24th November 2025: Mulwarrie Met Results and Drilling Commenced.PDF

I mentioned here somewhere recently about the importance of Met Work - Metallurgical Test Work to determine recoveries using the proposed milling process - with project developers - especially in terms of helping them (and us) to try to work out future milling costs.

The Met work shows how effective their planned milling process is likely to be, and one of the biggest things to look for is their recoveries, which means the percentage of gold that their process successfully extracts vs how much gold there was in the ore to start with. The higher the recovery percentage, the less gold goes through the process and into their tailings without being recovered. Obviously you want the highest possible recovery, and anything over 90% is considered good, and 98 to 99% is considered excellent.

The main reason why most mills never achieve 100% recoveries (and are usually never designed to) is that the additional costs to build a mill capable of getting those 1, 2 or 3 extra percentage points of gold out of the ore often becomes prohibitively expensive, i.e. it usually doesn't make commercial sense to build a mill that is consistently capable of extracting 100% of the gold out of the ore, especially when the company is building their first plant (gold mill) and they don't yet have any cashflow from production - they have to find a happy medium where they get the vast majority of the gold out of the ore at a reasonably cost.

Plants (mills) are often designed with space around the plant to enable additional processes to be added later to either increase the mill's annual throughput rate and/or increase gold recoveries. This would typically be considered after the plant has been built, commissioned and ramped up to full nameplate capacity.

Today, GG8 said:

Source: First page of today's Mulwarrie Met Results and Drilling Commenced.PDF announcement from GG8.

To save time, rather than typing out my own understanding of the Average Gravity Recovery (44.5%) vs the overall average gold recovery (93%), I've asked Goggle AI to explain it - Google said:

Average gravity recovery is a component of the total average recovery in a gold project, representing the gold recovered specifically through gravity separation techniques, while total recovery includes both gravity and other methods like cyanidation. Metallurgical testwork establishes the total recovery percentage, which is then broken down into the contribution from each recovery method to understand the overall process efficiency.

How it fits together

- Total Average Recovery: This is the overall percentage of gold recovered from the ore, encompassing all recovery methods used in the processing plant.

- Average Gravity Recovery: This is a subset of the total recovery, quantifying the gold recovered by gravity concentration alone, such as using a gravity shaker table or centrifugal concentrator.

- The relationship: Total Recovery = Gravity Recovery + Other Recovery Methods (e.g., cyanidation).

- Purpose in testwork: Developers use metallurgical testwork to determine both the total recovery and the contribution of each stage. This allows them to:

- Optimize the plant design.

- Understand the process efficiency.

- Identify opportunities for improvement.

- Perform economic evaluations.

Example

- A project's metallurgical testwork might show a total average recovery of 93%, with an average gravity recovery of 44.5%. The remaining 48.5% (being 93% minus 44.5%) is recovered through other means.

--- end of Google text ---

I've changed the numbers in the example to reflect GG8's numbers above so the example applies to today's announcement.

In general, the more gold that can be recovered by the gravity circuit, the less chemicals are required for the other processes such as cyanidation, and the less chemicals required, the lower the costs are likely to be. Gravity recoveries can also help to inform the size that the other parts of the plant need to be, i.e. how large the cyanide leaching circuit (such as CIL / carbon-in-leach) and associated plant needs to be - to extract gold from the remaining ore pulp after the gravity circuit.

So it's good to see that there isn't anything nasty or concerning in this Met Work update for GG8's Mulwarrie gold project.

That's one more hurdle they've crossed on the way to Mulwarrie becoming a profitable gold producing operation.

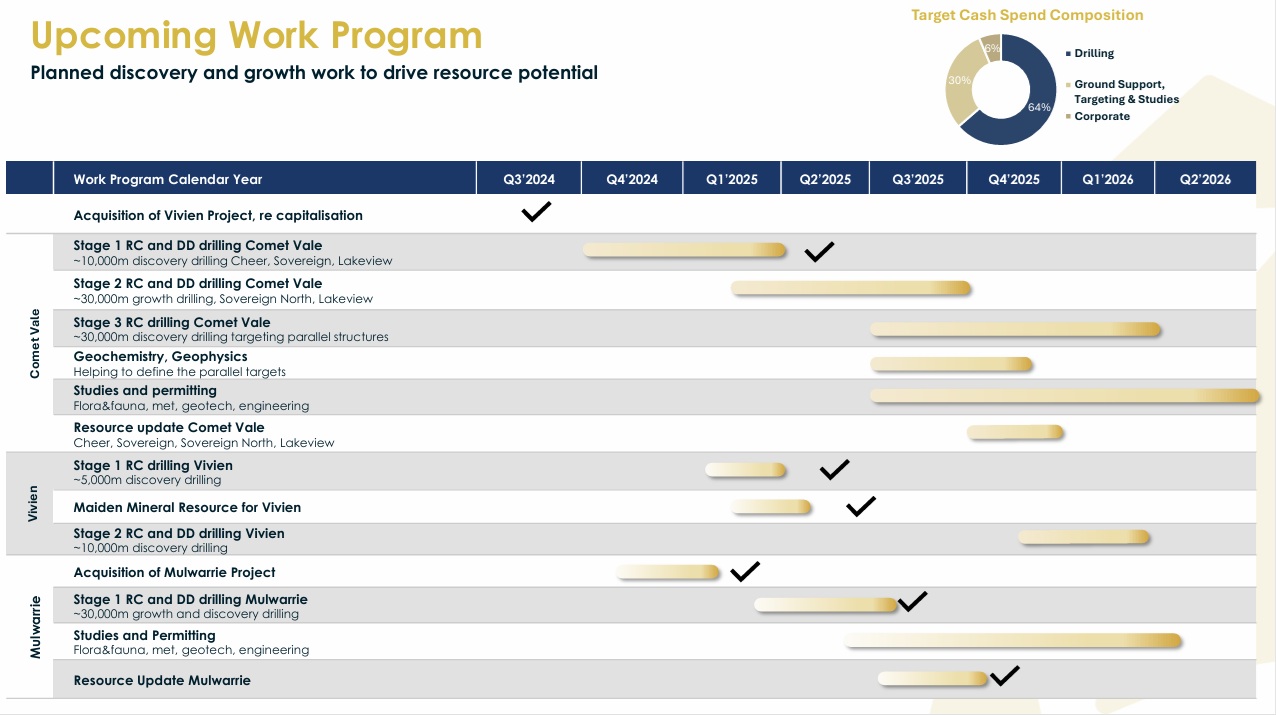

The additional drilling at Mulwarrie is also welcome news: 1 RC (reverse circulation) rig and 1 DD (diamond drilling) rig have re-commenced the next phase of resource growth drilling at Mulwarrie, initially targeting along strike to the south and at depth from previous intercepts.

So what they are seeking to do here is to test for extensions to the deposit both to the south of and also below their known mineralisation. In this way they can potentially keep growing the deposit (in terms of indicated gold) in every direction that hasn't already been closed off by previous drilling hitting no gold.

