Straws are discrete research notes that relate to a particular aspect of the company. Grouped under #hashtags, they are ranked by votes.

A good Straw offers a clear and concise perspective on the company and its prospects.

Please visit the forums tab for general discussion.

- Recent

- Votes

PYC had an investor update this morning. CEO Rohan Hockings re-explained each of the 4 programs with no real new news, the 50 minutes being an exercise in strengthening investor confidence and the share price. Slide deck issued at the same time.

Polycystic Kidney Disease (PKD): Potentially the most valuable asset will in CY 26 Q4 release Part A and Part B SAD data.

Phelan McDermid Syndrome (PMS) - currently still working with safety and toxicity in Non-human Primates. First patient dosing not until mid CY27.

Retinitis Pigmosa (RP11 drug) - slow progress, partly as a consequence of the disease progression itself taking decades. PYC attempting to get FDA to reduce the "high bar" of 15 letters sight improvement. Ongoing discussion and trials.

From the Q&A sessions:

- CEO was asked about Firetrail Funds Management exiting the register. Response was he had no information as to why and did not know who the new replacement investors were.

- PYC are actively engaging with US banks to get research on PYC with a view to obtaining a NASDQ listing. Believes the deeper US biotech market will better appreciate the PYC assets.

- Is aiming for an additional 2 people with a US focus to join the Board.

A long hard slog for PYC but with the benefit of 5 year cash runway and a clear strategy.

PYC this morning released 70 pages of PhI/II research to be presented to the ARVO ophthalmologist conference in Denver Colorado. The material was in relation to:

- VP001 for Retinal Pigmosa 11 (RP11)

- PYC-001 for Autosomal Dominant Optic Atophy (ADOA)

So what did all this mean? Some new material and already known information. The AI summary take on it:

"New Data (Previously Unknown to Market)

- PYC-001 Visual Acuity Gains: While the start of the SUNDEW Phase 1A study was known, the specific "encouraging improvements in visual acuity" in human patients were not previously disclosed. This is the first clinical evidence of efficacy for this candidate.

- High-Resolution Structural Maintenance: The specific findings from Dr. Jessica Morgan regarding peak cone density being maintained or improved via adaptive optics imaging are new, technical data points.

- Specific MAD Sensitivity Metrics: While the market knew the VP-001 MAD study was underway, the specific results—such as multiple retinal loci improving by $\ge$7dB—provide a level of granular success that was previously undisclosed."

So more like some incremental positive news that should progressively underpin the value of these two assets.

Some thoughts:

- The above two conditions are degenerative eye diseases that deteriorate over decades - so the trials also have to be long duration to get any meaningful data. For RP11 Phase 3 recruitment is intended to start in CY27 and if all progresses well, and it will not be until CY32 before you would see a commercial launch. Zzzzz.

- The bulk of the company value is in the potential of the Polycystic Kidney Disease Asset. This is the big one and is currently in Ph1/2 clinical trials. However all three conditions are "linked" in so far as they are haplo insufficient genetic diseases and PYC uses the same treatment approach to each. And whilst all three are independent trials, a setback with either RP11 or ADOA would adversely impact perceptions of the value of the Polycystic Kidney disease asset.

- At the last quarterly PYC had an astounding $666m and is spending around $15m/qtr.

- The Duracell bunny CEO Rohan Hockings was on Strawman back in May 2024 telling us how he hoped to have something significant by the end of the year for ODOA and RP11. Not a criticism of the remarkable Rohan, but these things always seem to take a lot longer than initially expected.

Interesting with this announcement Rohan did not provide a shareholder update. I guess now with $666m in his money clip he has got better things to do than waste time with retail shareholders.

