Consensus community valuation

Smartgroup shares were up over 7% during the day, possibly driven by the latest EV sales data and confirmation the FBT discount on salary packaged EVs will continue in full until March 2027 before being gradually scaled back.

According to an article in the AFR, about one in six cars sold in April were fully electric models. https://www.afr.com/policy/energy-and-climate/diesel-ute-sales-fall-off-a-cliff-as-fuel-prices-bite-20260505-p5ztwb

This will be a strong tailwind for Smartgroup over the next twelve months.

I’ve shared a few paragraphs from the AFR article below:

“FCAI chief executive Tony Weber said the changes were driven in part by generous federal government tax breaks for electric vehicle purchases, which will continue in full until March next year before being gradually scaled back.”

“The [tax break] has provided important stimulus to the market, and its continuation will support the growth of EVs,” Weber said.

“The policy, which exempts drivers from fringe benefits tax if they buy an EV worth less than $91,387 via a novated lease, can save a vehicle owner tens of thousands of dollars over several years but has been criticised by tax experts for disproportionately favouring wealthier drivers.”

“Under changes announced on Tuesday, the government will modestly decrease the tax breaks for vehicles priced above $75,000 from March next year, before scaling it back more significantly in 2029.”

04/05/2026

Smartgroup shares have risen sharply lately, from $7.37 on 23rd March to $9.29 today (up 26%). Given there has been no further company announcements following the FY2025 results on 26th February, I put this down to higher earnings expectations due to the spike in EV sales as a result of the higher oil prices. I’m expecting FY2026 NPAT of approx $85 million (64 cps), which is in-line with analyst consensus. At a mid-range PE of 15, that puts Smartgroup on a valuation of $9.60 per share.

Using McNiven’s Valuation formula and assuming equity of $2.04 per share, future ROE of 31.4% ($0.64/$2.04), 33% of earnings reinvested into growth, fully franked dividends, and requiring a 12% annual return, I get a valuation of $9.50.

Potential Risks

Salary packaging policies including the EV fringe benefits tax discount have been flagged for review by the Australian Government. I anticipate EV salary packages will drop if the discount is discontinued. This year the higher fuel prices and policy uncertainty are likely to increase demand for EV salary packages due to the FOMO effect, however the risk going forward is high.

Due to this policy uncertainty I will start reducing our holdings over $9.50 per share. Meanwhile, I’m happy to hold and collect the 6% fully franked dividend.

Held IRL (7.7%)

26/02/2026

See also my straw on CY2025 Results.

