Consensus community valuation

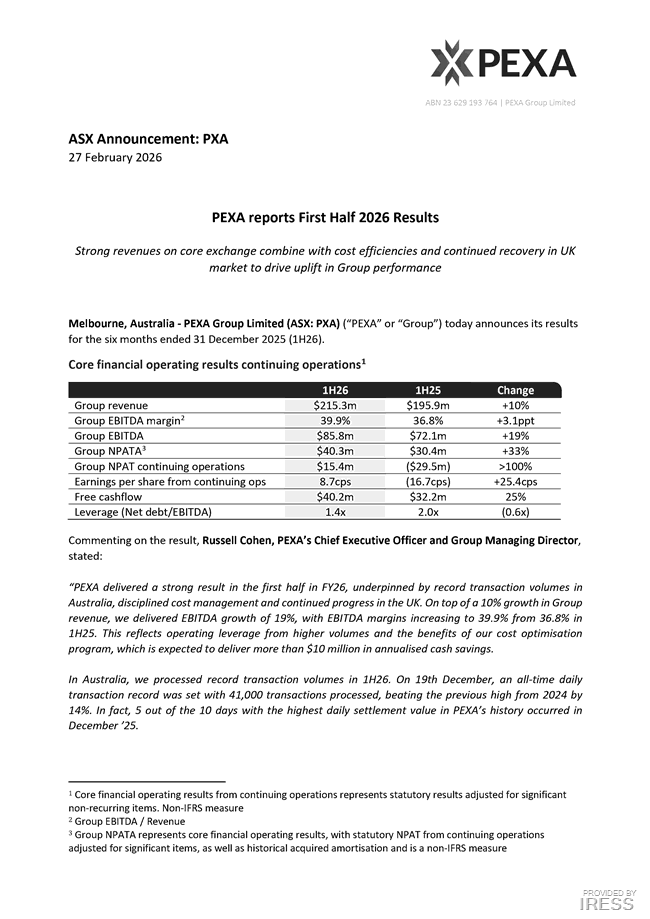

PXA has finally delivered a decent result (numbers below). No dividend but PXA has reduced leverage from 2x Net debt/EBITDA to 1.4x.

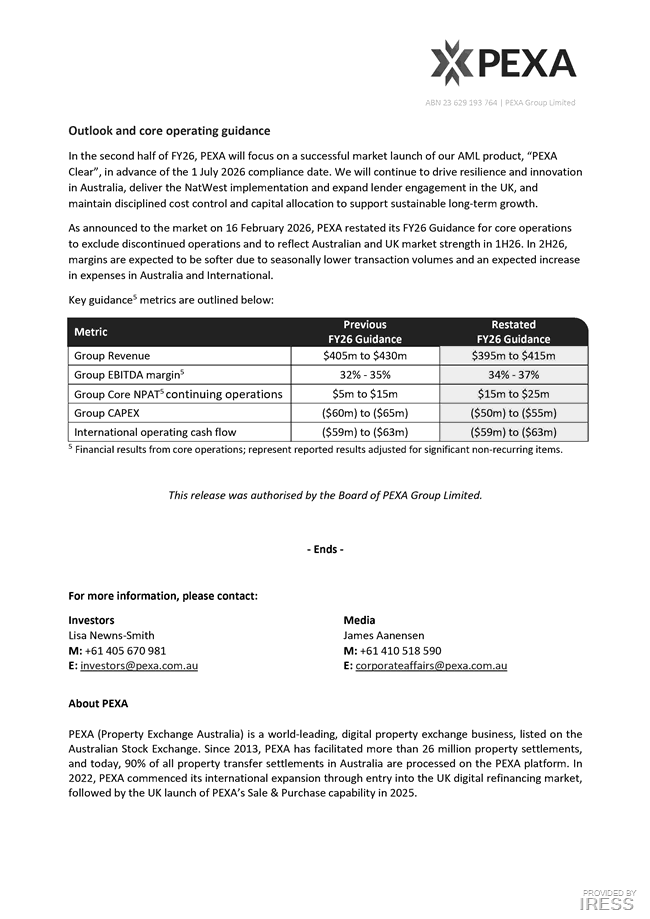

Revenue guidance for FY26 has been lowered but EBITDA margins have been revised up with higher underlying NPAT.

Market presently likes the result and guidance with shares up 7.69%.

Management Bios

Russell Cohen - Chief Executive Officer and Group Managing Director

Russell Cohen is a seasoned technology executive with more than 20 years of experience driving growth in the mobile, telecom and software industries across Asia Pacific. Prior to PEXA, Mr Cohen was the Group Managing Director of Operations at multinational technology company Grab, leading business performance, operations, platform safety, market expansion and a team of 3000 across seven countries. He also played a pivotal role in that company’s strategic growth throughout the region. Before joining Grab, Mr Cohen served as Board Director and Vice President of Business Development & Corporate Strategy at SoftBank C&S in Tokyo, a role he assumed after SoftBank’s acquisition of Brightstar Corp. At Brightstar, he was Regional Managing Director for Asia, overseeing nine markets, and founded the company’s Greater China operations in Hong Kong. He holds a Master of Information Technology from the University of Melbourne and a Bachelor of Commerce (Accounting & Finance) from Monash University.

