Consensus community valuation

<Long post warning>. My gut feel a few months ago, which I have no qualification to be giving, was that the odds of passing endpoints in November was 50:50. Today, AI casually told me it was 1:7, which made me pause. So I decided to have a serious chat, in which AI did most of the talking and I pretended to understand all the big words. But I got what I wanted and I honestly don't think the AI knew what my earlier guess was although...wait...did it just tell me what I wanted to hear?....

A few of you follow pharma and biotech so you might find the output interesting. Anything missing?

Q. What approaches would sophisticated funds and big pharma take to assess the odds of success of the XanaMia trial, now that it is past interim futility and is half way through the OLE? The Actingen CEO alluded to asking for the harder futility test to be applied by the reviewers. Does that shift the needle in any way?

Logically go step by step from the broadest averages, and then adjust for all relavant additional information specific to xanamem and this trial. Show your working down from a broad average to specific odds for the upcoming readout in November.

Here's the summary table

And here's the very long answer.

A. Sophisticated funds and big pharma would treat this as a Bayesian / decision‑tree problem rather than “one magic number”, but it is possible to walk from broad industry priors down to a Xanamia‑specific range of odds. Below is one way they might logically do it, including how a “harder” futility test and OLE uptake might shift probabilities. This is inherently judgment‑heavy; the numbers are illustrative, not precise.

1. Start with broad Alzheimer’s trial base rates

From 2020–2023 reviews of AD programs, phase 2 and 3 disease‑modifying trials historically had low success rates, especially before the recent antibody wins. The share of phase 2 AD drugs reaching approval was in the single digits, with phase 3 success rates on the order of 10–20% in many analyses.pmc.ncbi.nlm.nih+1

For a “typical” phase 2b/3 disease‑modifying AD trial using CDR‑SB as primary endpoint (like lecanemab/donanemab programs), a neutral, pre‑information prior for success might be something like:

- 10–20% probability of hitting a clinically and statistically meaningful CDR‑SB effect.

- This is before adjusting for mechanism, enrichment, trial design quality, and any interim data.

So a sophisticated fund might start with ~15% as a crude base rate for “phase 2b/3 AD trial reaches its primary endpoint and is viewed as a true win”.

2. Adjust for modern design and pTau181 enrichment

XanaMIA is not an average legacy AD trial. Two big positives:

- Biomarker enrichment (plasma pTau181):

