Consensus community valuation

Nice numbers from DUG released this morning. My thesis was always this company has valuable IP and a lead on its competitors. In summary, DUG takes undersea seismic surveys and gets significantly more insights from them with it's MP-FWI technology, meaning Oil and Gas explorers have a lot more certainty when they drill for oil. Given it can be a $50m to $100m exercise for an oil and gas explorer, I think that DUG's insights are worth a lot, and hopefully offshore oil companies are starting to come to the same conclusion. DUG was crossing to profitability when I bought it (in 2023) and on that basis the valuation was compelling - that was a few years ago and the price hasn't run up as much as I'd like, but I think the business is doing what I hoped it would. So valuation is still compelling in my view (if you're doing your own calc, and you should - bear in mind it reports in US$, but listed in A$). I was surprised the market didn't rerate DUG in line with the recent jump in oil prices, but that's Mr Market for you. Great to see the lift in HPC revenue, some big investment in that division starting to pay off as well. Still more to play out with this stock and my thesis and I'll continue to hold. Their IP for data centre cooling is pretty interesting too. Held IRL and SM.

Market Cap of $288.42m at price $2.13 per share

DUG Board Bio’s

Francesco (Frank) Sciarrone BCom -Independent Non-Executive Chairman

Over the past 35 years’ Frank has held senior management positions in the banking, funds management and investment advisory industries. Frank is currently the Executive Chairman of Vantage Wealth Pty Ltd and a Director of Biovision Pty Ltd and Biovision 2020 Holdings Pty Ltd. He is the former Chairman of the Fire and Emergency Services Superannuation Board and a former Director of Government Employees Superannuation Board. Frank was appointed to the DUG Board on 23 July 2015 and was appointed Chairman on 1 September 2022 and is also Chairman of the Remuneration and Nomination Committee and a member of the Audit and Risk Committee.

Matthew Lamont Ph.D. -Managing Director

Matt Lamont is the co-founder and Managing Director of DUG. He sets the Company’s strategic direction and remains intimately involved in its research and development and DUG HPC Cloud initiatives. Prior to founding DUG, Matt held senior technical positions at Woodside in Perth and BHP Billiton in Houston. Matt holds a Ph.D. in geophysics from Curtin University, Australia. He is an adjunct Associate Professor at Curtin. Matt was appointed to the DUG board on 5 June 2014.

Louise Bower HBCompt, CA - Independent Non-Executive Director

Louise is the former Chief Financial Officer of DUG and was responsible for global commercial operations including financial planning, management of financial risks, and governance. Prior to joining DUG in 2009 Louise held financial roles in different industry sectors and jurisdictions, including South Africa and the UK. Louise is currently a Non-Executive Director of Babylon Pump & Power Ltd (ASX:BPP) and a Non-Executive Director of Lycopodium Ltd (ASX:LYL). Louise was appointed to the DUG Board on 5 June 2014 and is a member of the Remuneration and Nomination Committee and a member of the Audit and Risk Committee.

Mark Puzey FCA, FAICD, CGEIT - Independent Non-Executive Director

Mark spent 33 years with KPMG where his roles extended across internal and external audit, IT advisory, risk management, governance, strategy and business transformation; focussed on ASX listed companies. Mark was the Asia Pacific IT governance and strategy service line leader, primary partner in Australia providing IT service organisation audit opinions and national leader of product heads (IT advisory). Mark is currently Deputy Chair and Audit & Risk Management Committee Chair of Horizon Power, and Audit & Risk Committee Chair and Non-Executive Director of Sircel Ltd. Mark was appointed to the DUG Board on 9 June 2020 and is Chairman of the Audit and Risk Committee and a member of the Remuneration and Nomination Committee.

David Monk Ph.D. - Independent Non-Executive Director

Dr Monk holds a PhD in Physics from Nottingham University in the UK and served as director of geophysics and as a distinguished advisor at Apache Corporation, until his retirement in October 2019. Dr Monk started his career on seismic crews in West Africa and has subsequently been involved in seismic processing and acquisition in most parts of the world including significant ongoing time in the Middle East. Throughout his career, he has retained an interest in developing innovative ways to acquire, process and utilise seismic data to improve final interpretation. Author of more than 200 technical papers and several patents, he was selected to deliver the SEG’s Distinguished Instructor Short Course (DISC) for 2020. He currently serves as a technical advisor for several geophysical companies including ACTeQ (a seismic survey design software company where he was co-founder) and GTI (a seismic node manufacturer). David was appointed to the DUG board on 18 October 2024.

