Kina Securities released an excellent FY22 result despite NPAT including provisions for a 45% tax rate. I exited large positions in KSL entirely IRL and on SM when the PNG Government released draft legislation to introduce the 45% bank super tax (up from 30%). If it weren’t for the super tax I would still be holding. Kina is an excellent business with ROE increasing to 17.9% and now trading on less than book value (x 0.9).

Results summary:

Full Year Result 2022 - Kina Bank delivers strong growth and ROE

• Underlying NPAT increased by 10% to PGK 106.1m.

• Net Fees and Commissions increased by 30% to PGK 116.2m primarily by continued development and build out of Kina’s channel network. Organic growth and digital expansion resulted in an increase of 78% in channel fees

• The Loan book grew by 11%.

• Kina grew its customer base by 19%, which delivered strong low-cost transactional deposit growth of 27.7%.

• Digital Channel growth of 89% year on year, due to expanded EFTPOS and terminal of choice strategy.

• Cost to income ratio remained flat at 58.7% with investment in a middleware API layer, and further investments in core technology and enabling infrastructure.

• Underlying ROE was 17.9% demonstrating Kina’s ability to generate quality returns.

• Reduction in impairment cost to PGK 4.8m. The lower impairment in the current year is due to such factors as the continued application of the asset recovery program of work and security database improvements contributing to robust loan and asset quality measures.

• Kina Investment Superannuation Services recorded an increase of 10% in total revenue associated with an increase in total funds under administration to PGK 17.3b and an increase of 4% in total membership.

• FX customer volume increased by 19%, albeit the revenue reduction was significantly driven by transactions using lower margin USD currency.

PNG Tax Implications

Management said in regards to the PNG Corporate Tax implications:

“In December 2022, the PNG government announced the 2023 budget with an increase in Corporate Income Tax for commercial banks from 30% to 45%.

It was also indicated in the budget announcement that further consultations will continue with the banking industry in the first half of 2023 to consider whether other tax alternatives may be more appropriate for the industry.

For the FY2022 full year results, the impact of the budgeted corporate income tax increase is reflected in the deferred tax assets (DTA). This has resulted in a revaluation inline with IFRS in tax credit of PGK 10.4m increasing the statutory NPAT to PGK 116.5m.”

Incremental improvement in ROE

Disc: Not held

No news out of Kina Securities that is!

So, what is going on with the Kina Securities share price? The share price closed up 4.5% today, and since June the share price has gradually crept up by 14%. There could be a number of things contributing to the recent buying strength.

Troubled PNG Election Now Over?

Perhaps it’s because Papua New Guinea's incumbent Prime Minister, James Marape, has been returned to the top job after following the country's controversial, and at times violent, national election? The election has been described by several analysts and MPs as the worst they have seen (ABC News, 9 August 2022).

Perhaps now the election is over there is more certainty and the people can get back to doing business once again?

New Government Focus on Agriculture?

Perhaps it’s because the government is more committed to expanding the key agricultural industries in PNG? For the first time Prime Minister, James Marape, has named dedicated ministers for coffee and palm oil.

“The appointments specifically spotlight agriculture in a very significant way, to see agriculture growth in the country,” said James Marape on Tuesday (The Guardian, 24 August 2022)

“Coffee production in the country is dominated by village-based small-scale farmers, who produce close to 85% of the country’s annual crop. It is a source of income for close to two million people – around one quarter of the population.”

“Coffee is the country’s second largest agricultural commodity after palm oil, accounting for 27% of all agriculture exports and 6% of the country’s GDP.”

“Marape said the coffee industry needed to be revived to bring in more export revenue.”

Are the planets aligning for Kina’s MiBank and regional agriculture?

Financial inclusion remains one of the most prominent structural issues for the PNG economy with over 70% of the population unbanked. Kina’s strategic investment with MiBank has been a key focus over the past year. Mibank onboarded 66,800 new customers during the year, resulting in 432,800 customers in total.

Progress in building digital services for the MiBank partnerships is steadily increasing productivity and ultimately accessibility to financial services and products. Our ability to onboard MiBank customers in Kina branches will materially improve accessibility across provincial areas.

A vital piece of infrastructure for Financial Inclusion and SME development is our branch expansion plans. We will look to open seven new branches in regional areas that will include a Commercial centre that will not only provide Lending products but will be a Hub for local business to utilise our expertise. Another important program is the rollout of our Point of Sale terminals to business in provincial areas. We will be adding another 1,000 terminals in 2022.

Is the market anticipating a healthy Q2 Report and a fat Dividend?

