Consensus community valuation

Clearly the key binary event for CXZ coming up is whether their GM contract is renewed (due mid/late this year). I note this excerpt below from their release today.

a) this is not nothing if it ends up coming off - probably 10-15% revenue increase which will mostly drop to bottom line but, regardless, b) is this the type of thing GM would commission them to do if they are intending to move to a new software provider this year?

If you think the contract will be renewed then you have a vehicle with around $10m in cash/investments and long runway of earning a steady A$3m+ NPAT (with growth options albeit patchy ones). All for $21m.

- Covertrue investment - I'm not overly excited about this overall. Seems like CEO using their previous fund manager experience. Is Connexion focused on core business or will other investments like this be made? Notes in quarterly that Connexion is actively interested in M&A so this type of buying may continue.

- Priced on an EV/P of less that 4 so continues to be very cheap and buy back shares at that price.

- Not much else to note besides revenue and subscriptions continuing to grow QoQ:

Will continue to hold. Covertrue is a relatively small investment. Connexion is a small holding as well. Still a value play given the very low EV/P ratio.

Connexion Mobility released full year results today and its hard not to be impressed with the results and continued discipline manner Aaryn Nania and the management team.

Before getting into the results its important to note that the biggest risk remains the concentration of revenue to General Motors (GM) which constitutes 99% of the groups revenue and is due for renewal over the next 12months . CXZ work for many years with GM has led to deep and meaningful relationships and seen the expansion of dealers on its platform which is fundamental to its business . CXZ has been able to capture 22% of the General motors franchise light vehicle dealership in the USA (as all dealership are not obligated to switch to CXZ) , so the contract remains important in terms of current revenue and future revenue.

One could say that the share price reflects such risks and if this is successfully negotiated and the concentration is reduced significant upside may lie ahead.

It is also important acknowledge that both Aaryn CEO and Ben CFO have customer diversification as the highest weighting in their incentive structure (see below) reflecting the importance this plays for the business long term.

OK on with the business results in which since Aaryn took the helm in 2021 we have seen

Revenue has risen by 253% , NPAT increased by 486% and EPS rise 500%.

Net profit margin have risen from 11.53% in 2021 t0 22.16 in 2025.

The share price however has risen 66% and thus valuing the business at 21m.

In Australian dollars CXZ is valued at just over 1x revenue, 5.46 NPAT and PE looking back of 9.

The low valuation has seen CXZ actively buy back its shares with a 104,714,395 share reduction in FY 25 or 10.84% of total shares (see below)

For the FY 2025 results were hard to fault.

The fall in Gross profit of 1% caused higher expenses in cost of sales in supporting " the higher engineering and product resources being deployed to support customer delivery and implementation activities". This investment secures future cashflows and has been a hallmark on how CXZ treat such costs.

In summary revenue rose 13.66% , NPAT rose 31.73% and EPS rose 50%.

I posted my thoughts on valuation for CXZ of 6.12c today.

Would appreciate thoughts from broader team on CXZ

Disc Held in RL and SM

Overview Comment:

Thesis playing out as expected. Connexion Mobility is gradually increasing revenue and profitability each quarter. Back stopped by a large cash pile and buying back shares. Will remain a small position, however, will increase in size.

General notes:

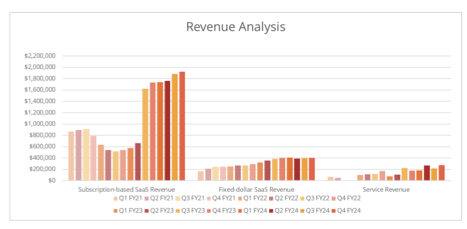

- Revenue growth 3% QoQ.

- Repurchased 18.7m shares during quarter at an average price of 2.5c.

- Main metrics continue to slowly trend upwards:

Positives:

- Diluted EPS for FY = 0.263 US cents = 0.40 AUD cents.

- Cash/investments = $5.9m US = $9.0m AUD.

- Subscriptions continuing to grow every quarter:

Negatives:

- No indication of success with other OEMs.

Has the thesis been broken?

- No, as expected. Still very cheap and keeping as a small position for risk management due to the knockout factors of the investment.

- Meeting all key investment KPIs of increasing revenue, continued buy backs and improving profitability. Will add to position.