Announcement from DUG this morning:

My thesis is that DUG has valuable IP and has advantages over its competitors in interpretation - with some interesting side-IP in DugCool and DUG Nomad. I am hoping this is the start of a transition to a SaaS business...

Held IRL & SM

Rich

The chart is in a breakout at . Is this data business worth pursuing or does DUG need to replenish its technology too often!

i think the business looks scalable..

Last

$1.49

Change

0.125(9.19%)

Mkt cap !

$199.9M

I’ve had Dug Technology on my watch list for over a year now.

This business sounds interesting and the share price is starting to look interesting also. It’s still not cheap according to McNivens formula, buts it’s getting close to a buy. I think it just went way over its valuation in 2024. Any thoughts from other Strawfolk on DUG as an investment?

Source: Commsec

What does it do?

“Dug Technology Ltd, a technology company, provides hardware and software solutions for the technology and resource sectors in Australia, the United States, the United Kingdom, Malaysia, and the United Arab Emirates. The company offers high-performance computing as a service solution; data centre cooling solutions; scientific data analysis services; and DUG Insight, a full-service, interactive software platform for advanced seismic data processing and imaging, interpretation, visualization, and QI across land, marine, and ocean-bottom surveys. It also provides data services, including on-demand support for data loading, quality control, and management services.

In addition, the company offers geoscience services, such as seismic and land data processing, DUG deblend, time-lapse and ocean bottom seismic, full waveform inversion, depth, and least-squares imaging, petrophysical processing and interpretation, quantitative interpretation, and regional velocity model services. Dug Technology Ltd was incorporated in 2003 and is headquartered in West Perth, Australia.” (Simply Wall Street).

Analyst Forecasts

Analysts are forecasting DUG to grow earnings at > 30% over the next few years (Simply Wall Street data).

I don’t hold this yet. It’s just starting to look a bit interesting and I’m wondering if anyone has done recent research, or has a view on it before digging deeper?

Not held

Capital Raise In October, DUG successfully completed an institutional placement to raise approximately A$30.0 million3 , at A$1.90 per share, which represents a 12.8% discount to the prevailing share price4 . We were delighted that the placement was strongly supported by both existing shareholders and new investors. The capital raised will be used to accelerate DUG’s growth across three key growth opportunities: o Data centre infrastructure for Elastic MP-FWI Imaging projects.

The capital raising knocked the wind out of DUG!!!

Return (inc div) 1yr: 3.83% 3yr: 33.42% pa 5yr: N/A

DUG chart:

What generation is AMD Genoa?

AMD 4th Generation EPYC™ Processor Platform (Genoa) AMD's “Genoa” microarchitecture is the first to support DDR5 for servers and features world-class performance while being energy efficient to meet the demands of today's data centers.

Overview Comment:

