Pinned straw:

08-March-2025: A week ago (on Friday 28th, the last day of Feb) I wrote here about NWH's H1 report and commented that because it was released after market close, I would have to wait until Monday (March 3rd) to see the market's reaction to it - and it could be interesting. It was.

Here's what they looked like at market close yesterday (Friday 7th March 2025):

I would argue (and I am) that they've been oversold, unless there are reasons other than OneSteel and a less positive iron ore price outlook for the sell-off. Firstly, this is not unusual, however, despite repeated drawdowns (or pullbacks), their share price has been on a north east trajectory if you zoom out and look at a 10 year chart:

Here's that same 10 Year chart (below) using daily data points instead of the monthly data points used in the 10 Year chart above.

That second one is not as clean, but the results are the same: If you are prepared to ride out the share price volatitlity they do eventually make up lost ground and go on to make new highs, although sometimes it can take a while, like 4.5 years for them to get back up to their $3.38 high point achieved on 20th Jan 2020, which they passed again in July 2024.

However they are increasingly compensating us for waiting, through increasing fully franked dividends:

Source: All of these charts and tables were sourced from Commsec today and tidied up by me. I've changed the Dividend yield above: Commsec had 5.8%, however based on 16 cps p.a. (the 7c div just declared plus the last final dividend of 9 cps) and a $2.81 share price, it's 5.69%, not 5.80%. I have also added their grossed up dividend yield which includes the full value of the franking credits.

So you've got that income to compensate you for a choppy share price.

But what about the risks? Yeah, there are risks, as there are with any contractor, and especially contractors who are exposed to commodities and commodity price movements, however it pays to remember that NWH aren't miners, they are mining contractors who are awarded multi-year mining contracts (recurring revenue), so the real risk is if their clients cease production or go broke and that work ceases prematurely, or if the client doesn't pay their bills as they fall due.

And many punters probably think that's what has happened with OneSteel, one of NWH's clients, in the past few weeks, however it's not that simple. OneSteel was put into Administration by the SA Gov after they ran out of patience with the parent company not paying their bills, including $17 million owing to SA Water, plus not paying their contractors including NRW who it turns out are owed $113.3 million by OneSteel for past work performed.

NRW are continuing to work for the OneSteel Administrators and are being paid from the date of Administration, but are having to pursue the $113.3 million for work done prior to that. NRW say they are confident that they will be paid and they have NOT declared any impairments (write-downs) in their H1 accounts related to money owed to them by OneSteel/GFG.

OneSteel is part of the GFG corporate group and is the legal entity that owns and operates the Whyalla steelworks and associated mines. GFG is controlled by Sanjeev Gupta and rather than me describing the man and his business practises, it is probably more instructive to watch a 7:30 report piece from ABC TV broadcast on Feb 13: https://youtu.be/ETNzD2BddFE which is titled, "Gupta approved to develop mansion as Whyalla and Tahmoor face uncertainty". It's not just Gupta's SA operations that are in deep trouble. The South Australian Government recognised where this was heading and moved to bring it to a head before the Australian federal election is called next month (April 2025) and hopefully giving themselves enough time to find a buyer and new long-term owner of the assets before the SA State election in March 2026.

I would argue that this particular situation has more to do with Sanjeev Gupta than it has to do with iron ore and steel prices and their respective outlooks, even though those outlooks don't look stellar in the short to mid term. Gupta can't make money in coal either, and in other areas throughout his global empire - and he just doesn't seem to like paying his bills, and part of that appears to be that he has too many fingers in far too many pies and is struggling to keep all of the plates spinning, to mix up some metaphors.

But what is NRW's exposure to GFG and OneSteel? Well, one of the things I like about NRW is their much improved risk management since our last really big mining boom went bust - and NRW almost went broke themselves, with their SP getting down to around 4 cps in January 2016. Even I wasn't brave enough to be holding them at that point - I thought they would go broke, but they pulled through, and haven't approached debt in the same way since, and are proactive now in securing their rights in situations like the OneSteel debacle. Here is the timeline, impact and current status of that one from NRW's POV, taken from their H1 results presso on Feb 28th:

Note the third dot point in the timeline. Whyalla Ports is a multi-use port facility - not just used for steel exports - and NRW have first ranking security over all of the shares in Whyalla Ports and many of the Ports' key assets. Golding is a division of NRW by the way in case that wasn't clear.

Because of this and NRW working collaboratively with the OneSteel Admistrators (KordaMentha), I believe they'll get either all of their money or most of it, or else they'll end up with Whyalla Port assets they can sell to recoup some or most of that money owed to them. It's also worth noting that of NRW's major contracts, OneSteel (shown below as "SA Operations") is the one that was already scheduled to expire first, later this year, and their other Iron Ore mining contract (crushing and hauling) at Karara is due to expire next calendar year if not extended.