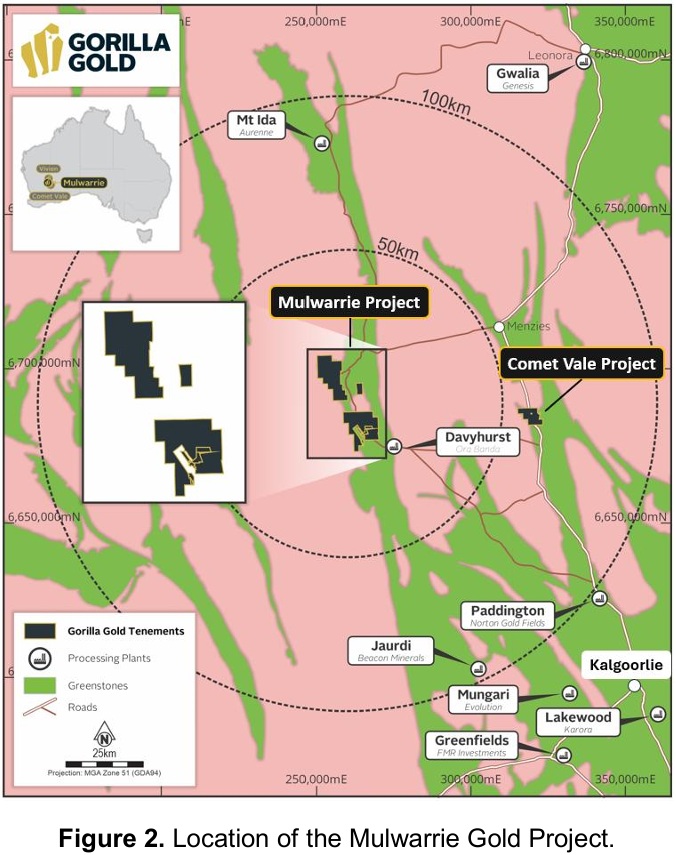

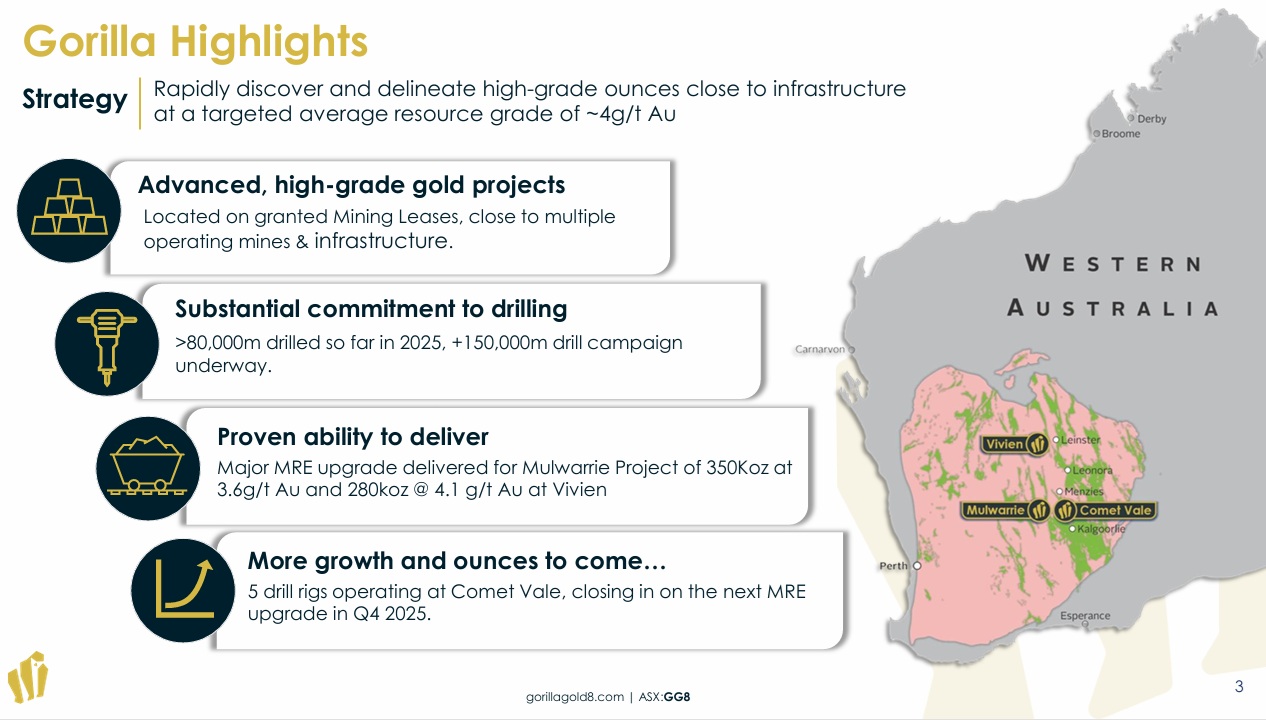

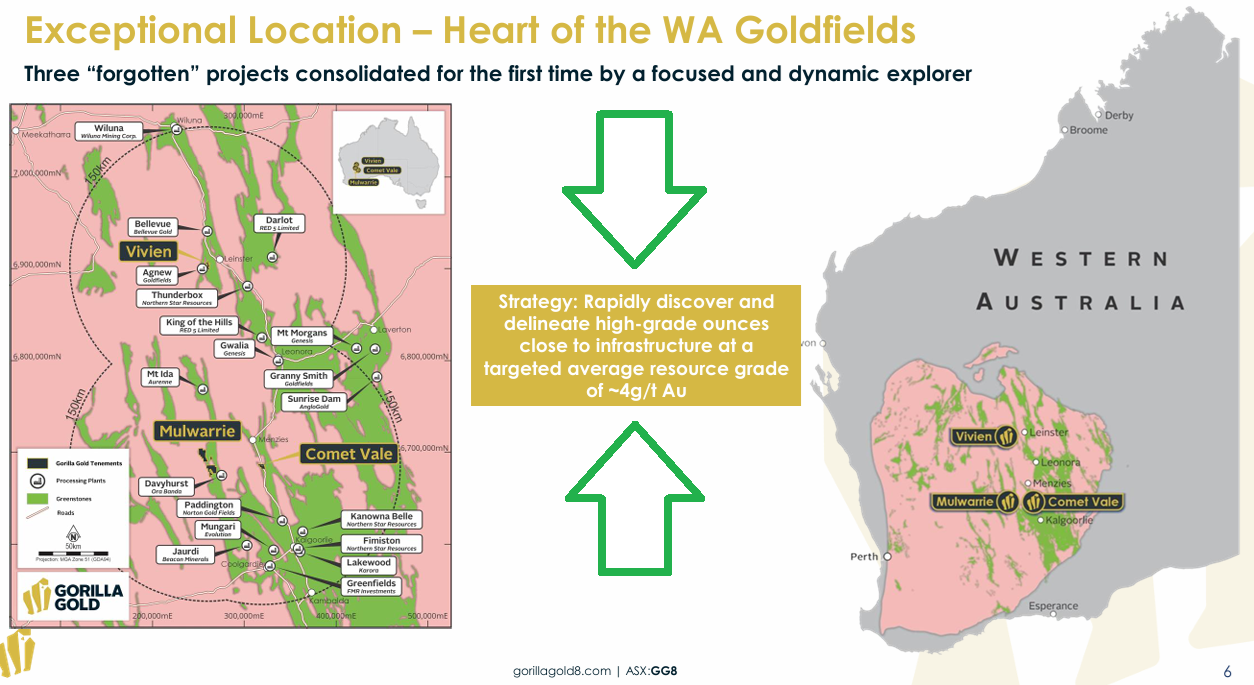

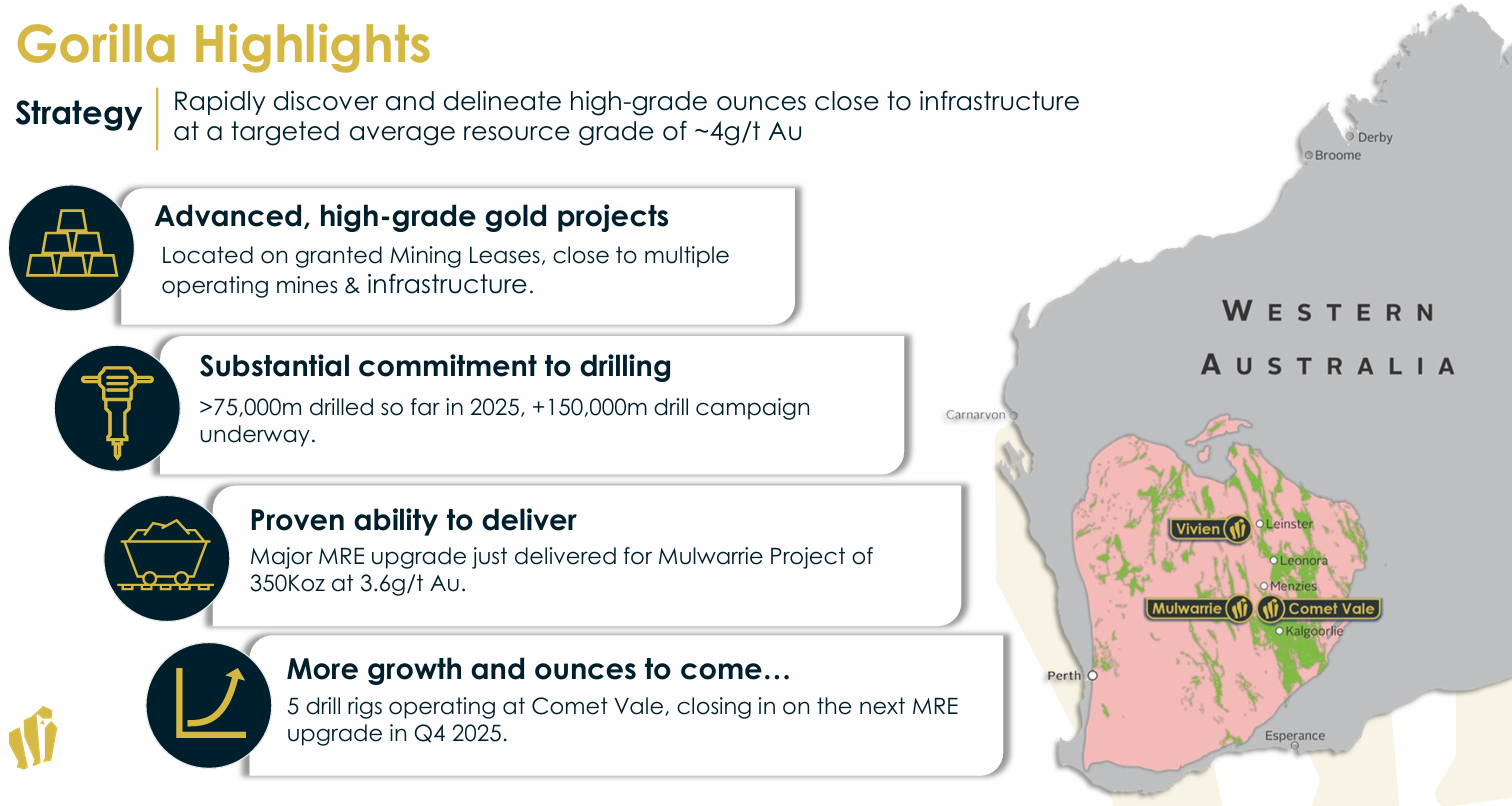

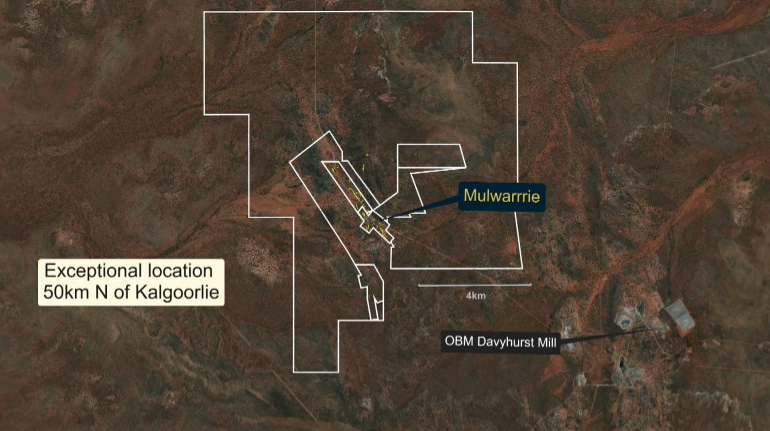

And remember - Mulwarrie is just one of 4 gold projects that GG8 own (3 of those in WA, one in Canada), and they're currently predominantly focused on 2 of those 4, being Mulwarrie and Comet Vale, because those two are their most promising projects at this point in time.

Both are close to existing mills that are owned and operated by experienced gold producing companies like Ora Banda (OBM), Norton Gold Fields, Evolution (EVN) and Genesis (GMD).

Disc: Held. 1.2%. Smaller company, no cashflow yet, so in the cashburn phase where they are spending money to prove up these deposits, so much higher risk than an established producer, so much lower weighting and held in my real money speccy portfolio only.

31-Oct-2025: Quarterly Activities/Appendix 5B Cash Flow Report.PDF

I tend to usually start at the end when the Activities Report and the Appendix 5B (Cash Flow Report) are lumped together in a single announcement - just to check on their cash balance - particularly with these pre-revenue explorers and project developers.

So their cash burn for the Qtr was around $8.5 million, and the vast majority of that was spent on exploration and evaluation, which is exactly what I want to see with these sort of companies - you do NOT want them spending more on G&A than on drilling. Tick.

Next, we can see that at the end of September they only had a bee's whisker under $16m left in the bank, so that represented 1.88 quarters (less than 6 months) at that Sept Qtr cash burn rate, however they explain at 8.8.2 and 8.8.3 that they raised another $31.7m in late October, so that means they have more like 6 quarters (18 months) of funding now based on the amount they spent in the Sept Qtr. All good. Tick.

Now, back to the Activities report:

(from page 1) 340% increase in Mulwarrie MRE with a 30% increase in grade! Big Tick!

(from page 3) Good Management. Another tick. Average grade of 4 g/t gold in a 700koz resource base for an early stage explorer and developer. Oh yeah, tick.