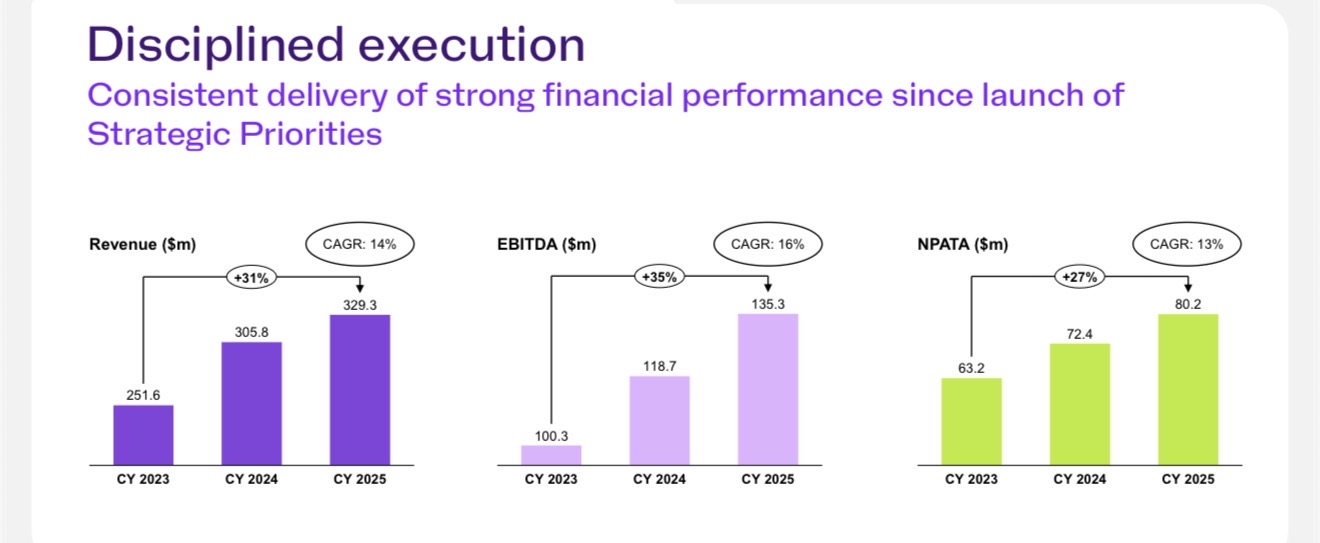

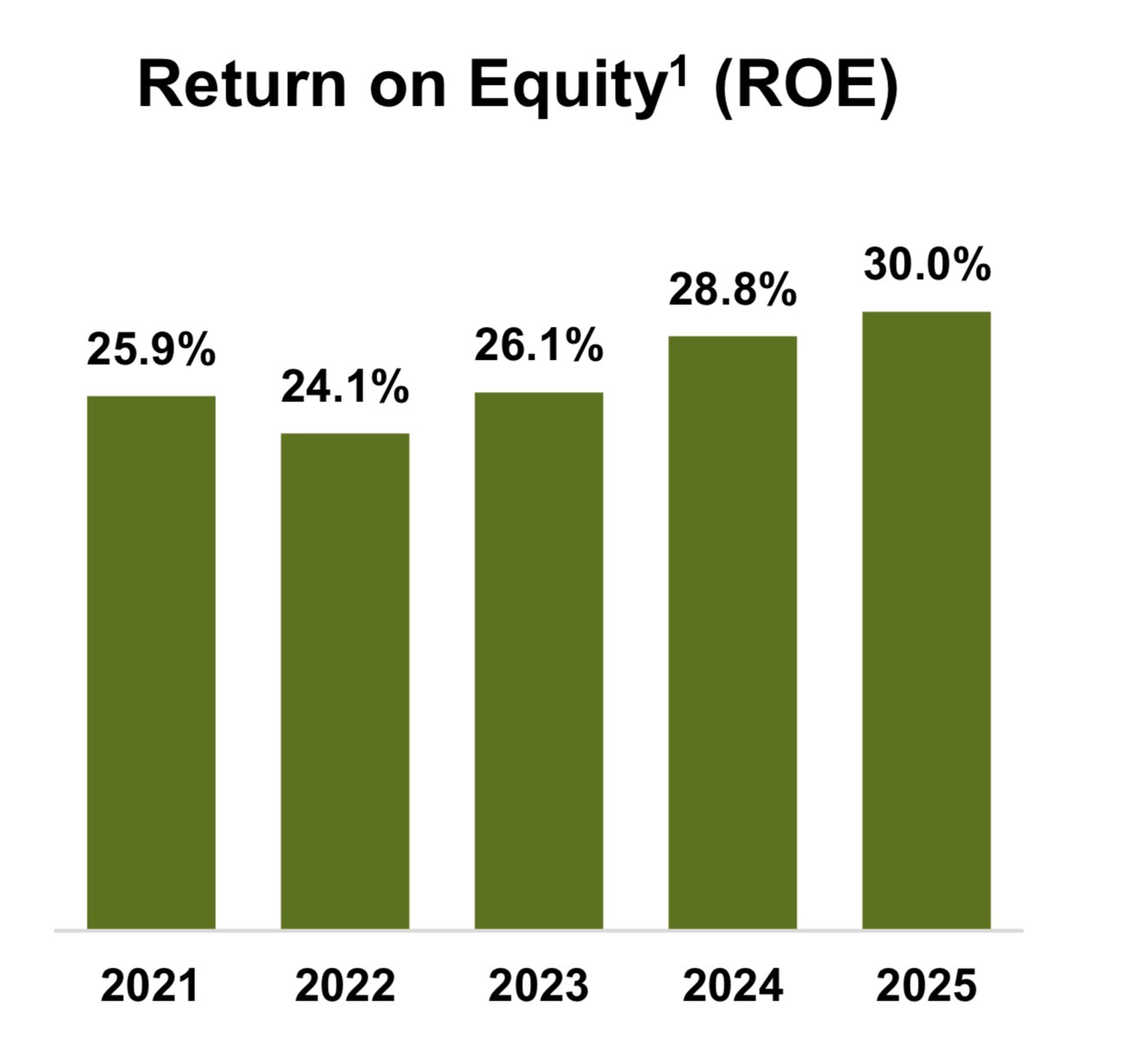

Revenue was $329.3 million up 8% on CY2024. Statutory NPAT was $79.4 million up 5% on CY2024. ROE improved to 30%.