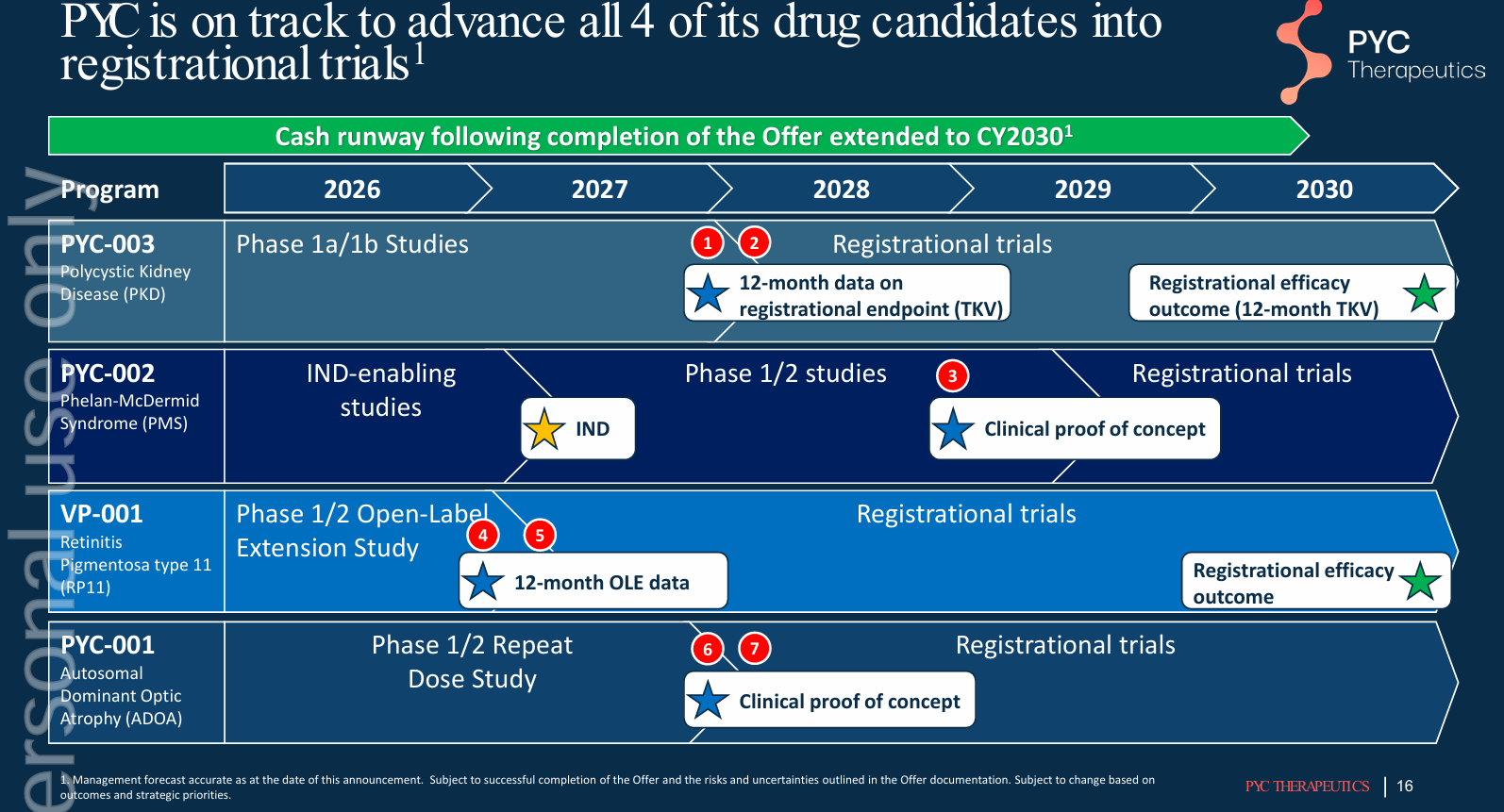

ASX listed biotech PYC Therapeutics released their investor update yesterday. Slide 16 (below) shows the upcoming milestones across the 4 drug development programs. Readouts start in 2027 and are spaced out to the end of 2030, so patience needed.

This month PYC will raise a minimum of $600m and is set to have a cash balance of around $750m which PYC maintain will fund them to the middle of CY30. Post the raise later this month, PYC will have a market cap of around $1.5b. Three and a half years ago PYC's market cap was $220m, and being a pre-revenue biotech has done nothing but lose money in the intervening time. Full credit to the remarkable CEO Rohan Hockings.

Given how market wonderkids of REA, WTC, XRO, PME and TNE have performed over the last 6 months PYC is now recommended a blue chip investment suitable for conservative mum and dad investors or near penniless widows and orphans.

PYC MD Rohan Hockings announced this morning PYC are raising $653m to ensure they are funded all the way to CY30 and can follow through to commercial milestones all its four drug development programs. These being:

- ADPKD drug candidate, PYC-003, (Polycystic Kidney Disease) into a registrational trial (This is the big one - the company maker and PYC are intending to spend a staggering $350m on this)

- PMS drug candidate, PYC-002, (Phelan McDermid Syndrome) into first in human trials and generate clinical proof of concept.

- RP11 drug candidate, VP-001, (Retinitis Pigmentosa – a rare genetic disorder of the eye) into a registrational trial.

- Fund progression of PYC’s ADOA Autosomal Dominant Optic Atrophy) drug candidate,

Back in September of last year there was a falling out between the then chair Alan Tribe (an older rich accountant, WA property developer and PYC major shareholder) and MD Rohan Hockings. Joining the dots, Alan shit his pants at the rate PYC was spending money and wanted to slow down the pace and number of drugs under development. Over the last decade Alan Tribe has reached into his own pocket and jammed a staggering $150m into PYC.

Hockings ended up resigning and Alan Tribe took over as both Chair and MD. Which was of course laughable and the shares tanked. Within a couple of weeks sense prevailed, Hockings came back as CEO, Tribe resigned and Hockings set about putting together a new Board to better reflect the challenges PYC faced.

Todays announced raise is at a 6% discount to Friday’s close. Will be interesting to see what local institutions have taken an allocation. Firetrail was already substantial. Alan Tribe had around 32% of the company pre-raise. The entitlement part of the offer is a 3 for 5 issue to raise $525m. To maintain his company ownership share would mean Alan ponying up around $170m. Will be interesting to see what happens here.

Looks like Rohan has taken a leaf from Alan Taylor at CU6 and raise a boatload while he could. At the end of the cap raising exercise PYC will have $830m. This and the current market cap of PYC is $930m. Amazing stuff. They are currently speeding around $60m/yr. Hockings has stated this additional cash will get them through to CY 30, so clearly PYC are planning to go at it even harder.

Bloom Burton Securities Inc. is acting as lead manager to the Placement and certain shortfall components of the Entitlement Offer in the United States and Canada. E&P Capital Pty Ltd and Barrenjoey Markets Pty Ltd are acting as joint lead managers for the Entitlement Offer. Significant, as you may remember at their last capital raise they had trouble getting the shortfall cash out of the underwriter.

MD Rohan Hockings was on S/M back in May 2024 indicating, with reference to his lead program RP11 they should have something significant by Christmas. Not a criticism of Hockings, but here we are 20 months later and there is nothing commercial about RP11 yet announced.

Well worth remembering, particularly with biotechs it almost always takes longer and costs more than these company leaders estimate.

It was announced today the current chair of PYC moneybags Alan Tribe, (owner of 34% of the company) will step down from the board and Peter Coleman will be independent chair. Mr Coleman formerly had 10 years as CEO at Woodside.

By way of background, in September of this year Alan Tribe must have woke one morning with an early onset case of faecal incontinence and went and forced Rohan Hockings resignation and took over himself as MD as well as retaining his chairmanship. Having old moneybags as MD, even for a short time was like asking the stewardess to fly the airplane and it only lasted a week and Rohan Hockings was back.

On the 13/10/25 Rohan hosted a webinar in an attempt to settle everyone down, where he explained he was now back as MD, all differences had been resolved and the progress of the PYC science had not suffered at all as a results of the antics of the previous weeks. In a roundabout way Rohan made known Alan Tribe wanted to pull back on at least two of the drugs being developed in order to save cash. Rohan was his usual effusive and diplomatic self, saying: “the company has outgrown its board” (meaning: “I still think Alan is a prize f%#kwit but we have agreed to tolerate each other for now”).

PYC had $150m of cash as at 30/6/25 and is spending somewhere between $15m - $20m per quarter. Rohan indicated he is fully committed for the next 24 months. By then all four drug development programs will have human readouts. Rohan at the above briefing expressed frustration the technical milestones PYC had achieved were not reflected in the share price and was considering a NASDQ listing to improve the share price. Maybe, but this did not seem to work for Telix. PYC has a current market cap of around $750m and there have been $290m of capital raises since 2018.

The four drugs being developed for the following conditions and their status as at 27/10/25 are:

- Polycystic Kidney Disease (PKD) ▪ Progression into Part B of the Single Ascending Dose (SAD) study in PKD patients. Presentation of the safety data from Part A of the SAD study at the Australian and New Zealand Society of Nephrology conference.

