Minbos set for construction to get underway.

It’s been quite awhile for any action to take place and I’ve been patiently waiting but recently the first tranche of funding hit there account and now with the construction contract signed it should be full stream ahead for production next year. With the low capex simple build and all equipment and plant on or near site depending upon winter weather it should be straightforward. Therefore It looks like sentiment and momentum has now changed with the more positive news flow and media coverage. Also there’s more localised positive news with Biden’s recent visit, huge US$2.9B+ US investment, Government support for agricultural development. I don’t think the timing could be much better.

Minbos’s phosphate project is forecast to deliver circa US$55M EBITDA per year over a 20 year mine life. They are currently capped at AU$66M. And there’s the green Ammonia project on top of that.

Biden visit: Mining Weekly

Minbos: Construction announcement

Minbos; Finance news

Minbos presenting this week at the Gates Foundation ( invite only) Fertiliser news symposium in Marrakech

Theme: Low-Carbon Decentralized Nitrogen Fertilizer Production in Africa

Presenting between Fortescue and ocpgroup ( OCP, are responsible for the world's largest phosphate reserves)

CAPANDA GREEN AMMONIA PROJECT UPDATE

”Partnership discussions well advanced, confirming Capanda as the most commercially attractive zero-carbon green ammonia project globally”

Early days but there seems to be little or no value associated with the potential for this Ammonia project. Near term there is still funding that needs too be finalised with the hope of the fertiliser project going into production this year.

other recent announcements were the Field trials

FIELD TRIALS CONTINUE TO DELIVER OUTSTANDING CROP PRODUCTIVITY RESULTS

Great Presentation and update for any one interested in a Fertiliser Company striving to make a dramatic impact.

Minbos edges closer to production next year. Final finance may be the next catalyst although it may have kept the brakes on the SP. Minbos currently maintains the stance final funding will be non dilutive.

Angola Rising: Announcement

An important note I found in the Preso is the bringing forward of production from the DFS by 6yr, up circa 40% for that period (quite significant)

The anticipated cash flow has changed significantly since the DFS due in part to Lower capex and now the bringing forward of production

DFS; Announcement

There's also activity with

CAPANDA GREEN AMMONIA PROJECT

Tender work for key engineering providers is underway in preparation for the PFS.

The PFS will further investigate the use of electrolysers to generate green hydrogen, designed to deliver 112,000 tonnes p.a. of Green Ammonia to produce 255,000tpa of Ammonium Nitrate, including fertilizer and mining explosives.

Driven by 100%-renewable power from the Capanda hydroelectric complex and supported by a competitive power concession, the study will access what the Company believes is one of the only cost competitive zero-carbon Green Ammonia projects being developed globally.

P4 (YELLOW PHOSPHOROUS) PROJECT

In early September, the Company announced it had engaged an engineering, construction and project management company to complete a study to investigate producing P4 otherwise known as yellow phosphate as part of its phosphate-based product offering.P4 is an essential critical mineral in the battery materials supply chain, required to produce lithium hexafluorophosphate (LiPF6), the electrolyte used in lithium-ion batteries. However, exploding growth in the battery sector is putting pressure on P4 supply to the agricultural sector.

Held SM and RL

Minbos has been quietly ticking boxes and going against the trend at the moment. The phosphate project is the bases of my initial interest but there have been a lot of additional opportunities under development . I am currently holding my breath for the imminent report from Stamicarbon in regards to the Green Ammonia Project. Minbos have highlighted that this may be a more valuable opportunity. Would be a nice bonus;)

From the chairman’s letter

“The last six months of 2022 saw Minbos seize a myriad of opportunities that Angola presents. The Company is now firmly ensconced as more than just a phosphate explorer, developer and near- term producer, with development projects that now span agriculture, fertilizers, mining explosives, carbon-abatement and LFP battery-grade phosphate paste.

Some of this growth - green ammonia, explosives and carbon abatement - has come organically, a positive externality from being a good development partner with the Angolan Government. However, opportunities in the battery metals space have locates from new relationships born from the use of phosphate in battery metals.

Phosphate paste is a critical material for the production of Lithium-Iron-Phosphate batteries, with our interest in the product driven by our phosphate production profile with assistance from our new partners who invested in Minbos in mid- 2022, corner-stoning our $25 million placement and bringing a wealth of experience in the battery space.

Our phosphate project has now entered its most exciting phase, construction and near- term production. Daily we are getting updates that the phosphate plant is arriving in its various parts into Angola, and we look forward to watching the plant turn on later in the year.”

held SM and IR

Positive announcement from Minbos today that the "SIMPLIFIED FLOWSHEET DELIVERS SIGNIFICANT CAPEX

REDUCTION FOR PHOSPHATE FERTILIZER PLANT"

The $10m reduction estimate is very significant when the original estimate was for $40m Capex. With the capex now $30m and the Cornerstone investors offering $25 million (Not yet signed off) Minbos now have just a $5m shortfall. This should be covered if the SP can get > 0.15c by the end of April when Minbos Options expire (I hold some).

Short term expected events

- Plant and Equipment due off the Boat any day and production Due Q4.

- While there is also expected significant Cash flow once Production is up and running of further note is that Stamicarbon are due to release the results of their technical study into the "Green Ammonia Project" using the cheapest Hydro Power in the World. Announcement 30 jul 22 . Study underway 20 sep 22 This may be a significant bonus as it appears that no value has yet to be placed on this project which may potentially be more valuable than the current Phosphate Project.