Going forward CEO Scott Wharton said “we see a supportive environment for further growth. Demand for our products and services is robust, supported by our marketing efforts and a large and growing client base employing around 2.5 million eligible employees. Our focus is on deepening our relationships with existing clients, broadening our benefits offering and continuing to grow novated leasing, across both EV and ICE vehicles.

“We are executing our Strategic Priorities with discipline as we continue building a more scalable and digital business, simplifying brands and systems, modernising our technology, and embedding automation and AI to enhance how we serve customers. With these initiatives progressing well, and based on current market conditions, we are targeting EBITDA margins in the mid‑40s range during 2027.

“Our capital‑light model, strong cash generation and measured investment in digital and data, position Smartgroup well to deliver sustained profitable growth and create long-term value for shareholders over the medium term.”

Valuation

I am expecting c. $83 million (63 cps) for CY2026 (5% growth). Working on PE valuation, Smartgroup has traded on a PE between 11 and 20 over the last 5 years. Assuming a PE of 15x that puts Smartgroup on a valuation of $9.45.

Using McNiven’s formula assuming current equity of $2.04 per share, ROE of 31% (based on forward CY2026 EPS of 63cps), 20% of earnings reinvested, and requiring ROI of 11.5%, I get a valuation of $9.18.

Im going to round off my valuation to $9.00 per share, up from my previous valuation of $8.50. I would consider adding under $8.00 per share (13% ROI) and taking some profits over $11.00 per share (10% ROI).

Held IRL (7.7%)

28/11/2025

My valuation is only up slightly on last year. See my post “On a Roll”. Fair value at $8.50. A buy below $7.50. Reduce above $9, depending on FY2025 results and the chart trend.

08/11/2024

See also my straw “A Smart Dividend Stick?”

Over the last four years SIQ has traded on a PE multiple between 11 and 22. It’s currently trading on PE of just over 14 times analyst FY24 consensus (forecast 54 cps, FY December 24). The average 1 year price target is $9.50. This year SIQ has traded between $7.55 and $10.97. It seems to be reasonable value based on the PE multiple and analyst PT forecasts.

Using McNiven’s Formula and assuming forward ROE of 26%, 35% of earnings reinvested, 65% of earnings paid out as dividends (6.2% fully franked) and a required return of 11%, I get a valuation of $7.80. Using a required return of 10% the valuation jumps to $9.00. I’m going to go in between with a valuation of $8.40 down from my previous valuation of $9.00.

Held IRL (3.7%)

10/01/2023

My previous valuation of $8 per share from six months ago needs revising.

Over the past six months the outlook for Smart Group (SIQ) has vastly improved.

Contract Win

On the 11 December 2023 SIQ announced that the South Australian Government appointed the SIQ subsidiary, Smartsalary, as its exclusive administrator of salary packaging services and novated leasing services under an initial 5-year agreement (10 years including extensions). The contract was previously held by McMillan Shakespeare (MMS). Given the mid-2024 contract start date and typical novated leasing sales cycles, SIQ does not expect a meaningful earnings uplift from this contract in 2024. However this will boost SIQs earnings from 2025 to 2030, and possibly to 2035 if the contract is extended.

EV Tailwinds

For the 5 years prior to FY2023, earnings growth was relatively flat. The novated leasing businesses struggled during COVID due to the delayed delivery of new vehicles. This is turning around as new vehicle deliveries normalise. In addition, EV novated leases have escalated due to the Government’s carbon emission targets, EV rebates, fuel prices and a pent up demand for vehicles. During 1H23 EVs made up 30% of all new novated leases and this trend is likely to continue boosting SIQ’s earnings for some time to come.

Source: SIQ 1H23 Results Presentation

Analysts (a consensus of 7 analysts, Simply Wall Street data) are forecasting over 10% earnings growth over the next 3 years, and I think this is feasible.

