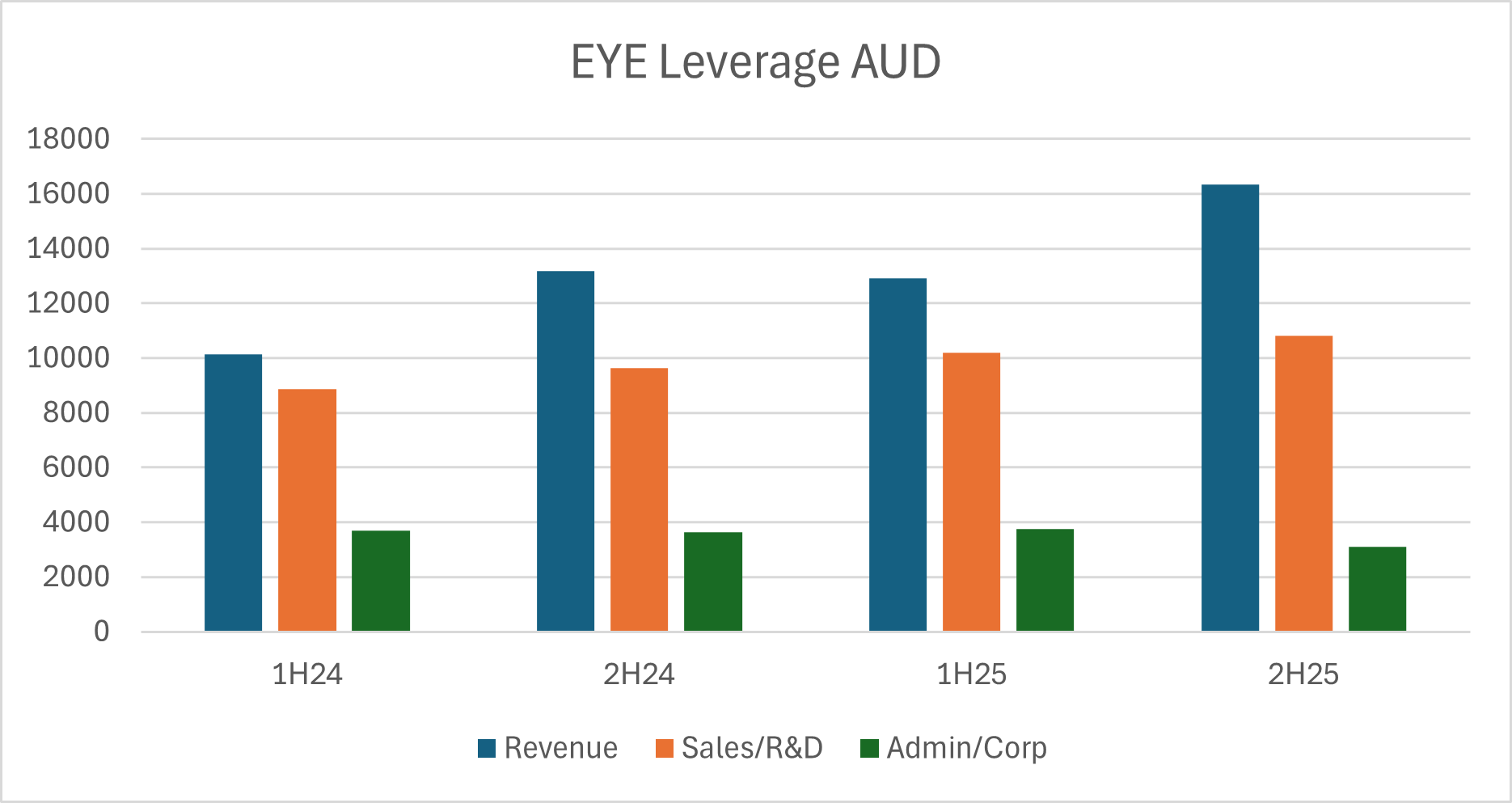

But we know what the market has wanted from microcaps for quite some time and that is profitability (or a clear path towards it). On that front EYE management has guided to EBITDA breakeven in 2H26, though it is worth noting that in the past this is a business/management that has missed targets and ultimately disappointed investors. That said, they have done a decent job in recent years of maintaining cost control while revenue has grown. It’s noteworthy that administration/corporate costs have been steady/falling with modest increases coming from sales/R&D:

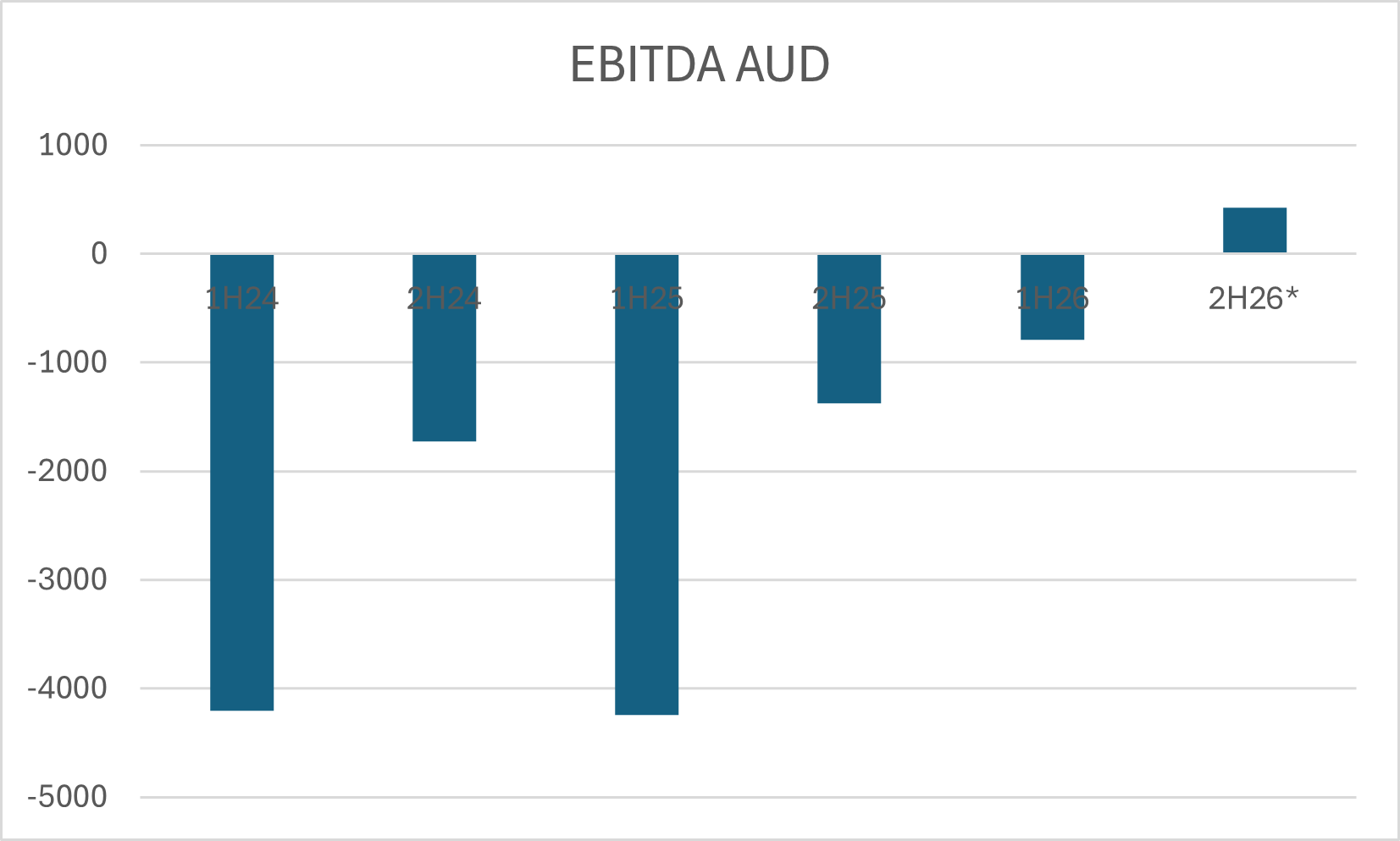

Assuming these cost trends continue and management land in the upper end of their guidance range, I think the target of EBITDA breakeven is achievable and would be a huge turnaround from the heavy operating losses of a couple of years ago:

Of course, despite being an interesting idea EYE is not short of risks. While they have shown consistently strong execution in their US sales since the launch of iTrack Advance, they need to continually invest in sales and R&D to maintain an advantage over larger peers with more resources. Changes to reimbursement is also a risk, right now reimbursement is $542 for surgeons and $2,231 for facilities which is supportive for MIGS growth, but reimbursement rates can change.

Finally, liquidity risk is real. EYE is tracking toward EBITDA profitability, but there is ~$1m in cash costs below that line in capitalised R&D and leases. At September EYE had $4m cash in the bank and a $2m working capital facility. The line between current cash liquidity and sustainable free cashflow breakeven is a tightrope, not impossible but it will require continued sales execution towards the top end of current guidance.

Ultimately, I think EYE is at an interesting point from an investment lens. A product gaining traction in the lucrative US market with high gross margins that can lead to genuine operating profit leverage as revenue scales over modest sales/R&D cost growth. The risk as we approach this key inflection is if US sales can't maintain its >20% revenue growth rate given the balance sheet may not be able to support any hiccups.

Would also love to get a view from the doyens of bio/medtech @mikebrisy and @Scoonieon this one!

Nova Eye pioneered the fastest growing segment in the burgeoning ophthalmic market; canal surgery for glaucoma, and holds over 100 patents in this domain

Nova Eye has invested in developing a next generation product (iTrackTM Advance)

The iTrack advance gained FDA approval of Friday 31 Mar. Shares jumped around 25% initially then pulled back for a 5% gain.

I notice there was some activity on strawman a few years ago. Perhaps some strawfolks are able to comment on these new developments;) With the original device still in use the new design should gain widespread adoption fairly soon and it will be interesting to hear progress on the rollout and uptake

Held SM and IRL