https://wcsecure.weblink.com.au/pdf/ARU/02926853.pdf

My thoughts:

- This will be the first of the off take announcments to come in the next few weeks. They seem to be starting small and will build up?

- The terms are very very good for ARU. We have the Option to sell to Traxys. This shows the demand for ex-china NdPr.

- Also the CP for 31 Dec 2028 lets us know that construciton will be complete by then, and that means the FID will be beofre June 2025.

I'm super pumped for this. This is my largest holding ever. It has been a difficult hold. But as they say in mining, Finance It And They Will Come. Do they say that?

I can see the SP moving up with every annoucment now. There has been movement up in the last week. So we have a leaky ship. With so many particpants in this deal...always likely to be some leakage.

TIme to jump on the ARU rare earth rocket ship!

That being said....i would imagine the SP will only go to about 30-40 cents in the short term.

But as said in previous posts....lots of other macro issues will push this higher int he medium term too:

- Tariffs

- China bans

- War

- new demand form robotics and chanigng asset use in military (i will do a post on this later...).

Ask any questions you want. I'm happy to answer these.

I have gone back and tested all the assumptions based on the last year or so of updates. Usual caveats….DYOR…I may have modelling errors…etc.

My key takeaway….ARU is not priced correctly at its current 13 cents. Maybe this is the market’s discount for not being fully funded yet and/or bit of market manipulation.

Here are the assumptions used in my model:

Here are the results of different NdPr prices and dilutions for Phase 1 (4,400) and Phase 2 (11,000).

Some points to make:

1 - Diluted to the Max - If ARU management had of raised when the SP was $0.70, exisiting shareholders would have been MASSIVELY in a better position than we are today. I think this borders on negligence because the board knew that ECE Nolans were going to sell on the market (creating downward momentum), short position was clearly going up, they knew the timelines of the finance etc. etc. It looks like we will be adding about 3-7 billion new shares to lock in the Final Equity Raise.

2 - Phase 2 is where it is at - It is clear we have a ‘gold plated’ project here. The cost is massive and we have contingency upon contingency. I understand that to reach finance on what the market perceives to be a risky project, they required all this gold plating and contingencies. But if management are up to the task, and can deliver Nolans and barely touch these contingencies, then combined with some of the first year ‘profits’ Phase 2 should be able to be built without raising more capital. If management can achieve that, I may forgive them for the failure in point 1 above. And this also does not factor in additional supply from other sources. So these SP’s are a lower bound.

3 - NdPr pricing is sensitive - Given everything that is going on with Trump and the rest of the world, NdPr pricing should go up, but by how much. My previous ex-china supply deficit modelling showed massive demand from 2026. This is a hard one to predict. But you want some skin in the ex-china NdPr game…..because the modelling shows the valuation is very sensitive to it.

4 - There is still value left!!! - From today's SP of 13 cents.....upon FID...my most likely scenario (in Yellow Box) will x2 your money. If you wait for Phase 2 (in Orange Box) (probably in around 2-3 years) will x7 your money. (obviously lots and lots of assumptions etc. etc.)

The analysis above is just looking at fair value using Net Present Valuation method. If the market was rational, it would be priced somewhere close to the above prices.

But there are some other tail winds that may cause SP to go up even more than the above:

- There will be a bunch of funds that were involved with the equity raise, that missed out, and would likely buy on the market (ie they have done the due diligence…and know what a great project it will be and happy to buy in a little above - or at least will provide a back stop if it drops).

- There will be lots of funds, institutions, family offices and retail that will not invest in a mine until it is fully funded.

- All the tariff talk is not only getting stronger, it is happening. This will be a wake up call to China and the west. None of this is factored into our SP.

- Once ARU achieve FID, watch all the other NdPr juniors out there contact ARU management to discuss processing. Expect lots of announcements around this.

- Also watch the phosphoric acid, and if we lock in much better terms due to ARU being pretty much the only unassigned ex China product!

Once FID is achieved, ARU will be the first NdPr mine (at scale) to begin construction since Lynas around 2010. That is 15 years ago. Back in 2010, NdPr demand was about 30,000 tpa. Today it is about 75,000 tpa and expected to double to about 150,000 tpa by 2035. ARU in phase one is only producing 4,400 tpa. Where is all the ex-china supply going to come from?