Share Buy Back

SIQ has continued buying back shares since 6th March 2023. The number of shares to be bought back represents only 1.3% of the total outstanding shares. Share buybacks are not always a good use of capital, however SIQ was well undervalued at the start of the buy back (c. $6 per share) and the business ROE was high and is improving. Based on analyst forecasts the current ROE of 24% should lift to more than 30% over the next 3 years.

Source: Commsec

ASX 200 inclusion

On the 1st December SIQ was added to the ASX 200 list. This doesn’t change the fundamentals or valuation of the business, however, it can give a boost to the share price as more institutions include SIQ in their portfolios.

Valuation

Analysts are forecasting FY23 earnings of 48cps up from 45cps in FY22 (consensus of 3 analysts on Simply Wall Street).

If SIQ continues to grow earning at 10% per year over the next 3 years earnings could be over 60cps in 2026 (Forward PE of 15).

SIQs average PE ratio over the last 5 years has been approx 18x. At the current share price of $9, that puts the SIQ on a forecast FY23 PE of close to 19x. I think this is reasonable given the forecast 10% earnings growth.

Using McNiven’s formula which estimates future owners annual return by considering forecast normalised ROE as the internal rate of return (IRR), the percentage of reinvested earnings, the current equity value, and dividends paid to shareholders (including franking credits), I get a forward annual return to shareholders of c. 11%. For businesses with variable earnings I would prefer a higher required return (closer to 15%).

I think SIQ is fairly valued at $9 per share, and given SIQs business model relies heavily on favourable government salary sacrificing policies, I would be reluctant to pay a high premium for the business.

Unlike McMillan Shakespeare, SIQs balance sheet looks good with a net debt to equity of c. 17%.

I think SIQ is a great business with high ROE and yields a 4% fully franked dividend (at a 70% payout ratio). However, given its vulnerability to government salary sacrificing taxation policies I would be reluctant to add more SIQ at the current share price. I am a happy holder at the current share price.

Held IRL (4%)

July 2023

See my Straw “Back to growth” for justification. At $8 Smart Group should return investors c. 10% per year including franking credits.

Smartgroup reported a pleasing CY2025 result this morning. Revenue and Statutory NPAT both slightly up on consensus. A surprise special dividend of 12cps in addition to the ordinary dividend of 21.5 cps (both fully franked) which put a smile on my face! Smartgroup will pay out 53 cps in fully franked dividends for CY2025. That’s a 9% gross yield on yesterday's closing share price of $8.30. The dividends are supported by a strong cash flow of $97.5 million, 122% of NAPTA and up 25% on CY2024. ROE at 30% continues to improve.

CY 2025 Highlights

- Revenue of $329.3m, up 8% on 2024 (pcp)

- Operating expenses of $182.7m, up 5% on pcp

- Operating EBITDA of $135.3m, up 14% on pcp; EBITDA margin at 41%, up 2ppt on pcp

- NPATA1 of $80.2m, up 11% on pcp, Statutory NPAT of $79.4m, up 5% on pcp

- Novated leasing settlements 7% increase on pcp

- Battery Electric Vehicles (BEV) accounted for 40% of 2025 new car lease orders, while plug-in-hybrid EVs (PHEV) and Internal Combustion Engine (ICE) vehicles accounted for 8% and 52% respectively

- BEV and ICE new car lease orders increased 49% and 4% respectively compared to pcp

- Continued strong Return on Equity (ROE) of 30% after tax, up 1ppt on pcp

- Strong and flexible balance sheet with low net debt position at 0.3x EBITDA2

- Final ordinary dividend declared of 21.5 cents per share (cps) and special dividend declared of 12 cps, both fully franked3

- total dividends declared in CY 2025 represent 90% of CY 2025 NPATA

Outlook

Commenting on Smartgroup’s outlook, Managing Director and CEO, Scott Wharton, said: “Lookingahead, we see a supportive environment for further growth. Demand for our products and services is robust, supported by our marketing efforts and a large and growing client base employing around 2.5 million eligible employees. Our focus is on deepening our relationships with existing clients, broadening our benefits offering and continuing to grow novated leasing, across both EV and ICE vehicles.

“We are executing our Strategic Priorities with discipline as we continue building a more scalable and digital business, simplifying brands and systems, modernising our technology, and embedding automation and AI to enhance how we serve customers. With these initiatives progressing well, and based on current market conditions, we are targeting EBITDA margins in the mid‑40s range during 2027.