Mark Joiner - Independent Chairperson

Mark is an experienced director of listed companies, currently serving as a non-executive director of Latitude Financial Services and Chairman of QBE Insurance Group Limited’s Australian and New Zealand subsidiaries. He has also held multiple directorships at NAB Group subsidiaries, including Clydesdale Bank Plc and JBWere. Mark served as Executive Director of Finance for NAB Group; CFO and Head of Strategy and M&A for Citigroup’s global wealth management business in New York; and Associate Director of Australian Ratings (now Standard & Poor’s). He also has 15 years of experience as a management consultant at Boston Consulting Group including as Senior Vice President, Global Head of Corporate Development. Mark is a Chartered Accountant and holds an MBA from the Melbourne Business School.

Helen Silver AO - Independent Non-Executive Director

Helen Silver has extensive experience as a non-executive director covering ASX listed, private company, not for profit and Government boards. As well as serving as a director of PEXA, Helen is currently an independent director of Crown Melbourne Limited, Deputy Chair of the Victorian Managed Insurance Authority and Chair of the Australian Children’s Television Foundation. In addition to her corporate success, Helen has worked at the highest levels of Commonwealth Government with the Productivity Commission, and Victorian Government in roles primarily in the Premier’s and Treasury portfolios, including as Secretary of the Victorian Department of Premier and Cabinet from 2008 to 2013. Ms Silver holds a Bachelor of Economics with Honours, Master of Economics and Honorary Doctor of Laws, all from Monash University.

Melanie Willis - Independent Non-Executive Director

Melanie has extensive experience as a non-executive director, including Challenger Limited since December 2017, Southern Cross Austereo since May 2016 and the Australia Pacific division of QBE Insurance Group Ltd since September 2020. Melanie was previously a non-executive director of Mantra Group and Pepper Group, Chief Executive Women and Chair of the Education Committee of the 30% Club. Melanie also serves as a non-executive director of PayPal Australia. Melanie has held executive roles as CEO of NRMA Investments (and head of strategy and innovation), CEO of a financial services start-up and director of Deutsche Bank, and has previously worked in corporate finance at Bankers Trust and Westpac. Melanie previously chaired the audit and risk committee at Mantra and was a member of the audit committee at Pepper Group. She currently chairs the risk committee and is a member of the audit committee at Challenger, chairs the audit committee and remuneration committee at PayPal Australia, chairs the risk committee at QBE AusPac, and chairs the audit and risk committee at Southern Cross Austereo. Melanie has a Bachelor of Economics from the University of Western Australia and Masters of Taxation from Melbourne University

Vivek Bhatia - Independent Non-Executive Director

Vivek is the current Managing Director and Chief Executive Officer of the Link Group.Vivek has over 20 years of experience in financial services, government and management consulting. Prior to joining Link Group, Vivek was Chief Executive Officer of the Australia Pacific division of QBE Insurance Group Ltd, and the inaugural Chief Executive Officer and Managing Director of iCare (Insurance and Care NSW). Prior to this, Vivek co-led the Restructuring and Transformation (RTS) practice at McKinsey & Company across Asia Pacific and held senior executive roles at Wesfarmers Insurance, including responsibility for leading the Australian underwriting businesses of Lumley, WFI and Coles Insurance as CEO, Wesfarmers General Insurance Limited (WGIL). Vivek holds an undergraduate degree in engineering, a post graduate degree in business administration and is a CFA (ICFAI).

Paul Rickard - Non-Executive Director and Commonwealth Bank of Australia Nominee Director

Paul served as a non-executive Director of PEXA from November 2011 to November 2018, joining the Board about twelve months after the company’s formation. Paul is an experienced director of listed companies, currently serving as a non-executive director of Tyro Payments Limited and WCM Global Growth Limited. At Tyro, he is the Chair of the Audit Committee and the Chair of the Risk Committee. He has more than 30 years’ experience in the financial service industry. He was a senior executive with the Commonwealth Bank of Australia for over 15 years, and was the founding managing director of CommSec. Paul was named ‘Stockbroker of the Year’ and admitted to the Industry Hall of Fame in 2005. Paul holds a Bachelor of Science degree in Mathematics and Computer Science from the University of Sydney, and a Diploma in Financial Planning from RMIT University.

Jeffrey Smith - Independent Non-Executive Director

Jeffrey Smith is an experienced executive who has worked at the highest level in the technology and digital transformation space. Jeffrey is currently an Independent Non-Executive Director at ANZ Group Holdings Ltd (ASX: ANZ) and serves as a member of several board committees, including its Digital Business and Technology Committee, Risk Committee, Human Resources Committee, and Nominations and Board Operations Committee. He is also a Director of Sonrai Security Inc. Prior to this, Jeffrey was a senior executive within global and technology organisations including Telstra, Honeywell, Toyota, IBM, Suncorp and World Fuel Services Corporation.

Georgina Lynch - Independent Non-Executive Director

Georgina Lynch has over 30 years combined executive and board experience in the property and financial services sectors, including significant experience across all classes of property and in corporate transactions, capital raisings, initial public offerings, funds management, corporate strategy, and mergers and acquisitions. Georgina is currently: Chair of Cbus Property and a member of its Audit, Risk, Compliance & ESG Committee and Remuneration Committee; Chair of Waypoint REIT and Chair of its Nominations Committee; an Independent Non-Executive Director of Vicinity Centres and a member of its Audit & Risk Committee and Remuneration Committee; and a Non-Executive Director of Evolve Housing, a community housing provider, and a member of its Audit and Risk Committee. She was previously on the Boards of Tassal Group (from 2018 to 2022) and Irongate Group (from 2019 to 2022) until their takeovers. Georgina holds a Bachelor of Arts and Bachelor of Laws degree, BA,LLB; Grad Dip Legal Practice