I'm back! Had alot of things on my plate (good things). And now I have a bit of free time again.

Alot has been going on with ARU.

First thing is the cap raise....very disappointing....and it has pushed the SP down to 16 cents. I imagine it will stay there until Sept when the raise is complete.

Second thing is the Final Cap Raise. The US $793 million. I met with the CEO a week ago and had provided questions beforehand. The meeting was a bit of complaints session from some retail holders which the CEO and CFO tried to deal with in a constructive manner. I had to jump in and talk about the future and what the Offer Price will be for the Final Cap Raise.

I told them that if they raise at 20 cents....that will erode all shareholder value in the short term. The CFO acknowledged this and said "the cornerstone equity investors can see past the current share prices". So that gave me some comfort that the raise will at least be above 20 cents. (i had originally thought the raise would be at about 40 cents...i'll explain why below).

I also asked if they had explored cash injetions from the Federal Australian Govt or the USA Dept of Defence? They didn't fill me with confidence. Kim Beezley has been saying that for global defence, the best way for the Govt to spend tax payer dollars...is to spend it on Rare Earths in Aust to help our global partners....rather than Aust. buying a new war ship etc. Here is the link:

He said $3-4 billion should be given to the Australian rare earth sector. He also said that China subsidies its rare earths and weaponises it by selling it below cost.

So....Right now....if they are to raise at 20 cents...this means a dilution of 74%.

The following tables model the likely diluted SP for different NdPr prices.

First tabe is for the current design of the processing plant for 4,400 t/pa.

Second table if for the proposed processing plant with the additonal NdPr of 11,000 t/pa.

Ok....so as you can see....if they raise at 20 cents....the SP should stay at 20 cents. However, some points to note:

- I think they will raise at around 25-35 cents. So that should see the SP move up a bit to about 30 cents (diluted).

- I think there will be a bunch of funds that miss out on the raise and will buy on market. They will have done all the due diligence...and can see it is a great long term investment.

- I think there will be some other funds, that have not been in the Final Cap Raise process, that will want to buy in and have not been able to because FID was not yet achieved. ie the rules of their fund prevents them investing in unfinanced miners (junior miners).

- We could then be near the $2 billion mark...and entry into the ASX200...which means some more ETF momentum.

- I also just think lots of people have thought for a very long time, a rare earth miner in Australia, will never get going...so with FID that may give them confidence.

But I'm not real happy with the way this is likely to turn out in the short term.

My short term play for ARU will only just break even for me or a small profit upon FID. I have been trying to work out where it has gone wrong. The amount of equity and debt to be raised is WAY more than the capex. The cost to build is about US $1 billion.....and we will be raising about US 1.5 billion. That extra US $500 million is for cost overruns!!! So when I did my modelling....it was always on a much smaller project cost and thus a smaller debt/equity amount of finance. And thus a much smaller dilution...and thus a better dilluted SP for us.

I spoke to the CEO about this....and his reply was interesting. First he said they had learnt from Lynas, and wanted a large buffer so they don't have to go back to the market and it was something the debt providers wanted. I did say that they have had 20 years to get the design right for the processing plant and hundreds of millions spent refining the design and pilot plants. So maybe this is over kill? He then replied and said, the money not used in these contingencies (US $500 million) and the cash flows from Phase 1....will then be spent on Phase 2 which will take ARU from 4,400 to 11,000 tonnes per annum! And his message to the market is, don't wait for a 'Phase 2 Cap Raise'....

So what does this all mean?

- Short term (and when FID is annoucned...likely Oct/Nov 2024), ARU fair value SP (diluted) is about 30 cents. Currently it is 16 cents. So if you invest now...should be able to double your money. The only risk is if it gets delayed by things like global down turn etc. Don't forget the Aust Federal Government has put in over $700 million in debt and guarentees. So they will make sure this goes ahead. I also think some FOMO from retail and funds will push it up a bit more.

- Long term (2-4 years) ARU will hopefully say, "hey...phase 2 is going ahead...and we have lots of room in our contingency for Phase 1 to build Phase 2". So bascially you can x3 the revenue for no additional capital. Once the market hears or thinks this....the SP is IMHO should be valued at about 83 cents (diluted).