“Our capital‑light model, strong cash generation and measured investment in digital and data, position Smartgroup well to deliver sustained profitable growth and create long-term value for shareholders over the medium term.”

Held IRL (7.3%)

Disc: Held IRL (8%)

The Smartgroup share price has been on a roll recently. I’m not sure what’s behind it? There’s been no new announcements or news to explain it! There could be number of reasons. Here are a few speculations:

Hybrid car sales have taken a leap lately. There were concerns the drop in hybrid cars sales following the withdrawal of the government rebate might impact Smartgroup’s salary packaging business. It looks like this has washed through and hybrid sales are now stronger than ever.

Political - Greens support for Environmental Policies.

Political - Greens support for Environmental Policies.

Government policy is always a threat to Smartgroup’s salary packaging business model. With Labour getting support from the Greens on environmental policies, the threat to “Net Zero” has been put off for a while. Withdrawal of rebates on new EVs is a risk to revenue.

Dividend Approaching

Smartgroup has a track record of paying a high dividends, forecast to be close to 6% fully franked for FY25 (8.5% yield). For high dividend payers the share price usually runs up ahead of the dividend, and falls when the shares go ex-dividend.

Technical Run?

I’m primarily a fundamental investor. However, when shares are going up they keep going up! When they get locked into a downward trend they keep going down! It sounds silly but it’s a real phenomena. It doesn't make sense, but I’ve learnt it’s not wise to ignore the charts either! It just makes the journey longer and more painful if you do. Mind you, I’m a slow learner!

Howard’s Buy Call?

Howard Coleman said he bought Smartgroup himself on “the Call” recently, under $8. A bit of tongue in cheek really, but who knows? I do have a lot of respect for Howard’s investment thought process.

Nothing Conclusive

There are a few things I think could be behind the rally. It pays a good fully franked dividend and has done well for me. If you pick it up less than $7.50, I think you can do OK with its current performance. I think it’s fair value is $8.50 but I wouldn’t pay that for it (It should return about 11% per year at $8.50, according to McNiven’s Formula. It has excellent RoE of around 30%, but only high single digit growth). Over $9.00 and I would start reducing, depending on the FY2025 results and the charts of course. Don’t ignore them!

Smartgroup has been bouncing off a $7.60 support level for a while now. Each time it goes there I’ve added more shares. I can’t work out why it’s trading down here? There’s been nothing but good news for this business, its revenue and earnings are growing, it has a 30% ROE, moderate debt, it could yield close to 10% including the franking credits in FY24 and FY25 (after reinvesting 35% back into the business) and it’s directors have been adding shares over the last 12 months. The final dividend I expect will be over 30cps, fully franked, and is due in March. Smartgroup will announce its FY24 results on 26 Feb at 9.00am AEST. So, if there are any disappointments I won’t need to wait long.

Smartgroup has been bouncing off a $7.60 support level for a while now. Each time it goes there I’ve added more shares. I can’t work out why it’s trading down here? There’s been nothing but good news for this business, its revenue and earnings are growing, it has a 30% ROE, moderate debt, it could yield close to 10% including the franking credits in FY24 and FY25 (after reinvesting 35% back into the business) and it’s directors have been adding shares over the last 12 months. The final dividend I expect will be over 30cps, fully franked, and is due in March. Smartgroup will announce its FY24 results on 26 Feb at 9.00am AEST. So, if there are any disappointments I won’t need to wait long.

A few days ago it won the Monash 3 + 2 year salary packaging contract (no contribution to 1H2025 earnings). It’s smart technology seems to be ahead of its competitors, and it is gaining business at its competitors expense (eg. McMillan Shakespeare MMS).

Bell likes the business and has a $10 PT on it (see previous straw). I’m not that enthusiastic, but I think the current share price is significantly under fair value.

One thing that could impact Smartgroup’s earnings is EV sales. They have peaked and have declined lately. However hybrid sales are increasing! Hopefully they have a finger in this salary packaging pie also.

Anyway, we will know the result and a better idea of the outlook in 15 days time. Fingers crossed!

