Consensus community valuation

Since Feb 2023 when Connexion Mobility announced its agreement with General Motors (GM) in the US and following Aaryn Nania appearance on Strawman in the same month i have been impressed with how two key areas of CXZ have evolved :

- Culture of the organisation and

- Capital allocation at CXZ.

I will step through why such a view has been formed.

Firstly having held Connexion Mobility from mid 2021 and having monitored the progress via (Quarterly 4C release as well as half yearly and annual results) the risk reward to the upside is more evident today than ever.

Recognising that Connexion Mobility revenue is heavily dependant on GM and due to confidentiality any investment MUST factor this into the risk.

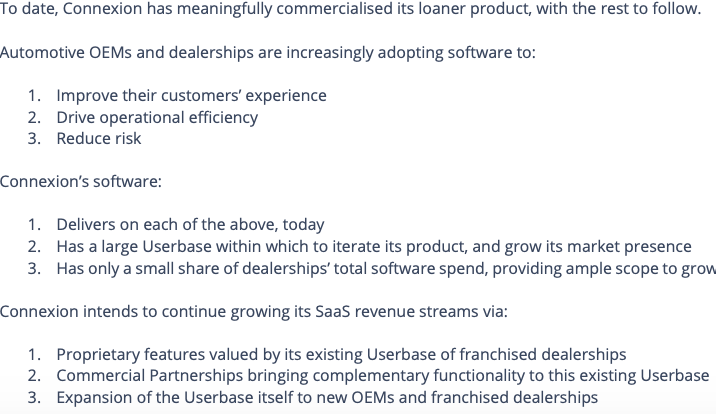

Much of the 7,000 GM dealerships are independent and thus even though GM has an agreement with CXZ it is the dealership discretion to determine the best software. No dealership is obligated to shift to CXZ platform and can make their own decisions on which platform is most suitable in seeking to effectively manage loan car as well test drive systems.

As an investor what is appealing about this model is the incentive for CXZ to develop and show the merits of their system is their for them to show. Failure to do this well will not only led to poor uptake but ultimately loss of contract longer term.

CXZ led by Aaryn recognise this and have not only invested into product development and resources but taking a considered approach to ensure the product is meeting the needs and is of great value.

Results over the past year 2023 and expectations for 2024 and beyond

Hard to fault with positive CF , earnings and NPAT and in doing this reinvestment back into the business to drive improved sales and margins.

Back to my two original points re the Culture and Capital allocation in which CXZ have done very well.

Culture of Organisation

Over the past year CXZ have recruited in a manner which is prudent and in line with revenues rising which has ensured financially profitability is still in check but at the same time place the appropriate resources on the sales and product focus to grow the number of GM dealers whom seek to convert to the platform. This is unfolding and expect this investment to deliver meaningful lift to revenue and profitability going forward.