- And this is what makes ARU intersting...the ex-Cina NdPr price is likley to go up substaintially AND there are lots of other Australian Rare Earth players already talking to ARU to process their Rare Earths. This magnifies the value of ARU and in time the SP.

Conclusion:

- Short term the likely dilution has screwed my modelled short term (ie upon FID) investment returns. Although I will be at about breakeven or small return.

- Long term, the current SP does not factor in the likely Phase 2 revenues for (almost) no additonal capex. Which should see a large SP increase up to about $1.55 (or a ten bagger from current SP of 16 cents).

- So my strategy from here is to HOLD and monitor the capex spend after FID. Phase 2 report should be completed about 6 months after FID which will have the estimted capex required. I have had a look at the modelled Phase 1 cash flows and the contingencies...and it is likley to be achievable.

Quarterly:

https://wcsecure.weblink.com.au/pdf/ARU/02830474.pdf

Debt and Phase 2:

https://wcsecure.weblink.com.au/pdf/ARU/02830241.pdf

Presentation:

https://wcsecure.weblink.com.au/pdf/ARU/02830242.pdf

Great news:

- Debt now all secured.

- Phase 2 could have about 150% more NdPr! For a modest capital outlay. Study being done post FID to determine best path forward. This is def not factored into the SP!

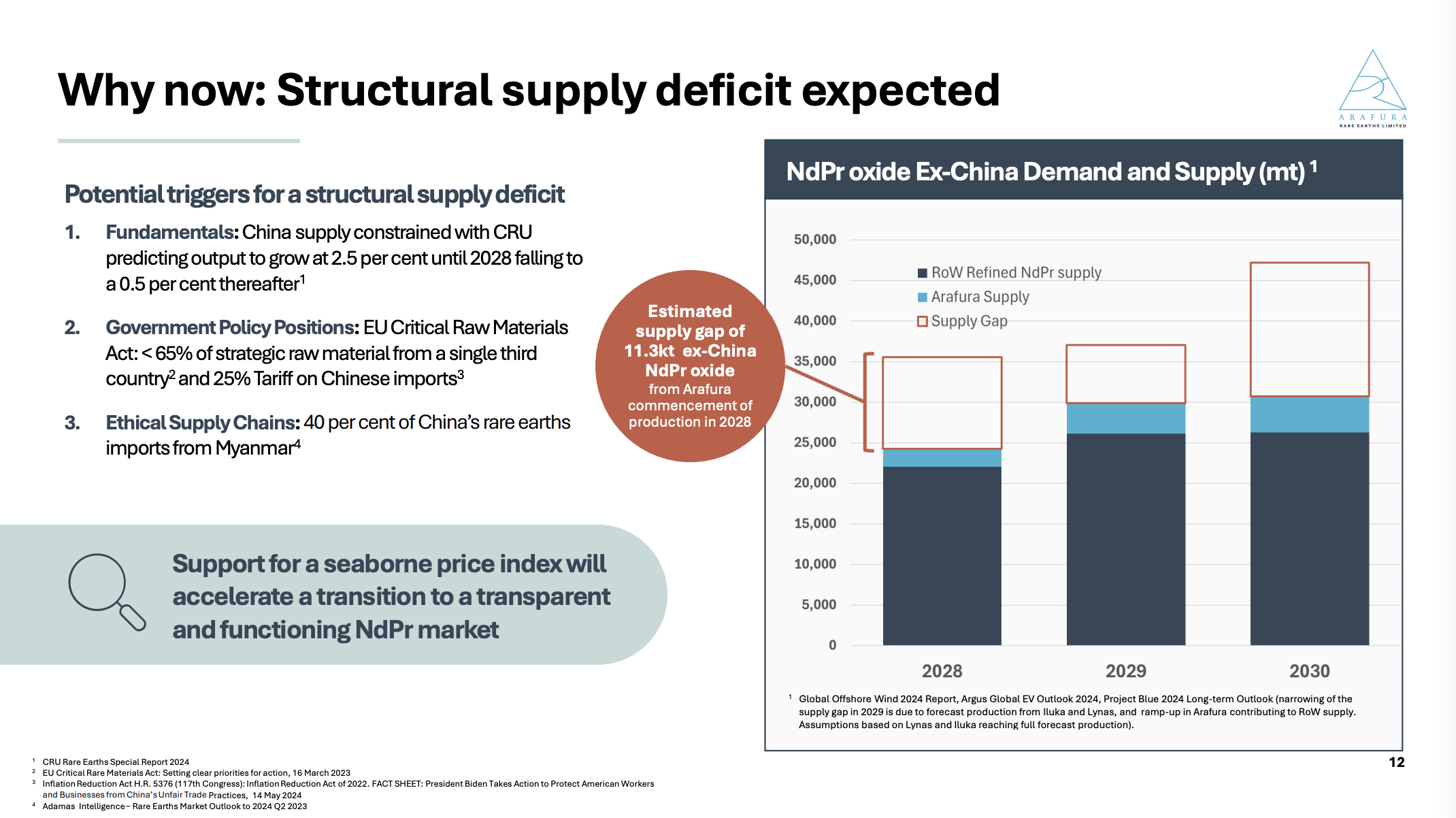

- Thier modelling is a touch less than mine regarding forecasting the impact of Tariffs. They have to be conservative....but this is an amazing graphic. Almost monolopistic.....our 20% of NdPr that we will be selling at spot prices....$$$. Also note the "Support for a seabourne price index......." China controls what prices we see.....the establishment of an ex-China NdPr Market....will show what the real cost is. The is again a decoupling of the market.

