Consensus community valuation

Not following or held, but as a positive signal they have just inflected into EBITDA profitability and expect next Q sales to be stronger than Q1 26

Cash outflows appear to be in an improving trend which they will need positive soon given where the cash balance is at: 1.5M, with another 1M available via debt facility

Had a random thought about Atomos this morning, a former market darling that hit $1.50 in 2021. I was shocked to see its share price under a cent -- representing 99% destruction of capital for shareholders that bought at the peak and hung around.

They recently signed a 13.7m debt facility, through a company associated with one of their directors.

Since 2019, shares outstanding have increased by 172m to 1.2b. The big one though looks like it came in 2023, when it went from 400m to 1.2b in a year -- evidence of how damaging a diluting cash raise can be when the vultures are circling.

Anyone following or know enough about their journey to comment? Where did it go so wrong?

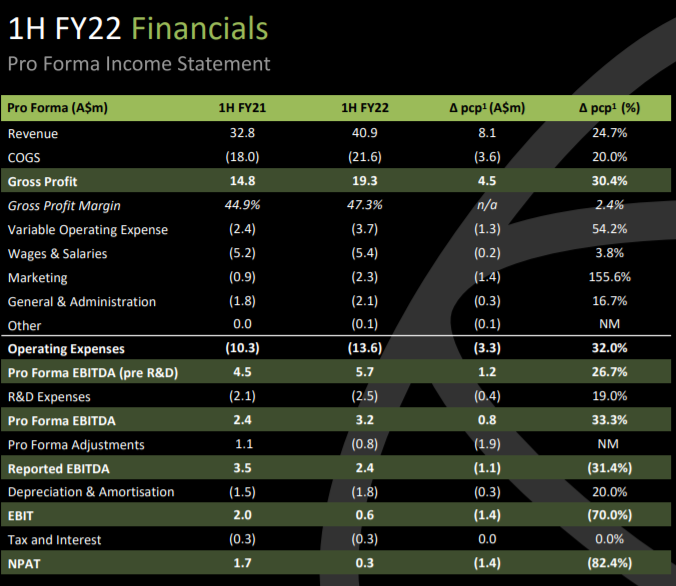

Further to @Rocket6 post about directors resigning you have the announcement below this morning adjusting reported FY22 figures at their auditors request.

It's a significant change too. Although they say it only relates to sales over four days, those four days account for more than 10% of the entire year's revenue (per the 4C). That in itself sounds a bit off. If you were an Atomos bull you might say it gives FY23 a huge free kick, but if you can't trust their accounting you have to start to second guess everything. I do note that the Chairman's letter in the annual report gives a little more detail to what is provided below and Deloitte have given them an unqualified audit opinion (based on the revised figures).

After the poor 2022, I wanted to put some numbers down as benchmarks check against for the next 3-5 years. This is what they want to achieve over next 5 years. Guidance for 2023 is for it to be stronger than FY22 (revenue, margin & earnings) but will skew more to second half.

So from this I am putting some conservative assumptions of 5% revenue growth per year and EBITDA margin increasing from 5.5% (2022) to 18% by 2027. I'm not trying to forecast accuracy here just using it as a thought exercise of different scenarios. I think a PE of 10 is appropriate for the current period before moving back up to 20 as the strategy is executed and FCF is positive again. At a PE of 10 it is pretty fairly valued at the current price of 18c. If the strategy execution is going well then they should be making a NPAT of 6-8m in 2-3 years and probably deserve a PE of 15, which would give them a 57c fair value (discounted back 10% is 41c today). I have a terminal value of $1.30 (55c today) in 2027 if their strategy is successful, and their EBITDA margins is at 18%. To me there is enough upside potential here to remain interested, but it does all hinge on getting back to positive FCF in the next quarter and avoiding a cap raise. If they can do this it might start to look very cheap. I am estimating the probability of a cap raise at <20%.