Below I've copied into this straw some stuff relating to the two projects that Gorilla Gold are mostly focused on right now, Comet Vale and Mulwarrie. They also own Vivien to the north of Mulwarrie, and their Labyrinth Project on the Ontario/Quebec border in Canada and their Denain prospect in Quebec, about 200km east of Labyrinth. Labyrinth might be an M&A target for a company like Kirkland Lake Gold who own gold mines and mills nearby in Ontario, but that's for the future. The focus right now is on Comet Vale and Mulwarrie,

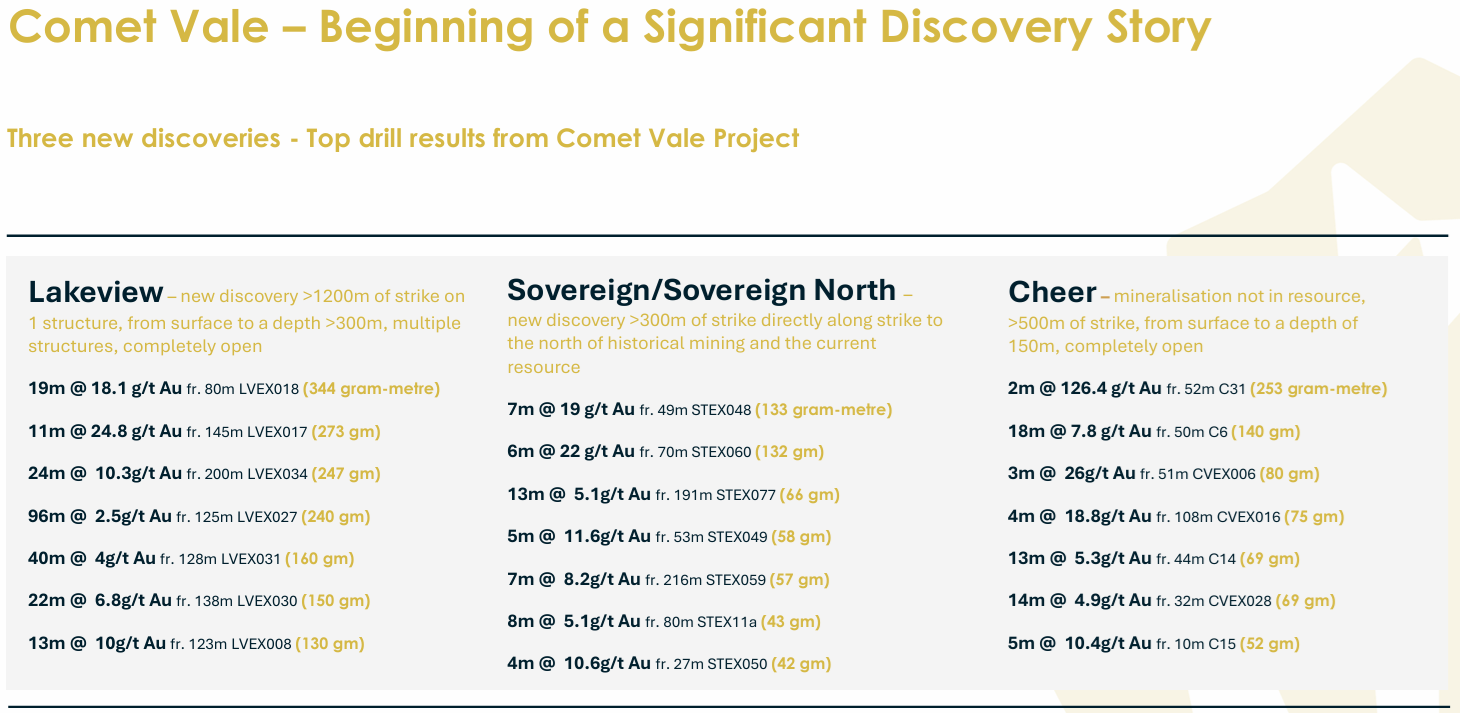

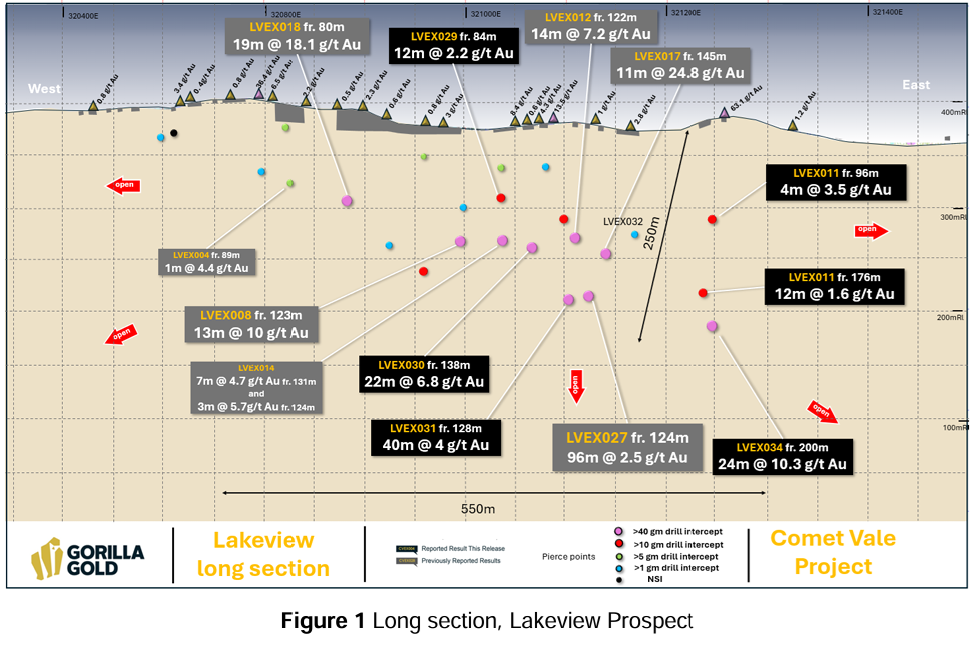

Lakeview Prospect at Comet Vale:

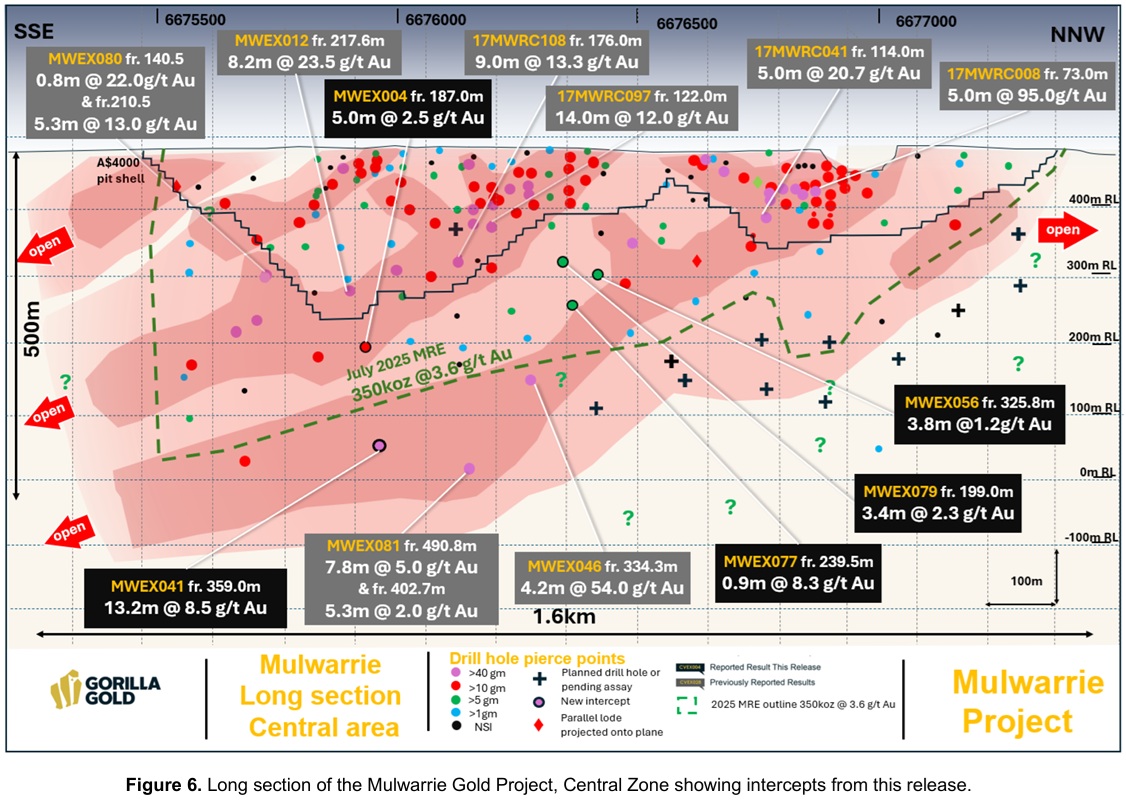

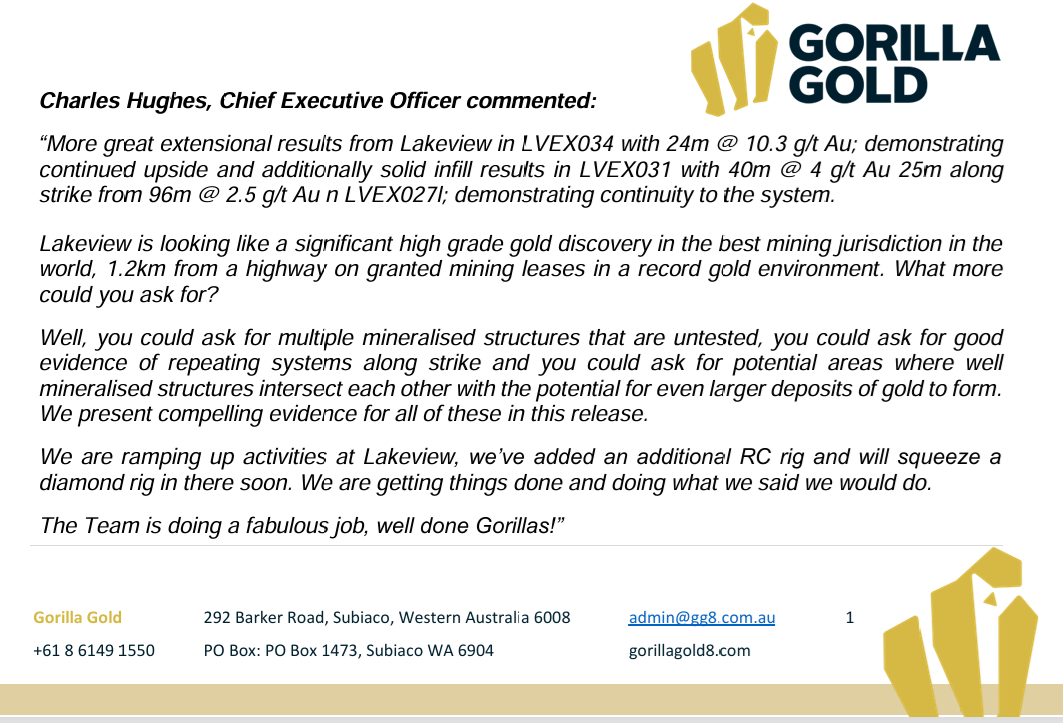

In February 2025, Gorilla undertook a scout drilling program along the Lakeview shear targeting coincidences of historical gold workings, major structural positions and anomalous surface gold geochemistry. Three shallow holes were drilled at Lakeview historically, with anomalous gold intercepts in two of the holes. Gorilla felt that the target was worthy of further testing as the structure had not been tested at different relative levels and some of the workings were quite significant. Gorilla’s scout drilling program returned significant gold mineralised intercepts associated with quartz veining and sulphide development within ultramafic lithologies adjacent to major structures. Early results included 13m @ 10g/t Au from 123m in LVEX008 and 19m @ 18.1g/t Au from 80m in LVEX018 (Figure 7), with follow up drilling this Quarter intercepting: 16m @ 3.5g/t Au from 280m in LVEX069 (Figure 5), 96m @ 2.5g/t Au from 125m in LVEX027 (Figure 5) and 24m @ 10.3g/t Au from 200m in LVEX034 (Figure 6).

Related to the Lakeview Long Section above:

Related to the Cheer and Happy Jack (Silverback Shear-zone) Long Section above:

They have multiple prospects at Comet Vale, however I'm just copying in the images that concern drilling results from the September quarter rather than all of their other older drilling results that were discussed in prior quarterly reports.