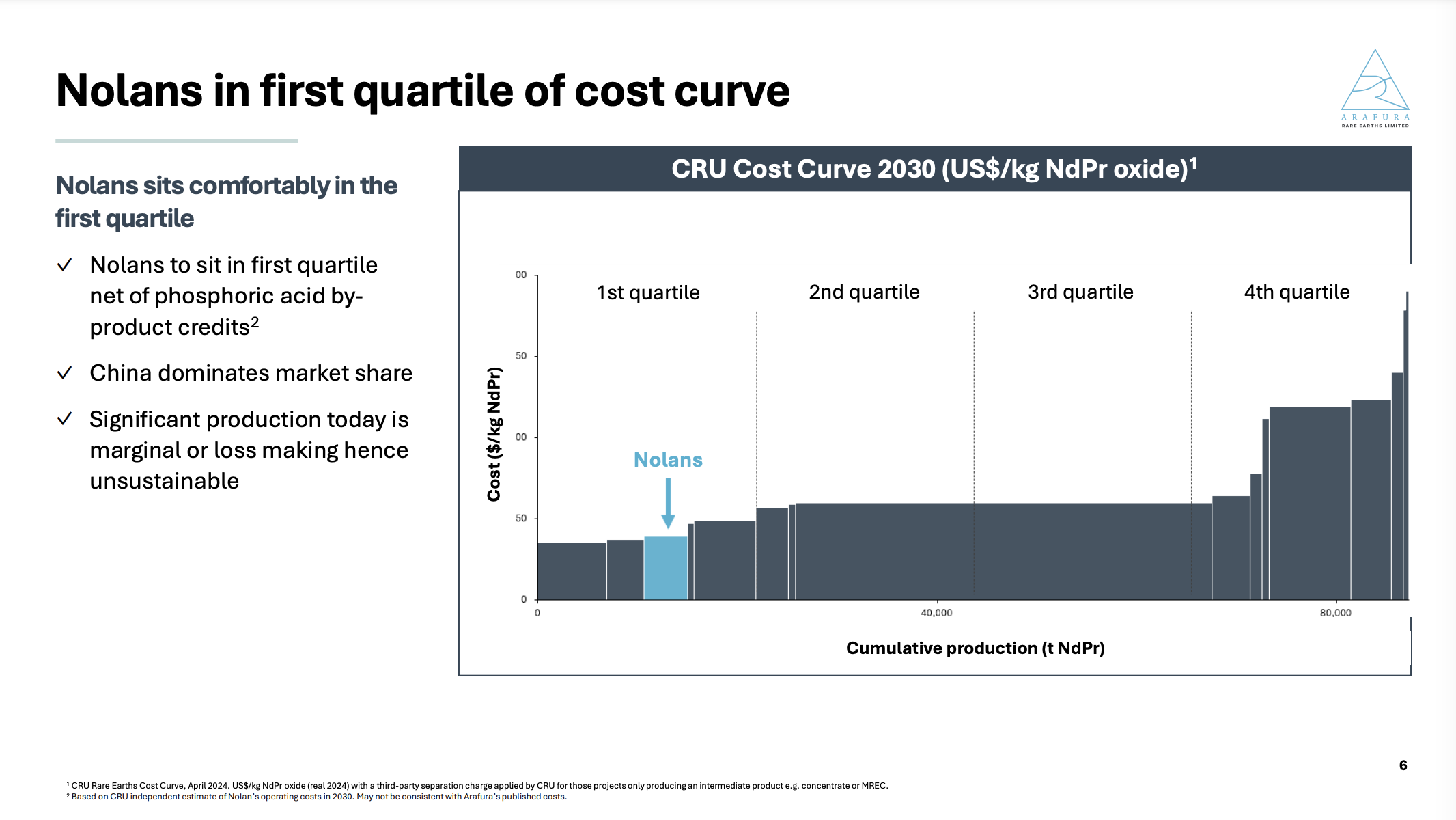

- This next slide is amazing...ARU one of the lowest cost producers. Even at these low prices....still profitable. I'm guessing that big one in the centre is most of China NdPr Production...

I listened to the webcast::

- First takeaway...super exeprienced team. World class. And paid in lots of options....so they are incentivised.

- Capital Raise.....will there be retail SPP....i'm still confused if they will give us a crack. I still think no. Even just the timelines to do a SPP takes about 6-8 weeks. I think they want to get cracking on the construction earlier.

- The rest just really went through the presentations etc.

- But there were some words from the CEO that really stuck in my mind...i can't remember the exact words (waiting for the video to replay)...but there were something like.....ARU will set a precedent in this market....

Anyway...i can't buy any more on Strawman...but I am buying in Real Life (RL). Time to load up! Back that truck up.....

Also there is this video from ARU CEO:

https://www.youtube.com/watch?v=28AC5oaHih8

https://wcsecure.weblink.com.au/pdf/ARU/02824445.pdf

ARU just announced another part of the debt pacakge. This was just the debt guarentee for the commercial loans. But another piece of the puzzle. So the last bit of debt to be locked in is the commercial package (ECA Covered Traches US$175m).

So what do we have to come:

- Commercial debt package US$175m (I expect this early next week)

- Off take agreements (this is unusual...because normally they would announce these before the debt and equity...but debt was apparently so comfortable...they have let ARU keep negotiating better deals). (i expect this late next week)

- Equity package. (i expect this between 15-19 July)

