Endo International plc to distribute Penthrox in Canada

- Release Date: 10/05/22 15:35

- Summary: MVP signs new Penthrox licensing agreement in Canada

- Price Sensitive: Yes

I thinking the share markets were bearish in May 2022..So MVP could get some momentum going forward..

Placement at $2 then a proposed Retail SPP

Passing the hat around!!

This is one that I got terribly wrong. I sold out at least a year ago for a big loss but glad I got out when I did.

They have a great product in Oz and should have been able to make it work internationally. Execution and capital management have been abysmal and it doesn't seem to be getting any better.

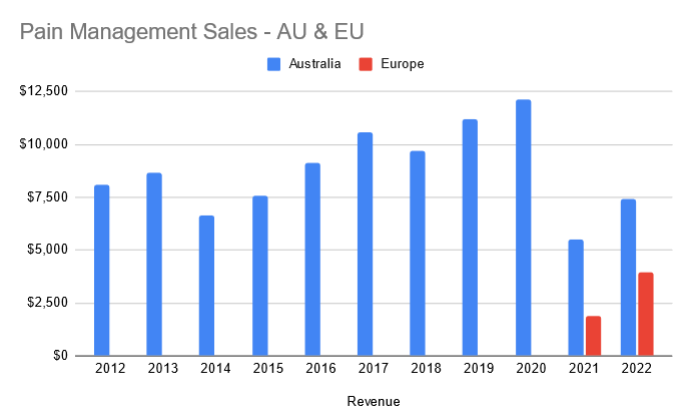

Another example of an Australia health company that cannot turn a great product into a viable business. So disappointing. This slide tells you all you need to know:

good luck to anyone still holding !

23 Half Year Results - Watch list

MVP announced it's half year results will be on Feb 24th. Thought I would do a straw on items I'll be looking out for in those results. All my watching is on the pain management side of the business (The Green Whistle) as I believe that is where the greatest opportunity lies (not in respiratory).

Progress to their strategic priorities in FY23

From the FY22 report, below are the strategic priorities for FY23

- Continue penetration of Penthrox in France

- Market entry planning for Germany, Italy & Spain

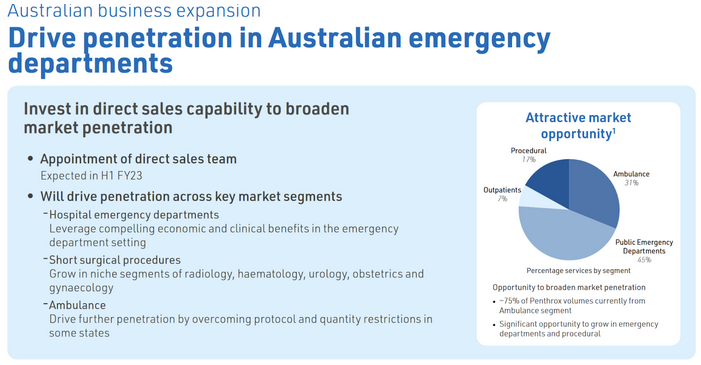

- Investment in direct in-market sales capability in Australia to drive penetration of Penthrox in hospital ED and the ambulance segment

- Further investment in platform capability to support growth

Continued penetration of Penthrox in France

France has a population size of roughly 65 million, as of FY22, MVP had 720 units sold per million population in France. This compares to 11,577 units per million population in Australia. There is considerable growth opportunity available, as part of this strategy management is expecting to sell circa 110k units in FY23, more than doubling FY22 sales (49k) but well short of the penetration of Australia.

Market entry planning for Germany, Italy & Spain

I’m not expecting too much here as the word “planning”. However there is opportunity for MVP in these markets. The population of these four is ~260 million, taking out France of ~65 million there leaves 195 million in the remaining 3 markets.

With Australia’s benchmark of 11,577 units per million population If these 3 markets get to that then that would be an extra 2.25 million units sold per year.

Direct in-market sales capability in Australia

MVP have now hired a direct sales team after taking the distribution rights back from Mundipharma in December 2020. I'll be watching to see how this translates to sales and turning around the recent decline in sales, two ways it might:

- Lock downs & Sell Through Over: The decline can be attributed to lock downs and Mundipharama selling through it's stock levels so hopefully they can get the levels back to FY20.