Mulwarrie:

--- end of excerpts ---

Source: Quarterly Activities/Appendix 5B Cash Flow Report.PDF [31-Oct-2025]

Disclosure: I hold GG8 shares, both in real life and here.

I like that they are now cashed up for another 18 months after their very recent CR ($31.7 million placement in late October), that they have good people there who have good track records of succesful discoveries of commercially viable gold, and that the vast majority of their spending is on drilling and evaluation, not G&A. I also like their ground (tenements), and their proximity to other gold companies that are already producing gold.

High risk, so I hold them in my smaller speculative company portfolio, but worth a punt with a reasonably small amount of my investable capital, in my opinion.

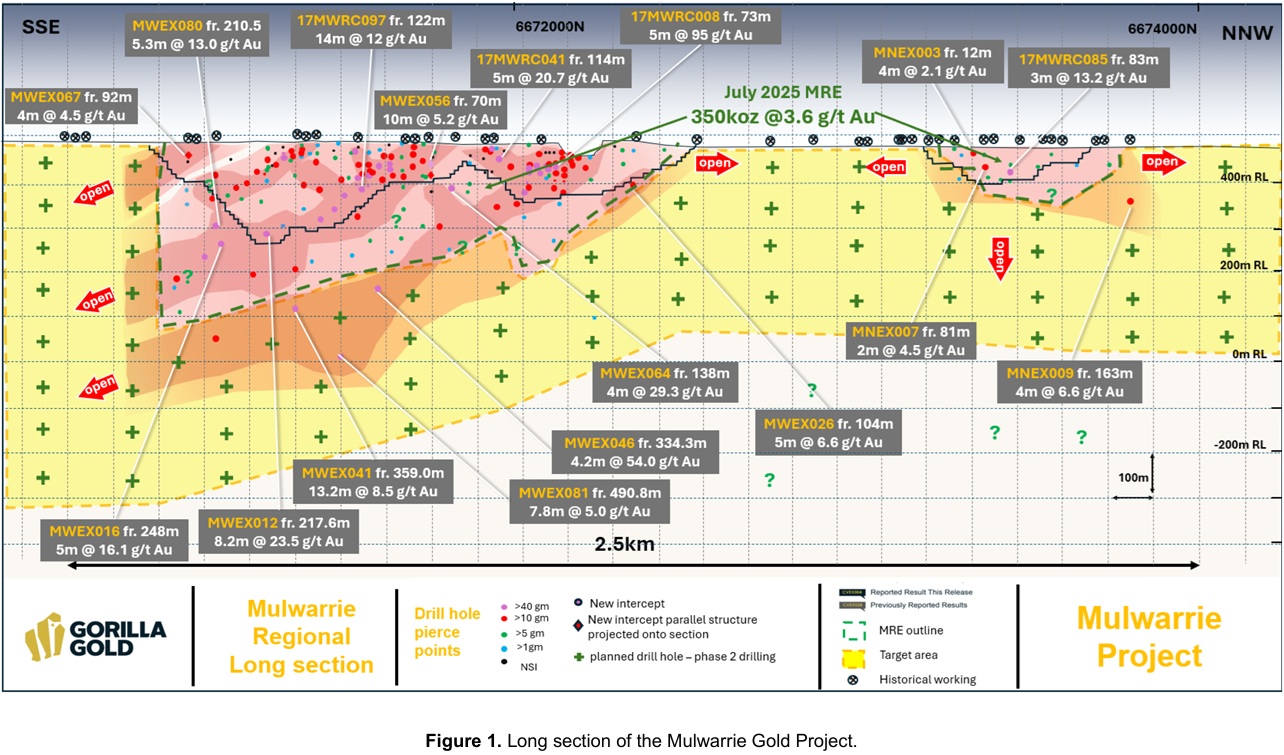

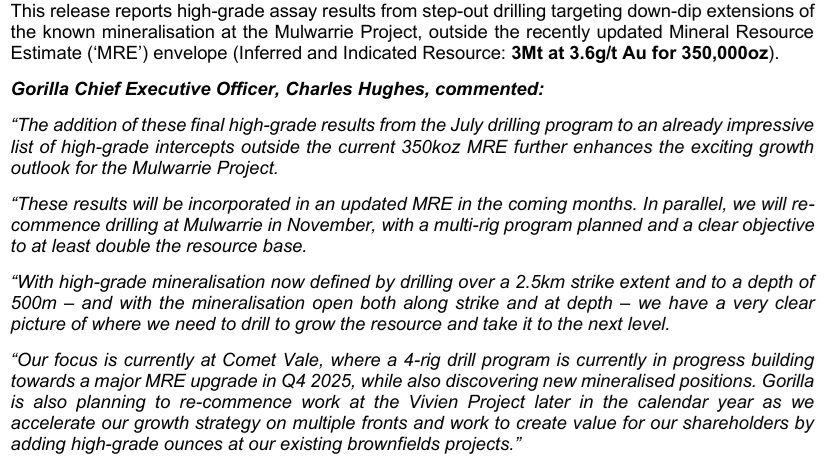

3rd October 2025: Mulwarrie High-Grade Step Outs

Excerpts:

Source: Mulwarrie High-Grade Step Outs [03-10-2025]

Plain Text Link: https://wcsecure.weblink.com.au/pdf/GG8/03003005.pdf

Disclosure: Holding.

17th September 2025: Most goldies fell today, but GG8 bucked the trend and finished the day up +10.53% @ $0.42/share, probably on the back of their presentation today at the Resources Rising Stars Gold Coast Investor Conference (which runs for two days, today and tomorrow).

Here's the slide deck from their presentation today: Resources Rising Stars Investor Presentation.PDF

It's 29 pages long, so I'll just share the 6 slides that I think best explain why I'm invested in this company in my smaller speccy portfolio of higher risk gold explorers and project developers which currently holds 5 such companies plus a tiny position in BluGlass (BLG) to keep me focused on them. BLG is not a gold company, they're a chip and laser company, but I class them as high risk also (so they'll go big or go broke - at some stage) so that small BLG position is also in my speccy portfolio. I also have an income portfolio, an SMSF and a small one-company portfolio I "manage" for our two kids (who are both adults now) which just has LYL in it bought at lower levels, plus my virtual portfolio/scorecard here on SM.

So, back to Gorilla Gold, and the 6 slides I like best from today's presentation on the Gold Coast:

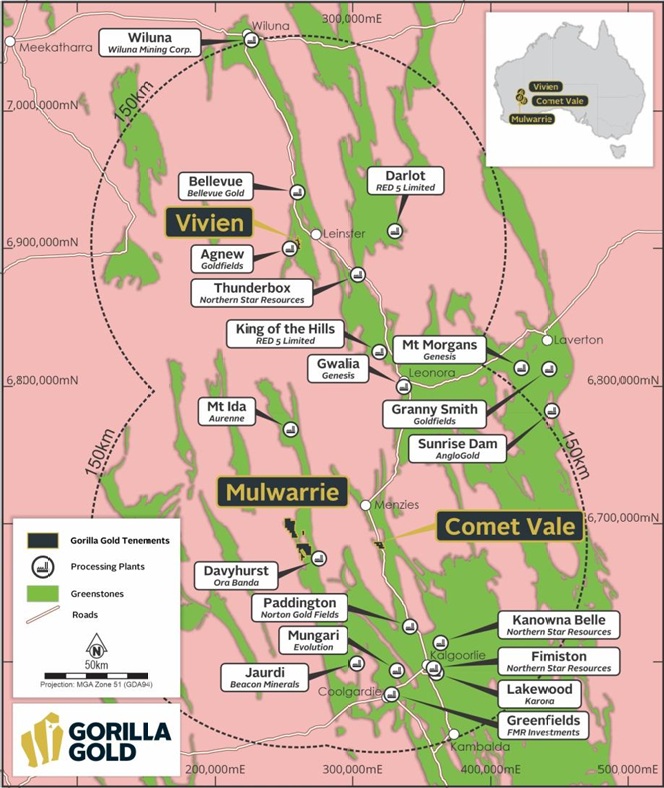

That map above a bit larger below:

Note: RED 5 Limited are now called Vault Minerals Limited (VAU, owners of Darlot and King of the Hills a.k.a. KOTH).

Source: Resources Rising Stars Investor Presentation.PDF [17-Sep-2025]

Discl: Held.

5th August 2025: Diggers & Dealers Investor Presentation [29 pages]

Slides from that presso are below in this straw.

Also today (5th Aug): Results from Initial Metallurgy Testwork at Lakeview

And yesterday (4th Aug): Mulwarrie Resource Update

And last week (30th July): Quarterly Activities/Appendix 5B Cash Flow Report

So, I've provided a price target (77 cents/share) and a brief overview of Gorilla Gold Mines (GG8) (formerly known as Labyrinth Resources Ltd) in my "Val" for GG8 here.

This straw is to provide a little more colour around their Board & Management, their skin in the game, more info on the locations of GG8's major WA gold projects particularly in relation to other gold producing mills (owned by other companies), and just how active GG8 have been so far and what their immediate plans are from here.

Warning: This is a pre-revenue company; they do not currently produce any gold; they are an explorer and maybe-wanna-be-project-developer, so there WILL be CRs along the way and it's much higher risk than an established gold producer. "Investing" in this one is more akin to gambling, and I'm betting that they find more gold and increase their own value while also making themselves more attractive as either a takeover target or a company with valuable assets that their neighbours might be interested in acquiring. I don't think GG8 will be progressing any of their projects through to production - my own opinion rather than fact - because I think they are a true exploration company run by geologists who are in it for the hunt - they love finding viable gold deposits and proving them up, selling them off, and then moving on and doing it all again.

That's the basis of my position in GG8 - they are a very active gold explorer run by very competent geologists who are finding more gold and adding value. It's an exciting gold play with money I can afford to lose if it all falls apart, but based on what they've found already, I doubt that they are going to go broke, the worst outcome scenario in my opinion is that they keep raising capital and diluting existing shareholders without finding enough gold to take them to that next level where they can sell off projects at good profits or be taken over themeselves. These sort of companies can keep mining shareholder wallets for years without ever providing a positive shareholder return, but that sort of outcome tends to come more from companies who don't do enough drilling and/or don't have good enough ground to start with. GG8 clearly have very good ground based on what they've already discovered there, and they are certainly very active with their drilling, so that's why I say they're one of the better explorers.

So I'm going to share some of the better (or more important, IMO) slides from today's 29 page D&D presentation in Kalgoorlie, without repeating stuff that I've already included in my "Val" for GG8.

Firstly, here's their Board & Management:

Simon Lawson was MD & Executive Chairman of Spartan (formerly Gascoyne Resources) prior to Spartan being acquired by Ramelius (RMS) recently, and Simon has now been appointed as Non-Executive Director (NED) and Deputy Chair of Ramelius Resources (see here). Simon is also a NED of Gorilla Gold (GG8) and their Technical Director (see here). Mr Lawson is a professional geoscientist with more than 16 years operational experience spanning multiple commodities and jurisdictions and was a founding member of Northern Star Resources (ASX:NST) that over his 6 years with the company transformed a small Western Australian gold mine into a multi-billion dollar global gold mining heavyweight. He also spent 3 years as the MD of Firefly Resources Ltd, a junior exploration company that merged with Spartan in November 2021. Prior to that Mr Lawson was Chief Geologist and alternate Resident Manager for TSX-listed Superior Gold (TSX.V:SGD) at Plutonic Gold Mine after selling the mine to the Canadian group out of Northern Star Resources in 2016-17. In his 12 months with Superior the 27-year-old Plutonic operation produced more than $20m free cashflow from month one through a combination of cost reduction, operational focus and commercial dealings. The man has some serious gold sector experience, particularly in management and exploration.