Looking at the trading patterns....someone is still layering the buy and sell to keep the SP where it is. But I have noticed the short position has started to drop (we only have week old data).

Hoping soon...ARU will boom.

So i pulled together this analysis.

Method:

- Align the Share Price movement, Short movement and NdPr Price movement along the same time series.

- Annotate the ASX anoucements.

- And have a good hard look.

Summary:

- To me this shows that the SP does not reflect the true value of the company.

Additonally:

- ARU was able to agree a one month extension to their gas supply contract. This was a CP to the gas contract (ie they had to start supplying by 1 July 2024). Why would they only pick a one month extension? Maybe becasue they are ready for FID?

- A few new people on LinkedIn have 'rejoined' ARU. ARU were constraining costs until FID. So with them coming back onboard now....FID is close?

- On HC one of the guys said they are starting back at Nolans next week. Again hard to know foresure....???

- These are all taken with a grain of salt.....but it adds to the overall picture.

So I have been working on a model to see what the new US EV Tariffs and proposed Euro Tarriffs might do for NdPr demand.

And wow.

I'll put these slides here....and tmrw will put up my modelling approach. But I have got my exPwC friends to review. And they were amazed by the effects...and couldn't find any issues in my model.

It has been a while since I have tried to value ARU. I have rebuilt my NPV model for ARU given the new information to date.

Notes on my model:

- I have used information from the Definitive Feasibility Study (DFS) (7 February 2019) and updated for recent events.

- My model tries to broadly look at the cash flows for 23 years (mine life). It is quite a ‘coarse’ approach but the results are broadly in line with the results of the DFS which would have generated its results from a much more detailed model.