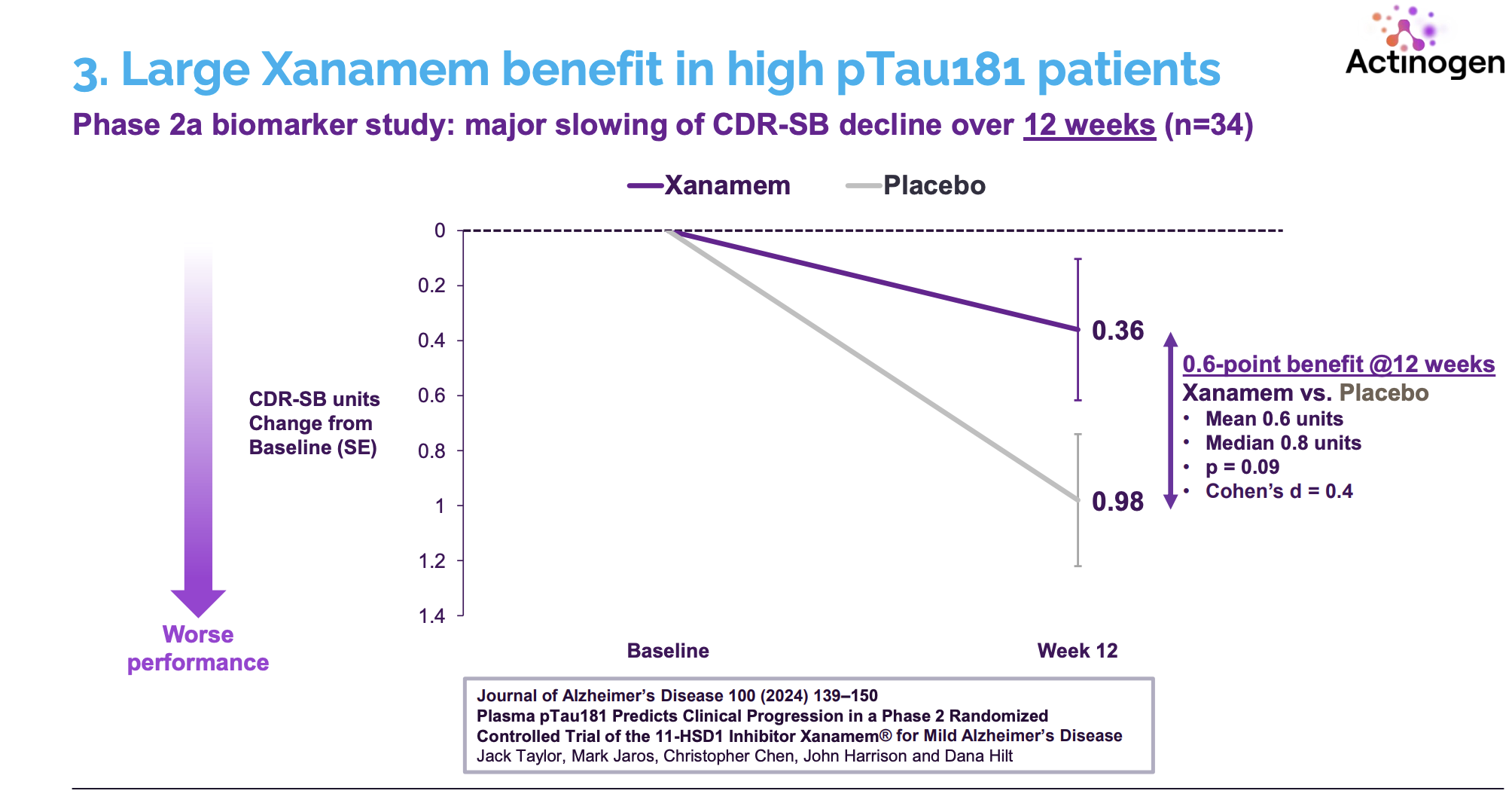

- The XanADu biomarker analysis showed that patients with elevated plasma pTau181 (the “high” group) progressed clearly faster than low‑pTau patients on CDR‑SB and other measures, and that in this enriched group there was a potentially meaningful Xanamem effect (LS mean CDR‑SB difference ~0.6 units, effect size ~0.41, p≈0.09) over 12 weeks.pubmed.ncbi.nlm.nih+1

- This supports:

- Better “signal‑to‑noise” because progressors are selected.

- Prior evidence that this drug can move CDR‑SB in the right direction in the biomarker‑positive population.

- Modern endpoints and trial design:

- CDR‑SB is now the dominant global function endpoint in early/mild‑moderate AD and has been accepted for recent mAb approvals.pmc.ncbi.nlm.nih

- XanaMIA follows a 36‑week, randomized, placebo‑controlled design in 247 patients with mild–moderate AD and elevated pTau181, across AU/US sites, described as one of two pivotal trials aligned with FDA feedback.ACW-HY26-results-XanaMIA-pivotal-Alzheimers-trial-progress.PDF+1actinogen

Relative to the “average, older‑style” AD trial, funds and pharma would typically up‑weight success odds for:

- Enriched, biomarker‑positive population that has already shown both strong progression and a trend to drug benefit.

- Alignment with contemporary regulatory thinking (CDR‑SB, disease‑modifying framing, etc.).

It would be reasonable to bump from ~15% to somewhere in the 20–25% range purely on trial design and biomarker enrichment, before looking at any drug‑specific data.

3. Adjust for Xanamem’s mechanism and prior clinical signal

Key Xanamem‑specific positives:

- Validated mechanism and CNS exposure:

- Xanamem is a selective 11β‑HSD1 inhibitor designed to lower cortisol production inside the brain. PET and pharmacology work showed high CNS target occupancy at 5–30 mg/day, and endocrine readouts (ACTH, cortisol dynamics) consistent with potent 11β‑HSD1 inhibition, with acceptable systemic cortisol effects at 10 mg.Jan-2026-ACW-positive-XanaMIA-Interim-Analysis-outcome.PDFactinogen+1ACW-HY26-results-XanaMIA-pivotal-Alzheimers-trial-progress.PDF

- Prior AD signal:

- In biomarker‑positive mild AD (elevated pTau181), Xanamem previously slowed CDR‑SB worsening vs placebo over 12 weeks, with an effect size in the small‑to‑moderate range.journals.sagepub+2

- Depression trial (XanaCIDD):