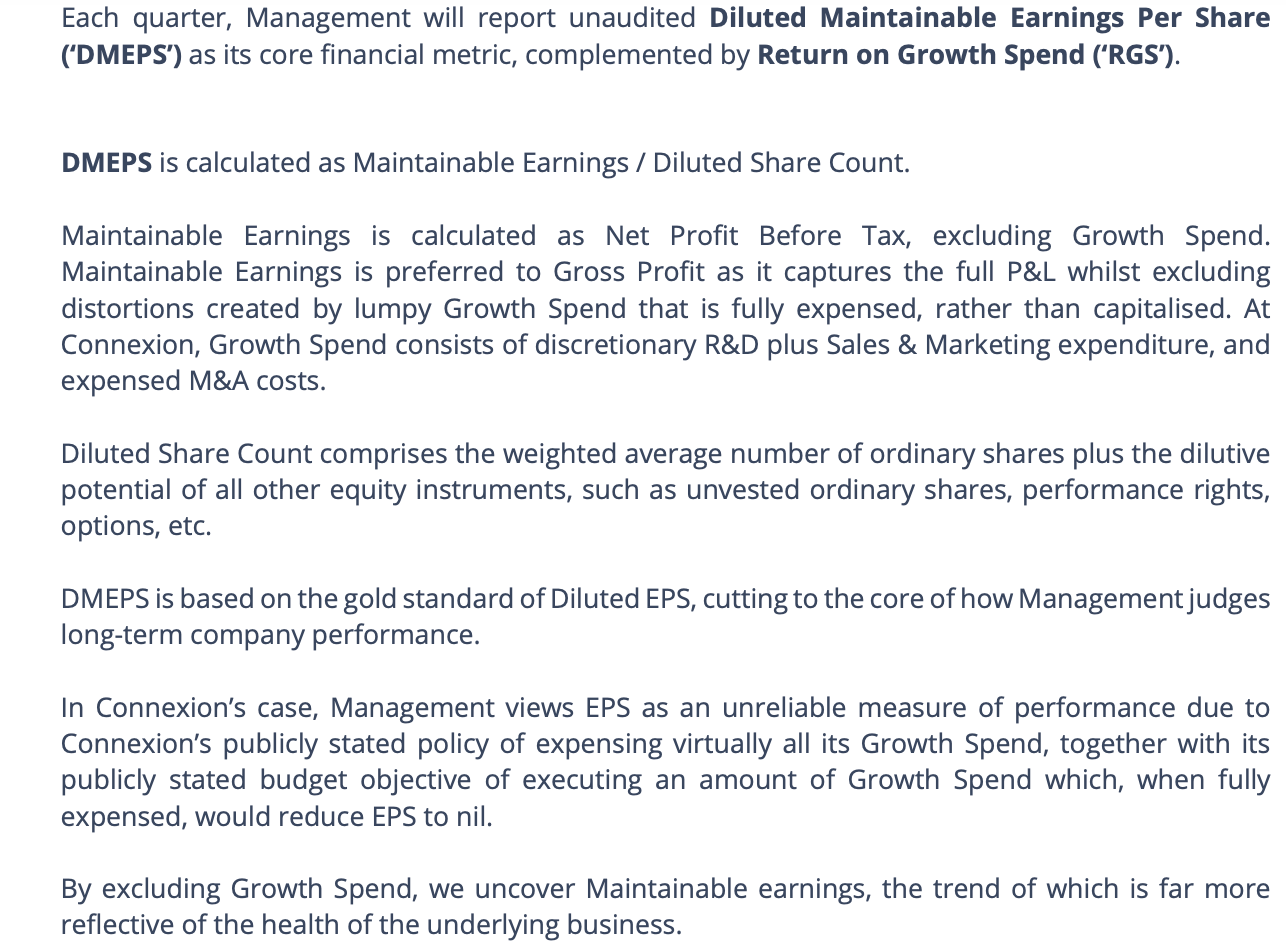

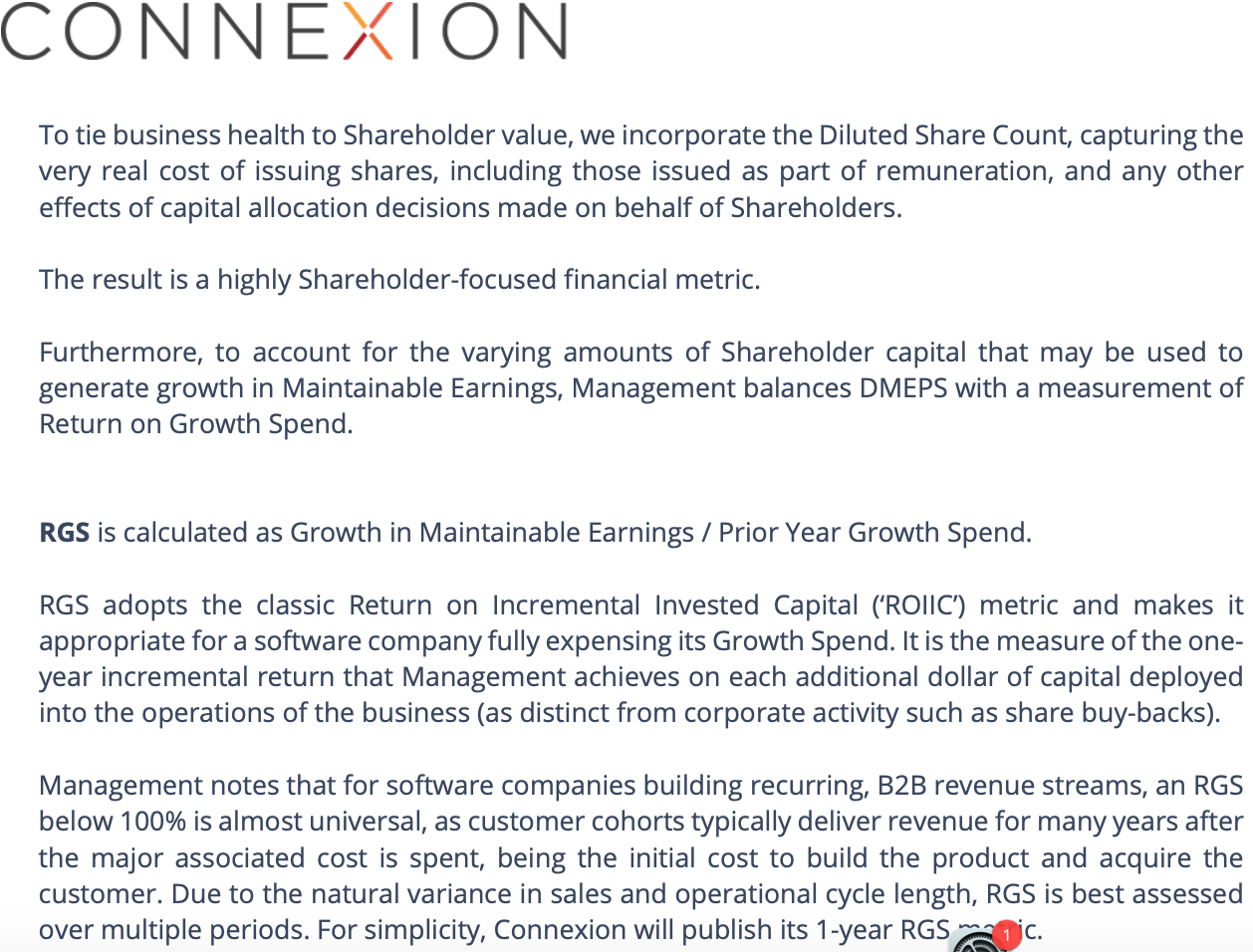

Second Half 2023 Management brought in metrics to align and improve the accountability of the team. The two metrics which are key to future are,

- Diluted Maintainable Earnings Per Share or (DMEPS)

- Return on Growth Spend (RGS)

If the previous guidance by Aaryn and the leadership team on focus on gross profit is anything to go by whereby in Q23 2022 GP was 605k and by Q2 2024 this increased to $3.83m the evolution of these two metrics provide optimism on the customer penetration that may be achieved and thus improved financial results that will flow.

Below is a extract from October 16th 2023 press release re both definitions and the link to management LTIP.

In respect to Capital Allocation i am very positive of the actions taken by Aaryn. His finance background as Co - Founder and Chief Investment officer at Lucerne Investment Partners is no doubt proving to be a real strength for the organisation. Below data speaks for itself.

- Share Count Reduction in 2023 of 45,233,733 ordinary shares or 4.7% of total share count which brings the share count down to under 900m.

- Investment into new product has been done without the need to raise monies or dilute shareholders.

- Cash on Hand of $4.3 mil

- No debt on balance sheet