- Penetration in Emergency Departments: Secondly, MVP have said they want to target emergency departments. Currently the ambulance segment makes up around 75% of AU sales, roughly 223k units based on FY22 sales of 298k units. MVP believes the ambulance segment makes up roughly 31% of the market opportunity however there is 45% opportunity in Public ED departments.

Cash Burn

Cash burn, currently MVP has roughly 50m in cash. Management have expressed that they believe they will be cash flow positive in FY25 and the recent capital raise will get them to 2025 (with the options exercised). Study costs for the US trials will be around 12m.

China Exit

Lastly, my two cents on the recent decision to cease planned trials in China. I think this is a good idea to allow the company to focus on growth in existing markets. China is a very difficult market to get into with Medical Devices, not only is the registration time for foreign companies longer with the China FDA but China has a 2025 made in China vision (Article 104). Although I’m not certain article 104 would apply to MVP, if it does, manufacturing would have to be set up in the country which adds its own costs and risks.

23 Half Year Results - Results

MVP announced it's half year results last week, at a high level revenue up 45% to 13.9 and a net profit of 2,658. However this was only due to a refund from the termination of the China contract. Taking out that revenue and impairment net profit sits at -8,864 which is an 8% increase on the PCP.

Overall, mixed results. Not the growth required in the pain management and a surprise 80% growth in the respiratory business. After listening to their announcement below is my take on the good, bad and progress based on my watch list.

The good

- Increasing prices in December for Australia resulting in higher gross margins

- Gross profit margin increased to 71% from 67.9%

- 29% Growth in UK and Ireland with the current distributor even with a deferred shipment in UK. Revenue is only recognised when shipment is made so this will flow into the FY results.

- Positive feedback from all customers, CEO mentioned he has never heard a negative thing about the product

- Re-launched in Canada with a new partner

- 80% growth in respiratory and expected double digit growth in US moving forward

The bad

- 24% growth in France is well behind the > 50% they needed to achieve 110k units. Current run rate is at 60k units which is the same run rate presented for Jun-22 quarter. Effectively meaning no growth from June quarter.

- Negative growth in pain management units in Australia by 6k

- Expenses increased by 16% on PCP and 27% on the last half.

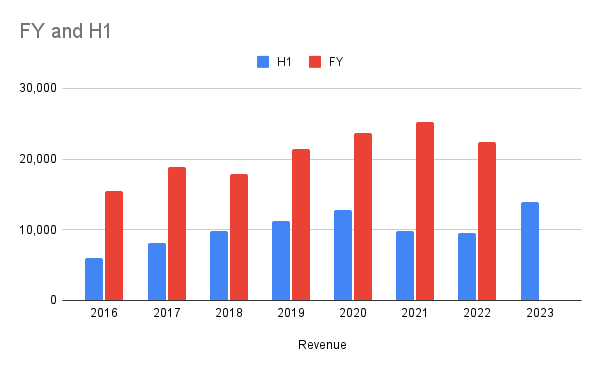

H1 / FY Total Revenue

Good growth in revenue, slightly beating H120

The split based on franchise

Continued penetration of Penthrox in France

At FY22, MVP were targeting ~110k units sold in France. Currently they are tracking on a run rate of 60k units. Well short of expectations.

Management have expressed multiple reasons which include

- Retaining / Recruiting: MVP uses a contract sales organisation in France. They are seeing issues retaining staff as they are going to companies which are offering permanent roles.

- Hospital Staff Shortages: Staff shortages in hospitals have made it harder to get the right decision makers on-board to add the green whistle to the hospital

- Bed Closures

- Budget Constraints

At a high level I get the sense that for pain management, they have to invest a lot of time in education. As this is a new product to majority of French hospitals there is effort in education to promote the benefits - ease of use and quick pain relief. I would imagine after time this education will reduce as this becomes the standard of care.

Market entry planning for Germany, Italy & Spain

Not much news on this apart from the next market they would target would be Germany sometime in FY24.

With the cash bleed at the moment, it does make sense to focus on growing and learning from France before spending more in entering another market.

Direct in-market sales capability in Australia

Slight decrease in Australia units sold in the pain management section. However promising that they have on-boarded 2 ED's in Australia since October. Interestingly the indication in Australia is wider than anywhere else in the world. Overall not much of an improvement here with the direct sales team so expecting more.

Cash Burn

MVP cash position is now 37m, free cash flow for this half was -11,604. Management still expect break-even / cash-flow positive in FY25.

For the US trials, they are currently assessing a funding plan. Currently the group has no planned capital investment activities and plans to seek partner or third party funding.