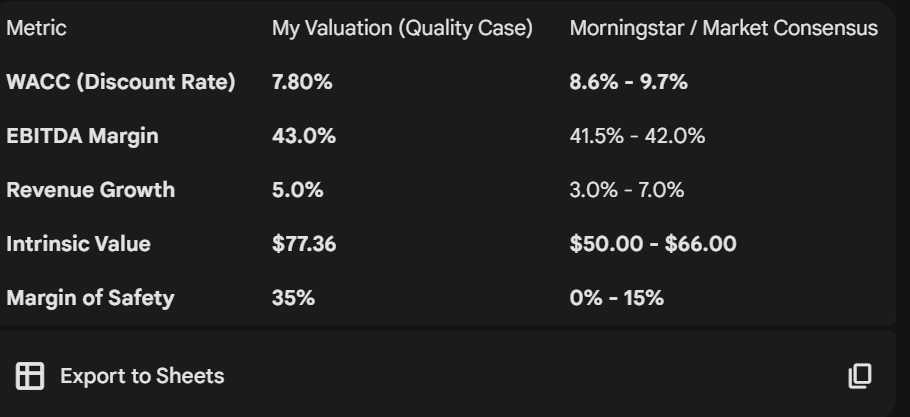

Consensus community valuation

For FY25, Aristocrat generated revenue of 6.3 billion dollars, an increase of 11 percent over the prior year, driven by organic growth and market share gains, and the inclusion of NeoGames for the full period.

Our EBITDA margin expanded from 40.1 to 41.7 percent, reflecting favourable mix and improved operating leverage.

Net profit before amortisation of 1.6 billion dollars increased 12 percent, while EPSA increased 15 percent, benefiting from the strong earnings outcome as well as our on-market share buyback program.

Following the recent legal settlement with Light & Wonder, we expect to recognise a 45 million Australian dollar legal cost recovery in Corporate Costs, relating to legal costs incurred to date,

In terms of Outlook, we reiterate our overarching Group NPATA growth and divisional outlook statements and FY26 modelling inputs provided at the time of our 2025 results presentation in November last year

CEO REPORT for the avid reader

ROE okay 'tick'

Net profit margin 20%

Free Cash flow is ok

Dividend payout ratio: 36% so they retained most of the earnings. ( vs Telstra 100% payout ratio)

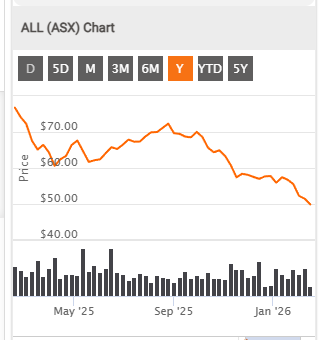

Need a catalyst to spark the share price!

Return (inc div) 1yr: -33.81% 3yr: 14.32% pa 5yr: 10.30% pa

18/5/2023: Growth Return (inc div) 1yr: 27.68% 3yr: 17.11% pa 5yr: 8.02% pa

Next Forecast Ex Div Date: 26/05/2023 (8 days away) : AUD 0.30cps up 15%

Franked:100%

My price target ( for 2023 ) $37.95 = 34.50 x 1.10pa

...........................................March 202 ....Sept 2022

Annual Report Sept 2022:

Chair & CEO message:

Net profit after tax and before amortisation of acquired intangibles (NPATA) of $1,099.3 million was 27% above the prior corresponding period in reported terms (20% in constant currency) compared to the $864.7 million delivered in the prior financial year. This was driven by exceptional performance in North American Gaming Operations and global Outright Sales, despite supply chain disruptions and mixed operating conditions across key markets. Pixel United delivered resilient performance in a challenging environment, as overall mobile bookings moderated post COVIDdriven peaks in the prior period.

ESG - 'extra social govenor'

Aristocrat also continued to execute against our ambitious Environmental, Social and Governance commitments across the year, with a disciplined focus on our most material issues. This included preparatory work to allow the Group to set a science-based greenhouse gas emissions reduction target in calendar 2023. In addition, we made meaningful progress in our responsible gameplay (RG) agenda, with highlights including the launch of an Australianfirst trial of cashless payment technology on gaming machines, and the rollout of proactive RG messaging, tools and information to players of our social casino games. In addition, we delivered enhanced anti-modern slavery training across the Group and achieved an above-benchmark employee engagement score for the year that places Aristocrat in the top quartile of technology companies globally.

Revenue up 5% in constant currency; reported revenue up 12%

• Revenue growth driven by strong performance of North American Gaming Operations and global Outright Sales

• Pixel United revenues reduced in local currency in a challenging macro environment where it continued to take share

• EBITA broadly stable in constant currency, with positive revenue drivers offset by lower margins in Gaming and Pixel United reflecting: o Continued, but easing, supply chain challenges o Product mix favouring Outright Sales o Sustained investment over time in great talent, technology and product underpinned strong performances

• Strong operating cash flow and superior financial fundamentals maintained

• Conservative balance sheet and ample liquidity, with higher interest income benefiting net interest

• $338 million cash returned to shareholders through dividends and on-market share buy-backs, while maintaining full investment optionality

More 2924-02667167-2A1449951 (markitdigital.com)

Aristocrat has announced the proposed acquisition of 100% of NeoGames S.A. (“NeoGames”) for a cash price of US$29.50 per share (the “Acquisition”) • NeoGames is a compelling strategic acquisition for Aristocrat to deliver its online RMG ambitions and comprises four complementary business units •

NeoGames' iLottery business is an industry leading global iLottery full technology PAM providing solutions and services to national and state-regulated lotteries • AspireCore is a leading B2B PAM and managed services provider globally serving 30+ partners with a full suite of products •

Pariplay is a leading aggregator and content provider in the iGaming industry with over 15,000 multiplatform games across a significant network of >140 operators • BtoBet offers a fully customisable sportsbook solution in the attractive Online Sports Betting segment •

Acquisition values NeoGames' fully diluted equity at approximately US$1.0 billion ($1.5 billion) and implies an enterprise value of US$1.2 billion ($1.8 billion)1 and represents a premium of 104% to NeoGames' 3-month volume weighted average price as at 12 May 2023 of US$14.45 •

Represents a valuation multiple of approximately 15x NeoGames' Adjusted EBITDA2 for the twelve months to 31 December 2023

Dear shareholder, 2023 Annual General Meeting On behalf of the Board, I am pleased to invite you to attend the 2023 Annual General Meeting (AGM or Meeting) of Aristocrat Leisure Limited (Company or Aristocrat), which has been scheduled as follows:

Date: Friday, 24 February 2023 Time: 11.00am (Sydney time) Registration opens from 10.00am Venue: Aristocrat Head Office, Building A, Pinnacle Office Park 85 Epping Road, North Ryde New South Wales, 2113