- Lead blinding eye disease (RP113) ▪ Progression into an Open Label Extension (OLE) of the Multiple Ascending Dose (MAD) study in RP11 patients and preparation for a Type D meeting with the US Food and Drug Administration (FDA) to align on a registrational trial design.

- Second blinding eye disease (ADOA5) ▪ Presentation of data from the SAD study at the Neuro Ophthalmology Society of Australia conference and progression into a global MAD study directed towards establishment.

- Neurodevelopmental Disorder - Phelan McDermid Syndrome (yes same condition as NEU is going after and excellent recent analysis by MikeBrissy on NEU) Generation of Non-Human Primate (NHP) data to complement the outcomes previously generated in patient-derived models and confirm progression into formal Investigational New Drug (IND) enabling studies10 and Presentation of the pre-clinical data pack supporting this drug candidate at the Oligonucleotide Therapeutic Society meeting.

From the same 27/10/25 ASX notice: “PYC is now preparing for upcoming human safety and efficacy read-outs across all four programs with data expected in: CY25 for the RP11 program; CY26 for the PKD and ADOA programs; and CY27 for the PMS program.”

PKD is the one with potentially the largest return, the condition affecting around 600,000 in the US. PYC appear to have enough cash to get them to well into CY27.

Wilsons has a PYC holding, and earlier this month Firetrail went substantial - not that these two are noted biotech investors greats.

By way of a potential upside, PYC competitor in PKD targeting microRNA drug development Regulus were acquired by Novartis in June this year for US$800m and a further US$900m assuming FDA approval. This was done based on a 1b trial and Rohan Hockings claims he can get 10 times as much drug into the kidney of PKD sufferers as has Regulus. Big numbers, big dreams.

Today PYC announced:

“PYC Therapeutics Limited (ASX:PYC) (PYC or the Company) announces the appointment of Chairman Mr Alan Tribe as the Company’s Managing Director following the resignation of Dr Rohan Hockings as Chief Executive Officer and Executive Director. Dr Hockings has given 2 months’ notice and it is currently expected that he will leave the Company by 16 November 2025.”

Mr Alan Tribe is (was?) a wealthy WA accountant, property developer and PYC True Believer who back in February 24 kicked in a further $35m in the most recent $146m PYC capital raise. Alan owns around 34% of PYC.

The lively and affable ex CEO Rohan Hockings, the driving force behind the science at PYC was on Strawman back in 29/5/24. This interview makes a contrast to the recent SM interview with the prickly Alan Taylor of CU6. Rohan did not own much of PYC, however at one point his father a Perth cardio, had around 5% from memory.

Looks like one hell of a blow up, though we may never really know just what happened. Not good news for science, PYC investors and Alan Tribe in particular I would think.

PYC set out to raise A$146m just prior to all this current market turmoil. Well done to CEO and Strawman guest Rohan Hockings. If he tried a capital raise now he wouldn’t get 146 cents.

However in today’s announcement there is an issue in PYC getting the last $13m.

“PYC is currently in the process of completing a ~$146m Entitlement Offer. The Company today announces that it has received ~$133m of the total contemplated (bringing the Company’s cash runway to >$200m2) with the remaining balance of ~$13 million expected to be received prior to the end of the month. The underwriter of the remaining balance has advised the Company that they have a liquidity issue and have requested an extension of time through to 30 April to pay the outstanding liability.”

c6d443f74829da1b0b873c04dbf313e0

How much of this type of counter party risk shit is out there everywhere?

Hidden for the moment, but will all come to light if this current correction continues.

Stinky Pete from Toy Story was right when he said: “It’s a dangerous world out there.”

PYC announced this morning a 1 for 4 pro-rata share offer to raise $145m. In the absence of any announced drug development breakthrough and perhaps due to the specter of this capital raise, PYC’s share price has drifted over the last 4 months from $2 to around $1.27 last week.

Notable about the cap raise is:

- There is an accelerated institutional placement and a call on the “True Believers”. Or more correct the one big “True Believer” - which is of course PYC chair Alan Tribe whom currently owns 34% of PYC. Alan has committed to putting in $35m. If Alan took up the full pro-rata entitlement then he would be tipping in $67.4m. So I guess even giga-bucks Alan has his limits to both his bank account and conviction - or maybe he is just being kind and allowing room for new institutional investors.

- If they don’t get the full $145m, PYC are saying they will be happy with just $105m. They have commitments for $70m from existing shareholders.

- Just how costly these drug development programs are. This cap raise, if delivered in full will mean PYC will have $215m in cash. Whilst three of the four development programs are in clinical development, they are early stage with the most advanced drug for the treatment of Retinitis Pigmentosa Type 1, is at Stage1/2. The raise if accepted in full, will fully fund PYC's work on their four lead drugs through to FY27.

- E&P Capital Pty Ltd and Barrenjoey Markets Pty Limited are the joint lead managers. The institutional offer not underwritten and the raise is at a 3% discount to the last close.

Assuming PYC raised the asked for $145m, then at $1.25/share PYC will have a market cap of around $745m. Big for an Australian speculative biotech. However there is a potentially huge upside with PYC, particularly in relation to their polycystic kidney disease drug which this month started human trials.

Wilson Asset Management, not known for their biotech investing has taken a position with PYC, as revealed in one of the Oscar/Tobias folksy little shareholder updates late last year.

Will be interesting to see how the placement is received, and if any new investors end up joining the register.

PYC released today its lates preclinical data for Autosomal Dominant Polycystic Kidney Disease (PKD).

Investors & News | PYC Therapeutics

Of the three RNA drugs and their associated carrier peptides PYC is developing, the treatment for PKD is the largest and most financially significant. PKD is estimated to have a potential annual market in the US of around $10b. This is contrast to the two other orphan genetic conditions PYC are proving up for Retinitis Pigmentosa, estimated annual market $1b and Autosomal Dominant Optic Atrophy with an estimated annual market of around $2b.

Today’s results were for lab grown tissue PKD affected samples, mouse models and non human primates (monkeys). It can all be read in their announcement today, however very schematically what they were able to demonstrate was:

i) A satisfactory drug safety and tolerability profile

ii) An efficacy profile in 3D models created from PKD patient kidneys and in mice & monkeys

iii) High target tissue concentrations at low drug doses.

It remains to be seen how the drug functions in humans. However these are very impressive results that permit PYC moving into human trials.

Shares went up a modest 7% on the news, giving PYC a market cap of now $933m.

What is it? Make it quick Schoonie.