Atomos FY Results

Atomos ($AMS) reported their results yesterday. It has been a tough year, so to their credit, CEO & CTO Trevor Elbourne and CFO James Cody fronted two investor calls – one yesterday and one today.

As usual, I’ll outline: 1) reported highlights, 2) key insights from the call and 3) my key take-ways. As part of 1) I will add my own summary of “low-lights”. I conclude by stating how I have assessed value, the decision taken and rationale.

1) Reported Highlights

- Record revenue of $82.0m, up 4.3% on pcp (previous corresponding period) with a record Q4 result of $37.5m

- Underlying EBITDA of $4.5m (5.5% of revenue)

- Successfully launched Atomos Cloud Studio and new Series 2 ‘connected’ products in Q4

- Executing on strategy of expanding into connected and cloud products and services

The challenges $AMS has faced this last year are well-discussed here on SM, so I wont repeat. For me, the standout “low-light” was that this business has in one year turned from generating a FCF of almost $8m in FY21 to a result of -$32m in FY22.

To management’s credit, there was a fair amount of air time given to this in the presentation and the Q&A.

Key drivers were:

- Inventory build to mitigate pandemic-induced supply chain issues

- A fall in receipts due to a failed sales and marketing strategy in Q3, reported as quickly rectified in Q4

- Margin reduction and inventory write-offs due to Series I models coming to the end of their life cycle and overstocking of models where demand failed to be realised

- Exceptional staff charges due to “unnecessary” hires

(If, I had my way, I would mandate that firms be obliged to communicate at summary level, the 5 most significant things that went well in the year, and the 5 most significant things that didn’t go well.)

2) Key Insights from the Investor Presentation

Summary, Strategy and Outlook

Trevor began by reminding us of the progress of the company since first sales in 2011 and gave an update of the strategy and the outlook. Slides 8-12 are a very clear summary, so I’ll let them speak for themselves. The big themes are continuing to innovate with new connected products; launch and add services to the Cloud platform; and augment existing sales channels with direct-to-customer sales, including innovative ways for customer to pay for hardware/software bundles.

By 3-5 years they aim to get to an EBITDA margin “towards 20%” getting to “well into the teens” in 2-3 years.

Financial Review

The bottom left-hand chart below shows part of the issue last year – a collapse in sales in Q3, which was reported in June as due to a “change in marketing approach and lower promotional activity”. I’ll come back to this later. The timing could not have been worse, because inventories has been built to mitigate supply chain issues, including shutdowns in China.

The bursting back to life of revenue in Q4, was as a result of promotional activity and discounting – also foreshadowed in June – rapidly getting the new cloud-enabled products into the market.

Upon further discussion, we learned there had also been discounting and write-down of the old Series I models and clearance of discontinued products.

So, in terms of core operational performance is was a perfect storm: big inventory build + sales shock (quickly corrected) + margin reduction due to discounting and clearances. Ouch.

Consumer electronics are generally not super-high margin products, so that explains a horrible change in cash flow fortunes.

But there’s more.

Staffing and Organisation

We were told about “significant further headcount added under previous leadership – largely unwound”. When we dug into this in the Q&A, it was stated that a bunch of senior, highly paid sales and marketing personnel has been added in the USA (by you know who). Once Trevor took over, it was decided that these resources were not needed, so they were let go as part of a larger “right-sizing” of the organisation. All of this then also drives an increase in “professional services.

(So this gave us some insights into what happened under the previous CEO, and I speculate, a wider dislocation in organisation performance as these changes took place. I am trying to be measured with my words here.)

Trevor made clear that there is a strong leadership team in place that has a lot of experience in the company. He himself has been there since the early days, and James has been CFO since 2017. However, they are looking to fill several key roles:

- Chief Commercial Officer (they’ll be running direct sales in parallel with the current channel partners. Trevor believes they won’t cannibalise partners, and having AMS being more involved in direct marketing will build the brand. )

- Chief Product Officer (necessary because Trever has stepped up to CEO)

- Head of Manufacturing and Supply Chain (they are diversifying manufacturing from China by adding Malaysian capability).