From a valuation standpoint i will complete an update but support the 3.2c listed last year.

Disc : Held on SM and RL

CXZ H1 2024 Interim-Report-Highlights.pdf

CXZ Feb 9th 24 -Half-Yearly-Report-and-Accounts.pdf

CXZ GM Agreement 2023 Market-Update.pdf

Pricing - Connected Car Software Development - Leaders in Smart Car Technologies (connexionltd.com)

Debt / equity ok.

Return (inc div) 1yr: 109.09% 3yr: -5.20% pa 5yr: 35.69% pa

Dealerships:

The Connexion platform for locations focused on cost recovery & essential management of courtesy vehicle fleets$150 /month

Groups & OEMs:

The fully connected solution for Dealer Groups & OEMs looking to deliver consistent & efficient fleet programs across a network of dealership locations.

"We estimate an ARR of US$6.5m (A$9.3m) incorporating the recent product upgrade/price increase, which would see CXZ trading at ~1.7x EV/ARR against an estimated EV/ARR small SaaS peer average of 2.8x (EVS, PRO, UBN, SKF, KNO, 8CO and K2F). A peer average would imply a valuation of $0.027/share. Larger peer Infomedia (ASX:IFM) is trading closer to 3.6x EV/ARR, and would imply a valuation closer to $0.038/share. More importantly, CXZ will be profitable at the EBIT and NPAT line, which none of their small peers can currently claim. Our numbers suggest an FY24 PER (incorporating a full 12-months of the upgrades) of 7.0x and EV/EBIT of 3.0x."