- I’m not a tax specialist, so I have tried to be conservative with the tax assumptions.

- I’m unsure how much Phosphoric Acid is to be sold (ie revenue) and how much is retained to offset the opex costs. This is not clear in the DFS. But even if I am wrong, it is only a small amount in the total revenue <5%.

- I have used a discount rate of 10%. I think this is quite conservative (especially given the Govt backing). But I have kept it at 10% which was also used in the DFS.

- For those of you running your own model, be very careful with currencies and units. Lots of data is provided in Chinese, USA and Aust. And different units like Kg, Tonnes etc.

- It does not factor in the dilution that will happen in the final equity raise.

Key points to note:

⁃ NdPr Pricing - The NdPr price obviously is key to the profitability of ARU and its corresponding Share Price. So to invest in ARU you need to take a view of the future of NdPr pricing. So I note the following on NdPr pricing:

o ARU will have lowest opex cost to produce NdPr. So it will have higher margins but also importantly, if the China tensions disappear (unlikely) it can ride out the troughs of NdPr pricing. Also, there is only so long China can sell NdPr at a loss. Or if they do, it will make western countries nervous. They are backing themselves into a corner with this price suppression strategy.

o ARU has locked in NdPr Pricing in its offtake agreements that are well above current spot market pricing. This means ARU will be profitable in the short term.

o NdPr demand is growing (even with the recent media saying it is not). And there are just no other NdPr projects coming online soon at scale. This will give monopoly type pricing power for ARU for its remaining 15% of supply. And if we can ramp up production, just adds to the profitability.

o The USA (and soon Euro) China tariffs will create large demand. These tariffs could be increased if Trump wins. This is a massive tailwind for NdPr pricing. I’m yet to estimate the impact of these policies. But I would expect it to be quite large. Again….this is NOT factored into my model’s assumptions.

⁃ Additional Revenue - ARU should be able to process other companies’ deposits (Minhub?). This is another revenue stream not factored into the model. We have asked ARU to clarify what it can do in this respect. Also, ARU have stated they will seek approval for Phase 2 for Nolans with much more NdPr below 200m. Either of these events will warrant a rerate of the SP.

⁃ Cost Overrun Risk - Much of the risk for a rare earth project is getting the processing plant working as designed. Lynas had massive issues in the early days. ARU has been on a 20-year journey. So there has been a lot of work done in this space. And the Cost Overrun Facilities provide a good-sized buffer should things not be quite right. So I think this risk has been managed quite well. But something to keep an eye on towards the end of construction and into the ramp up phase.

⁃ Processing Cost Rebate - The 10% government Processing Cost Rebate is great. But if it is removed by the Liberal Party, it will not have a massive impact on ARU.

The ARU Model:

Here is a screen shot of the inputs/outputs from my ARU model:

Conclusions:

- The modelled cashflows show a SP around $1.00-1.50 is realistic.

- NdPr pricing is likely to be strong given the current and prospective geopolitics and commitment of Governments to the energy transition.

- ARU has great potential for additional revenues (more NdPr onsite, additional processing of others, acquisitions).

- Senior management’s incentives aligned with shareholders.

- Strong environmental credentials.

Note - I will also post on Hotcopper.

https://wcsecure.weblink.com.au/pdf/ARU/02784883.pdf

Still digesting the details.

But great result.

The headline figure is a bit decieving. A large chunk of the money is for Cost Overrun Facility Gaurentees (ie if the bank has to increase it's cost overrun facility...then the Export Credit Agency (in this case the Export Finance Australia and Northern Australia Infrastructure Facility) with provide increased guarentees. But the other side of it, means that if there are cost over runs....we have money! So this has de-risked it somewhat. But the way it is presented is confusing. I think Govt wanted to make the largest number possible...so just threw all the numbers into the annoucement. But I still need to fully understand what it means.

This is a quick table i knocked up.

The key thing i'm trying to work out is the size of the major capital raise to happen in a few months time.

If my understanding of the Cost overrun facility is correct....then they need to raise about $640 million (aussie). Which is about what we were told a month ago.

Approx 110 million shares are short for ARU. Approx 5%.

With the Aust Govt funding news coming out, debt funding to be annouced shortly, off takes to be announced and equity.....there is alot of positive news coming. Will be interesting to see if the shorts decided to exit the ARU Rocket Ship in the next few days?