Held IRL 6.4% by weight

If you’re looking for a cash cow for your portfolio I don’t think SmartGroup (SIQ) is the dumbest idea out there at the moment. Most stocks are looking quite expensive IMO. However SIQ is trading near 12 month lows at around $7.70. This might be due to electric cars sales coming off the boil a little. It might have something to do with Trump’s lack of enthusiasm for renewables? Perhaps the market is worried about a change of government in Australia and the policy for renewables here?

In any case I think SIQ looks like good buying at the current price and I’ve been topping up around $7.60 per share. It makes up 3.7% of our portfolio and the dividends have been handy at over 6% fully franked (over 8.5% gross yield). Due to strong free cash flows I expect the business will continue paying out good dividends above 6% fully franked over the next few years. Analyst consensus is for earnings to grow at over 6% per year with a future ROE close to 30%. That’s quite feasible given they have grown earnings over the past decade and ROE has been c. 20% to 25%.

Source: Commsec

What does SmartGroup do?

SIQ “provides outsourced employee benefits and administration services, being primarily salary packaging, novated leasing, fleet management, payroll administration and workforce optimisation services to employees of State and Federal Government departments, Public Benevolent Institutes and corporate employers Corporation Ltd (SIQ) provides outsourced employee benefits and administration services, being primarily salary packaging, novated leasing, fleet management, payroll administration and workforce optimisation services to employees of State and Federal Government departments, Public Benevolent Institutes and corporate employers” (CommSec).

My daughter used SmartGroup to salary package a new Tesla recently and they are receiving some nice tax savings.

Key Risks

SIQ is price sensitive to government policy for salary packaging and the market gets nervous around election time. This is one of the key risks for businesses like McMillan Shakespeare (MMS), SG Fleet (SGF) and SIQ. Although MMS pays an even higher dividend (c. 9% fully franked) and also looks cheap, I am frightened off by their balance sheet (over 300% net debt on equity). SIQ is more conservatively geared with only 23% net debt on equity.

Valuation

Over the last four years SIQ has traded on a PE multiple between 11 and 22. It’s currently trading on PE of just over 14 times analyst FY24 consensus (forecast 54 cps, FY December 24). The average 1 year price target is $9.50. This year SIQ has traded between $7.55 and $10.97. It seems to be reasonable value based on the PE multiple and analyst PT forecasts.

Using McNiven’s Formula and assuming forward ROE of 26%, 35% of earnings reinvested, 65% of earnings paid out as dividends (6.2% fully franked) and a required return of 11%, I get a valuation of $7.80. Using a required return of 10% the valuation jumps to $9.00. I’m going to go in between with a valuation of $8.40 down from my previous valuation of $9.00.

Held IRL (3.7%)

Today SmartGroup (SIQ) released its FY22 results. The market is ecstatic! The share price was up 8% at the time of writing. I must admit I’m pleased to see the share price up too with Smartgroup making up 3% of my portfolio IRL.

The market is excited because Smartgroup just declared a fully franked dividend (ordinary + special) of 29 cps for 2H, bringing the total FY22 dividend to 46 cps. That is a whopping 7.7% fully franked dividend, or 11% grossed up yield for the year based on a share price of $6.

Not bad you say? The problem is, that is all you are likely to get. Your total return. It’s still not bad and I’m certainly not complaining about it. There was certainly an opportunity to add some additional share growth after Smartgroup announced the loss of the contract with Department of Education and Training Victoria in October 2022 when it traded as low as $4.62. A big risk though back then!

Remarkably the business has managed to offset this loss with salary packaging growth from new and existing clients, bringing revenues back to FY21, plus 1%. If they can do this, perhaps they can win more new customers going forward.

The dividends are sustainable because of the NPATA of $61 million, which was slightly ahead of guidance. That’s about 46.9 cps. The problem is Smartgroup will pay out 98% of this as dividends. That’s what I call a CASH COW!

Whats wrong with that? The internal rate of return for Smartgroup is 23% (ROE). This has been steady for about 8 years. Over this period Smartgroup have also paid out almost their entire earnings as dividends, and surprise, surprise the earnings haven’t grown in 5 years.

Source: Commsec

What is this saying about the business? While the ROE is very good, the business can’t find opportunities to reinvest earnings for growth. If it could, it would. It tells me the market it operates in is almost saturated.

There are also risks in the industry. If the federal government rolled back on tax benefits through salary sacrificing, this would knock the wind out of the sails for the likes of Smartgroup, McMillan Shakespeare and SG Fleet.