Kina is scheduled to deliver its Q2 report tomorrow (26 August 2022). Last year Kina’s statutory NPAT took a 26% hit due to one-off costs associated with the attempted acquisition of Westpac’s Pacific division, which was quashed by PNG’s competition watchdog. One analyst (S&P Global data) is forecasting underlying FY22 NPAT to increase by 15% to 111m PGK.

Earlier this year Kina said ROE had stabilised circa 16.7% and Net Interest Margin at 6.7%.

FY22 dividend yield is forecast to be a fat 13% (unfranked) based on the current share price. I expect the interim dividend to be upwards of 3cps (3.4% yield) paid early in October, similar to last year.

I am waiting in anticipation for the Q2 report tomorrow. Perhaps we’ll find out more about what has been driving the buying strength then?

Disc: Held IRL (6%) and Strawman (18%)

@DrPete123 I’ve expanded on the business and country risks for Kina. The Country risks are Moderate to High for most categories. Kina is not operating in a low risk environment and may not suit some investors.

Country Risks

Rather than repeat the PNG Country Risks in full here, this Australian Government -Export Finance Australia resource covers and rates the risks of doing business in PNG in some detail. I have summarised the risks below:

- Overall Country Risk - High

- Ease of doing Business - Low

- Risk of expropriation risk - Moderate

- Governance Indicators risk - High

- Risk of expropriation - Moderate

- Political risk - Moderate to High

Loan Default Risks

I think the biggest risk for Kina is loan defaults. According to SWS data Kina has a low allowance for bad loans (44%) and there is over 4% bad loans. .The ongoing impact of COVID19 on the economy could worsen bad loans.

Macro Environment

The PNG economy is dominated by the capital-intensive mineral and petroleum extractives sector and the labor-intensive agricultural sector. COVID19 has significantly affected PNG’s economy, which contracted by 3.3% in 2020, followed by a weak recovery to 1.3% growth in 2021. GDP growth is forecast to be 3.4% this year and 4.6% in 2022. https://www.adb.org/countries/papua-new-guinea/overview

Kina said “ Several key mining projects were put on hold and key resources such as coffee, vanilla and sugar experienced a slowdown due to COVID impacts. Despite this backdrop, growth in Kina’s targeted segments of corporate lending and FX products supported the strong underlying growth, demonstrating Kina’s expertise in the corporate market here.”