Fingers crossed.

The announcment is that ARU has got another US$75 million from the Korean Credit Export Agency (KEXIM).

With GE stalling on their offtake (due to their turbine division internal issues), ARU will be going to the other major players. ARU will def find another teir 1 off take player. This could change the funding mix. Ie if the other off take player is not german, then they may have to use their Export Credit Agency etc. This has def slowed their Financial Close. But I feel like they should be able to get there by March/April 2024 and with little dilution (ie only a small capital raise). I just hope they don't screw retail investors if they do go down the cap raise.

I have done some modelling of their business with a range of variables. But through all of the scenarios, I had always put in a larger capex (around $1.3 billion when they had about $1 billion in their Definitive Feasability Study.). The additional time lag has meant that inflation has absorbed some of that 'fat' i had put in. But I had also kept constant the operating costs of about $30/kg as opposed to their figure of $25/kg. Again i would assume some of that 'fat' will have been absorbed. I also assumed that it would take three years to be at a decent production (as opposed to their low 2 year figure). The NdPr prices have been steadily increasing again. But China is 100% manipulating the market prices. From the research I have done (and it's hard to get a definitive picture of how the Chinese operate their mines), the Chinese are selling at cost or a bit below cost. And that is at the current NdPr price of around US$60/kg. ARU's break even (at my inflated costs and timelines) will about US$55/kg and will be one of the cheapest rare earth producers AND do it with the best ESG credentials. With lots of companies now keen to spruik their ESG, I think this will make ARU's product highly sought after. And then there are the geopolitcal considerations that can only help ARU.

In summary the fundamentals of the project have not changed. GE stalling on their offtake obviously threw ARU's Financial Close off the timeline. I think we will hear some new off take announcment ealry next year (around mid Feb). And then hoepfully they can close this beast and start building!

I have looked back at how I could have invested in this stock better. And I feel that I entered about the right time except for two things that happened. The first was the chinese selling their stake in ARU on market. I has assumed that Gina or a big Insistution would have bought off market. So that constant selling gave the shorters and manipulators an opportunity. The second part i got wrong was that GE would fall away as an off taker. This has added 6 months to the timeline.

Anyway, good learning.

Parko

PS it is a bit of a ramble....but if anyone is interested, i can present more detail on any of the above or other issues regarding ARU or Energy Transition etc.

This is my first post on Strawman. So please let me know if I have not followed the right process or proforma etc. And please let me know your thoughts on any of the points below. This is just a quick summary of a longer report I wrote for myself a couple of months ago with more graphics from different sources etc.

Why invest in the rare earth mineral sector:

- Governments globally committing to energy transition.

- Hard to pick winners from the manufacture or operation of solar/wind/electric vehicles sectors. However, they all need minerals to be produced.

- All the minerals (Copper, Cobalt, Lithium, Aluminium, Graphite and Rare Earths) will see a large upshift in volume. However, due to substitution effects, many of the minerals will only see modest price increases.

- However, it is hard to substitute Rare Earths because the magnets produced by rare earths are the highest performing, most efficient for motors.

- There is also scarcity of rare earths because there has not been any investment in rare earths for 15 years due to China cornering the rare earth market (85-90%).

- Also it takes significant time for rare earth mines to begin production – typically 16 years from discovery to production.

- Due to geopolitical reasons/reshoring issues, the western world wants rare earths from safe western alliance countries.

Why ARU?

- ARU is the only major/material rare earth company about to begin production (3 years away).

- ARU will be mined and processed near Alice Springs.

- Low geopolitical risk

- Mined and processed with high ESG standards when compared to China. Many companies are looking for ethical mineral supply. This is likely to increase over time.

- Location is near Alice Springs which makes it easier to:

- Attract quality staff (ie close to town with schools etc.)

- Road/Rail infrastructure is close by reducing capex/opex

- Cornerstone investor – Gina Rinehart ($60m at a SP of $0.37 for 10% of ARU).

- Initial Offtakes almost complete:

- Financial Investment Decision due soon.

- Capital Raise completed with establishment works underway.

- Not likely to be another Capital Raise unless there are cost overruns (this would be known around mid 2025).