I’m going to continue holding Smartgroup though. They have been concentrating on building smarts into the salary sacrificing platform, and when the vehicle supply chain starts to improve, there might be an opportunity for further growth in the future. I’m hoping they will start to win customers with a smarter, more user friendly platform.

The outgoing Smartgroup CEO Tim Looi said “Our business has proven to be resilient and has maintained steady operational performance despite the challenging economic environment and the ongoing supply chain disruption for new vehicles.”

“With vehicle orders continuing to exceed settlements, the company is well positioned to benefit upon the easing of new vehicle supply constraints. When this occurs we will realise the excess new vehicle order pipeline of c.$15 million as well as reduce the operating costs associated with maintaining this excess pipeline. Together with the introduction of the Federal Government Electric Car Discount Policy and the associated growth in electric vehicle leasing, Smartgroup is well placed for future growth”

Valuation

Using McNiven’s StockVal formula and assuming forward ROE of 23%, 98% of earnings paid out as dividends, 100% franking, and a required return of 15%, I get a valuation of $4.90. If you were happy with a 12% required return you could pay up to $6.16 which is about where it is trading today. For me it is a hold at the current price. If it goes much higher I will consider reducing.

Disc: Held IRL (3%)

It looks like private equity might be back kicking tyres at SmartGroup again. Last year the SmartGroup Board knocked back a bid of $9.25 per share. Now it is trading at an absolute bargain price of $4.80. Big mistake!…HUGE! (my favourite quote from “Pretty Woman”). I will be definitely keeping an eye on the share price today.

Last night (9.35pm, 1 December, 2022) the AFR published an article titled “PE takes another look about Smartgroup, board the battle”. I’ve copied part of the article below:

The private equiteers are back out for salary packaging, novated leasing and fleet management play Smartgroup, assessing whether it would be possible to pounce after a poor year and snap up the business for less than $1 billion.

Only 13-months after Smartgroup’s brief and unsuccessful fling with a PE suitor, buyout shops and credit funds have re-opened their files to try to work out what’s gone wrong and how easy it could be to turn performance around.

This time US private equity firm TPG Capital’s understood to be on the sidelines, leaving it to its rivals to think about getting serious about Smartgroup and putting the company in play.

The biggest and likely untested question is at what levels Smartgroup’s board and shareholders would be willing to sell the company.

The board was happy to engage at $10.35 a share last year, but cut off talks with TPG and its bid partner Potentia Capital when it returned at $9.25 a few weeks later.

Disc: Held IRL

SmartGroup announced it has lost the DET Victoria contract this morning (see previous straw)

The market is punishing SmartGroup, down 10% at time of writing. Is this justified?

SmartGroup said the contract loss will not materially impact CY22 earnings, and the impact on CY23 would be less than 5%.

Also within the announcement “Smartgroup advises that it currently expects H1 2022 revenue and EBITDA to be in line with H1 2021”

This is more likely to be the reason why there is severe pressure on the share price today.

Looking at the earnings forecasts on Commsec, analysts were expecting CY22 earnings to be circa 54cps.

CY22 earnings were 47.2cps, and according to SmartGroup H1 2021 and H1 2022 are expected to be similar.

I expect H122 earnings are under some pressure due to the supply of cars for salary packaging, and it is unclear at this point if this will improve in H2.

Regardless, this does put pressure on SmartGroup to meet the analysts expectations of CY22 earnings of 54cps.

It will be interesting to value SmartGroup assuming flat CY22 earnings to see if the sell off is justified.

Lets assume CY22 earnings are 47cps (same as last year). Current shareholder equity is $2.05 per share. That gives us a forward ROE of 23%. Still very respectable.

Using McNiven’s StockVal formula and requiring a return of 10%, and assuming 80% of earnings will be reinvested to grow earnings:

V = (23/10 x 0.2 x 23% + 0.8 x 23%) /10 x $2.05

= $5.94

This valuation excludes dividend franking credits. 80% of SmartGroup’s earnings are paid out as earnings so the franking credits are substantial.

Making adjustments for franking credits, and assuming SmartGroup’s earnings will be flat this year I think $6.50 is fair value.

For me it’s a HOLD, and there could be some potential on the upside if SmartGroup win some new contracts.