Alex Hewlett is a qualified geologist who is highly skilled at project identification and acquisition. Previously Chairman of Spectrum Metals Limited, Mr Hewlett oversaw its growth from mid-2018 through to Spectrum being taken over by Ramelius Resources (RMS) in early 2020. More recently, Mr Hewlett led the identification and acquisition of Tabba Tabba (from GAM owned by RCF) for Wildcat Resources Limited and the acquisition and development of the Mt Ida project (from Ora Banda) for Delta Lithium Limited.

Charles Hughes is GG8's CEO, and is a professional geologist with 17 years of experience in the resources industry, during which time he has held executive positions at Delta Lithium and senior management positions at Bellevue Gold, Northern Star and Saracen Minerals (which was Australia's 4th largest gold miner prior to being acquired by NST, now Australia's largest gold miner). Mr Hughes is highly skilled at identifying growth opportunities, developing and leading aggressive resource growth and development strategies, and delivering results. More recently, Mr Hughes has overseen more than 400km of drilling across multiple development projects in the last 3 years with Delta Lithium defining >40Mt of Li2O resource and >750koz of high grade gold resources as well as driving mining permitting, and mining and processing feasibility studies.

Matt Crowe, GG8's Exploration Manager, is an experienced exploration geologist with 20 years’ experience working for major and junior companies across a broad range of commodities in the Western Australian resources industry; including Principal Geologist at BHP, and Chief Operating Officer/Exploration Manager at Dreadnought Resources. He has extensive experience leading both greenfields and brownfields exploration teams which included discoveries in copper, gold, nickel, iron ore, rare earths and niobium. In 2023 he was co-recipient of AMEC’s Prospector Award for the Yin REE discovery which involved a period of rapid exploration and resource definition following the initial discovery.

Much of that can be found here: https://gorillagold8.com/directors-management/ but I've supplemented some of that info with some cross-referencing with other gold company websites, Commsec data and some LinkedIn profiles.

Next, the overview:

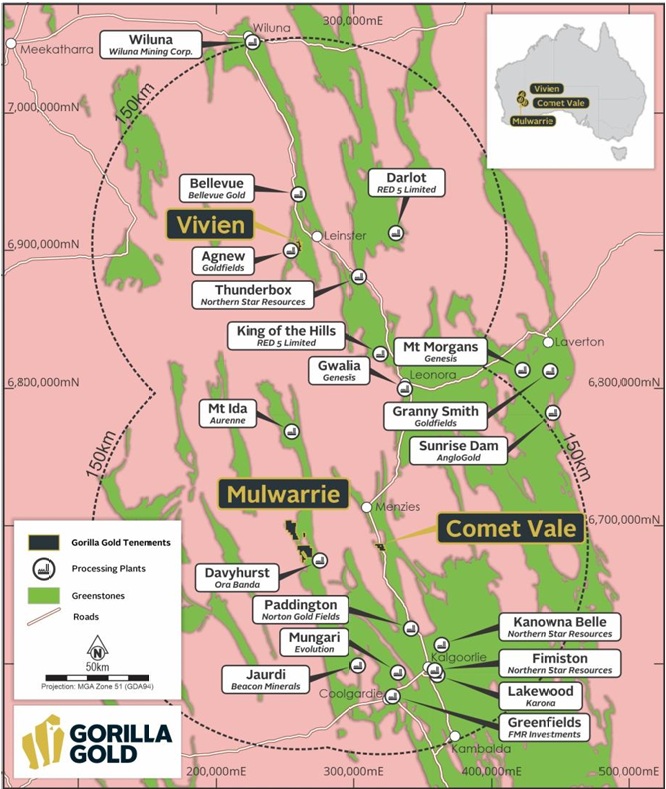

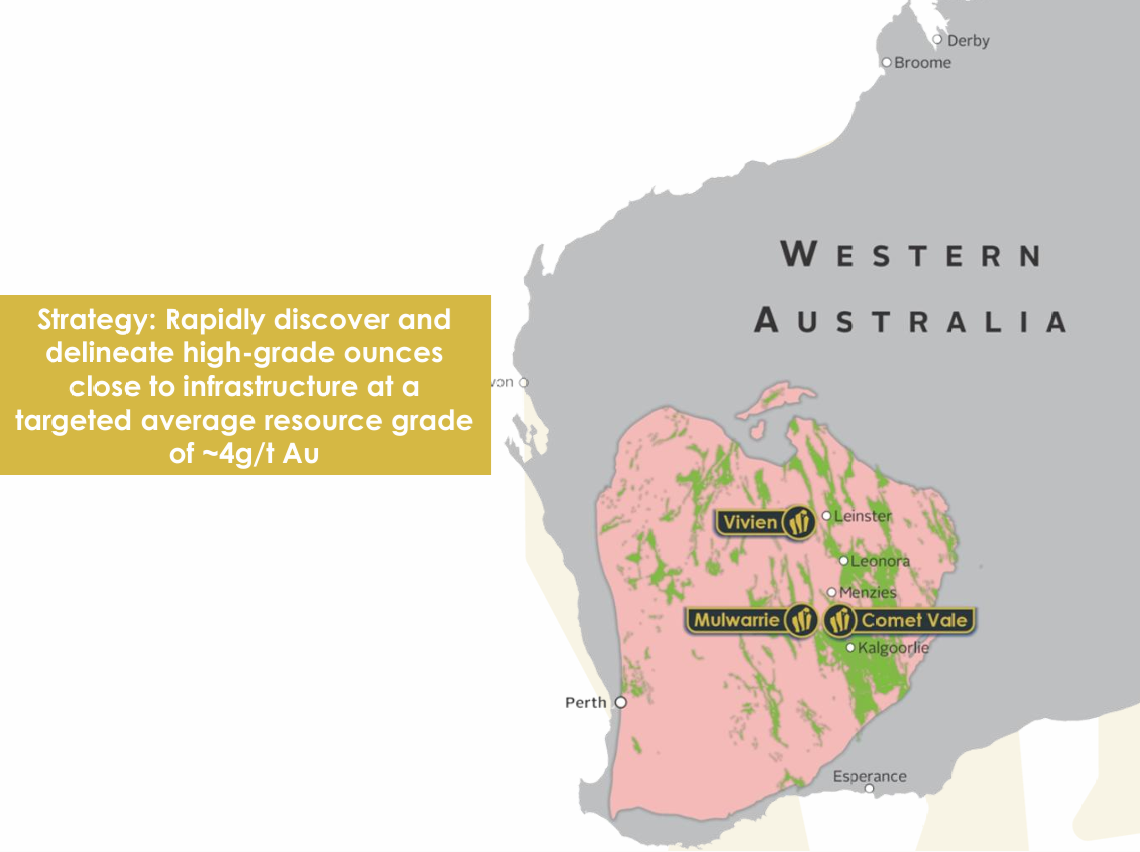

They also have a project in Canada, but they are entirely focused on their WA Goldfields assets at this point in time, and with good reason - look at where they are:

And the grades of gold that they're finding:

More on that in a minute - and also plenty of details of that in my "Val" for GG8.

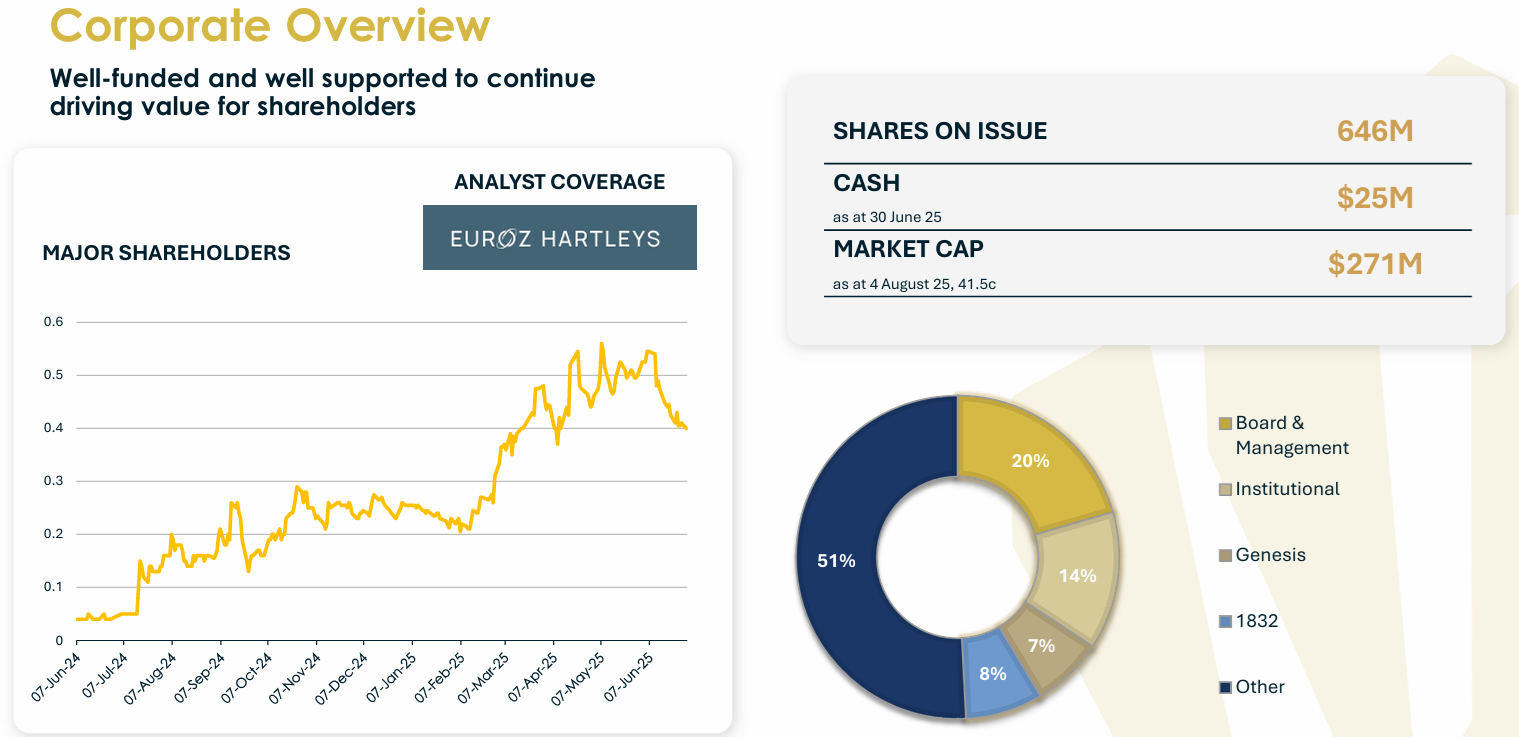

But firstly have a look at their ownership structure below. 20% owned by their Board and Management - that's substantial skin in the game - and 7% owned by Genesis Minerals (GMD) which is probably the best growth story among all of Australia's current gold producers (and yes, I do hold GMD shares).