From DFS 17 Oct 22

Minbos planting all the seeds now for future growth, The market liked the news. up 18% on the day

The main news for me was that the,

- Initial construction activities at the Cácata phosphate deposit are on target and within budget.

- Fertilizer plant and equipment are now enroute to Angola with Development and EPCM activities ramping up in anticipation of first production H2 2023.

I expect a flurry of announcements over the next few months prior to production

CABINDA PHOSPHATE FERTILIZER PLANT ENROUTE

Minbos Vision "To build a nutrient supply and distribution business that stimulates agricultural production and promotes food security in Angola and the broader middle african region.

Angola remains one of the worlds great untapped agricultural regions, with +35 million hectares of arable land (the size of France), high rainfall and some of lowest rates of fertilizer use globally. Currently, 100% of all nitrogen, phosphate and potassium (NPK) is imported."

- Minbos may be currently priced at this advanced PFS at 10%NPV. This value was before the significant and ongoing fertiliser price rises and also developments in a Green Ammonia project.

- DFS is due any day.

- Strong Angolian government support and the IFDC (International Fertilizer Development Center) to get this project up and running.

- While there has been little news on the green ammonia project, it looks like it hasn't been priced into the the current share price, but if they are able to secure there request for 200MW from the 100MW already highlighted, it may become a significant project in its own right.

- I think the SP may already be discounted for some sovereign risk.

- Early site works underway, Long lead items paid for a due for delivery Q2, production 2023. Low capex

https://www.investi.com.au/api/announcements/mnb/b50a5f90-260.pdf

With Sky rocketing Fertiliser prices, Minbos may be due for a re-rate very soon. DFS due Q122. What will it be with the higher MAP price and also the proposed reduction in the % of MAP in the Blend (50% -15%).Current mc of $46 million with potential NPV of around US$600+ million

LOW CAPEX US$28M

DFS 1Q22 TO PRODUCTION 2023 Around $8.1M Cash after Placement, expect a lot of news flow in 22

SHARES SOLD DOWN TO CR LEVELS Minbos just had a CR via a placement @10c Directors and Management taking $595k of the capital raise. MNB was at 21c in Oct

https://www.investi.com.au/api/announcements/mnb/b50a5f90-260.pdf

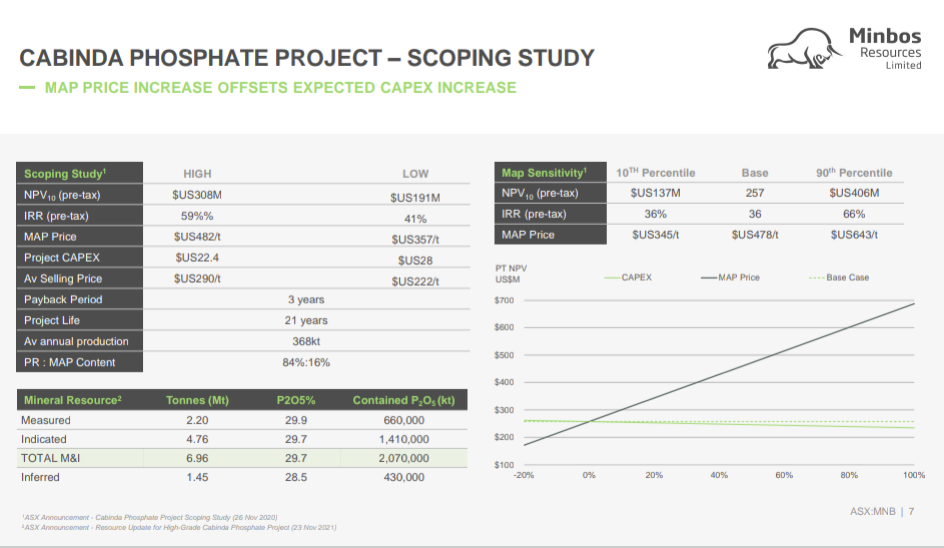

NPV Scoping Study RESOURCE High-grade Resource 8.4MT @ 29.6% P2O5 (85% ownership) Scoping Study

NPV $257M | IRR 58% Scoping Study MAP Price $478/t

AUG 2020; DAP FOB price increased to $328/t as Minbos published its Scoping Study using $428/t FOB ($478/t ex port)

DEC 2021; DAP FOB reaches $820/t after USA introduces countervailing duties on imports and China halts exports.

PRODUCTION Long lead items ordered ,DFS and approvals Q1 2022, Plant shipping ex USA Q2 2022 ,First sales 2023

MINBOS ADDITIONAL PROJECTS AND INTERESTS

Hydrogen & Green Ammonia

Green Ammonia

Government support to establish a Green Ammonia Project

Currently Engaging with technology partners

Land allocated for Green Ammonia Plant

Access to local markets to sell Ammonia Fertilizer through the IFDC and AFFPP

Access to continuously available and clean hydropower with pricing negotiations underway

Angola’s Hydro Power

World-leading Hydro Power Generation

Some of the cheapest power prices globally

Currently negotiating even lower tariff for engaging with technology providers

THE FUTURE

Future Opportunities

NPK Blending and Distribution – Lime

Nitro Phosphates

Soil Carbon

Angola Agriculture

57M ha arable land

1,000 -1,500mm annual rainfall

100% of fertilizers imported