Which would leave NRW's commodity exposure (via mining contracts) to Gold (through EVN's Mungari gold mine) and Met Coal.

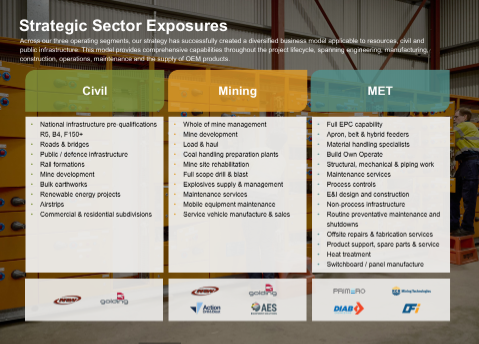

It should also be noted that while Mining remains NRW's largest division and the mining sector is also their largest sector exposure, NRW's Civil Revenue was up strongly (+40.6%) in H1 and MET (NRW's Minerals, Energy & Technologies division) was also up by +15.6%, and NRW's EBIT Margins improved in both Civil and MET, with EBIT improvements of +75.9% and +25.3% respectively, being greater in percentage terms than the corresponding increases in revenue for those two divisions.

On the one hand, the revenue generated by Civil and MET combined now exceeds the revenue generated by Mining, AND the profit margins on Civil and MET are improving, but on the other hand it's worth noting that the EBIT that Mining generated ($63.7 million) is still significantly higher than the combined EBIT from Civil and MET ($48.5m), so the margins are still clearly better within NRW's Mining division, despite that Mining division EBIT margin slipping this half compared to the p.c.p.

So it's a trade-off - they are achieving further diversification of revenue, which is positive when the commodities outlook is so mixed, but that diversification is into other sectors that have so far had lower profit margins than NRW have been achieving in their Mining division traditionally, albeit those other sectors are exhibiting improving margins while their profit margin in Mining is slipping, so all things considered I'm happy enough as a shareholder with this progression - and that trade-off.

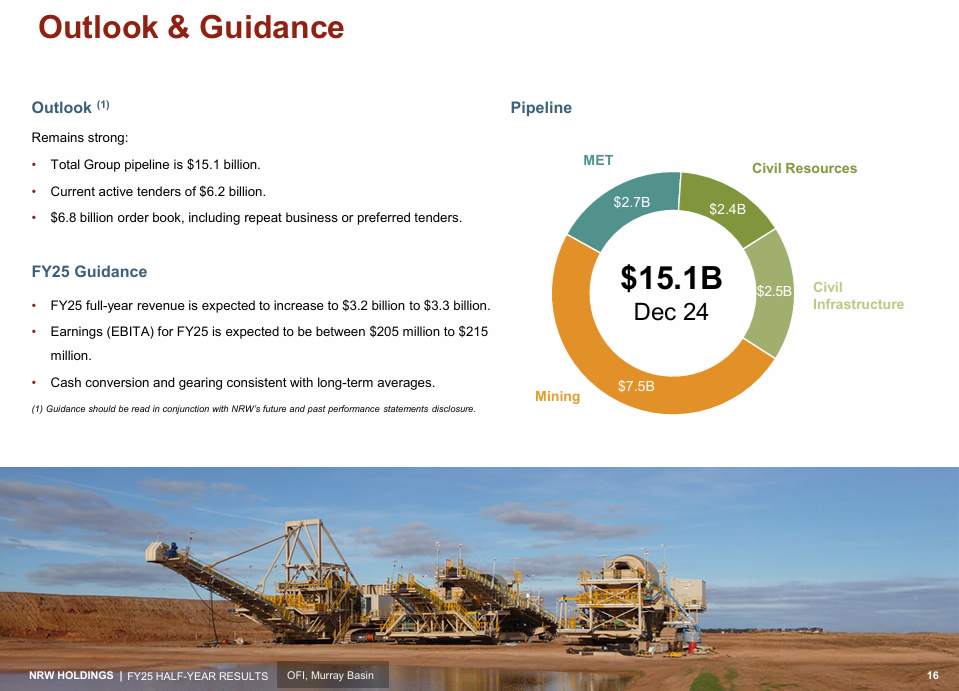

Their actual Revenue and Earnings (EBITA) for FY24 was $2.9 billion and $195.1 million (see NRW-FY24-Full-Year-Results-Announcement.PDF) so that guidance above for FY25 full year revenue of $3.2 to $3.3 Billion ($3.25 B mid-point) and FY25 full year earnings (EBITA) of $205 to $215 million ($210 M mid-point) represents improvements of +12% and +7.6% respectively over FY24, using those FY25 FY guidance midpoints, so overall they are guiding for a better year in FY25, but with a slight slip in margins overall (seeing as the earnings increase is forecast to be lower than the revenue increase in percentage terms).