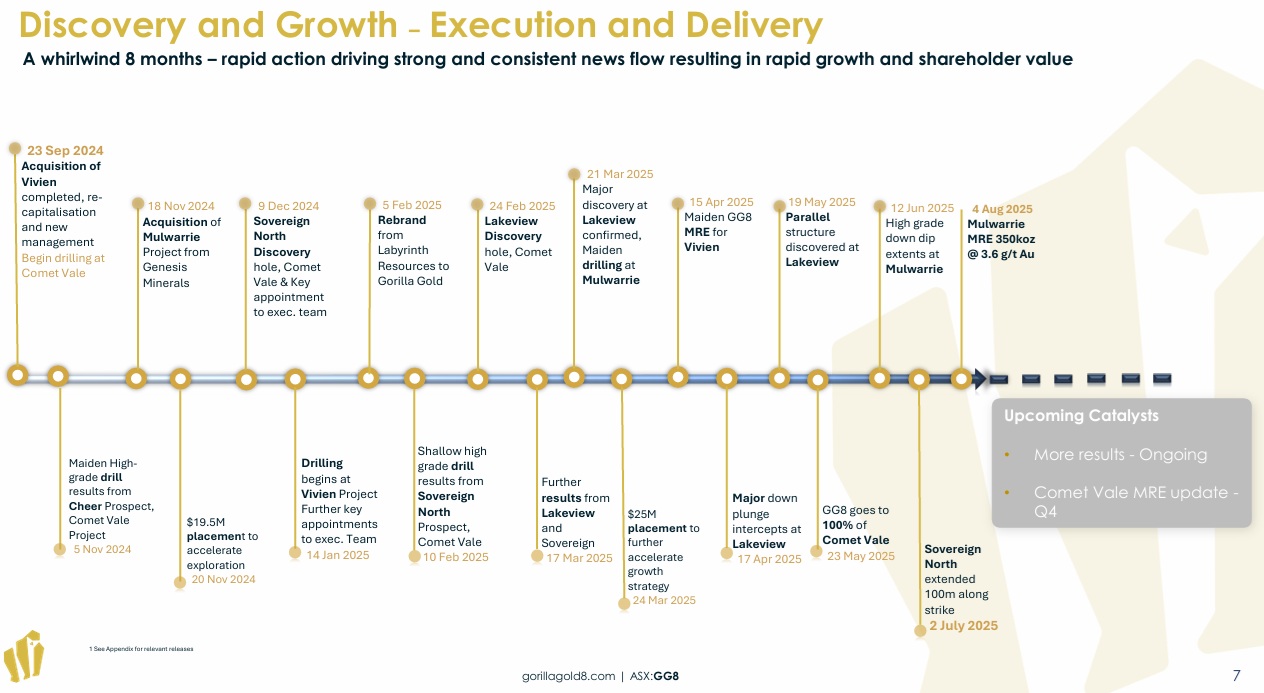

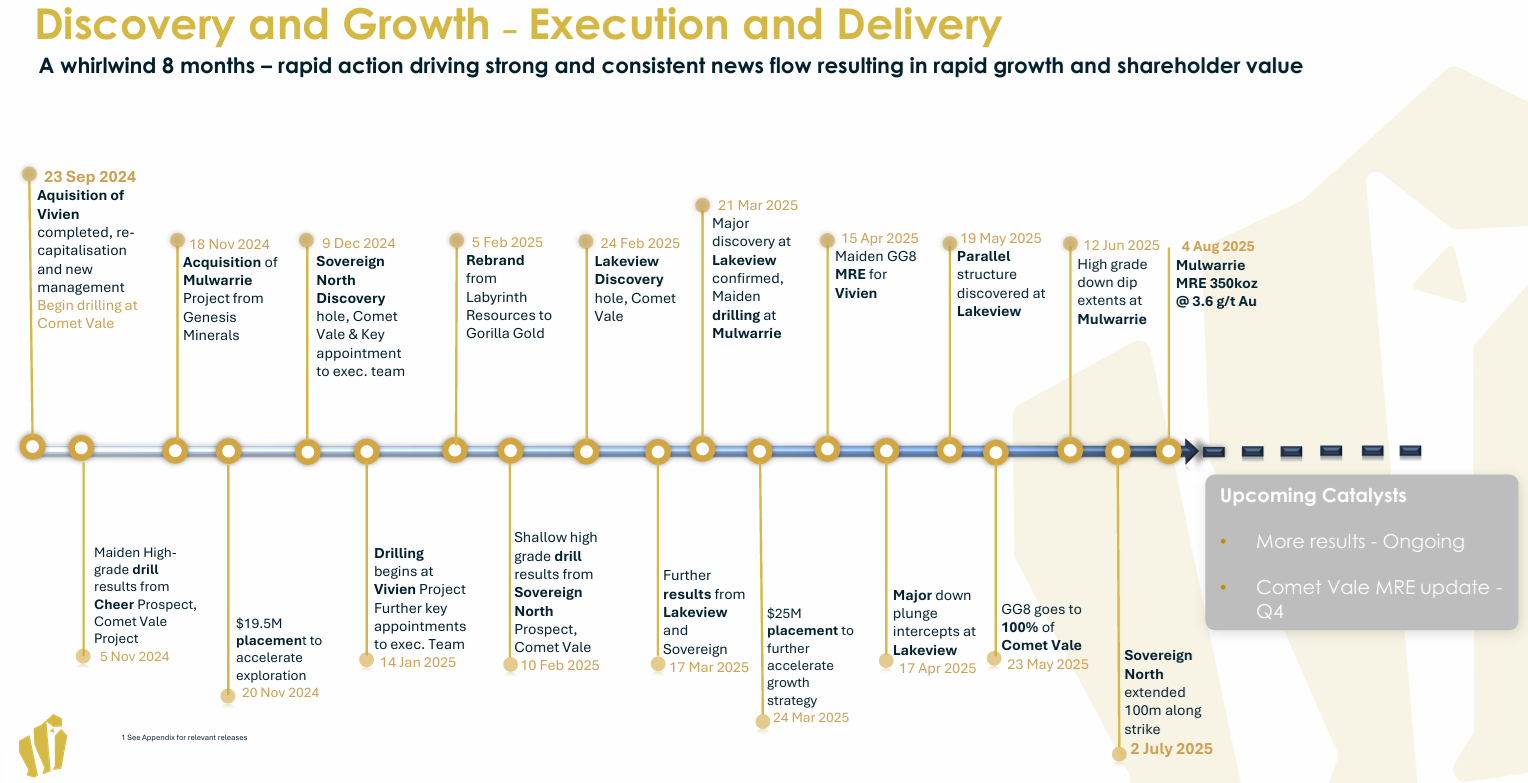

And their market cap is still sub-$300m. Next - what they have already achieved and the timeline they achieved it in:

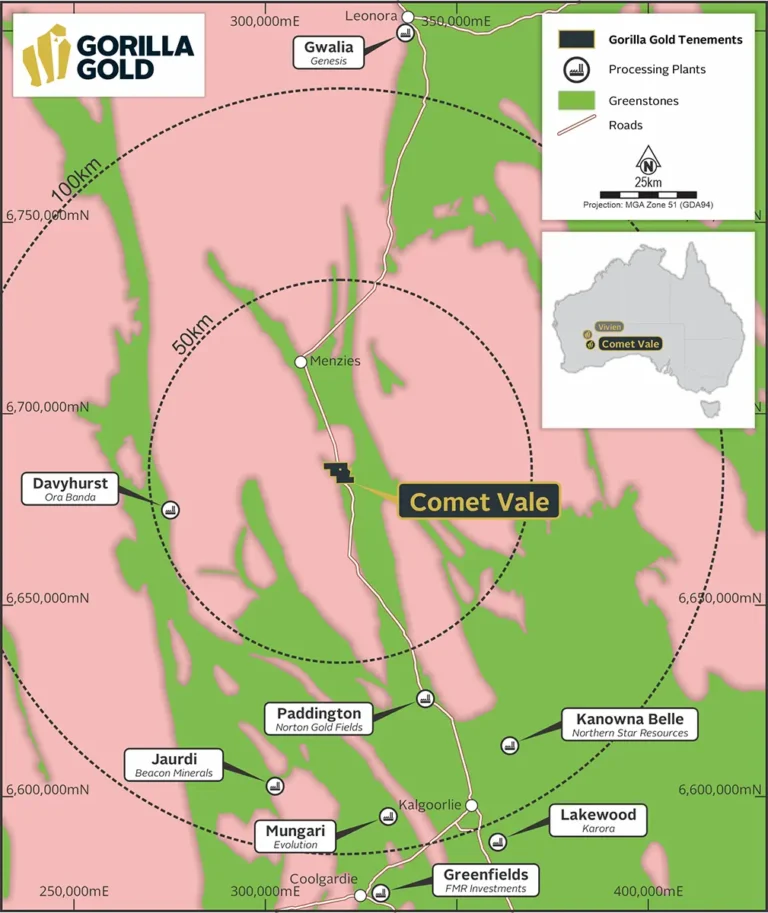

A quick overview of some of their better recent gold hits at just one of their projects, Comet Vale:

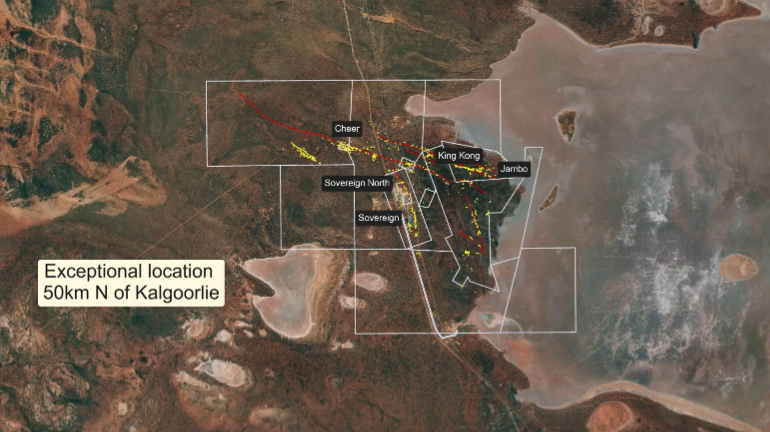

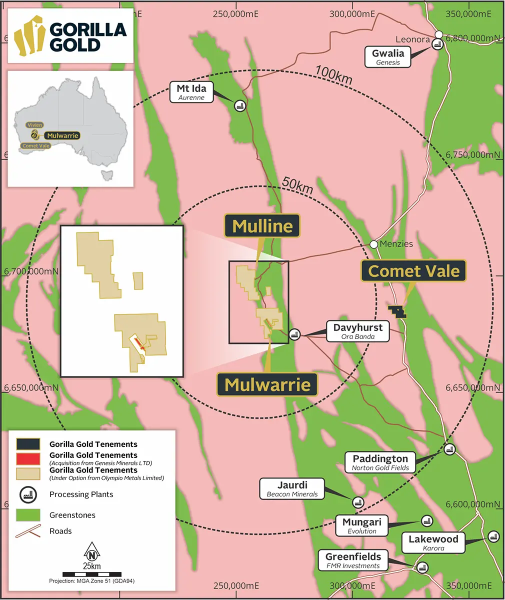

Below is a satellite image of Comet Vale with their tenements and gold hits marked on it, and then below that is the same thing with their Mulwarrie project, which is just 60km west of Comet Vale.