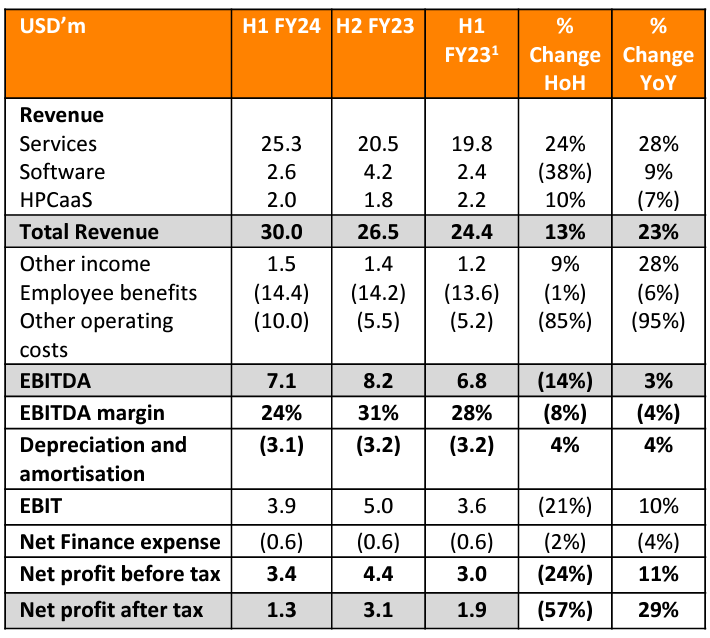

Cash from operations looks good while profitability down. Extra costs throughout the half due to the ordering of new compute and cost of 3rd party compute appear to be temporary issues. Revenues and order book continue to grow as expected so the growth narrative is still there.

General notes:

- A wild swing in the share price throughout the day. Started at $1.80 and closing at $2.44. Price down 4.3% for the day.

- $12.2 of capex in the half (for new compute).

- Financial figures half by half:

Positives:

- Strong revenue growth to $30m. Up 24% HoH or 28% PcP. MP-FWI imaging is gaining momentum and key driver of revenue growth. Record high half for revenue for the company.

- Order book as of end 1HFY24 $40.6m. Up 45% from FY23 end.

- Operating cash flow of $6.2m and expected to strengthen further in H2.

- New compute expected to be available by late April, at this point compute power would have doubled.

- The significant cost of third-party compute compared to DUG's own compute shows their relative efficiency and justification of their business model to complete the compute themselves.

Negatives:

- Still do not have enough compute to meet demand. Started using external compute. This reduced profitability due to the additional cost. Debt levels have increased due to asset financing of new computers.

- Profitability down HoH and PcP.

- HPCaaS still not looking like it will take off as a product.

- New graph showing client relationship length and value. Negative is it showed one client provides around 20% of revenues.

- Cost of construction for Geraldton HPC campus significantly higher than expected.

Has the thesis been broken?

- No, as long as revenue continues to grow and temporary costs such as 3rd party compute can be removed due to DUG getting on top of the compute demand of orders.

Valuation:

- Unchanged at around $2.40-2.50.

What are you expecting and what do you need to see over the next reporting season or generally into the future?

- New compute is able to meet the demand of customers and remove unnecessary extra costs associated with this. I expect higher profitability into the future as a result.

- Start to pay down financing debts as expanded compute meets demand.

- Still watching the CFO revolving door from the past.

- Order book continues to grow. Even after compute starts to meet demand.

- Share price has been on a run. I think it is fairly valued for the growth at $2.40-2.50. Maybe consider trimming at prices above $2.75 unless there is news which justifies a higher valuation.

Note: USD used for all figures except share price.

- New "Multi-Parameter Full Waveform Inversion" (MP-FWI) product had US$11mil of new project awards in the last quarter.

- New project announced. "DUG Nomad" which is a mobile supercomputer installed inside a shipping container. Using the DUG Cool immersion system, the mobile contain can be deployed anywhere for "edge solutions" such as defence, mining and education.

- Generally high tendering activity continues, good outlook.

- Still constrained by computer power and expecting new computers in December.

Trading notes after AGM.

- MD Matt Lamont has sold 2.5mil shares (in wife's name), he still owns around 24 mil shares.

- Wilson asset management has sold down their position to under 5%.

Image from presentation of "DUG Nomad":

Overview Comment:

Very positive results for DUG. Order book is looking very strong already for FY24 so hopefully results can continue to improve from here. Seems like a step change has occurred driven by oil and gas exploration.

General notes:

- NPAT = $4.9m. Slightly below what I hoped but inline with my valuation. However, cash flow was stronger than NPAT.

- Order book at $27.9m. About the same as what it was at during Dec 22. However, in July 23 $18.6m of work was signed.

- Op cash flow seemed very strong but not sure if this was a result of timing?

- Outlook for oil and gas remains strong according to the company.

- Making a $7m investment in the install of new hardware in Houston to support new services projects (this will be asset financed).

Positives:

- Revenue = $50.9m up 51% and 70% in services division.