Valuing ARU - #valuation

ARU’s Definitive Feasibility Study (DFS) used the following assumptions:

- Capex of $1b including contingency

- Opex of US $25.94 /kg (this is considered very low for NdPr globally)

- Mine life of 23 years

- Discount rate of 10%

- NdPr priced at US $ 67 -90 /kg over the life of the mine

- Annual production of 4,357 tonnes

They get an NPV of A $729 million which would equate to a SP of about $0.30 - $0.40. Current SP is about $0.25. Breakeven would mean the NdPr price is around US $55 /kg.

However, if you look at the following NdPr prices and corresponding NPV/SP you can see how sensitive it is (note all approx.).

So we need to look at the long term pricing of NdPr.

Some factors at play:

- The geopolitical two-tier pricing of NdPr will likely mean ARU will get a premium for being ex China supply. Not in the short term because the companies signing up to the initial offtake agreements know they can source their NdPr from China. But in the long term ARU should be able to charge a premium.

- ARU will also get a premium for its strong ESG. Most of China’s supply are from African and Myanmar where health, safety and environmental concerns are largely ignored.

- Energy Transition rate of progress forecast means there is a massive supply gap of NdPr. Currently neodymium has global revenue of approx. $0.5 billion in 2022. And By 2030 this is expected to be $7 billion. This is a x15 increase in 7 years!!!

- Due to the historic lack of investment in rare earths, it will take at least 10 years for the market to bring new mines online into production.

So the current NdPr price of around US $80/kg could be considered low.

Since Strawman asks for a valuation, I believe that in the near term (ie next six month or when Financial Investment Decision/Finance is achieved) ARU should be valued at about $0.70 – 0.90. I think during construction the market will probably get bored…and then the SP could fade. Also there is the risk of cost overruns or delays. So that may also cause downward pressure on the SP. But once production begins and ARU is ramped up….I believe that a SP of around $1.20 is realistic. This would be around 2027.

Key risks

- Key risks are that China will push down rare earth prices. This has happened to the NdPr prices over the last 6 months (US $145 /kg to around US $70 /kg) and is most likely to happen again to try to dissuade investment in new rare earth projects. But geopolitics should create a two tier rare earth market. China/Russia and Western Alliance countries. Western Alliance country rare earths prices should go very high in the next 10 years until other western sources can be brought online.

- Another key risk is if governments decide to slow down the energy transition. This is unlikely, but even if they slow it down, rare earths will be in high demand.

- Substitution is also a risk, but the magnets produced by rare earths are the highest performing, most efficient for motors. There is a cost/benefit calculation when substituting rare earths for less effective alloys (like Elon Musk’s recent comments about Ferrite in their motors). But that price point should be quite high unless they can find a larger/lighter form of battery. Which would be 10-15 years away from commercial viability…if they discovered now.

Other considerations:

- The initial offtake agreements appear to be linked to the China supply prices. So we need to think about what China is likely to do. China is going to need to re-start their economy. And they are likely to invest in projects that decarbonise their industries. Thus the internal NdPr demand is likely to be high.

- China has also previously restricted supply of NdPr to Japan over a dispute. If this were to happen again, then ex China NdPr prices will rise massively.

- Other sources of revenue could also increase revenue such as processing other rare earths for other businesses (lots of Australian mineral sand companies could use this processing plant). There have already been some ARU announcements regarding this. This has not been included in the valuation analysis above.

- Mines have typical investment patterns. I forget the term for it. But right now we are in the down turn waiting for the FID/Financing. There is likely to be a jump in SP when that happens. Management have previously said FID/Finance was to be done by end of June 2023. That came and went. And the SP is getting punished. They have now said second half of 2023. Having worked on large deals with many different sources of funding, I can understand why it is taking a long time. Also they are dealing with Credit Export Agencies from respective countries. There is also another likely down turn before the plant is built and production begins. Especially if there are delays.

Conclusion:

- I think ARU has great potential in the near and long term.

- I think it is currently undervalued.

- I think in the next six months it will move up rapidly from the current $0.25 to around $0.70.

- In the next three years could downward trend before it begins production.

- Then once steady state production is achieved (about 4-5 years from now) it should start producing healthy dividends.

Cheers

Parko