Here's just how busy they've been and will continue to be:

In Summary:

For more: https://gorillagold8.com/

Disclosure: Holding.

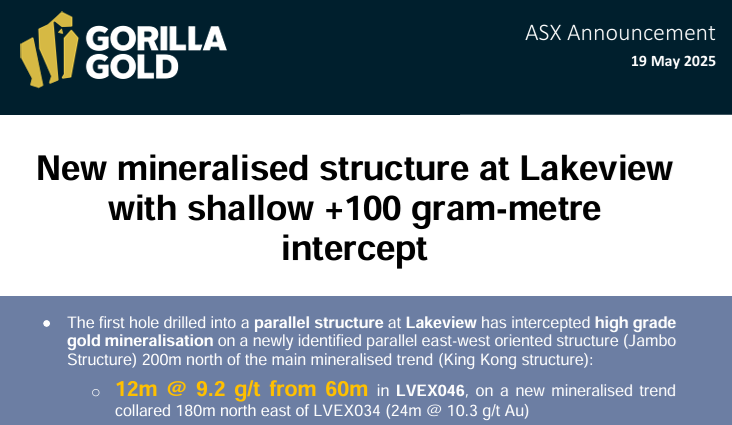

Gorilla Gold released another nice update this morning:

Parallel Structure Discovered at Lakeview [19th May 2025, 8:43am]

From the first page:

Source: Parallel Structure Discovered at Lakeview.PDF [19th May 2025, 8:43am]

Disc: I hold GG8 shares. (see here)

The market liked today's announcement:

https://gorillagold8.com/directors-management/

Warning: Small explorer, having drilling success but with no income other than from cap raisings (and possible asset sales) so not profitable, so more of a gamble than an investment. My position in GG8 is therefore appropriately small.

May 14th, 2025: Gorilla Gold Mines (GG8) is an interesting company. Originally called Orminex Ltd (ONX), they were founded in 1970 and have always been headquartered in Subiaco, a suburb of Perth, Western Australia (Subiaco and West Perth are home to the HQs of a plethora of mining companies and minerals exploration companies). Marketindex.com suggests they were also formerly known as Mintails Ltd (MLI, 2018) and Trans-Global Resources NL (TGL, 1999), but ChatGPT only goes back as far as Orminex.

The company specialises in gold mining and has been involved in various mining ventures in Western Australia. In November 2021, Orminex Ltd underwent a rebranding and changed its name to Labyrinth Resources Ltd and its ticker code to LRL. It was at that time mostly focused on the Labyrinth Gold Project, located in the Abitibi Greenstone Belt in Quebec, Canada. The company also held the Comet Vale Gold-Copper-Nickel project in Western Australia and they later acquired the Vivien Gold Mine from Ramelius Resources (RMS).

In November 2024, Labyrinth announced they had entered into a binding term sheet with Bardoc to acquire 100% of Admiral Gold, which owned 100% of the Mulwarrie Gold Project. Bardoc was a fully owned subsidiary of Genesis Minerals (GMD), which Genesis gained when they acquired St Barbara's (SBM's) Leonora (WA) assets in June 2023. That acquisition of Admiral / Mulwarrie from GMD by LRL was effected via an upfront consideration of $3.75 million settled via the issue of ~17.86 million fully-paid Labyrinth shares (17,857,143 LRL shares) at an issue price of $0.21 per share (21 cps), with a $1.0 million cash milestone payment due upon first commercial production from the tenements.

That's how Genesis Minerals (GMD) became substantial shareholders of LRL (now GG8). In addition to being issued those 17.86 million LRL shares, GMD acquired additional LRS shares in September, October and November and held 7.64% of GG8 (then LRS) on 29th November 2024 (when that deal settled), so 41,319,637 LRL shares at that time. When GG8 raised another $25 million in March (two months ago) "to accelerate exploration activities at its recent Lakeview discovery and maintain ongoing exploration momentum at its Comet Vale, Mulwarrie and Vivien projects", GMD committed to subscribe for another A$1.84m of GG8 shares to maintain its pro-rata 7.64% shareholding in Gorilla.

Commsec doesn't list GMD as being a "Sub" for GG8 because the Becoming-a-substantial-holder-from-GMD-for-Labyrinth-Resources.PDF announcement was only posted by the ASX to GMD, not to LRL (Labyrinth Resources, now GG8), which was clearly a mistake, so the system wasn't able to scrape the data and update the "Subs" list for LRL as it should have - so purely an administrative error by whoever compiles that data that Commsec displays - due to the ASX not posting that announcement to LRL.

But GMD remain GG8's 4th largest shareholder with 7.64%.

In February 2025, Labyrinth Resources Ltd (LRS) changed its name to Gorilla Gold Mines Ltd and their ticker code to GG8. Their new company logo is above. Gorilla Gold describe themselves as a gold explorer based in Western Australia focused on the exploration upside of under-explored mining projects close to existing infrastructure. The strategy is underwritten by its current global JORC Resource of 675koz at 4.7g/t, providing a platform for further resource growth.

Gorilla Gold benefits from access to capital and expertise for accelerated exploration within Western Australia. While the company continues to explore and develop gold, lithium, rare earth elements, copper, tungsten, and nickel deposits in Australia, it's their current focus on gold that interests me personally.

According to ChatGPT, regarding the founders of Orminex and Labyrinth Resources, specific information is not readily available, however the company has been associated with key individuals such as Kelvin Flynn and Alex Hewlett who are both current Non-Executive Directors (NEDs) of Gorilla Gold Mines and have been involved in driving value creation at other companies like Red Dirt Metals Limited (now Delta Lithium), Spectrum Metals Limited, Mineral Resources Limited, Silver Lake Resources Limited, and Wildcat Resources Limited.

Kelvin Flynn is currently GG8's 3rd largest shareholder through his company Sharlin Nominees Pty Ltd which owns 46,821,306 GG8 shares, being 8.38% of their SOI (shares on issue).

Alex Hewlett is currently GG8's 2nd largest shareholder through his company Elefantino Pty Ltd which owns 56,542,710 GG8 shares, being 9.02% of the company.

Their largest shareholder is Samuel Wilson who holds (mostly in his own name but also through a company he controls called Pilbara Conveyor Supplies Pty Ltd) 471,913,059 GG8 shares, being 10.62% of the company. Samuel Wilson was a non-executive director of Orminex for 4 years from March 2018 to January 2022, so when he left, the company had changed their name to Labyrinth Resources (in 2021).

The only other current Substantial Shareholders of Gorilla Gold (after Samuel Wilson, Alex Hewlett's Elefantino, Kelvin Flynn's Sharlin Nominees and Genesis Minerals) is 1832 Asset Management with 6.92%, and that position is usually attributed to the Bank of Nova Scotia because 1832 Asset Management is a wholly-owned subsidiary of the Bank of Nova Scotia (BNS), registered in Ontario, Canada. Some of those shares may at times be held in other controlled and managed entity of BNS, such as their Dynamic Precious Metals Fund. 1832 Asset Management L.P. also operates under the business name Scotia Global Asset Management, All part of the Bank of Nova Scotia, Canada.

Circling back to Kelvin Flynn (pictured above), a NED at GG8 and their third largest shareholder (with 8.38%), according to Commsec, Mr Flynn has 30 years experience in investment banking and corporate advisory roles including financing, M&A, private equity and special situations investments in the mining and resources sector. He has held various leadership positions in Australia and Asia, having previously held the position of Executive Director/Vice President with Goldman Sachs and Managing Director of Alvarez & Marsal in Asia. He is the Executive Chairman of Harvis, which is a specialist private lender and corporate advisory firm in Western Australia. Mr Flynn was previously a 14 year Director of Mineral Resources Limited (MIN, aka MinRes), a 13 year Director of Global Advanced Metals Pty Ltd and is currently a NED of Vault Minerals Limited (VAU). Prior to Red 5's recent merger with Silver Lake Resources to form Vault (VAU), Mr Flynn had been a Director of Silver Lake Resources for 8.5 years.

Regarding Alex Hewlett (pictured above), also a NED at GG8 and their second largest shareholder (with 9.02%), according to Commsec, Mr Hewlett has experience in project identification and acquisition. Previously Chairman of Spectrum Metals Limited, Mr Hewlett oversaw its growth from mid-2018 through to being taken over by established gold miner Ramelius Resources Ltd (RMS) in early 2020. More recently, Mr Hewlett led the identification and acquisition of Tabba Tabba (from GAM owned by RCF) for Wildcat Resources Limited and the acquisition and development of the Mt Ida project (from Ora Banda) for Delta Lithium Limited.

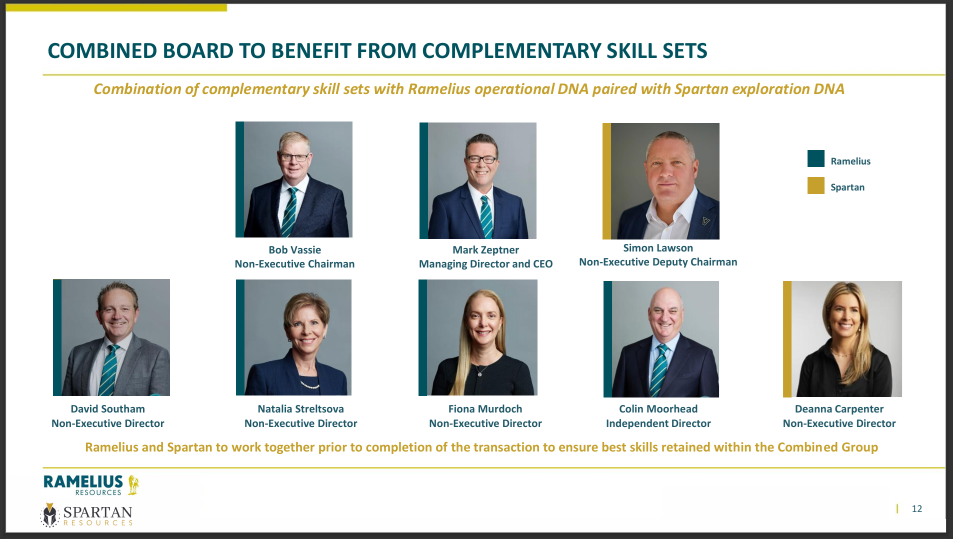

Another GG8 Board Member, their Technical Director, Simon Lawson (pictured above and below) is a professional geoscientist with more than 18 years of experience in exploration, production and managerial roles spanning multiple commodities and jurisdictions, and was a founding team member of Northern Star Resources Ltd where he held senior geology roles including Principal Geologist and, along with NST's then Executive Chairman Bill Beament and NST's current CEO & MD (then CEO) Stuart Tonkin, helped transform NST from a small WA gold explorer into a multi-billion dollar gold mining heavyweight that became (and still is) the largest Australian gold miner and a top 10 global gold miner in terms of both market cap and annual gold production.