On Friday 31/8/24 PYC released to the market two announcements. One stating they had orphan drug designation for the Retinitis Pigmentosa (RP-11) treatment drug under development, VP-001. Not unexpected however a positive.

Secondly they announced a Q3 update.

What was the Q3 update all about?

There was a generalised discussion of where PYC is up to in its three drug development programs (and an early stage further drug being developed for Phelan-McDermid syndrome) and the huge opportunity ahead. This was correctly, tailored to new investors.

The CEO Rohan Hockings indicated the timing of the next two RP11 readouts, which are this month and just after Christmas. The timelines of the development program were given on presentation slide 13.

Rohan spent considerable time on the topic captured in the slide heading: “RP type 11 human safety and efficacy data a deep dive today”.

So why did he do that?

I don’t know I am not Rohan Hockings. However, I suspect it was in response to some investor disquiet in relation to the latest RP11 results released on the 12/8/24.

And what was the investor disquiet?

The Retinitis Pigmentosa trial results for the 3 patients in the SAD trial dosed at 75 micrograms were released on the 12/8/24. The results were reported as an improvement in the 2 of the 3 patients - all well and good. However the results were reported as decibels of eye function improvement. This was a different to the way in which they had reported the results in of the 30-microgram trial a month earlier. And of course, you would expect a better result for the 75 microgram trial versus the earlier 30 microgram. If you were paying attention you would think: “Hu, what is going on here?” On the results release the shares flopped down to 10 cents. Up to this point the VP-001 safety and efficacy results were very encouraging.

Well did Mr Hockings satisfactorily explain the above?

Firstly the CEO Rohan Hockings is a very good communicator and leader. Secondly it is early days for PYC and investors have a propensity to demand a miracle a month or they tend to lose interest.

Not interested in what you think of the CEO or what the market did or did not do. Did the CEO explain what you seem intimating was some sort of a stumble the company attempted to disguise?

At great length the CEO explained it was still a point of some contention as to what marker/s of improvement the FDA would ultimately accept as an endpoint/s. He outlined the two methods of microperimetry for measuring improvement in visual acuity. That being: “whole of grid” or taking 5 or more points and seeing if they move by 7db or more.

Not following you.

Well in a sense from an investment perspective, you don’t have to.

Explain yourself

The CEO after discussing the ins and outs of retinal functionality and measurement never addressed, to my satisfaction anyway, as to why the reporting of the 75microgram and 30 microgram results were not provided on the same measurement scale. Which would make you think that the higher dose was not as efficacious as the low dose. How does that make sense or build confidence in what PYC is doing?

Well, did either you, or someone just ask the CEO that bloody question!

No one else did. I did and received no response.

Hang on. No one asked the question. Then there is no investor disquiet! Sounds to me like you and you alone have got it all cocked up Scoonie!

That could be true. However I asked the question via the moderator and it was not passed on and addressed by the CEO. I don’t know if I was the only one with this query or not. Subsequent to the investor update I asked it again, and again silence.

So what are you trying to tell me?

At 13 cents PYC is sporting a solid market cap of around $600m. Whilst it has around cash of around $80m it has no revenue and is not likely to have any for several years, even if the research goes to plan.

Whilst the three drug development programs are all independent and the first in the pipeline RP11 is the least valuable, success with RP11 is critical for PYC to have a decent shot at developing the remainder of the pipeline.

Sounds like you are on a loser Scoonie.

Well in any early stage biotech you could say that and 95% of the time you would be correct. My interpretation, for what it is worth, is the results reported on the 12/8/24 have shifted the odds against PYC. However I would not write them off.

Eh! Thanks for nothing Scoonie.

What is it Scoonie?

PYC released their results for the 75 microgram dose patients stating:

“PYC today announces an improvement in vision in 2 additional patients with RP11 after they received a single 75 microgram dose of VP-0012”

“Two out of the three RP11 patients in this cohort had enhanced retinal sensitivity across the entire macula at 3 months of follow up when compared to baseline.”

Also: “the third patient in cohort 3 of the SAD (whose results were not included in the announcement of 5 August because they did not undergo microperimetry assessment at 3-4 months post-dosing) completed their 6-month follow-up visit including assessment on microperimetry. The results show a marginally slower rate of disease progression in the treated eye (-0.5 dB) when compared to the untreated eye (-0.7 dB) on whole grid mean retinal sensitivity at this time-point.”

Yeah, all sound all fine and dandy. But, notice how the reporting format was not the same as the results released on the 5/8/24. They did not report on Scotomas number reduction, nor did they report these results as being ‘clinically significant’ with reference to FDA blinding eye disease endpoints.

I told you multiple times, but you won’t listen, your on a complete loser mate. These things go along fine and then, crack, the whole ship springs a giant leak and sinks like a rock.

Agree, whilst today’s results are positive, you make a valid point. Today's reported results are a lesser outcome than might have been expected. Given the very positive outcomes from the 30 microgram dose you might have expected a much improved results from a doubling of the dose.

And all that stuff about them “preparing for a registrational trial, scheduled to commence next year” is just puss. There to fill up the pages and make everything look on good. Get out of it you moron while you are still in front.

Maybe, it is early days. There are the Multiple Ascending Dose readouts to come between now and the end of the year and the Single Ascending Dose Part B extension readouts. In addition, there is the near-term wider program consisting of Autosomal Dominant Optic Atrophy (readouts in 2024 and 25), Autosomal Dominant Polycystic Kidney Disease (animal readouts in 2024, human readouts in 2025). These is around $100m cash runway to fund the program this year and into 2025.

Hope springs eternal. Fool.

What is it Scoonie? I thought I made things clear to you on the weekend, and now your back again.

Well, PYC have just released some further results in their retinal drug VP for treatment of patients with the blinding eye disease Retinitis Pigmentosa type 11 (RP11).

So?

They are very positive. They had one patient out of three in Cohort 3 of the Single Ascending Dose (SAD) trial previously report improved eye function. That was positive, now the same patient plus an additional patient is showing improvement at 4 months. What is more the extent of the improvement exceeds the FDA provided guidance criteria. I think this is a big deal.

Doesn’t seem much to me.

And there is lot more readout to come between now and Christmas. Of special importance this month there will be a readout on the single dose at 75 micrograms. This is the highest dose to date, and you might expect that this one will give a positive result if two out of three of the lower dosed patients in Cohort 3 have shown improvement at 4 months.

Further the Multiple Ascending Dose trial (MAD) will provide readouts in Q3 and Q4.

