16th Sep 2018: I've posted a few straws here about Sandfire (SFR). I sold them when they did their 4th quarter production report and conference call, which I listened in on live. I thought there was a good chance of analysts downgrading them based on the tone of the questions and responses that Karl gave. That did occur, and the price subsequently dropped a couple of dollars over the next couple of weeks. I've since bought back into Sandfire.

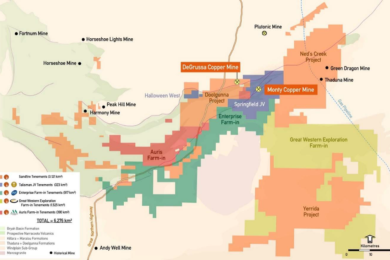

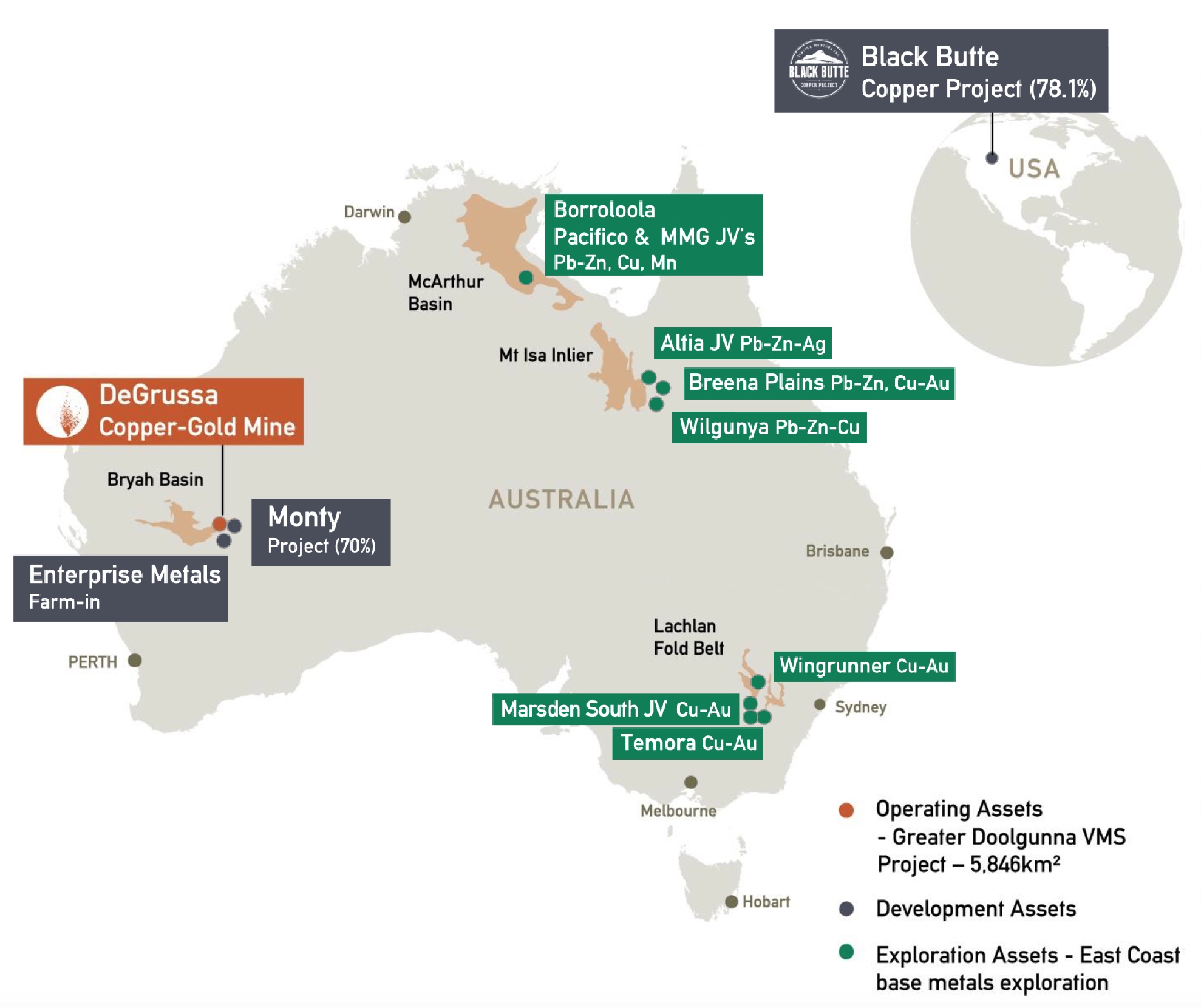

There are concerns about their mine life at DeGrussa. They need to find more commercial deposits close to DeGrussa to keep the processing plant operating. They have already achieved this with the Monty deposit, which sits 10 kilometres east of DeGrussa. They are in the process of buying TLM's 30% share of that deposit, which will leave SFR with 100% of that area in addition to their other extensive landholdings. Sandfire are also currently exploring areas to the south of DeGrussa and Monty via JVs with AUR, FEL, ENT & GTE.

They have a high grade deposit in Montana (Black Butte) ready to go, and are progressing the permitting and expect to break ground over there early in calendar 2019.