As well as being GG8's current Technical Director, Simon Lawson (above) is also currently a NED at Firetail Resources (FTL) and is the Chief Executive Officer (CEO), Managing Director (MD) and Executive Chairman of Spartan Resources (SPR), formerly known as Gascoyne Resources. Spartan (SPR) is now under an agreed takeover offer from Ramelius Resources (RMS) which Lawson helped to arrange and get over the line, and Lawson is one of only two people from Spartan that will be joining the Ramelius Board when the acquisition completes - expected to be in late July or early August this year:

Source: Page 12 of their March 17th "Transformational Combination of Ramelius and Spartan" Presentation

Prior to joining Spartan (SPR), but after his time at NST, Mr Lawson was also Chief Geologist at Superior Gold Inc. which was acquired by Catalyst Metals (CYL) in June 2023.

GG8 only have 4 people on their Board, and the fourth (after Lawson, Hewlett and Flynn) is their non-executive Chairman, Dean Hely, who is a corporate lawyer. Mr Hely is the Managing Partner of the independent West Australian legal firm Lavan and a partner in the Corporate and Reconstruction group. Mr Hely has over 28 years of experience working in corporate reconstruction, insolvency and commercial litigation. Mr Hely and others established Quadrant Advisory, a debt advisory practice that assists clients ranging from midsized companies though to ASX listed companies with their debt requirements.

So a decent board with relevant experience and plenty of skin in the game. And a couple of interesting Substantial Shareholders (Subs) in Genesis Minerals (GMD) and 1832 Asset Management / Bank of Nova Scotia (and their Dynamic Precious Metals Fund).

I should also mention that in mid-January this year, Gorilla Gold (or Labyrinth Resources as they were still known at that time) announced the appointment of Mr Mark Rozlapa as their new Chief Financial Officer (CFO). Mr Rozlapa is a qualified Chartered Accountant with over 20 years’ experience, including more than 15 years for listed mining companies across the exploration, feasibility, construction and production phases. Mark previously held senior finance roles across a broad range of commodities and jurisdictions including at Sandfire Resources, Ramelius Resources and IGO. He has experience in project financing and the implementation of processes and systems to support resource growth and development strategies. Another Tick.

Now to where their projects are in relation to other players in the gold space:

Source: https://gorillagold8.com/

So, there's the background - they still own 100% of the Labyrinth Gold Project in Quebec Canada, approximately 40km NW of Rouyn-Noranda and 13km NE of the Kerr-Addison Mine which had historic production of 11 million ounces of gold at 9g/t, but that's not what interests me - it's these various WA goldfields projects that have existing operations all around them, and GG8 are drilling the crap out of these projects - as explained below - click on the image to load the page and then click on the "Play" icon in the middle after the page loads to watch the video:

He mentions "Lakeview" being a priority at this point in time, and that was recorded last week (7th May 2025), so it's current, but you may have observed that Lakeview does not appear on the area maps above. That's because it's part of their Comet Vale Project, as shown below:

Source: Lakeview Extended 125m Along Strike.PDF [17th April 2025]

Have a read of that one if interested (link above).

I titled this straw "Business Model/Strategy" and after plenty of background we've finally got to that; their strategy is to pinpoint the best gold projects in the best WA goldfields locations - and then turn them into swiss cheese.

I'm not convinced they're going to take any of these projects through to production because they can make great money by proving up these deposits and then selling them off to existing gold producers who already operate nearby.

From those producers' POV, it's all about replacing depleting reserves and also trying to grow reserves where possible, and it's a lot easier to buy projects where the drilling has already been done than to find viable (profitably mineable) new gold deposits themselves from scratch.

Approximately 60% of major global gold miners are prioritising investments in exploration and development to replace depleting reserves. This focus addresses the industry's long-term sustainability challenge, as many mines face declining ore grades and reserves (source: https://discoveryalert.com.au/news/free-cash-flow-gold-mining-industry-2025/).

That development is most easily achieved through M&A, i.e. buying projects with plenty of gold from smaller players, and that's the demand that companies like Gorilla Gold (GG8) are trying to supply or cater for.

It's not easy. It takes a lot of drilling, which takes a lot of money, but GG8 have the cash and they're certainly doing the drilling. And at the end of the day, it's still a lot quicker than taking one of these projects through to production, which might be best done by an existing gold producer. GG8 have a number of highly prospective projects and they can hopefully prove up Lakeview and Comet Vale and then sell that off and recycle that cash into their next projects, and so on. Either that or one of the larger players might just buy all of GG8 - at a decent premium of course.

So, yeah, I bought a small position in GG8 this morning.

High risk, as all explorers with zero production are, but as high risk punts go, this is one of the better ones I've come across lately.

Gorilla Gold do have a lot of positives, as I mentioned earlier in this post.

I also bought a small position in Rox Resources (RXL) yesterday, a gold project developer whose Youanmi GP (gold project) sits directly north of (and very close to) Ramelius' exceptionally high grade Penny gold mine. In their 12th March, 2024, "Ramelius delivers 10 Year Mine Plan at Mt Magnet" Announcement Ramelius Resources (RMS) said that their Latest Mineral Resource for Penny (at that time, just over a year ago) was 380kt (thousand tonnes) at 22g/t Au for 270koz Au (270 thousand ounces of gold) with Penny West now included in their Penny Production Target of 380kt at 15.9g/t Au for 194koz (effective from 1st July 2024). RMS truck that ore from Penny to Mt Magnet, and it's significantly increasing their gold production and lowering their costs at Mt Magnet.

So far, RXL's grades at Youanmi aren't quite that spectacular - but they're certainly decent - they've declared a mineral resource estimate (MRE) of 2.3 million ounces (Moz) of gold at the Youanmi Project with the open pit portion estimated to contain 6.5 million tonnes (Mt) of ore at 2.7 g/t for 0.6 Moz of gold and the underground portion estimated at 9.7 Mt of ore at 5.5 g/t for 1.7 Moz of gold.

RXL is still very early stage and many punters will likely bypass them simply because their gold is intimately associated with sulphide minerals and silicates in zones of strong hydrothermal alteration and structural deformation. Typical Youanmi lode material consists of sericite-carbonate-quartz-pyrite-arsenopyrite schist or mylonite which frequently contains significant concentrations of gold.

The short version is that it's sulphide ore that requires additional processing to liberate the gold, however that's being done successfully at scale all over the place, including by Emerald Resources (EMR) at Okvau in Cambodia, and the Golden Mile ore, which is the primary ore type at NST's KCGM (a.k.a. the Super Pit, Northern Star Resources' largest mining operation), is known for containing abundant sulphides, including minerals like pyrite. That's one of the reasons NST weren't afraid to buy DEG (De Grey Mining) for $5 Billion recently because the ore at Hemi is primarily a sulphide ore, containing significant amounts of the sulphides pyrite and arsenopyrite.

That stuff can and is being viably mined, but a lot of people associate sulphide ore with cost blowouts, low recoveries and even company failures, citing the Wiluna Gold Mine in Western Australia as an example, however Wiluna Mining Corporation (formerly known as Blackham Resources) had other issues including logistical and funding issues coupled with too much debt, in a time of significantly lower gold prices, which ultimately led to them entering voluntary administration in July 2022.

On the flip side, one of the highest grade and most profitable mines in Australia, the Fosterville Gold Mine in Victoria, owned by Agnico Eagle (previously Kirkland Lake Gold before they merged with Agnico Eagle) has been making very good money extracting gold from sulphide ore there for many years, using a process that includes crushing, grinding, flotation, bacterial oxidation (BIOX), and carbon in leach (CIL) circuits. This process first involves crushing and grinding the ore to free the gold-bearing minerals. Then, flotation separates the sulphide minerals, including pyrite, from the rest of the ore. The sulphide concentrate is then treated with BIOX to oxidize the pyrite, releasing the embedded gold. Finally, the gold is extracted through a CIL circuit, which uses cyanide to dissolve the gold and then absorbs it onto activated carbon.

Extracting gold from sulphide ore is absolutely doable and people really shouldn't be scared of it, but some still are.

Finally, the ore at Ramelius' Penny mine is also sulphide ore, and Ramelius is probably the natural owners of Youanmi, IMO, so will likely buy Rox (RXL) at some point - again IMO - no guarantees - but RMS do have their hands full currently with the takeover of Spartan (SPR) which is going to take another 2 or 3 months from here.

OK, I got sidetracked talking about Rox and sulphide ore there for a minute, and this straw is supposed to be about Gorilla Gold, but it is relevant because Gorilla Gold has identified sulphide ore at both the Lakeview and Comet Vale projects. At Lakeview, the gold mineralisation is associated with quartz veining, sulphide development, and biotite alteration within a major fault. Specifically, that mineralisation has been associated with pyrrhotite and chalcopyrite sulphide development within quartz-carbonate veins. At Comet Vale, the Sovereign Prospect has high-grade gold mineralisation associated with biotite alteration and fine sulphide in quartz veins.

So, again, people may be thinking that's all too hard and they'd rather invest or speculate in gold projects that do NOT contain sulphide ore - because it should be a cheaper and easier to liberate the gold (extract the gold from the ore) from oxidized ore (or oxide ore) than from suphide ore. Sure, but grades matter. All other things being equal (and they rarely are), I'd rather invest in a project that has a heap of gold at 4 or 5 grams per tonne in sulphide ore than a project that has between 0.5 and 1.5 grams per tonne in oxide ore. As long as the people building the mill know what they're doing, and everyone's done their homework properly during the PFS and the DFS (now mostly just being called the FS - feasibility study) stages.

But, once again, always remember that explorers and project developers all carry far more risk than producers do, so if you want to roll the dice with these sort of companies, keep the position sizes appropriately small, and only speculate with what you can comfortably afford to lose.

Disclosure: As of right now (14th May 2025) I hold the following gold companies:

Explorers and Developers: Meeka Metals (MEK, who are very close to production now), Gorilla Gold Mines (GG8), Rox Resources (RXL), Medalion Metals (MM8) and New Murchison Gold (NMG). All held in my largest real money portfolio, with only MEK held here on SM.

Gold Producers: Northern Star Resources (NST), Genesis Minerals (GMD), Ramelius Resources (RMS), Evolution Mining (EVN, who produce gold and copper), Gold Road Resources (GOR, arbitrage trade on the Gold Fields Ltd takeover of Gold Road) and Bellevue Gold (BGL). All held in my two largest real money portfolios (including my SMSF) and most also held here on SM,

I sold all my Spartan (SPR) shares last week, as they were an arbitrage play on the takeover of SPR by RMS and I was happy to lock in the profit I'd made.

I also hold NRW Holdings (NWH) who do have a mining services contract with Evolution Mining at Mungari, and my largest position is in Lycopodium (LYL) who do a few different things but specialise in designing and building gold mills (processing plants). I also have a decent position in GR Engineering Services (GNG) who do similar work to LYL, but where LYL build plants outside of Australia mostly, GNG mostly build here in Australia. Both GNG and LYL do dozens of feasibility studies every year for different types of miners, but especially for gold and copper miners, which ranges from scoping studies to pre-feasibilty studies (PFS) to definitive feasibility studies (DFS, also just called FS) to front-end engineering and design (FEED) which all often lead into being awarded EPC (Engineering, Procurement and Construction) or EPCM (EPC + project Management) or EP&PM (Engineering, Procurement and Project Management) contracts if and when those projects do get a positive FID (final investment decision) by the project owners. I hold LYL, GNG and NWH both here and in my real money portfolios.

So, yeah, I do have plenty of exposure to gold, both directly and indirectly.