In addition there is the extension to the SAD trial announced last month that will provide further readouts in Q3 and Q4.

Results to date are impressive and if they can keep producing positive results, and from the evidence to date the odds are in favour of them doing so, then knowledgeable investors and people in the industry will begin to take notice.

Oh right, and I suppose you are one of those “knowledgeable investors” you dumb prick. Zero qualification in retinal eye disease, biotechs or bloody anything relevant as far as I can see and now you think you know everything. The closest you ever come to a scientific breakthrough was when you knocked over a bunsen burner in Year 8, you useless f$#k. You’re a bloody dick-wit.

And what more you wouldn’t know if your arse was on fire!

Scoonie stood up, moved his right shoulder forward, turned his head and looked down. Reassured he walked slowly towards the door.

PYC announcement 23/7/24:

“PYC today announces that it has received approval from the Institutional Review Board (IRB) governing its ongoing clinical trials in RP11 to allow patients who have received a single dose of the drug candidate in the existing SAD study to rollover into an open-label extension arm of this study (known as Part B of the SAD) under which they will receive multiple doses of PYC’s drug candidate.”

This information is an important and a positive development. However currently is not material in terms of knowledge of drug efficacy or company valuation. As a consequence of the above development you would expect the probability of positive efficacy readouts has increased due to both additional drug dosage per patient and additional patient numbers.

RP 11 readouts will happened between now and Christmas in the Part B SAD study as well as the Multiple Ascending Dose study. Specifically the RP11 trial single 75 microgram dose readout is expected next month.

What is the PYC ASX announcement this morning all about?

In relation to their clinical trials for the first drug candidate for the blinding eye disease Retinitis Pigmentosa Type 11, the key aspect of their announcement is: “Four cohorts of patients have now been dosed with this drug candidate in a Single Ascending Dose (SAD) study with no evidence of Treatment Emergent Serious Adverse Events in any patient at 4-weeks of follow up post-dosing.”

What does this mean?

Like the announcement says at the 4 week follow up for all patients there was no observed safety concerns. This is particularly significant for the highest single dose of 75 micrograms of drug per eye. This is good news.

Just why is it important?

Because it is only at the higher doses does there appear to be any efficacy. This is evidenced by the May 2024 report where one of the three patients with a single dose of 30 micrograms per eye showed an improvement. The earlier lower dosages showed no observable improvement. (This improvement was in a younger patient, so no doubt PYC will use this information to design further trials skewed towards younger patients).

So with no observed safety concerns for the higher dose it is a great confidence booster for the Clinicians and the whole program.

Really, just what is the big deal?

Well, this is not the big deal. But rather a positive step in the direction of what could be a big deal. PYC is now free to go ahead with multiple low and HIGH dose rates. You want to see the full force of the drug brought to bear on the condition. This is the green light to do just that.

So what should investors be looking for in the coming months?

You want to see one or more positive results with the 75 micrograms per eye single dose trial. In addition as the Ascending Dose Trial results come through you would be looking for positive results here. It would be a huge validation if any of the results came through positive, however if at the low dosage rates utilising multiple doses there was observed efficacy that would be even better.

So should I buy PYC?

That is a stupid question. How can I answer that. I don’t know your circumstances.

Maybe the best way to look at is only put in as much as you can afford to lose. Because you could easily lose the lot.

PYC announced today their fourth drug candidate for Phelan McDermid Syndrome (PMS): “..... has been able to restore the missing SHANK3 protein that causes PMS in neurons derived from a PMS patient.”

PMS being the same genetic condition NEU is going after with their NNZ2591 molecule. The approaches are very different with PYC using a RNA drug.

PYC have been able to grow the neurons from an affected and two unaffected individuals in the lab, apply the PYC drug and have had a positive response.

This is of course a positive however a very early step in the development of this drug. Essentially what was observed was the positive results for the “organ in a dish” trial as we have seen for the 3 other drugs they have under development.

However what will cause investors to take notice, is if PYC have further success in their dose escalation clinical trials for their most advanced drug for the treatment of Retinitis Pigmentosa type 11. This represents the frontier of testing of their suite of drugs in humans. We will find out between now and Christmas.

Excellent interview Andrew. A relaxed interview subject is always the best subject.

Background

PYC has three RNA drugs and their associated carrier peptides for treatment of orphan genetic conditions they are proving up. They are:

i) Retinitis Pigmentosa RP11. Drug

VP-001. Est $1b annual market.

ii) Autosomal Dominant Optic Atrophy

(ADOA). Drug PYC-001. Est $2b annual market.

iii) Autosomal Dominant Polycystic Kidney Disease (ADPKD). Drug PYC-003.

Est $10b annual market.

Interview

Rohan Hockings (RH) indicated the company completely re-focused in 2018 to RNA drug and delivery development. What we have now is the product of 4 – 5 years of work coming to fruition over the next 18 months.

RH said there were two parts to the technology, the active RNA drug and the delivery agent the Cell Penetrating Peptides (CPP).

Early “naked RNA drugs” are low effectiveness because they are poor at entering target cells. That is where CPP come in.

RH indicated PYC are focused on orphan genetic diseases. These are broadly defined as where there is less than 200,000 suffers in the USA. He indicated the financial incentives for going after these conditions were highly favourable.

In addition RH indicated the 3 conditions they were developing drugs for all were mutations on a single gene or monogenetic targeting drugs. This he indicated was important because drug developers know exactly what it is they need to target. He also initiated drugs of this type had success rates in clinical trials 5 times that of other types of drugs. RH quoted US company research indicated post lab trials, there was a 64% chance of successful market entry on these single gene condition drugs.

He also indicated no regulator need for a Ph 3 trial, since there was no existing standard of care.

RH talked about why they are so confident in their science. That is principally around Japanese technology developed around 10 years ago that permits say a skin sample to be turned into stem cells, then into a specific body organ cells like retinal cells. So you can grow a human retina and test the drug on the lab retina. As a consequence, RH describes the Phase 2 risk being largely removed in the preclinical setting.

RH gave some interesting background on RNA science, and to think about it like this:

DNA makes RNA and RNA makes protein.

CRISPR technology acts on DNA to fix a strand that has a “spelling error”. This represents a one-off change to the patient DNA to rectify a genetic defect. These molecules are large and difficult to get into the cell. Think about like the architect on a building construction.

