At a recent value investing conference, money manager Mohnish Pabrai, a self-described “shameless cloner” of Buffett and Munger, sat down for a fireside chat. In it, he shared wisdom that, while far from original, bears repeating.

Indeed, the fact that Pabrai’s wisdom is essentially repackaged lessons from Berkshire’s dynamic duo is precisely one of his key messages. In investing, while novel and unique ideas tend to be intellectually seductive, the smarter move is often to simply ride the coattails of proven investors. There are no extra points for degree of difficulty or originality; all that matters is finding and backing the very best ideas available.

That is actually a big part of our raison d’être here at Strawman. Surfacing top-tier investors and tracking their positions is an excellent way to discover investment ideas, as well as the rationale behind them.

Not that you should blindly copy and paste what others are doing. As I’m fond of saying, you can borrow an idea, but you can’t borrow the conviction. Different investing styles and strategies are suited to different temperaments, strengths, and goals. But, as Pabrai suggests, it is a wonderful way to zero in on new opportunities and effectively shortcut much of the discovery process.

“What I found is that if you are a shameless cloner like yours truly, it gives you a huge edge because there are so many things in the world that have already been done by great people… we benefit a lot by standing on the shoulders of giants.”

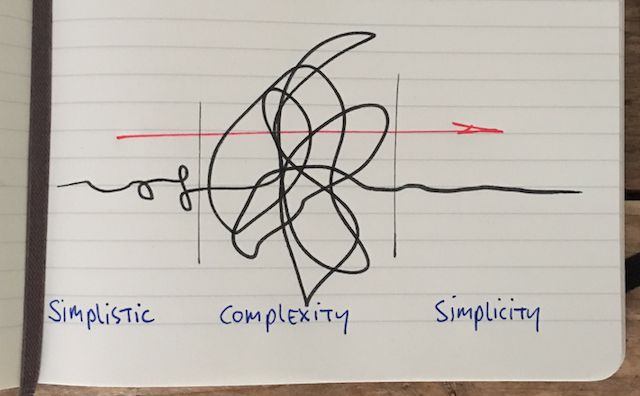

Another idea espoused in the interview was the importance of shunning unnecessary complexity. Echoing Munger, and many of the world’s great thinkers for that matter, Pabrai suggests that the highest form of intellect is actually simplicity.

The most dangerous trap for capital allocators who consider themselves reasonably savvy is the “seduction of the sophisticated,” which causes us to underestimate the tremendous weight of simple ideas. We ignore the obvious winning strategies because they feel too easy.

In fact, that is one of Buffett’s explanations as to why more money managers don’t try to emulate Berkshire’s investment process. Buying high-quality businesses at sensible prices and “sitting on your bum” is, for many people, too simple to be effective. Despite all the evidence to the contrary.

The next non-consensus view Pabrai emphasises is the importance of concentration, or, put another way, the danger of (over) diversification.

“The simple thing I didn’t understand is that if the job is done right, your portfolio is going to be 95% one stock.”

That quote seems more than a little reckless, but his point is that truly great businesses are extremely rare, and your capital is far too precious to waste on mediocrity. Moreover, he’s not saying you should ape all your money into one stock immediately. Rather, he implies that if you let your winners run, a highly concentrated portfolio is an inevitable end state. The poor performers, of which there will unavoidably be many, will dilute themselves, while the success of your best picks will lead to their inevitable concentration.

Ok, maybe a 95% weighting in one stock is stretching the concept a bit far. But the point remains. And it gets at another insight pressed by Pabrai: that the hardest work in investing is the ability to do absolutely nothing.

We must learn, Mohnish insists, to embrace the boredom of compounding. Adapting Pascal’s famous line, he states that investor misery comes from the inability to watch paint dry. This is something that professional money managers struggle with specifically due to a need to justify their existence through activity.

“We trade, we rotate, and we hedge when the most profitable action is often lethargy. True power in this business comes from the conviction to sit on your hands when you are right.”

Last, but certainly not least, was the emphasis on asymmetry, something which is at the very core of my own investing approach. Referencing his famous “Dhandho” principle, Pabrai says you want situations where it is “heads you win, tails you don’t lose too much.”

It’s just maths. You can watch most of your investments drop to zero and still do really well overall if you nab only a single 100-bagger. Provided, that is, you don’t continually fiddle with things along the way.

That asymmetry is not going to happen with Telstra, CBA, or other “blue chip” stocks. Not to call them out as bad investments, but only to say that the compromise you make for relative safety is very average returns. Which is fine, if not preferable, when your goal is capital preservation. But if your goal is material wealth accumulation, and you have a reasonable runway ahead of you, then it’s a good idea to swing for the fences.

Not, I hasten to add, in a reckless manner where you simply spray and pray over a variety of high-risk moonshots. That’s a great way to lose money. Rather, it means seeking out companies with a reasonable potential for significant and enduring growth, limited downside if they fall short, and for which there is at least some evidence that they are on the right path.

Narrative and hope alone won’t cut it.

Ultimately, the thread running through all of Pabrai’s philosophy is that successful investing is less about raw intelligence and more about character. It requires the humility to clone, the discipline to simplify, and the patience to wait for the right opportunities with meaningful upside, and to simply get the hell out of the way when you find them.

It’s all rather straightforward, at least in concept — although in practice, it is anything but. Still, these ideas serve as a valuable North Star. And when we inevitably stumble, take solace in the fact that, in Pabrai’s words:

“Mistakes are the best teachers. One does not learn from success. It is desirable to learn vicariously from other people’s failures, but it gets much more firmly seared in when they are your own.”

Strawman is Australia’s premier online investment club.

Members share research & recommendations on ASX-listed stocks by managing Virtual Portfolios and building Company Reports. By ranking content according to performance and community endorsement, Strawman provides accountable and peer-reviewed investment insights.

Disclaimer– Strawman is not a broker and you cannot purchase shares through the platform. All trades on Strawman use play money and are intended only as a tool to gain experience and have fun. No content on Strawman should be considered an inducement to buy or sell real world financial securities, and you should seek professional advice before making any investment decisions.

© 2025 Strawman Pty Ltd. All rights reserved.