I have written plenty here on NRW over the years, which you can access here: https://strawman.com/reports/NWH/Bear77

I topped up my NRW (NWH.asx) position in my SMSF yesterday and also added them to my income-orientated portfolio (outside of my super). I'll probably look to increase my NRW position here at some point also now that I've done it in my main real money portfolios.

I still don't like holding companies that look to me to have a share price that is more likely to go down than to rise in the near-term to mid-term, however that's not how I view NRW at this point - I see them as oversold and having an SP that could bounce at any time, just with a change of sentiment, a broker upgrade, and/or one item of positive news from the company. That's also my view on LYL, my largest position both here and across my real money portfolios, which is why I'm happy to hold both LYL and NWH during their current respective pullbacks. I fully accept that they might go further south before they recover, but I remain confident of that recovery, and I don't want to be on the sidelines when it happens, because it could easily be a decent and fast move back north, when they do start to recover. And it could happen any time, without notice.

- - -

Further Reading (while NRW were still in that trading halt, so before they released their H1 report and the info included above):

Whyalla steelworks fallout trips up $1.5b mining contractor

by Simon Evans and Phillip Coorey, AFR, Feb 23, 2025 – 12.23pm

NRW’s mining contracting business Golding is owed up to $120 million in the collapse of the Whyalla steelworks and the nearby iron ore mines that supplied raw materials to the Sanjeev Gupta-owned group.

Meanwhile, Treasurer Jim Chalmers on Sunday played down the prospect of the government taking an equity stake in the Whyalla steelworks, but flagged mandating quotas to ensure the plant’s product was used in government projects.

Sanjeev Gupta’s Whyalla steelworks. Ben Searcy

“We’re looking at the procurement part. I think already 75 per cent of the steel out of Whyalla goes to things like railways in Australia, infrastructure projects, so there’s already a big opportunity there, and if there’s more we can do, more that we can think through on that front, we will do it,” Chalmers said on ABC’s Insiders.

The $1.5 billion ASX-listed NRW has asked that a trading halt be extended until February 28 while it hastily recasts its first-half financial accounts following the dramatic move by the South Australian government to force Sanjeev Gupta’s Whyalla plant into administration.

NRW’s Golding contracting business is the largest single creditor to OneSteel Manufacturing, the corporate entity pushed into administration that owned the ageing Whyalla steelworks and associated iron ore mines operated by another Gupta company, SIMEC, about 60 kilometres from the plant.

Two sources with knowledge of the situation, both of whom requested anonymity because they are not authorised to speak publicly, said Golding was owed around $120 million.

NRW did not detail how much money it is owed in an ASX statement on February 21 when it sought a trading halt extension.

It had been scheduled to unveil its interim 2024-25 result on February 20.

“NRW therefore requests a voluntary suspension until the company is in a position to provide the markets with an update to the SIMEC position and the timing of the release of the half-year results, expected to be no later than Friday, February 28,” company secretary Kim Hyman said.

NRW, which provides mining contractor services around Australia, has suffered a 20 per cent fall in its shares since November 19, when the stock was trading at $4 and it became apparent Gupta was struggling to refinance his global steel operation.

Golding had about 600 workers at three iron ore mines in the Middleback Ranges when the $600 million three-year contract was announced in early 2022, running until January 2025. The Golding workforce had been progressively pruned back over the past few months as Gupta attempted to cut costs and prepared to take mining back in-house.

KordaMentha was appointed as administrator of the Whyalla steelworks and the iron ore mines on February 19. Prime Minister Anthony Albanese and SA Premier Peter Malinauskas collaborated on a $2.4 billion rescue package on February 20.

That included $292 million for buying railway lines to help underwrite production.

KordaMentha declined to comment on amounts owed to creditors, or the status of any specific creditor. The first creditors meeting is due to be held on March 3.

The SA government lost patience with Gupta over mounting unpaid bills that left the town of Whyalla, 380 kilometres north-west of Adelaide, reeling. Gupta’s unfulfilled promises about future upgrades of the plant angered many local businesses, and bigger ones too. ASX-listed rail freight operator Aurizon suspended hauling iron ore for several weeks because it was not getting paid.

Whyalla Mayor Phill Stone described the SA government’s move as a circuit breaker.

“It’s going to be a long, hard slog. There needs to be a regeneration, but it is going to take time,” he said. “But it has definitely lifted the town’s spirits, having a long-term injection of funds.”

SA government water utility SA Water is owed $17 million in the collapse. Malinauskas has diverted $600 million earmarked for a taxpayer-funded proposed hydrogen plant near the steelworks to the rescue fund for the steel plant instead.

--- ends ---

See Also: NRW-Half-Year-Results-Release.PDF [5:01pm, 28-Feb-2025]

And: NRW Half Year Results Presentation.PDF plus NRW Half Year Accounts.PDF [all released @ 5:01pm on 28-Feb-2025]

Disc: Holding.