RNA therapies – act on RNA and are smaller molecules than Crispr drugs. This is what PYC is targeting. The drugs need to be repeat dosed, since there is no permanent cell changes. Think of them like the Builder on a construction site. RNA therapies are particularly useful at addressing autosomal dominant conditions like PYC is targeting.

Changes to Proteins in the Cell – is like the construction site subcontractor – actually doing something.

How does PYC know to focus on a specific area?

RH said, if trying to catch all the rabbits then will end up catching none. They had a Strategic Review process : Where can they get RNA drug to do something impactful. They settled on the above 3 conditions.

The mutations they are attempting to treat only appear in one gene. This is called autosomal dominant diseases. It is where RNA therapies are best applied, and PYC have the CPP technology to get enough of the drug into the cells

Path to Market?

Commercialisation expected in RP11 in 2027 and revenue in 2028.

In 24-26 they hope to do a RP11 registration study

Clinical proof of concept they are working on now. This is the hard part Ph 1 and Ph2 . When complete will sit down with regulator on registration trial.

Will you be manufacturing the drugs?

Rare diseases do not need Big Phara for sales and distribution. Can sell an approved drug through specialist clinicians.

At some point further down the development path if successful, they expect to have buy offers from a larger companies.

Financial Situation

This year had a capital raise of $75m and PYC will shortly have $120m cash inclusive of tax rebates.

RH: “Our market cap does not stack up. We have better than 50/50 chance and if successful will tap a $1b recurring revenue and 95% margin”. Comparable US companies have a market cap of $5b.

Management concern is PYC is undervalued. Makes PYC think about out-licensing since the ASX market does not recognise the value.

What is special about PYC technology?

RHs response was interesting: “Nothing”.

PYC utilises a proven and approved class of drugs utilising existing RNA technology. PYC apply this in the right context plus PYC have solved the problem of getting more drug into the target cells.

Competitors RNA Kidney disease drug

Regulus a US company listed on the NASDQ are more advanced than PYC. RH said exciting data has been recently released – that being missing proteins are shown turning up in the urine of patients. Also Regulus are showing kidneys shrinking in size. All positive and similar to PYC.

However Regulas have trouble around market skepticism in the class of molecule they are using. This is because the FDA has never approved a small RNA modifying molecule like the one they are using. This is because there may be an impact on other body functions. And there is the risk the treatment might be longer term carcinogenic.

In the second half of the year, what readouts would you like to see?

RH: “3 or more patients showing improved visual function before Xmas would make me very happy”

They have seen this recently with one patient, however need to see this with 3 or more patients “for people to take notice”.

If PYC see this, then they will be gearing up for a registrational study in the middle of next year.

Professor Sue Fletcher remains on the Scientific Advisory Board.

Prof Fletcher developed RNA drugs for muscular dystrophy that are FDA approved and now in use. Serepta a US company that developed these drugs went from m/cap of $100m to $20b. RH points out this company is now working on improved peptide cell delivery technology similar to PYC is using that will increase efficacy by around 10 times.

CEO Worries

i) Access to capital on fair terms.

Alternative path to finance. Preference at the current market cap would be to licence one of the more mature drugs.

ii) Organisational transition - next year PYC will be running 10 concurrent clinical trials. This will stress the organisation and require increased resources.

People in the Organisation

RH: Shree is chief of R&D in the Los Angels office – a key role. Shree came from a big company and has built a great team.

Recently PYC put incentives in place for key staff.

Legacy of Phycologica (PYC listed precursor) Failures

RH: Definitely baggage in Australia, some fund managers will not talk to PYC. In first few years there was nothing to show, but easier now since PYC now have some results. However it is international and overseas companies that are important who are/will take notice of “globally differentiated science”.

Chair and 30% owner Alan Tribe

RH described as Alan as having a clear vision. PYC would not have survived without his funding.

“Is about to happen”. 3 assets about to go into clinical trials with a 60 – 70% success rate around monogenetic diseases of this type.

RH spoke about the potential annual profit of these drugs being multiples of the current market cap.

“We go 24/7”.

San Francisco Office

RH referred to the value chain split. Lab and clinical expertise largely in Australia. FDA regulatory expertise in the US.

Phelan McDermid Syndrome (PMS)

PYC has a PMS program. RH outlined why PYC’s approach is more comprehensive than NEU since it is disease modifying and gets to the root of the problem. NEU’s approach addresses a neural pathways, which is only part of the issue.

In 18 months where should PYC be?

RH: By 2028 hope to cash flow positive

In 24/25 - 3 clinical proof of concepts to be running

The big one: Kidney disease drug, in the first half next year are intending to get efficacy read outs.

For RP11 registration trial will start in the middle of 2025.

If PYC gets safety profile and initial efficacy readouts, then there will be a step change in the value of the company.

Anything else investors should be aware of?

Visual functional improvement we are now seeing with RP11. We know from the monkey trial we can get the drug to the back of the eye. And now know can safely administer in humans.

We know from "human retina in a dish" trials we can completely rescue the disease. The images of the improvement tell the story. So it all should work.

The underlying root cause of the condition is addressed. If you can move the needle in the clinic then the commercial opportunity will take care of itself. Comparable drugs have been shown to reach 80% of peak sales within 18 months

Scoonie Summary

As a new investor to PYC, you are potentially about to reap in the next 18 months the benefit of 4 years of hard work. Add into the 10 years of failure prior to the recent re-focus. RH is a very engaged and enthusiastic CEO. It all comes down to your confidence in the science and management.

Announcement this morning:

PYC today announces the receipt of Orphan Drug Designation (ODD) from the US Food and Drug Administration (FDA) for this drug candidate (known as PYC-001) for the treatment of OPA1-associated vision loss. ODD is given to drug candidates designed to treat rare diseases. Benefits of an ODD include tax credits for qualified clinical trials, exemptions from some regulatory fees and the potential for 7 years of market exclusivity post approval

This announcement, whilst not unexpected is another step in the right direction and talks to the ability of PYC management to execute.

By way of background PYC has three RNA drugs and their associated carrier peptides for treatment of genetic conditions they are busy proving up. They are:

i) Retinitis Pigmentosa RP11. Drug VP-001. Est $1b annual market.

ii) Autosomal Dominant Optic Atrophy (ADOA). Drug PYC-001. Est $2b annual market.

iii) Autosomal Dominant Polycystic Kidney Disease (ADPKD). Drug PYC-003. Est $10b annual market.

What will drive the share price, either up or down is further clinical and pre-clinical readouts for all of the above drugs expected between now and the end of the calendar year.