From the $3m USD boost to ARR ($4.35m AUD), the most important task is to now work out what proportion would fall to the bottom line. Aaryn may choose to reinvest these profits for further growth (I think that's a smart play), but investors will look to see what the level of underlying profit is (even if the company does choose to reinvest these new profits). We know that CXZ has a gross margin of ~80%, so they will take circa 80% of the A$4.35m revenue as gross profit, that's $3.48m AUD in GP. From here, CXZ doesn't actually need to expand its sales & marketing (S&M), nor R&D (although it is likely to reinvest in R&D). So this boost to revenue is being serviced from the same cost base as before. We know that there are 3 new customer success managers who are joining. Let's assume they are on $100K AUD each. That's a $300K AUD increase in fixed costs. Other than that, there's no need to increase costs in line with this increase in revenue. This is what I love about SaaS companies - excellent scalability. So we might see around $3.48m AUD - $300K AUD - $180K AUD other costs (just to be conservative) = ~$3m AUD of the $3.48m AUD in GP (and $4.35m AUD in rev) fall to the bottom line as profit before tax (PBT). That's about ~A$2.1m net profit after tax (NPAT). On a 10x multiple of that, we have a market cap of A$21m (2.3c/share). I think a 10x multiple would be fair for minimal future growth. If we bake in some prospects of solid future growth, on a 20x PE, we have a market cap of A$42m (4c+/share).

My rough back-of-the-envelope estimates based on this $3m USD boost to ARR:

Assumptions:

- $1.5m USD boost to rev in 2023e (half of the financial year remaining)

- $3m USD boost to rev in 2024e (versus 2022) (all $3m USD of the ARR boost flowing through)

- NPAT margin expands to 25%

- PE of 15

Leads to a share price estimate of 3c for FY23e and 3.8c for FY24e, versus 1.4c currently.

We're back to all-time highs in performance.

Would love to get other thoughts.

Seems to be trending really well and continuing to chalk up all-time highs in gross profit. I'm happy with this. Running at annualised $3.6m USD in gross profit, which equates to $5.11m AUD GP. They have $2.5m USD in net cash and investments ($3.55m AUD). That's an EV/GP ratio of 1.2x [($9.9m AUD mc - $3.55m AUD cash) / $5.11m AUD GP].

"The Company recognised total revenue during the Quarter of $1,125k, which included a 6-Quarter high of $1,017k of SaaS Revenue. This led to an unaudited Gross Profit of $891k for the Quarter – the highest in Connexion’s history".

"From a financial perspective, we will continue targeting growth in Gross Profit combined with a neutral bottom line. To date, the current Management and Board have successfully demonstrated a disciplined approach to the management of Shareholder capital, and this will continue as the Company invests for growth."

Not long to go before the next quarterly (Q2 FY23) is due (end of the month), hopefully, we see a continuation of the recovery (semiconductor shortage induced) with a further increase in both i) subscription-based SaaS revenue and ii) fixed-dollar SaaS revenue...

Some insights on the size of the prize (the broader market that CXZ plays in, and its growth rate) from the IFM AGM Presentation (slide 26) are presented below:

Currently, CXZ's product (fleet and rental platform) only represents a very small, single-digit % of a typical dealer’s total software spend.

Given the strong gross margins typically of SaaS, if CXZ can grow from, say, 1% of a dealers annual spend to 3%, then that should see CXZ generate multiples of the cashflow that they do today.

Pleasing results:

- Another profitable quarter (PBT = $199K USD), with increased R&D (all-time high), and the 2nd highest gross profit result on record ($767K USD)

- The global vehicle shortage (linked to the semiconductor shortage) finally seems to have bottomed out... (refer to "subscription based SaaS revenue" chart below)

1.0c/share is a $5.49M USD market cap for a company doing run rate revenue of ~$4M USD (1.4x) and run rate PBT of ~$800K USD (6.8x)... with these numbers set to continue increasing as i) the vehicle shortage unwinds further and ii) increasing product investments yield more fixed-dollar SaaS revenue...

I'm personally quite pleased with the progress the company is making in possibly the most challenging macro environment it has experienced since listing. The global semiconductor shortage continues to impact GM and has done so in a very material way. But, I believe that the worst of this crisis is now over and that we may see an impending recovery in revenue (as global vehicle inventories recover)... the market is forward-looking... which is why I believe the share price appears to have bottomed out and is slowly moving up from the $0.008 (0.8c) low...

The next couple of quarters will be telling...

- No debt.

- Profitable.

- Pricing leader.

- Sub $10m market cap.

- Relatively lean cost structure.

- Recurring revenue model (SaaS).

Personally, I'm very happy to continue holding and slowly accumulate. I'd love to see CXZ at a $30m+ market cap in time and I don't see why that's not possible if they can hit A$2m EBIT in time (15x multiple).

For CXZ, the most important variable is the level of dealer inventory, which has been suffering since Q3 FY21 due to the semi-conductor chip shortage. That appears to be showing signs of recovery now for GM, based on the chart below (subscription-based SaaS revenue). Although, in management's typical conservative style (great) they are not claiming that yet.