Supply Chain

In the Q&A we probed on the current supply chain situation. As we have been told earlier, Trevor confirmed that all key products had been engineered/re-engineered to be made of components that are available and for which suppliers will hold suitable stocks. He is confident that FY23 sales will not be constrained by supply chain.

Cash

As you can tell from other posts on SM, fellow StrawPeople were aghast at the turnaround in the cash position. $5.0m in the kitty at year end, and the $12m debt facility (expanded after the Q3 nightmare) largely drawn. Gulp!

So, on the calls yesterday and today, your faithful fellow Strawpeople asked about the capitalisation of the firm and the need for a capital raise. From the responses on both days, CEO and CFO do not yet see this as necessary. The main reason is that they expect to see a significant improvement in working capital as inventory levels are reduced, and the receivables from the big Q4 sales push are paid.

(In addition to @mushroompanda‘s analysis, I have done some quick and dirty cals, Provided sales continue, if they are able to return the key working capital levers back to the FY21 levels (as a proportion of revenue), I could see them getting to a cash position of $10-$15m by the end of 1Q23. My analysis is very rough, and I haven’t assessed the risks around this. But if the ship is steadied, a highly dilutive raise should be able to be avoided. So, I will give Trevor and Cody the benefit of the doubt. In fact, Cody stated on both days that the cash position has improved since YE22.

3) My Key Takeaways

I’ll be brief. In my opinion, FY22 is a case study of how quickly fortunes can change when there is a macro-shock combined with leadership misalignment/discontinuity. I’ll leave it at that.

I don’t doubt that the products are great and that customers are going to value enhanced connectivity and functionality enabled via the cloud. At its heart, a core capability of $AMS is product development and delivery. But businesses need much more than that, as we have learned.

The direct-to-customer strategy is unproven, and the vacancy of Chief Commercial Office is a key gap. (I’m not convinced the S&M resources hired in the USA were “unnecessary”. But there are several reasons why they might have been classified so.)

It is certainly a comfort, given everything that has happened, that we have continuity in Trevor and James.

The overstocking and write-downs were perhaps a necessary risk given the information available when key decisions were made in their height of the pandemic. I am not going to be a hindsight hero.

However, the investment thesis has changed, the story revealed today highlights a range of risks going forward. The trials and tribulations of the last 12 months raise real questions in my mind as to whether $AMS has the capability to execute its refined strategy.

What do I value AMS at?

Tough to do this, so I’ll keep it simple. If we assume ongoing revenue growth of 25% p.a. out to YE 2026, and that EBITDA margin at that time is 20%. I assue some share dilution to 250M SOI. Then using two methods, discounted back to today at 10% discount rate I get.

- Use revenue multiples of 1 and 1.5, reasonable for the sector: $0.55 to $0.82 / share.

- Using EV/2026EBITDA of 7 (again reasonable for the sector), I get $0.77.

But these valuations assume success in implementing the strategy. There has to be a reasonable chance they fall short, so I can't value $AMS today at much more than $0.40 - $0.50/share.

Limitation - I haven't assessed the upside. But even trying to be objective, I can't bring myself to do this today.

In RL, with the SP dropped, I was reduced to a 1.5% holding in $AMS. The paper loss hurts, but this risk profile around the above valuation is too high.

Personal Lesson learned: $AMS was way too high risk to hold a 4.5% position, even though this had run up from an initial investment of 2.0%. And when the short-lived CEO exited, I should then have re-assessed risk and reward. I didn't. I paid for it. But, on a positive note, my maximum position sizing "policy" for high risk firms saved my bacon and I live to fight another day.

Decision: Sell 50% of $AMS holding (Executed). Hold at 0.75%

Update 10/08/2022

Recent announcement that Trevor Elbourne will take over the CEO role permanently and there was an update last month in regards to FY22 sales.