What is it Scoonie? Make it quick I’ve got a lot of work to get through today.

I have been looking at an ASX listed biotech, based out of Perth Western Australia called PYC. Market cap $460m (post capital rasie @ 8 cents, currently selling at around 10 cents).

Have you now. Last week you were telling me about a bauxite miner, now a biotech. You know what Scoonie, I think you might be a little bit Schizo. A…little…bit… Schizo.

These days its probably best not to say things like that. You know, mental health being such a sensitive subject and all that.

You might trigger someone.

Don’t tell me what I can and can’t say!!! And, don’t give me any of that touch-feely bulls%#t!

Anyway what the hell would you know about biotechs!

True, but you don’t have to be a chemistry Phd. Just have to take the time to think things through. And look many of the companies that people think they know about they don’t. Who really knows what goes on at the almighty Macquarie or any insurance company? You’ve got no idea really, your just believing what everyone else is telling you. Anyway, this is not about me. Its about PYC and whether they represent a company worth investing in.

Eh. Why are you wasting my time with this.

Because there could be opportunity.

PYC’s business is RNA therapy focused on orphan designated genetic diseases. As we have seen with NEU these have a lower regulatory hurdle, making them easier to get to market. And once in market the drugs can command very high prices.

What is gene therapy you ask? “ Gene therapy is a medical technology that aims to produce a therapeutic effect through the manipulation of gene expression or altering the biological properties of living cells.”

Its hard to believe, but science is able to use a vector such as a virus or special molecule to enter cells and fix a genetic defect. Closer to home, CSL have done this with their FDA approved Hemgenix used for the treatment of adult haemophilia. Essentially they have used a virus to travel to the liver and deliver a functioning gene that allows the patient to produce the missing blood clotting factor. Costs around $US3.5m for the one off treatment. Just incredible, worlds most expensive drug.

Roughly, this is what PYC is about. They currently have most advanced programs up and running, the fourth Phelan-McDermid Syndrome is less advanced:

i) Rare eye disease retinitis pigmentosa RP11, a genetic condition for which there is no treatment that results in progressive blindness. Targeting this condition is their drug VP-001. Around 5,000 – 7,000 patient population. (est $1b annual market)

ii) The second program is for a genetic optical disorder called autosomal dominant optic atrophy (ADOA) for which there is no treatment available. Targeting this condition is their drug PYC-001. Prevalence is around 9,000 to 16,000 suffers in the western world. (est $2b annual market)

iii) Autosomal dominant polycystic kidney disease (ADPKD) is marked by extreme swelling of the kidneys. Currently there is no treatment available other than kidney transplant. Targeting this condition is their drug PYC-003. Prevalence is about 160,000 patients in the US. This is the largest commercial opportunity (est $10b annual market)

iv) Phelan-McDermid Syndrome (PMS). Is on the backburner due to the regulatory obligations in enrolling the required child recruits. And yep, the same condition Neuron (NEU) is currently working on. NEU having released their very impressive topline phase 2 results back in December.

What makes PYC special is cell penetrating peptides (CPP) that are better able to get the active RNA drug that produces the change, to penetrate into the cell. As you can be readily figured, there is no point in producing the therapeutic molecule if you can’t deliver it to where it is needed.

As said by CEO Dr Hockings: “To further explain the science, people have a copy for each gene on the two arms of a chromosome, but with the genetic disorders being targeted there’s a mutation in one of the copies that inhibits protein production.

We are increasing the gene expression to compensate for the unstable protein, by making two units of the protein from the good copy of the gene. ….. industry is starting to understand that using RNA therapies to increase gene expression is a really smart thing to do”.

What’s their history?

The guys at PYC, or more correctly their predecessors have been ruining investor’s Christmas holiday plans since 2005. They first listed as a company called Phylogica and have only ever produced disappointment. All their promising tie ups with the likes of Medimmune, Roche/Genentech Johnson & Johnson, Pfizer and Astrazeneca all turned to mud.

They are head quartered in Perth and have an office in San Francisco.

Since about 2019, they have completely refocused with a board renewal and new management. The re-focus includes using the in-house expertise to firstly identify and target retinal genetic orphan conditions. There are 3 drugs under active development over the next 18 months with Ph1, Ph2 and Ph3 trials planned.

What’s the blokes running it like?

The CEO and ED is Dr Rohan Hockings. He’s about 40 years of age MBBS (honours) and spent 4 years working for McKinsey. You have to be pretty cluey to be the CEO of a ASX listed company (usually, but not always), but you want to see a video of him talking about PYC. He’s pretty sharp. For all his science training, there is also the element of the promoter about him. Which is needed.

How much of it does Hockings own?

He doesn’t show up with any shareholding in the 2023 annual report. However there is a note that states: “ Subsequent to 30 June 2023, Dr Hockings received shareholder approval to participate in a placement for 18,181,818 shares at price of $0.055 which were issued on 14 July 2023”.

Unusually the 2023 AR states “Dr R Hockings’ cash salary and fees are paid under a contractor arrangement”. So he doesn’t work for PYC directly. He was paid $395k last year. His father Bernard, a Perth cardio owns about 4.4%.

A fellow by the name of Alan Tribe owns 33%, so he effectively controls it. Seems as though he made his money out of property and sold his WA Ikea franchise 7 years ago. Looks like a big part of his net worth is sitting in PYC. IKEA Australia buys out WA, SA franchisee

In the April Capital raise Alan Tribe took up his full entitlement in the amount of $24m.

Alan, Rohan and his father might all be drinking mates for all I know. It’s Perth, so there is probably an in-crowd there you and I will never be a part of. That’s OK, as long as they are relatively honest. They do appear to be people who have worked hard for what they have and are not spivs who are about to run off with the petty cash tin.

The other two board members are Dr Rosenblatt, a US based academic, being at one point Dean of Tufts University School of Medicine. Mr Haddock is also US based and a finance person who has spent 20 years working in and around biotech companies.

So PYC could be an ASX outlier where maybe outside of Alan tribe who is there because he pretty much owns it, directors were chosen on the basis of competence. You know, people who know what they are doing and are able to get the job done.

With only 4 on the board, there is also room to build out the board if they need to.

Dorothy Dixer Bing Videos

Nov 2023 AGM presentation Bing Videos

NRW presentation April 24 Bing Videos

Have they enough cash?