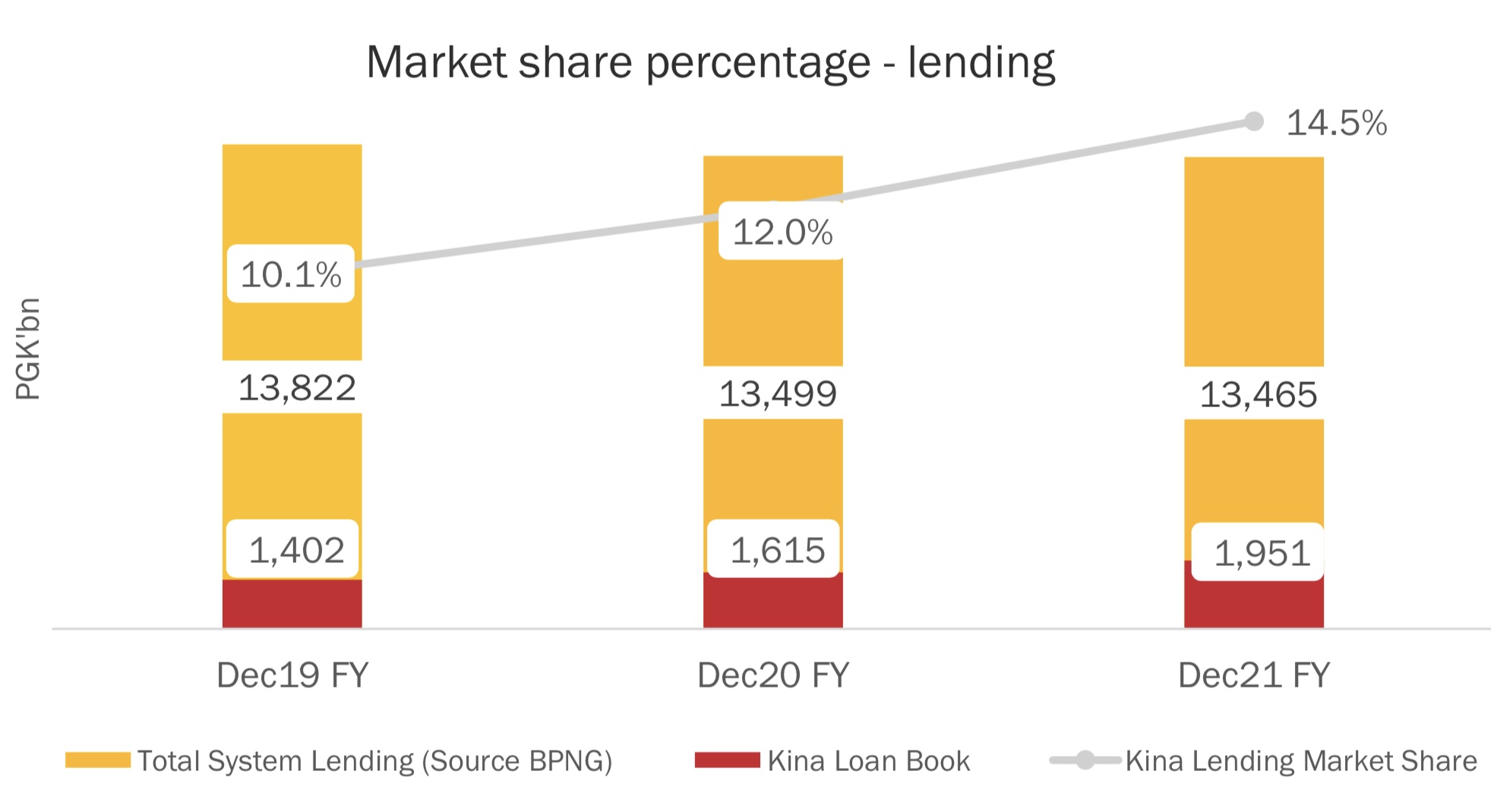

Competition

Kina has the second largest market share in lending at 14.5%. The largest bank is Bank of South Pacific at 65% and the remaining share is held by Westpac and ANZ.

Kina has increased market share in lending by 19% in FY20 and by 21% in FY21, a total increase of 45% increase over 2 years.

Disc: Held IRL and SM

Kina Securities Limited (KSL) is a diversified financial services provider in PNG offering its customers end-to-end financial solutions including asset financing, provision of commercial and personal loans, money market operations and corporate advice, fund administration, investment management services and share brokerage. Kina group has two operating divisions, Kina Bank and Kina Wealth Management (Commsec, 2022).

I think Kina is a quality business yielding a whopping 12% dividend and it seems to be incredibly cheap for those who are willing to take on some risk.

What’s happened to the share price?

(Commsec, 11/5/22)

(Commsec, 11/5/22)

The KSL share price reached $1.53 in Dec 2019 and as with many companies plummeted with the onset of COVID in March 2020 to a low of 64c. Since then the KSL share price has had a bumpy ride reaching $1.15 in Feb 2020 and currently trading at 86.5cps (11/5/22).

Kina’s agreement to takeover Westpac’s Pacific Business was blocked by regulator

On the 7 December 2020 Kina announced that it had entered into a sale and purchase agreement to acquire 89.91% of the banking operations in Papua New Guinea and 100% of Fiji (together, the “Pacific Businesses”) of Westpac.

On 14 September 2021 (despite Kina putting up a case in response the draft ICCC determination) the PNG ICCC opposed Kina’s Acquisition of Westpac PNG due to likely reduced competition in the PNG markets.

Subsequently on 22 September 2021 Kina and Westpac mutually agreed to terminate the agreement.

Of the $42 million advance payment Kina Securities put up front to purchase Westpac, only $32 million was returned. Westpac kept $10 million, as a “cost reimbursement”.

Westpac said it will try to find another buyer later this year, and will meanwhile cease investment in the Pacific network (AFR 3 May 2022)

Impact on FY21 Results

Taking into account the costs incurred in the transaction and the expected revenue from the Acquisition not occurring, Kina’s full year 2021 results were impacted, but still OK.

FY21 Results

https://www2.asx.com.au/markets/company/ksl

Despite the impacts of COVID and the failed acquisition in FY21, underlining net profit after tax increased by 27% and Kina has been averaging a return on equity (ROE) of above 16% (FY21 Report).

Kina’s Managing Director and Chief Executive Officer, Mr. Greg Pawson said, “Whilst we are disappointed that the Acquisition has not proceeded, this in no way changes the Company’s strategy of seeking both organic and inorganic growth in PNG and the Pacific Region, and the outlook for the Company remains positive.”

Macro Environment

The PNG economy is dominated by the capital-intensive mineral and petroleum extractives sector and the labor-intensive agricultural sector. COVID19 has significantly affected PNG’s economy, which contracted by 3.3% in 2020, followed by a weak recovery to 1.3% growth in 2021. GDP growth is forecast to be 3.4% this year and 4.6% in 2022. https://www.adb.org/countries/papua-new-guinea/overview

https://www.adb.org/countries/papua-new-guinea/economy

Kina said “ Several key mining projects were put on hold and key resources such as coffee, vanilla and sugar experienced a slowdown due to COVID impacts. Despite this backdrop, growth in Kina’s targeted segments of corporate lending and FX products supported the strong underlying growth, demonstrating Kina’s expertise in the corporate market here.”