Valuation:

Based on EV/NPAT = 8X. Valuation = $2.1m X 8 (EV/NPAT) + $9.0m (cash) = $25.8m MC or 3.2c per share.

What are you expecting and what do you need to see over the next reporting season or generally into the future?

- Continuing to grow revenue and EPS.

- Continued buy backs.

I have increased my valuation from $0.023 up to $0.027

CXN: Net Profit Margin V Good for a market cap of $21.7Mill.

EPS Growth: has slowed.. Needs new contracts.

below: For the Quarter Ended 31 March 2025

............ .................... .....................

at 10 July 2024 Return 1yr: -10.00% 3yr: 34.89% pa 5yr: 8.45% pa

Valuation: (Try the Strawman - Google idea)

Todays Share Price is $0.027

Say Best Case $0.03078 = $0.027 x 1.14% growth per annum

Valuation: at June 2023 $0.023

Pricing - Connected Car Software Development - Leaders in Smart Car Technologies (connexionltd.com)

Debt / equity ok.

Return (inc div) 1yr: 109.09% 3yr: -5.20% pa 5yr: 35.69% pa

Dealerships:

The Connexion platform for locations focused on cost recovery & essential management of courtesy vehicle fleets$150 /month

Groups & OEMs:

The fully connected solution for Dealer Groups & OEMs looking to deliver consistent & efficient fleet programs across a network of dealership locations.

A profitable 26m small cap. Today’s 10% jump might suggest investors are starting to notice?

Connexion reported FY results and pleasing overall.

ALL the reported numbers are in USD.

I have pasted the key elements of the report below but in summary

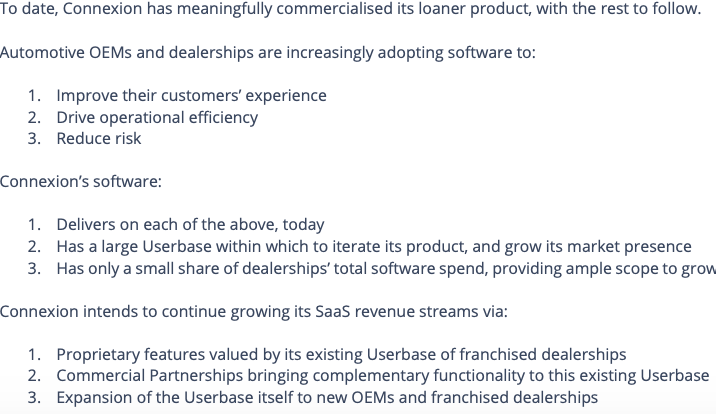

- Strategy outlined by Arryn found interesting, "come for the tool, stay for the network". As has been consistent Connexion are playing the long game growing and enhancing dealership usage and product offerings. This creates stickiness / high retention.

- Top line growth strong with revenue growing at 47% to $9,841,340 USD and Gross profit 78% to $7,680,585USD. It was a 200 basis point decline from 2023 but considering Connexion expense the R&D this is a plus.

- NPAT rose 7% to $1,882,127

- From a Capital allocation perspective just under 7% of shares were repurchased at a favourable purchase price.

- Balance is solid with NO debt and total current assets growing by 29.97% to $7,9120,38. Total equity also grew by 19.3% to $6,280,349.

- Long term alignment across the organisation via LTIP is a feature and is intended to assist with retention which s crucial in capturing new dealerships long term.

- Guidance was non existent for 2025 but this reflects the nature of the Connexion business which has 99% of revenue coming from General Motors dealership in the USA. The ability for Connexion to shift out of this single customer focus will be the challenge over the next 2-3 years. It also reflects the conservative style of Aaryn.

- Connexion is clearly growing well and doing so profitably.

FY 2025 Projections (my projections)

- Revenue grow - 15% plus

- EPS and NPAT - grow faster than revenue

- Share repurchase to continue as opportunity presents itself.

Disc: Held on SM and RL

Connexion Mobility released Q4 results Friday 19th July.

Solid quarter to finish the year with no change to the thesis in terms of Connexion mobility being a long term buy and hold.

Difficulty in assessing CXZ is the lack of client transparency to understand the traction they are getting with dealerships or OEM but the revenue does provide a solid guide as the direction.

