Consensus community valuation

November Update

- Profit Reserve - 55.4c - 5.2yrs of Dividends

Some familiar names in the top holdings

They say this was recorded on Tuesday July 20th, 2023, however the 20th was a Thursday. It was posted on Livewiremarkets.com on Friday (July 21st): https://www.livewiremarkets.com/wires/oscar-oberg-small-caps-are-primed-to-rally-and-it-doesn-t-happen-without-these-stocks

Oscar Oberg is the Lead Portfolio Manager (PM) of WAM Microcap (WMI), WAM Research (WAX), WAM Active (WAA) and WAM Capital (WAM), however his strength is in WAM Funds' Research-Based investments (WMI, WAX, & half of WAM) rather than the market-based, short-term-arbitrage-based strategy of WAA and the other half of WAM, which is demonstrated by WMI and WAX consistently outperforming WAA and WAM over recent years - since Oscar joined WAM Funds from his previous role at the Hong-Kong-based CLSA (he was at Grant Thornton before that).

In this Livewiremarkets.com "Rules of Investing" podcast episode, titled, "Small caps are primed to rally, and it doesn't happen without these stocks", Oscar covers off the following:

Timestamps:

0:00 - START

1:50 - When will small caps bottom?

4:30 - No small cap rally without consumer discretionary

6:30 - Profit taking

7:30 - Why large cap tech matters to small caps

10:14 - 30-40% rally is not out of the question

14:30 - Harvey Norman's (ASX: HVN) property backstop

16:00 - Wearing the volatility

17:00 - Industrials

20:20 - Going tactical

24:15 - Mermaid Marine

26:30 - Body language matters

27:30 - City Chic (ASX: CCX) was a mistake

29:20 - Managing liquidity in small caps

32:45 - Takeover target

34:50 - Balance sheets look good

36:55 - Going public too early

40:25 - The classifieds company for the bottom drawer

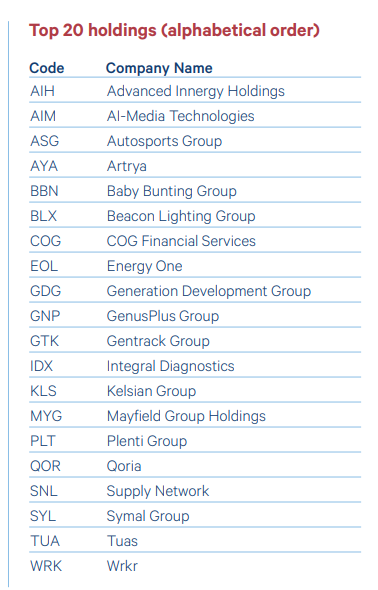

Here's a snapshot of his WAM Microcap LIC (WMI.asx) as at June 30th, 2023:

Their top 20 positions (in alphabetical order, not weighting order) are listed there in the bottom right corner of the slide.

Disclosure: I do not currently hold WMI or any other LIC managed by WAM Funds, nor do I hold any of those 20 companies in their "top 20" list above, however I have time for Oscar Oberg, and when I have spoken to him at WAM Roadshows in previous years, he always came across as knowledgeable and smart, without being cocky, and he often has some good insights into what is going on within various sectors. Many of his good ideas are too big (in terms of their market cap) for WMI (which only holds Microcaps), so may end up in WAX instead - here's how WAX looked at the end of June:

WAX is not constrained by the size of the companies, other than if they are large caps they are more likely to end up in WLE (WAM Leaders), so WAX holds mostly Small and Midcap companies, plus some microcaps. If you see companies in both WAX and WMI - such as CAJ, RIC, TPW and TUA currently - then it's safe to assume that Oscar has some serious conviction about them. Of those 20 in WAX, I hold PME here (but not currently IRL) and I hold TNE both here and IRL.

WAM Capital (WAM), which used to be their flagship fund, the OG if you will, holds all of the companies that the other funds hold, but usually in larger quantities, because it is a much larger fund. The exception is WLE (WAM Leaders) which is even larger at $1.85 billion. WAM is $1.7 billion. WMI = $305 million. WAX = $222 million. WAA is a tiny $52.5 million.

Here is what WAM held (top 20 positions) at the end of June:

You can often work out which companies are the larger positions in WAA, WAX and WMI by whether or not they also make it into WAM's top 20 list for the same month. Remember however that WAM is supposed to be 50/50 Research/Active, meaning that around half of their top 20 positions are market-based or arbitrage opportunities rather than based on fundamental research like the positions in WAX and WMI are. That is backed up if you look at the following slide (below) - of WAA (WAM Active) - and see how many of those positions are also in WAM's top 20 (above).

It's therefore safe to assume that Neuren (NEU), Life 360 (360), Bellevue Gold (BGL), Flight Centre (FLT), Fisher and Paykel (FPH), NextDC (NXT) and Worley (WOR) are all reasonably high conviction positions, and larger positions in WAA, because they are also top 20 positions in WAM (WAM Capital). And that companies like Codan (CDA), Megaport (MP1), Smartpay (SMP) and TPG Telecom (TPG) are smaller positions in WAA, because they do NOT feature in WAM Capital's (WAM's) top 20.

WAM Capital (WAM) also used to occasionally hold some large-cap positions that were also held within WLE (WAM Leaders) - see here:

However, only the highest conviction positions in WLE (which is a bigger fund than WAM) also make it into WAM's top 20, and in this instance there were no companies that were in the top 20 of both WAM and WLE, which may suggest that WAM Capital has gone back to ONLY holding Microcaps through to Mid-cap companies, and no large caps, which would make a lot of sense, because that's where they had all of their success in their early years. WLE is also a well-run fund - Matt Haupt is the lead PM of WLE, so different PM there - however I believe it's a different skill set that is required to be succesful in small and microcap investing compared to large cap investing. For one thing, you need to consider liquidity issues with smaller companies, something that Oscar touches on in this podcast, near the end.

Disclosure: From WLE's top 20, I also hold CSL, FMG and S32. From the top 20 lists of WAA and WAM, I also hold CDA and TNE, and I've been in and out of BGL (currently out). I also have NEU on my watchlist and I'm following them closely thanks to a lot of great content on them here on SM.

It is good to hear Oscar admitting that City Chic (CCX) was a mistake - as it's a company that they were very bullish on for a number of years and they also heavily promoted.

I also found his comments on Harvey Normal (HVN) and their property backing interesting, as well as his assertion that a rally of between 30% and 40% is "not out of the question".

By the way, I'm not suggesting anyone buy any of those LICs based on what they hold, coz there are other considerations. For instance, whether the LIC is trading at a premium or a discount to their NTA (aka NAV). In WMI's case, they ended June at $1.41, being a 8.3% premium to their before tax NTA (which was $1.30), and they've put on another 3.5 cents since then, closing at $1.445 on Friday. I'm not generally keen on buying a portfolio of shares (which is, at its heart, what a LIC is) for more than I could buy the same shares on-market unless there are other positive considerations that make the premium worth considering. I guess it's fair to say that some of the gaps (between share price and NTA) that some of Wilson's LICs have previously enjoyed have narrowed a little of late, but I still regard an 8.3% premium to be too high personally.

Further Details:

Another consideration is the fees they charge and whether they are attractive or excessive. See here: WAR - Risks (strawman.com) [Thank you @ArrowTrades for that gem!]