Competition

Kina has the second largest market share in lending at 14.5%. The largest bank is Bank of South Pacific at 65% and the remaining share is held by Westpac and ANZ.

Kina has increased market share in lending by 19% in FY20 and by 21% in FY21, a total increase of 45% increase over 2 years.

Fundamentals

There is not much you can fault about Kina’s fundamentals as far as a bank goes:

Net Interest Margin (NIM)

The NIM margin is much more attractive for banks in PNG than here in Oz. Kina’s 2021 NIM was 6.7%. This compares very favourably to Australian banks currently around the 2% mark. This is possibly due to less competition for lending in PNG.

Earnings and Return on Equity

Kina has a good track record for increasing earnings over the past 6 years, although COVID19 has been brutal to the people in PNG. Kina’s performance has also been impacted by additional costs related to the failed Westpac acquisition. Both earnings and ROE have been effected, but not as much as you might expect under the circumstances. FY21 ROE was a very respectable 17%. This compares to the average Aussie bank hovering around 10%.

(Commsec, 14/05/22).

Future ROE based on forecast earnings growth of 23% over the next few years (1 analyst S&P Global, SWS data) could be as high as 24%. With the trend in organic and inorganic growth over the past 3 years, I wouldn’t count this out as the PNG economy recovers. However, for valuation purposes I would rather work on a more conservative future ROE of 17%, similar to Kina’s historical performance.

Risks

I think the biggest risk for Kina is loan defaults. According to SWS data Kina has a low allowance for bad loans (44%) and there is over 4% bad loans. .The ongoing impact of COVID19 on the economy could worsen bad loans.

Valuation

Working on forecast earnings of 23c per share in 2024, and a PE of 7 and discounting at 10% per year:

V = 7 x 0.23 x 0.7= $1.12 per share.

Alternatively, using Brian McNivan’s StockVal formula and assuming:

APC = 17% (Conservative Future ROE)

E = 79c (Shareholder equity per share = Shareholder equity/outstanding shares = 226/286 = 79c, Commsec, 14/5/22)

DI = 20% (percentage Kina reinvests back into the business, ie. normally pays 80% of earnings as dividends)

V = (17/10 x 0.2 x 17 + 0.8 x 17)/10 x 0.79

= $1.53

What this means is that if Kina can maintain a forward ROE of 17% (this seems realistic to me) and effectively reinvest 20% of their earnings into growth, you could expect a 10% return on your investment if you paid $1.50 for Kina shares right now. This makes Kina sound incredibly cheap at 86cps.

If Kina were trading at $1.50 right now, that would put it on an historical PE ratio of 11.5 based on FY21 earnings (13cps). Doesn’t sound ridiculous to me, at least not as ridiculous as its current PE of 6.6 based on FY21 earnings.

The fact is that Kina will probably never trade on a PE that reflects its fundamentals, because it is based in PNG and it is viewed as a very high risk.

I think that’s OK, KSL is cheap to buy and will be cheap to sell (on a PE basis). However, while you hold KSL at 86cps it is likely to continue to pay a dividend of least 12% (no franking credits unfortunately) while reinvesting 20% of its earnings back into growing the business. If that’s not a cash cow, I don’t know what is!

Please don’t be afraid to critique my reasoning here on Strawman, including use of StockVal. I could be horribly wrong with my assumptions, and if that’s the case, I’d rather know now!

Disc: Accumulating IRL and currently my largest holding on Strawman.

This morning Kina Securities released its FY21 results. As expected statutory NPAT was slightly (7%) down on last year, impacted by one-off costs associated with the termination of the Westpac acquisition. Underlying profit (excluding separation costs) was up 27%.

Key performance across the business looks good and has improved on last year. Nice fat dividend too! Kina is paying a 7 cps dividend on 8 April 2022 bringing the total to 10 cps (11% yield). No franking credits, but not such a problem in a tax free super account. Underlying ROE was 16.7%, very respectable for a bank.

Key highlights:

- Underlying NPAT increased by 27% to PGK 96.2m

- The Loan book delivered a 21% growth.

- Foreign Exchange (FX) revenue grew by 19%

- Net Fees and Commissions increased by 17% to PGK 89.3m

- The performance in non-interest income from fees and commissions and foreign exchange income contributed 18% to Kina’s strong revenue growth

- Cost to income ratio (underlying) maintained at 58%

- Reduction in impairment cost to PGK 6.5m

- Kina’s Funds Administration business achieved NPAT of PGK 10.1m, which reflects a 22% improvement.

Disc: Held IRL.