- In 2024, the 6‑week phase 2 depression trial showed clinically and statistically significant MADRS improvements and positive patient‑reported severity measures vs placebo, reinforcing the CNS cortisol‑control mechanism in another population.firstwordpharmaJan-2026-ACW-positive-XanaMIA-Interim-Analysis-outcome.PDF+1

- Safety:

- More than 500 individuals have now received Xanamem up to 36 weeks with no reported serious adverse events attributed to the drug, which supports the ability to dose long enough to see disease‑modifying effects.Actinogen-March2026-quarterly-4C.PDF+1

On the other hand, the magnitude of prior AD effect was modest (trend in a subgroup), and cognition in XanaCIDD improved similarly in both arms (placebo strong), so it is not an obviously “home‑run” profile.

A sophisticated buyer typically:

- Further steps up the probability because there is some prior disease‑relevant signal, in a biomarker‑enriched subgroup, not just target engagement.

- But does not jump to antibody‑like odds because effect size and duration are shorter and there is no prior large successful pivotal.

Reasonable adjustment:

From 20–25% (design/enrichment) to perhaps 25–35% based on mechanism + prior signal.

4. Incorporate the interim futility analysis outcome

4.1 What the DMC saw

The independent DMC reviewed unblinded safety and efficacy (for futility) on ~37% of the planned final dataset: 136 participants with at least one efficacy data point and 52 who had completed the full 36 weeks. The recommendation was to continue the trial “without amendment” after an earlier positive safety‑only review.Jan-2026-ACW-positive-XanaMIA-Interim-Analysis-outcome.PDF+2

In Bayesian terms, “passed futility” means:

- The data at ~37% completion were inconsistent with the trial being clearly futile under the pre‑specified futility boundary.

- That boundary, if more stringent (“harder futility test”), will itself shape how informative this decision is.

4.2 “Harder futility test” – what does that mean?

In practice, a “harder” futility test usually means a more aggressive stopping rule (e.g., higher conditional power threshold) such that:

- If the emerging effect size is modest and unlikely to reach significance at N=247, the DMC is encouraged to stop early.

- Only trials with plausible effect sizes consistent with success at full enrollment are continued.wikipedia+3

The Actinogen disclosures and your comment that the CEO alluded to asking for a harder futility test are consistent with:

- Sponsors pushing for a low tolerance for mediocre signals; i.e., they would rather the DMC tell them it is futile than spend money on a long‑shot.

- Given that the DMC, under that stricter rule, chose not to stop for futility, the posterior probability of ultimate success is meaningfully higher than the prior.

There is no published futility boundary, so one cannot quantify this exactly. But experience across oncology and neurology suggests that for a trial with aggressive futility rules:

- Passing futility at ~⅓–½ information can easily double the market’s fair probability, because the scenario where the true effect is “near zero” is heavily pruned.

From 25–35% pre‑interim, a disciplined fund might move to something like 35–50% post‑interim, with the center of gravity perhaps around 40%, acknowledging:

- The DMC did not say “overwhelming efficacy”, merely “not futile”.

- Some trials still fail after passing futility, especially if the emerging effect is borderline.

5. Open‑label extension (OLE) uptake as a soft signal

The OLE began in March 2026, with the first participant treated 31 March, and early data showed 15 of 17 (88%) eligible participants rolling over into the OLE within the first month.Actinogen-March2026-quarterly-4C.PDF

Funds and pharma will see OLE uptake as:

- A strong safety signal: Participants and investigators are comfortable continuing on active drug for up to 25 months.Jan-2026-ACW-positive-XanaMIA-Interim-Analysis-outcome.PDF+1

- A maybe‑weak efficacy signal: If the drug were clearly hurting, investigators might discourage OLE participation, but with AD and no other curative options, high OLE uptake is expected even with neutral efficacy.

Given AD context, 80–90% OLE uptake is not enough to materially change efficacy odds by itself. It likely confirms:

- No obvious catastrophic safety issue emerging.

- Engagement of sites and patients, which reduces operational risk and missing data but does not say much about CDR‑SB separation.

So sophisticated assessors might tweak probabilities marginally up for “no obvious negative signals surfacing”, but not more than a couple of percentage points.