In saying that, the main risk that I am watching is that dealer inventory levels may never return to the pre-COVID peak (Q4-FY20). We've now had a couple of years of dealers operating with very very low levels of inventory and they have found ways to work around that. So I don't expect that they would give up those efficiencies -- there should be a recovery, but I personally don't think we're going to go back to pre-COVID dealer inventory levels.

Overall, it looks like the share buy-back has put a floor in the share price for the moment at 1.0c. I think that was a very smart move, particularly given their profitability and high level of cash in hand relative to market cap. It reaffirms the belief of the company that the current share price is undervalued at 1.1x EV/GP [A$8.8m MC, A$3.75m cash and investments, A$5.05m EV, A$4.59m GP, A$1.04m EBIT]*

I think Aaryn is playing a very long-term game here, which I like and I also like the fact that CXZ is not at the mercy of the market (i.e. a capital raise). Fairly cheap on all multiples; revenue [0.87x EV/sales], gross profit [1.1x EV/GP] and EBIT [4.9x EV/EBIT], and the upside opportunity (other than multiples expansion) is the co-sell of other services (ie. the tolling pilot), new OEMs (they finally have a chance now with Ford and Lincoln) and the GM recovery (led by an increase in dealer inventory numbers). As long as they re-sign GM again in 2026 and retain key talent, I am of the belief that we will see a consistent path of steady gross-profit growth.

* For gross profit and EBIT, I've taken Q4-FY22 figures of US$795K and US$180K respectively, converted to AUD at an FX of 1.44x, and annualised (x4). Gross profit has increased quarter on quarter now for 4 consecutive quarters and is now at an all-time high.

$CXZ. Difficult to model out the potential upside scenarios. But, as a starting point, here's what I believe the bear case $CXZ.AX valuation to be: assuming a) zero OEM expansion, b) no partnership revenue and c) the loss of the GM contract in 2026 (all reasonably far-fetched).

A good quarter in challenging circumstances. I for one really appreciate the transparent breakdown of the drivers of performance via the waterfall chart that is shown.

CXZ has actually added $744k p.a. in organic top-line growth in the past 15 months (see the second waterfall chart), plus pipeline. So far, that has simply been outpaced by external headwinds (FX, COVID, and the semiconductor chip shortage).

Headwinds and tailwinds come and go... but Connexion's strong underlying progress should become apparent before too long. Until then, management's focus remains on executing against the strategy presented to shareholders.

With $2.6m in gross profit for FY21, at a share price of 1.7c (MC of $15m), the company is trading on circa 5.8x GP. Personally, I think the downside risk is minimal from here. CXZ's financial performance will rebound as the global semi-conductor shortage unwinds over the next 12 months (and beyond). And importantly, GM is locked in for a minimum of 5 more years.

If we conservatively assume that CXZ rebounds to pre-pandemic levels of $800K GP per quarter for $3.2m GP per annum and assume that the GP multiple increases to a conservative 10x (on the back of CXZ showing promising signs of growth), that equates to a market cap of $32 million (excluding potential upside from other commercial deals). With circa 880m SOI, that leads to a short-term fair-price target of 3.6 cents.

The company is building a shareholder base of committed long-term investors who understand the medium-term nature of this investment and the scale of the upside on offer if the company commercialises its strategic asset with GM. CXZ investors are also increasingly aligned with Aaryn and his leadership style (transparent, no bluff, and hard-working).

The register is slowly improving and flushing out those who are misaligned. That's exactly what I want to see. I'd rather this be a gradual share price climb from here rather than a volatile and trading-fueled share price ride.

Investor registers with committed, knowledgeable, and long-term hands often result in the best share price journeys. There's likely still a bit of turnover we need to get through because the scale of the register flush at 3c last year was extreme (evidenced by the large upper wicks on the candle bar chart from Aug 2020 and high volume), but everything is moving in the right direction.

Between the 21st of May 2021 and the 28th of July 2021, the collective holding of the Top 20 shareholders has increased by 88.9 million units, with 6 entities across the Top 20 buying over this period and only 2 selling.

Entities/individuals ranked between #21 and #100 on the shareholder register increased their holding by a collective ~24m units across this period with 23 entities buying and 8 selling. The Top 100 shareholders of CXZ are strengthening; buying from investors ranked #101 to #500+.

Whilst not guaranteed of course, I'm confident of doubling my money in this investment from these levels over the next 12 months or so. The semiconductor shortage might take a further 12 months from here to resolve itself, but it is likely that the forward-looking market will react prior and "climb a wall of worry" as it often does.

Any additional, unexpected commercial deals, and watch out...