Consensus community valuation

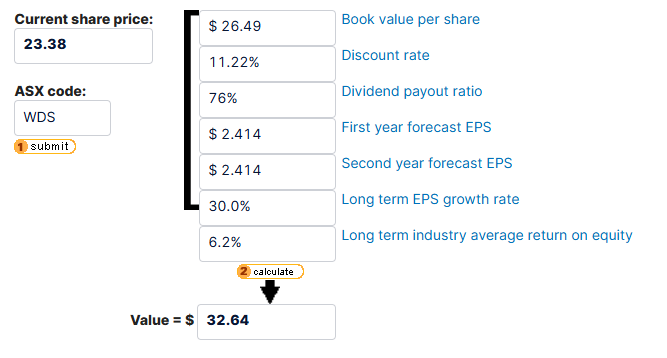

I'm reposting my valuation for WDS as it didn't seem to stick. I don't see any reason to change my valuation of $32.64, It is a lot closer to it now closing today at $30.42 than it was at $24.01 when I first posted. I also did another valuation with the @Strawman ' s tool which gave me $30.17. That valuation (WDS was $26.48 then) is right at the bottom of the notes. While I am still bullish on WDS and comfortable with my valuation, I have rebalanced today. With all the capital growth WDS had ballooned to over 37% of my RL portfolio. Having just gone ex-Div I was happy to rebalance, restock cash and be able to go on the hunt for another winner. Previous valuations are below:

A little case for why I think WDS is still a value proposition moving forward considering today’s release of full year 2024 results.

Record production achieved in 2024 with 193.9 MMboe, with more production coming online with Sangomar, Scarborough, Trion, and Louisiana LNG.

Net profit up 115% YOY despite a fall in realised oil and gas prices. Unit cost of production down by 2%.

Higher production and lower unit cost of production combined with the potential for higher prices gives pretty good potential upside.

The 53 US cent dividend is worth about 0.835 AUD at today’s exchange rate, bringing the total for the year to AUD$1.86, a 7.73 percent return at (the current price when writing of) $24.01 before franking credits. PE is sitting below 10 and WDS share price has been well above its current malaise for the last couple of years.

I’ve attached my CMC value calculation below. I reckon $32.64 is a pretty conservative value for this company. As recently as September 2023 its price was over $38 per share.

Disclosure: This is one of my biggest holdings in RL and on SM.

WDS valuation

I thought I'd do a little update on this valuation since I've finally had some time to watch @Strawman 's basic valuation video and started playing around a bit with WDS figures. So I started with a revenue increase of 4% per year for 3 years giving me $23.844 Billion multiplied by a 20% NET profit margin (average over the last 4 years is over 25%) giving me $4.768 Billion. 1.989 billion shares outstanding gives me $2.51 per share. (That figure is definitely realistic as it did over $3.40 per share in dividends in 2023).

So $2.51 x a PE of 16 gives a share price in 3 years of $40.16. Taking that backwards wanting 10% per year gives a share price for today of $30.17.

The 2024 financials provided $3.6 billion in Net profit after tax, and using the current exchange rate $2.87AUD per share of earnings. So $2.87 x a PE of 16 gives a current price for today of $45.92. At a PE of 12x you get $34.44 and at 10x $28.70 (obviously). All of those are comfortably above the current (at time of typing) share price of $26.48.

So there's my first stab at the 'rough and ready valuation'. I'm going to dig a bit deeper and play with the figures some more and do a more in depth analysis soon.

Thanks again @Strawman for the helpful video and the Excel tool. (Yet to try that, I was using the desktop calculator too).

WDS is my biggest holding IRL and on SM.

This morning I dialed into the Woodside call via the Quartr App (Quartr is amazing btw)!! Woodside is my 5th largest holding and one I look to for Dividends.. It's fair to say I came away grumpy with Management's presentation style.

I open the presentation also on Quartr and start scrolling.. The first financial numbers I want to see are the key financials, including dividends compared to last year. Funny enough with 24 companies in my portfolio, I don't walk around with last year's comparatives in my head. Slide 5 is the financials and it's anything but what I want to see.. it's the story they want to spin "Strong Results".

Interim CEO Liz Westcott announces we've had great results with "strong shareholder returns" with total full year dividends of US$112cps. But I can't remember what they paid me last year so why can't they just give me the entire picture in one slide...

I keep scrolling as Liz drones on with her sales gibberish, until I get to SLIDE THIRTY.. Where I can finally wrap my head around a bunch of Non-IFRS financial measures myself.. yet here I find the table of numbers we should be included in the bank of chart/table crimes.

Maybe it's just me, but my eyes scan the table and my first glance sees EBIT up 14%.. But wait.. When I read the table carefully I see the FY25 number is smaller than the FY24 number.. why is the 14% written as a positive number... oh.. these stupid ($%&'s have put a small grey down arrow indicated that the positive 14% number is actually a negative (14)%.

Turns out strong shareholder returns means lowering dividends (8)% from last year!!

If Interim Liz can't be honest and straight forward with Shareholders l hope she's not confirmed as full time CEO!

Cheers

JM

So I'm sure a lot of you here listen to The Motley Fool Podcast, and there was a section recently on 'crimes in charting' and the benefit of companies that report clearly.

Below is a snip from the investor presentation from WDS today:

Nice and clear. Production volume up - good, Unit Production Cost down - good, EBITDA up - good, NPAT down - bad, LNG reliability down - bad, Marketing EBIT contribution down - bad, Dividends down - bad (fiscally responsible?), Gearing up - high end of targeted range ok.

So here's my dilemma. My macro investing strategy, when I am deploying capital, has always been very simple:

Big liquid companies, P/E of as close to 10 as possible (below is amazing), Dividend before franking credits of greater than 6% and share price below 52 week highs.

There's a few other things that I look at but this is my starting point.

Now WDS, with its share price dropping as I type this is still comfortably within these metrics. I accumulated when it got sub $20.

Here's the rub though, WDS is my biggest holding already and I am wary of the old 'too many eggs in one basket'. I am still bullish on WDS as demonstrated by my last valuation, but I'm wondering if anyone here would like to put a case for why I shouldn't buy more WDS (other than the obvious, got too much already).

Talking about dodgy charting, back when I was doing M&E I provided a chart to the bosses with the improvement that had been achieved by a project. It accurately represented what had been achieved. The boss was very unhappy with the graph, saying it 'didn't show enough improvement'. I obviously wasn't going to fudge any figures, so I simply changed the scale of the graph. Visually much better, cue happy boss, but data was the same. Misleading optically, sure, but if you read the data, factually correct.