It is important to point out that this lack of transparency means understanding the customer concentration is not clear but something Aaryn (CEO) is seeking to reduce and something as shareholders we must keep at the back of our mind as a risk.

CXZ have and are placing a high priority when working with dealers and OEM's to build a solution that solves their problem in managing their fleet of cars and associated issues. Ultimately the uptake will be seen in revenue.

High level Results were as follows:

- 2024 FY Rev 9.8m USD v 2023 6.6m USD . 32% Higher YOY.

- Subscription revenue in Q4 was a significant driver of this growth hitting a all time high to 1.92m of. Total Q4 revenue of 2.6million.

- Currently there are 46 partners as subscribers with a trial underway to have many more join the network.

- To ensure this occurs and is supported the additional 3.5 FTE during the quarter reflects the priority to develop deep relationships with dealers and OEM's.

- This is also being supported by 5% plus increase in the past quarter in costs in the areas of Sales and Marketing and Research and Development.

- With these additional costs profitability for the year remained flat to 2.63m implying a 26.8% net profit margin. Very healthy and positive.

Capital Management strength continues to shine through.

Net cash under Aaryn's leadership has grown from 2.8m in Q4 2022 to 5m in Q4 2024.

Share Buybacks similarly have been used very well to be value for shareholders.

The buyback and retiring of 153million shares since 2022 at a price range of 1c-2.74 (all below current share price of 2.8c) is solid and not something common on the ASX, especially in small cap land (see below)

Looking to the future the best results for Connexion is ahead of them.

It is pleasing to see a CEO take a long term view to build what is necessary to deliver products which are sticky and when scaled will see net profit grow to be 30% plus. How wide can this software be applied time will tell ?

Mission and Vision is clear as noted below :

Finally from a valuation standpoint CXZ @2.8c has MC of 24m AUD.

Converting the key metrics from USD to AUD @ 1.5x

Rev AUD 14.7m

Cash AUD 7.5m

Net Profit 3.9m

Disc Held RL and on SM

Since Feb 2023 when Connexion Mobility announced its agreement with General Motors (GM) in the US and following Aaryn Nania appearance on Strawman in the same month i have been impressed with how two key areas of CXZ have evolved :

- Culture of the organisation and

- Capital allocation at CXZ.

I will step through why such a view has been formed.

Firstly having held Connexion Mobility from mid 2021 and having monitored the progress via (Quarterly 4C release as well as half yearly and annual results) the risk reward to the upside is more evident today than ever.

Recognising that Connexion Mobility revenue is heavily dependant on GM and due to confidentiality any investment MUST factor this into the risk.

Much of the 7,000 GM dealerships are independent and thus even though GM has an agreement with CXZ it is the dealership discretion to determine the best software. No dealership is obligated to shift to CXZ platform and can make their own decisions on which platform is most suitable in seeking to effectively manage loan car as well test drive systems.

As an investor what is appealing about this model is the incentive for CXZ to develop and show the merits of their system is their for them to show. Failure to do this well will not only led to poor uptake but ultimately loss of contract longer term.

CXZ led by Aaryn recognise this and have not only invested into product development and resources but taking a considered approach to ensure the product is meeting the needs and is of great value.

Results over the past year 2023 and expectations for 2024 and beyond

Hard to fault with positive CF , earnings and NPAT and in doing this reinvestment back into the business to drive improved sales and margins.

Back to my two original points re the Culture and Capital allocation in which CXZ have done very well.

Culture of Organisation

Over the past year CXZ have recruited in a manner which is prudent and in line with revenues rising which has ensured financially profitability is still in check but at the same time place the appropriate resources on the sales and product focus to grow the number of GM dealers whom seek to convert to the platform. This is unfolding and expect this investment to deliver meaningful lift to revenue and profitability going forward.