They raised $75m at 8 cents in April. With the money they already had and a tax rebate coming up they will have a little over $100m. They claim this will keep them going for the next 18 months. There are enough milestones in that period if they are successful they can likely secure further funding. What they end up doing will no doubt depend on the major shareholder Mr Tribe. If successful or partially successful there are plenty of options: sell out, licence some of their technology, joint venture or raise more cash and go it alone.

What’s the competition like?

Hard to know really. I do know about a NASDAQ listed company called Regulus Therapeutics that uses RNA technology similar to PYC and is working on ADPKD, the kidney disease. Which is the biggest market PYC is chasing .

Last month Regulus had a Ph1b readout, link below.

A rough summary of the results in their words was: "We are pleased with the data we have seen in the second cohort, in particular, the mechanistic dose response, as it continues to validate RGLS8429's potential efficacy in ADPKD".

The shares jumped from $1.50 to around $2.80 in the days post the above release and are now around $2.00. Its market cap is only around US$132m.

On the same day they announced the above they announced: “Oversubscribed US$100 Million Private Placement of Equity”

So the market while not convinced as evidenced by the market cap and the share price change, evidently thinks there is some validity in what they are trying to do. God knows who else is out there doing this stuff.

Anything else?

On Tuesday PYC announced the successful safety results on their Non-Human Primates (monkey) trials with ADOA. This means the path is cleared a regulatory submission to enable human trials to commence.

On April 24 they completed dose range finding studies for its Polycystic Kidney Disease (ADPKD) drug candidate in monkeys. It was positive in safety and high concentrations of the drug found were in the kidneys. This has led the way for human trials for which data will be available in 2025.

Today PYC announced: “The dosing of the fourth cohort of RP11 patients within this Single Ascending Dose (SAD) study has now been completed.” Which I agree is a bit like the mining company saying they now have a drill rig on site. Like I said there is a bit of the promoter about these guys – which is good and bad.

Anything Else?

You see these little ASX biotech’s talk about getting TGA approval. Means either they have not got the funds to go to the US and never will and/or their science is weak. PYC is squarely focused on 3 drugs and FDA approval. In part that is the rationale for the US office. This is a positive.

I think you’re piss weak on the scientific analysis Scoonie. You haven’t put in the work.

Well I am not pretending to know all the scientific ins and outs of it all. However below is some higher-level summary stuff you can have a think about.

Mr Hoskins talks about having created “humanised models”. That is, they have taken skin sample of affected patients turned them back to a stem cell then turn them forward into the retina cells to create “retina in a dish”. From experimenting on these human samples, they claim to know the drug works.

With the kidney trials PYC directly took the impacted organ from a transplant patient and were able to test the drug on real affected tissue samples. Which lends the theoretical science some credence.

In addition in their announcement of the 22/4/24 with respect to the monkey dosage trials: “high concentrations of the drug present in the kidney highlighting the impact of PYC’s proprietary drug delivery technology”. That’s really important, the carrier or “cell penetrating peptide” is taking the drug to where it needs to go.

Similarly they have reported in the RP11 retinal trials on monkey subject, it is safe and high concentrations of the drug were found in the retina.

The other point is the 3 drugs are all different. They are independent. Failure of one trial does not impact the other two.

In addition they have selected genetic conditions where 50% of what you want is already beign expressed by the cell. In other words they have not made it overly hard for them to achieve the outcomes they want

And there is plenty happening. By the end of this calendar year VP-001 should be in or preparing for a PH3 trial, PYC-001 close to completion of Ph1 and the PTC-003 the kidney drug about to go into human studies. Over the next 2 years there will be Ph 1/2 human safety and efficacy readout in all 3 of the above trials.

In some ways the conceptual complexity around what they are doing may be a plus. It may keep some investors away. Contrast with PAA. They have a cannabis derived drug for Motor Neurone Disease. Well everyone can relate to that, gets the market real excited. What Aussie doesn’t like pulling cones on a Sunday afternoon and everyone knows someone with MND. Nice and simple. Even I get it.

Another factor in PYC having a low profile maybe they are headquartered in Perth. Everyone knows WA’s central station for shonky small caps.

What the downside?

Well that is clearly that some or all of the 3 drugs (4 if you include the PMS drug) fall over at some point.

Hoskins indicates the key risk as he sees it, is getting enough of the drug into the right location in the patient without any deleterious side effects. The results of the monkey kidney safety and dosage trial released on the 22/2/24 are very positive on this. Same with the RP11 trial. They are important leading indicators the drug might work.

Another relevant issue is any readout from the retinal programs is going to take some time, might not know for certain if the two drugs are any good until 2027. This is because the therapy does not reverse already existing sight deterioration. The only way to measure the efficacy of the drug is by measuring a lesser deterioration (hopefully) in the patient’s eye sight over time. So it’s a subtle measure.

In the case of the kidney drug, there are markers in the urine that are helpful in relatively quickly identifying if the drug is working. Also the FDA has indicated a reduction in size of the bloated kidney will be considered an endpoint. This can be easily measured through imaging. So the kidney drug development will likely move faster than the two retina drugs.

Also it is not a gift, you are paying $460m for an early stage development company.

Nearly half a billion and they are still on the laboratory bench!

RP11 is in dose escalation trials in humans - but you’re right it is not cheap for where it is at. However I would counter, there are strong lead indications that all 3 drugs might work. And the upside is huge.

Well there is risk/return trade off everywhere. Look at NEU and CU6. You could buy them even at these levels and both could easily 2x from here. But equally there are risks. For instance even for the market’s white haired boy NEU, if they cannot get their new drug NNZ 2591 up you could easy see the share price halve. Something like PYC, given its early stage and the orphan indications it is chasing, could 5x or more. The 3 lead drugs they are working on have to date only got stronger over time.

Think you know bloody everything don’t you?

Not at all. Look there is also an element of psychology to it. It’s a bit like Neuren. John Pilcher battled away for years and everyone who invested lost money and got worn down. Shareholders were all cranky and pissed. But as it turns out, the gold brick was sitting in the long grass just three steps away. You can see rough parallels with PYC in the April cap raise. They only got $13m from their retail shareholders leaving a shortfall of $21m which they had to place elsewhere.

There must be a 100 biotech wanabes on the ASX, all with a good tale to tell. You know what you are Scoonie? You’re a dreamer. Just a bloody dreamer. Not only that, you’re a f&%^*# idiot as well.

I am not asking you tear out and buy. I just think it’s interesting.

Just in case your in any doubt, I still think you are a f&%^*# idiot. Thanks for nothing Scoonie.

Post a valuation or endorse another member's valuation.