Disc: Held IRL

Smart Group’s released its presentation Macquarie Australia Conference and business update this morning (to be presented today).

Smart Group is not a businesses that will shoot the lights out from one report to the next, however, since its IPO in 2014 it has returned investors >700%, including franking credits. I think it’s a steady consistent cash cow to have in your portfolio with high ROE (30%) and low debt/equity (10%). It has also been one of the few businesses whose share price has defied gravity over the past 3 months.

Business update to 30 April 2022

Salary packaging customers are up c.5,000 since 31 December 2021, +1% growth

Year to date novated leasing leads are up 6% versus the prior comparable period (pcp)

Excess vehicle order pipeline revenue now at c.$14 million, up from c.$12 million at 31 December 20211

Transition of novated funding from St George to Angle Auto Finance successfully completed and further automation within the existing funding panel also completed

Revenue and EBITDA in line with our expectations and pcp

Low net debt position of $47m and leverage of 0.5x EBITDA Smartgroup CEO Tim Looi said:

“We are pleased with the start to 2022. In the four months to 30 April 2022, Smartgroup has seen good growth in salary package numbers and achieved continued growth in novated leasing lead volumes.

Vehicle settlement timeframes continue to be extended due to ongoing global vehicle supply shortages. Consequently, our vehicle order pipeline has continued to grow and now represents an additional $14 million of future revenue, above pre-COVID levels. In terms of financial results, revenue and EBITDA are in line with our expectations and in line with the prior corresponding period.”

Outlook

Smartgroup CEO Tim Looi said: “We have made good progress so far in 2022 and look forward to building on our Smart Future program momentum, which is targeted to generate sustainable EBITDA growth through both revenue expansion and operational efficiencies.”

Disc: Held IRL

I’ve held Smart Group for a number of years. I think it is a quality business that pays an excellent dividend and more recently has been spewing cash!

I added substantially to my holding just prior to going ex-dividend on the 8th March 2022. Including the one-off special dividend SIQ paid out 49c fully franked, or 70c including the franking credits (100%). For the FY22 year SIQ paid out 66.5c fully franked, or 95c including credits. That’s equal to a grossed up yield of over 11% including the tax credits based on an $8.50 share price. Not a bad cash cow! :) But is it a dividend trap?

Smart Group (SIQ) provides outsourced administration, primarily salary packaging, software, distribution and group services (SDGS) and fleet management services to employees of State and Federal Government departments, Public Benevolent Institutes and corporate employers. SIQ operates mainly in three segments: Outsourced administration, Vehicle services and Software, distribution and group services (Commsec summary).

Smart Group has two main competitors, SG Fleet (SGF) and McMillan Shakespeare (MMS). All 3 companies have been growing by organic growth and acquisitions. I believe there is little opportunity of further acquisitions for Smart Group, and free cash flow and tax credits have been accumulating.

Fundamentals

Smart Group has more than doubled earnings in 6 years, and has averaged an ROE of approx 20% for several years (see CommSec graphs below).

Gross Margin is 61% and Net Profit Margin is 27% (Simply Wall Street).

Smart Group pays out 80% of its earnings in dividends and reinvests 20% back into the business. According to 6 Analyst Estimates (S&P Global) forecast earnings growth is 9.5% per year until 2024.

Valuation

Working on average forecast FY24 earnings of 61c and a PE of 17 (approx average over past 4 years) and discounting at 10% per year, I estimate the current valuation for Smart Group as:

v = 17 x .61 x 0.7 = $7.26

Now this doesn’t account for any dividends payments over the next 2.5 years. As a consistent dividend payer, we could expect approx 50c fully franked per year. If we also discount 2.5 years of grossed up future dividends at 10% this would be equal to 2.5 x 70c x 0.8 = $1.40. (70c Including tax credits).

Adding the two values we get approx $8.60 which is close to where Smart Group is currently trading. Therefore, at a current share price of $8.60 it is possible that Smart Group could return investors an average 10% per year until 2024. Smart Group is not going to shoot the lights out, but for me it’s a HOLD as a cash cow for the next few years. The current share price momentum is also looking good.

Key Risk

Government policy in regards to salary sacrificing and fringe benefits tax remains a key risk for SIQ, SGF and MMS. The values of these businesses could plummet if the employee tax benefits were scrapped, as has been threatened in the past.

History