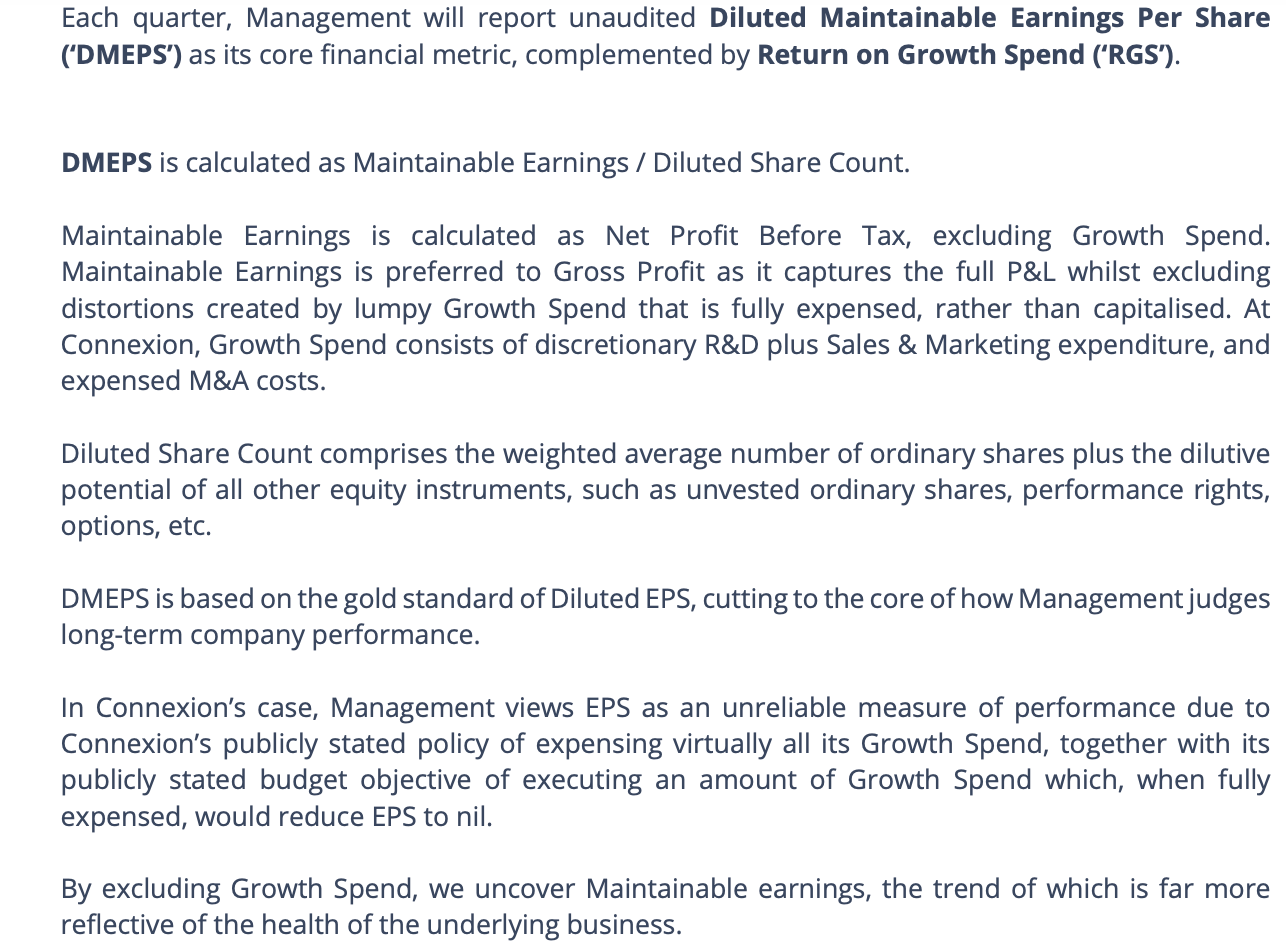

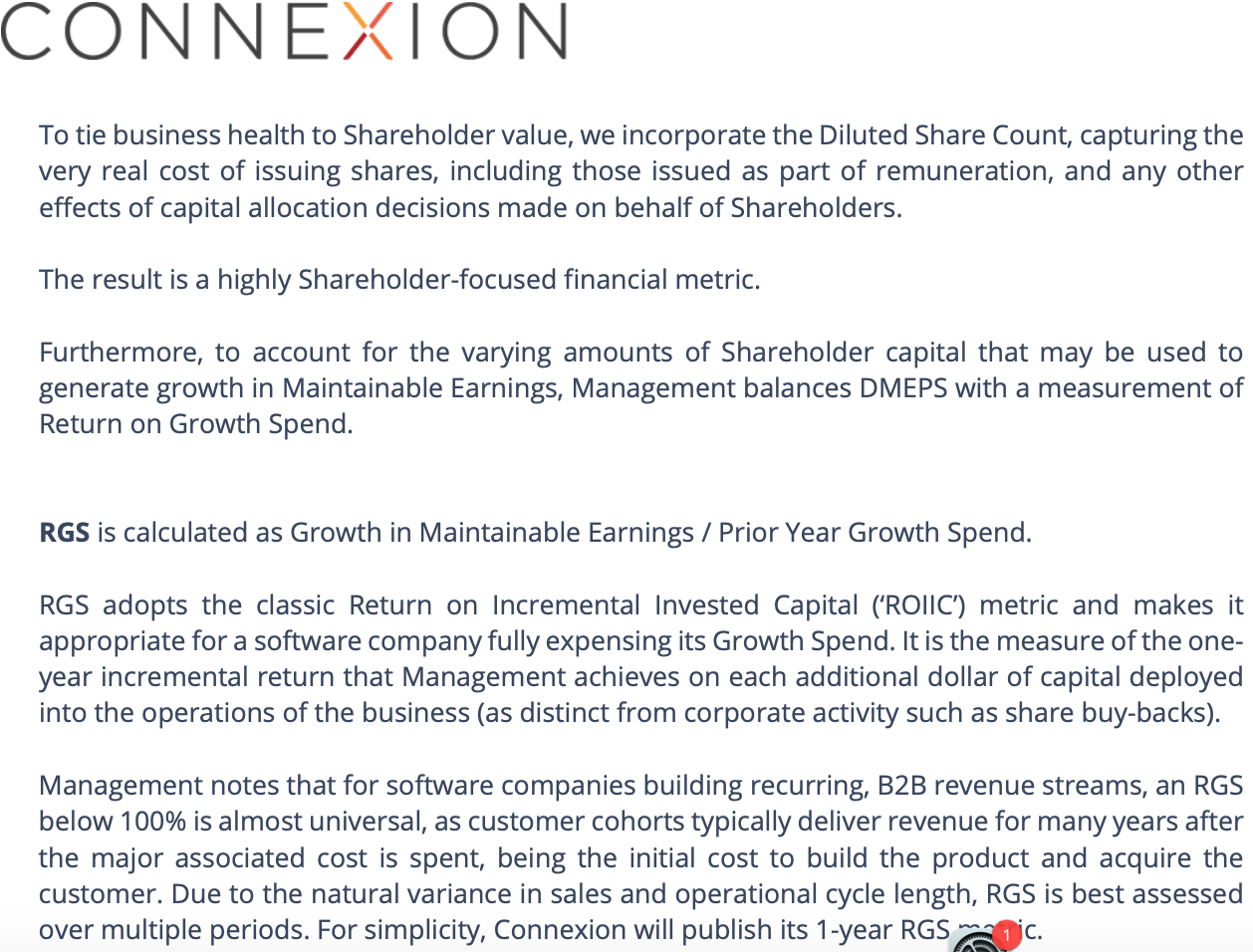

Second Half 2023 Management brought in metrics to align and improve the accountability of the team. The two metrics which are key to future are,

- Diluted Maintainable Earnings Per Share or (DMEPS)

- Return on Growth Spend (RGS)

If the previous guidance by Aaryn and the leadership team on focus on gross profit is anything to go by whereby in Q23 2022 GP was 605k and by Q2 2024 this increased to $3.83m the evolution of these two metrics provide optimism on the customer penetration that may be achieved and thus improved financial results that will flow.

Below is a extract from October 16th 2023 press release re both definitions and the link to management LTIP.

In respect to Capital Allocation i am very positive of the actions taken by Aaryn. His finance background as Co - Founder and Chief Investment officer at Lucerne Investment Partners is no doubt proving to be a real strength for the organisation. Below data speaks for itself.

- Share Count Reduction in 2023 of 45,233,733 ordinary shares or 4.7% of total share count which brings the share count down to under 900m.

- Investment into new product has been done without the need to raise monies or dilute shareholders.

- Cash on Hand of $4.3 mil

- No debt on balance sheet

From a valuation standpoint i will complete an update but support the 3.2c listed last year.

Disc : Held on SM and RL

CXZ H1 2024 Interim-Report-Highlights.pdf

CXZ Feb 9th 24 -Half-Yearly-Report-and-Accounts.pdf

CXZ GM Agreement 2023 Market-Update.pdf