- My "FCF" = $7.6m.

- Strong operating leverage. Employee and other expenses only rose by $5.6m while revenue grew by about $17.2m.

- July order of work worth $18.6m is a strong start to FY24.

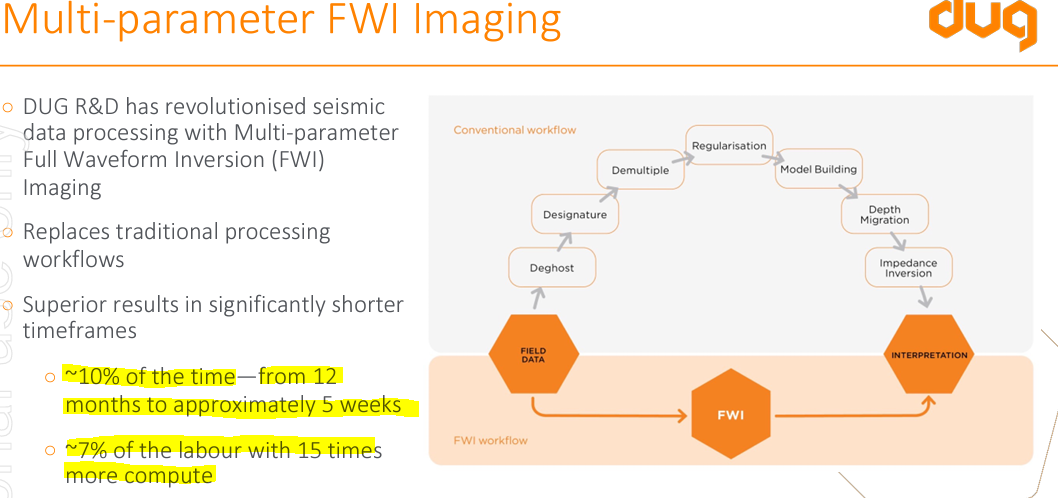

- Turnaround in services is due to expansion into new markets and commercialisations of DUG's "multi-parameter FWI imaging".

- Net cash of $5.2m. Very positive that the company is no longer in debt. Additionally $7.1m cash was received i August due to repayment of a loan funded share plan.

- Market liked the results up 10%.

- Given some numbers in the presentation the FWI product appears to be a leap in magnitude type better product. It can replace traditional processing of imaging of seismic data. The improvement for customers shown below in presentation:

- Multiple examples provided by the company in their presentation of the significant value proposition they provide to their customers. See bottom of post for copied quotes.

Negatives:

- HPCaaS only up 2% to $4.0m of revenue. Clearly not a focus anymore for growth. No sign of the graph of monthly sales again.

Has the thesis been broken?

- No, opposite, all seems to be going well. Starting to see DUG make some real progress and becoming a valuable resource for its customers. Examples of order of magnitude improvements such as FWI will help adoption. Lots of investment in increasing computer side indicators expected growth in compute time which directly relates to revenue, especially given the just in time format of their computer setups.

- Worried about valuation here but all depends on what happens with profitability. The order book as been a very rough guide as to the revenue over the next 6-month period over the previous year. As of end of July this figure is indicting a large improvement in revenue potentially. Given the operating leverage that has appeared in this year's results if things go well DUG will probably look cheap, if not expensive. Adding to position very cautiously.

What are you expecting and what do you need to see over the next reporting season or generally into the future?

- It is clear oil and gas through FWI imaging is a key driver for revenue growth for the business. If oil and gas explorations slows DUG will be impacted.

- If DUG continues to grow revenues rapidly it will be through the continued expansion of FWI.

- Revenues to be above FY23. Order book at the end of FY23 $27.9m with $18.6m added to that in July. Order book as of June 30 22 was only $22.2m.

- Watch the order book numbers. Does it continue to grow?

- Share price has been on a run. All news has been generally positive in recent times. Watch out if some bad news hits, I would expect a pull back.

NOTE: All values in USD unless otherwise specified.

Value proposition quotes in company presentation:

Announcement below... Another recently highly charged tech stock with pretty significant exposure to SVB. I will expect this craters pretty hard on opening.