They also have further exploration assets within Australia:

Karl Simich has also flagged that they are evaluating various other overseas opportunities. He views DeGrussa as the launch pad for Sandfire and expects they will be bigger and better long after DeGrussa has been mined out. Pleasingly, the company has a big pile of cash and no debt and, as Pmonkey has mentioned, Karl is a high quality manager. He can seem a little aggressive at times - and can get annoyed with analysts on conference calls, but he knows his stuff when it comes to managing a copper producer!

The recent copper price falls & the associated negative sentiment towards copper miners generally - & Sandfire more specifically - seems more like a good opportunity to pick SFR shares up at much cheaper levels, or to top up, than to bail out of the stock.

Trump is playing a dangerous game with China, but he is getting pushback from within his own administration now, and it would not be in China's best interests to escalate this either seeing as they export much more to the US than they import from them. A trade war does hurt China more than the US, but it could also stall global growth and will hurt stock markets, and Trump has publically linked his own success as POTUS with the success of the US market, so he doesn't want to crash it.

I hold SFR.

Tuesday 31st July 2018:

"Dr. Copper" is generally regarded as a historically reliable leading indicator of global growth - which means copper companies like Sandfire might be a good way to go if you're bullish on global growth continuing, and probably best to avoid if you're expecting an imminent global recession.

Here's the most recent view from S&P:

http://www.miningnews.net/research/news/1342130/s-p-boosts-outlook-for-nickel-copper

Remember that S&P don't always get things right (such as their AAA ratings on dodgy CDOs prior to the GFC)...

Listening to the SFR 4th Qtr results conference call, I can see why the market may have got a little jittery about SFR. On top of trade war fears, the copper price in US$ have been falling recently, SFR is guiding for around the same level of copper production in FY19 as what they achieved in FY18 - but at ~10% higher costs due to having to transport the Monty ore 10km to the DeGrussa plant as well as the lower grades from Monty that will have to be processed before they get to the higher grade ore. While copper production in FY20 is expected to be around 20% higher, with lower costs (as they process a lot more of the higher grade ore from Monty), we have to get through FY19 first. SFR's 78% owned Black Butte (pronouced "Beaut") project in the USA could take longer than expected to get permitted - they don't expect to be breaking ground there until January at the earliest. And SFR's CEO/MD Karl Simich has a little bit of empire-building about him. While SFR do need to grow to remain relevant, and achieve economies of scale, it could be worrying some analysts that he sees a lot of that future growth being in various other countries - rather than here in Australia, and he was clearly prepared to invest in deposits (such as Black Butte) that are clearly inferior to DeGrussa.

http://webcasting.boardroom.media/broadcast/5b2aeea449e38c1023dbd10f

Finally, Karl was keen to squash the false rumour that SFR had a capital raising brewing. He stressed 3 times that while Sandfire America (which our SFR own 78% of) would continue to raise capital, mostly via rights issues to fund development, which SFR would participate in, there were NO plans for our ASX-listed SFR to raise capital. They have plenty of cash - and no net debt.

Disclosure: I often hold SFR, but I'm currently not holding. I'll likely buy back in when the copper price starts rising again.

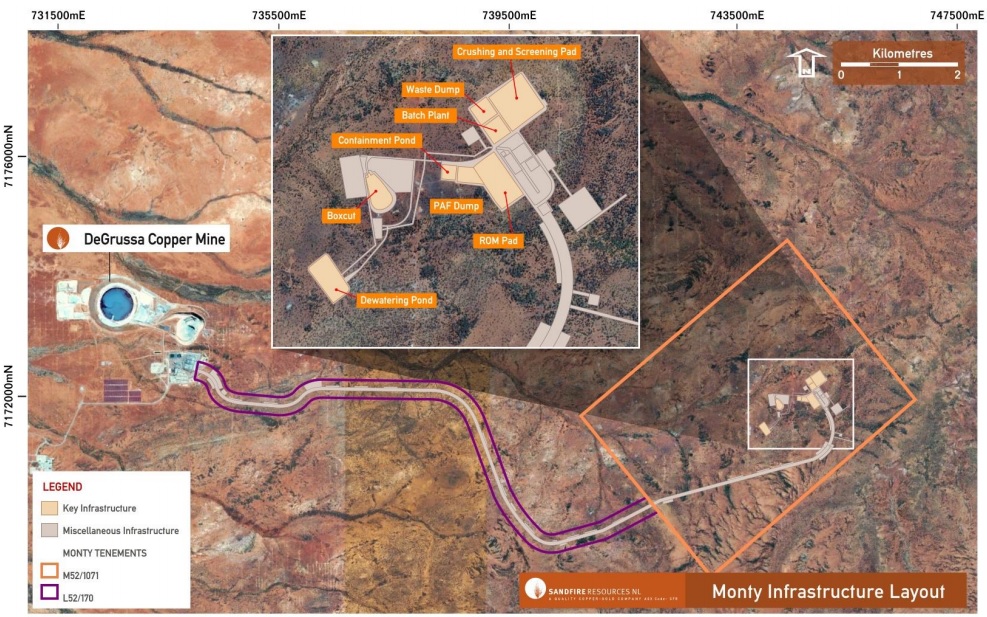

DeGrussa open pit and processing plant.