50m-exclusive-german-supply-agreement

This expanded agreement aligns with Bioxyne’s strategy to scaleitsGMP-certified manufacturing and supply platform across regulated international markets. Europe, particularly Germany and the United Kingdom, remains a key focus for growth, supported by increasing patient demand and evolving regulatory frameworks.

The Company continues to leverage its established cannabis platform as a foundation to expand into a broader portfolio of pharmaceutical products and controlled substances.

BXN seems of quietly performed okay here:

Disc: at SM

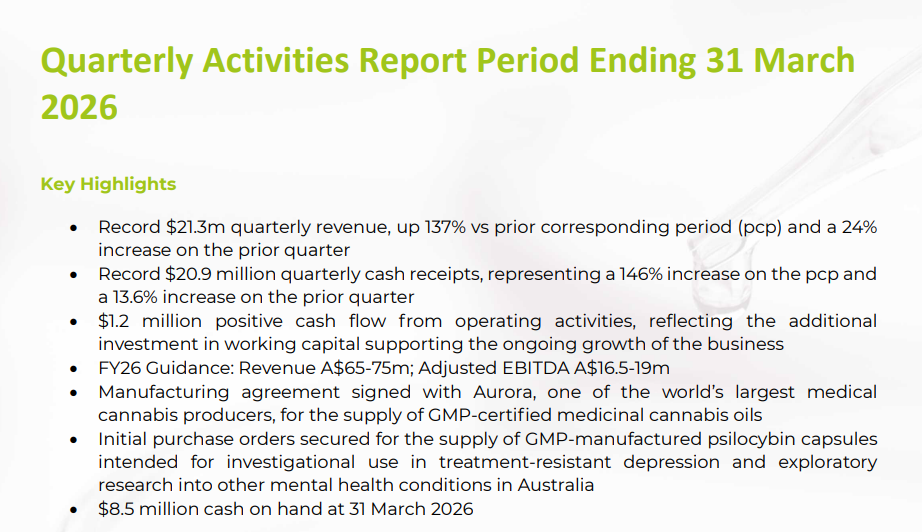

The result was driven by increased demand for the Company's GMP-manufactured medicinal cannabis, MDMA and psilocybin products across key international and domestic markets.

European performance was a strong contributor, with UK and Europe/Germany revenues for the quarter at $2.4 million a 34% increase over the prior quarter.

New high-value contract wins with global partners, initial purchase orders for GMP-manufactured psilocybin capsules (BLSPSIL25), and positive regulatory tailwinds further supported the period's performance.

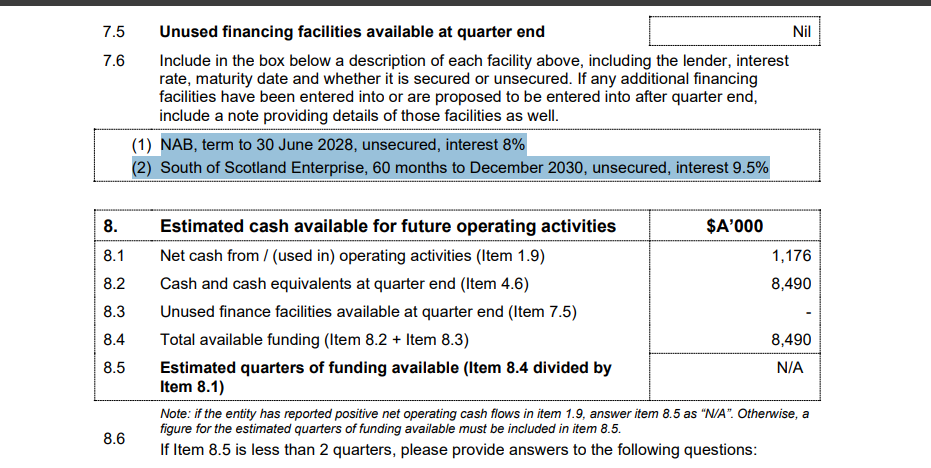

NAB, term to 30 June 2028, unsecured, interest 8% (2) South of Scotland Enterprise, 60 months to December 2030, unsecured, interest 9.5%

Cash available shown below:

Return (inc div) 1yr: 204.00% 3yr: 44.86% pa 5yr: 29.34% pa

Discl: held - SM

Is BXN a Buy at these levels or Bye see u later! - 1 Oct announcement below

Business has cash in bank..

has the USA pharmaceutical restrictions hurt the aspirations here?

BXN trying to put the holders at ease .. i guess .. BXN still bearish Tuesday 7th Oct

Can BXN scale -up the model here?

Outlook The Company is focussed on:

• Growing its manufacturing customer base in Australia, the UK and Europe;

• Substantially exceeding FY25 revenue performance in FY26;

• Gaining EU GMP certification in Czechia for distribution to European markets; and

• Launching its medicinal cannabis products in the UK and European markets with local partners. The Board intends on providing FY26 guidance at the release of the FY25 results next month.

Revenue Group revenue (Figure 1) attributable to significant outperformance from BLS Australia and now enhanced by increased manufacturing capacity. The additional €3.2 million contract with Farmakem and Adrex will underpin growth into FY26. The Company is continuing to negotiate multiple additional contracts in both Australian and overseas markets, which will drive revenue expansion in FY26.

Outlook The Company is focussed on: • Growing its manufacturing customer base in Australia, the UK and Europe; • Substantially exceeding FY25 revenue performance in FY26; • Gaining EU GMP certification in Czechia for distribution to European markets; and • Launching its medicinal cannabis products in the UK and European markets with local partners. The Board intends on providing FY26 guidance at the release of the FY25 results next month.

BXN seems to be delivering. Great for very early holders.

Return (inc div) 1yr: 900.00% 3yr: 43.28% pa 5yr: 30.92% pa

Thursday 24th July:

Last

5.0¢

Change

0.003(6.38%)

Mkt cap

!

$101.7M

BXN has outperformed its growth forecasts over the last 12 months. In 2024 our goal was to become the leading medical cannabis manufacturer.

Micro cap;

'A microcap stock is a public company that has a market capitalization of roughly $50 million to $250 million. Companies with a market capitalization of less than $50 million are typically referred to as nanocap stocks'

Last

4.1¢

Change

0.001(2.50%)

Mkt cap !

$88.75M