6. Overlay current AD competitive landscape

Compared to anti‑amyloid antibodies:

- Lecanemab’s CDR‑SB separation at 18 months was ~0.45 units (27% slowing) with baseline CDR‑SB ~3.2.eisai+3

- Donanemab and others showed similar 20–30% slowing in early AD.pmc.ncbi.nlm.nih+3

These set the bar for “clinically meaningful” effect size: regulators and payers now expect at least modest slowing on CDR‑SB.pmc.ncbi.nlm.nih

For a first‑in‑class oral cortisol‑modulator:

- A smaller effect than antibodies might still be commercially compelling (especially if safe, cheap, easy to administer, combinable).

- Statistically, however, XanaMIA still needs a detectable and robust CDR‑SB effect at 36 weeks.

Given the earlier 12‑week effect around 0.6 CDR‑SB in the enriched subgroup, one can reasonably hypothesize:pmc.ncbi.nlm.nih+2

- If that effect sustains or grows modestly over 36 weeks, the trial could hit.

- If the effect attenuates with time or the pTau181 enrichment plus trial noise reduces signal, it may miss.

This context probably keeps a sophisticated analyst from moving probabilities above ~50%, because:

- There is no prior large, clearly positive AD trial; everything rests on one biomarker‑subgroup signal + mechanism.

7. Putting it together – worked‑through “house view” range

Pharma BD and sophisticated funds might end up with ranges rather than a single number. A reasonably defensible step‑down could look like this:

<summary table I moved to the top>

Where a pragmatic central estimate could easily cluster in the 35–45% band for “meeting the primary endpoint in November,” with a bull‑case investor perhaps leaning toward 50%+ and a bear staying closer to 30–35%.

This aligns with the Space instructions: the bull case focuses on:

- Enriched biomarker‑positive population and prior Xanamem signal in that exact setting.pubmed.ncbi.nlm.nih+2

- Validated mechanism and multi‑indication evidence (AD and MDD) with a good safety profile.pmc.ncbi.nlm.nih+1ACW-HY26-results-XanaMIA-pivotal-Alzheimers-trial-progress.PDFpmc.ncbi.nlm.nihActinogen-March2026-quarterly-4C.PDF+1

- A positive, stricter futility read, which strongly de‑weights the “true effect ≈ 0” scenario.pubmed.ncbi.nlm.nih+3Actinogen-March2026-quarterly-4C.PDF+1

The bear case highlights:

- Only modest prior effect sizes and short‑duration data, not a prior pivotal win.journals.sagepub+1

- History of failure of most non‑amyloid AD mechanisms, even with reasonable biology.explorationpub+3

- The fact that passing futility is a necessary, but far from sufficient, condition for success; many such trials still fail.fda+2

Crucially: the CEO’s comment about asking for a harder futility test does reasonably “shift the needle” relative to a standard or soft futility rule. If the rule was genuinely stringent, a continuation decision at ~37% information justifies moving from, say, ~25–30% into the high‑30s or low‑40s as a central probability, but not into the 70–80% territory that you might reserve for a drug with a prior clear pivotal win.

From Monday's presentation, this slide shows a possible trend over 12 weeks for biomarker-positive patients in the phase 2a Alzheimers trial (n=34). If this trend is proven out for the current larger phase 2b/3 trial (n=245), and extends out to 36 weeks, then we have a winner.

Because this bio-marker group (n=34) was a subset of the overall trial (n=72) the above result is not statistically significant. It is nonetheless a clue that the current trial is designed and powered to tease out, because all 245 patients were screened to have this bio-marker, and AI tells me that that should be enough for a significant result. Also, the CEO has 30 years of experience including at FDA, the team is high powered, and they appear to know what they are doing.

Actinogen are now ramping up their phase 2/3 XanaMIA Alzheimer's trial, with interim data expected in Q3 CY2025, following the interesting results from the depression trial. This year has a lot of potential catalysts, that may be enough to bring in a partner to take it to the next level.

Here's an IR presentation where the CEO lays out the state of play, and why it might be a step up from the current Alzheimer's drugs, which are a bit controversial. The more I hear from him, the more I feel it's a good bet (I do have a small stake).

They are going for the holy grail - a safe, once a day pill for the modification of Alzheimer's and then also depression. It's a pill that might be able to be safely paired with other medication. It's a novel mechanism of action - reducing cortisol in the brain (while not affecting the normal hormonal function). It hasn't shown the kind of side-effects associated with SSRIs and other established anti-depressants.

They have evidence that it improves cognition, even in healthy adults. If the trial results prove consistent, it's the kind of thing I think anyone who's interested in maintaining good mental health might take a look at in the long run.