Management expecting around $82m of Revenue which is at the lower end of updated guidance given in May. EBITDA also expected at the lower end of guidance so around 6%.

Q4 saw a huge turnaround after the previous CEO left (may be a reason for her departure) and I expect that this may lead to some good momentum heading into FY23.

Will update valuation based on 20x EBITDA but waiting on full year results and potential guidance for further updates.

Update 07/05/2022

Lo and behold management have downgraded guidance 2 weeks after reiterating them when the CEO left. Guidance is now at $80-90m Rev and 6-8% EBITDA so taking the low end ($80m and 6%) EBITDA should equate to around 4.8m. Almost exactly double of their 1H FY22 results. I was expecting quite a strong 2H as is usually season with this business but obviously with the latest update this is not going to happen. If I just do a simple double of 1H results then NPAT will be around $0.6m which is well below their FY21 results of $4.2m.

Hard to value this on a PE basis given this update so I'm just going to update and give them a P/S of 1x. Conviction is very thin at the moment.. Looking more like a sell at this point with June 30 coming up..

EDIT: 18/02/2022

Revisiting my valuation post their 1H FY22 results.

Management have still guided for 12-15% EBITDA from 95m+ which is around $11.4m at the low end of guidance. This means that they are expecting quite a strong 2H FY22. This is assuming that they are stating that this EBITDA figure is at least the "Pro Forma EBITDA" before they take off $1m for Videogram expenses. If this figure is "pre R&D" then they'll actually have made less EBITDA than FY21 ($13.2m). Given these assumptions, I may have underestimated their Depreciation and Amortisation and Tax and Interest and so NPAT may come in around $5.6m.

I'm going to be a bit more conservative and give them a PE of 40 which would alter the valuation to around $1.

Original Valuation

Management have guided for $95m+ of revenue and EBIDTA margins of 12-15%. If we take the low end of guidance then EBIDTA will come in at around $11.4m.

Subtract $1m for opex costs from their investment in Videogram and assuming stable depreciation, amortisation, tax and interest will give an NPAT of around $6m representing around 25% growth compared to FY21. See table below for their FY21 results.

A P/E of 50 is not unreasonable if they can continue to grow at 25% CAGR which results in a valuation of $1.35.

Disc: Held IRL and on Strawman.

Spot the effect of a poor CEO - Estelle started as CEO at the start of Q2 (Sep 21) and was terminated mid April 22. On these numbers its safe to say that the new sales strategy she implemented was not working. The 80% decline in sales during quarter 3 was a lot more than I was expecting, especially given the board was still reitirating the old guidance at this time. Was Estelle keeping them in the dark or were they asleep at the wheel? I guess its good that the sales numbers support that it was a leadership/strategy/ execution problem rather than a broader strucutal product quality/demand type problem.

It is also positive that they were able to move the inventory stockpile that they had built up during quarter 4, but i was hoping their margin guidance would have been for the high rather than the low end of the 6-8% range. Still happy to hold my existing stock and monitor the recovery. I was thinking it was looking very cheap at 20c, but I am wanting to see further positives regarding continued sales momentum and margin re-expansion back to the 12% range, before I am willing to chase this rally and add to my positions.

Below is a Black Magic add in the latest New Scientist promoting a multi device streaming product. Thought this was an interesting avenue to advertise, I’m unaware how widespread the marketing campaign is, but the direct marketing makes sense given the online collaborations that now take place across all industries.

There are companies in the US also chasing the multiple cameras, streaming options, as is Atomos. Impossible to say at this point who will succeed, but my gut feel is the simplest option will win. The customers looking to use this type of product are not professional operators, they may not even be particularly tech savvy, so it simply needs to connect easily and work. (Easier said than done)

What I find interesting is Black Magic used to be a different product range to Atomos. However now both companies are now developing similar products, with hardware recorders and now multi streaming device options.