Consensus community valuation

June 2024: $4.20 price target if copper turns around and rises, however if copper stays down for a while, I'd expect EVN's SP to fall to around $3 - or to settle somewhere between $3 and $3.50. So let's split the difference and call it $3.25.

Two of their mines produce more copper than gold so it pays to understand that Evolution are not a pure gold play any more, they are a gold/copper play and both gold and copper price movements will impact them.

I'm not currently invested in them because while I am bullish on copper longer term, I'm not sure if we;ll see substantially higher copper prices in the shorter term - like this calendar year, so while there will be a time to buy EVN for both copper and gold exposure, I do not personally think that time is now (26-June-2024).

17-Oct-2024: 4 months on and I'm bullish on copper now, and I've always been bullish on gold, with good reason - the gold price hit another all-time high overnight - see here: https://www.miningnews.net/precious-metals/news/4370509/gold-record-territory [17-Oct-2024, i.e. today]

I've bought back into EVN last week in real life and then here @ $4.69 on Monday, as (a) they're back in a strong uptrend on the back of rising prices and a more positive outlook for copper now, and (b) I am personally more positive on the outlook for the copper price to rise from here now that I've done a bit of digging.

Copper is one of the base metals that has so much demand that China has little control over the price - they do manipulate it via hedging and hoarding physical copper (stockpiling for later use), which you can't do with lithium I hear, not for more than 12 months anyway, but China has other methods of controlling lithium prices, mostly via their own in-country production, which seems to be moderating now in terms of some Chinese Lepidolite processors curtailing production finally, after running at losses for a long time.

I have also started to become less bearish on lithium, but that's another story - no direct investments in lithium producers just yet, but RIO's takeover of LTM (Arcadium) is a positive signal, even though I don't rate RIO's record of M&A as being anything better than disastrous. RIO actually buying counter-cyclically for a change (i.e. NOT at the top of the market) is a welcome change, not that I own any RIO directly, and likely never will, but it's good to see both BHP and RIO being a lot smarter in recent years with capital allocation decisions - after burning billions of in prior years on failed takeover attempts as well as completed takeovers where they overpaid at or very close to the top of the market.

But back to Evolution Mining (EVN) - I have NOT liked them in recent years because of their copper production - with two of their mines (Northparkes and Ernest Henry) both being copper-gold mines, rather than gold mines that also produce copper. To be clear, they both produce far more copper than gold, both in dollar value terms and of course in actual material produced. This means they have been hard to compare cleanly with other gold producers who do not use that copper production as byproduct credits to reduce their gold production costs (AISC) like Evolution do - and in fact they claim their AISC for both Northeparkes and Ernest Henry are both negative, i.e. less than $0 per ounce, because of those copper byproduct credits. While that's certainly legal, it tends to be misleading because it reduces their total group AISC (all-in sustaining costs) across their full suite of mines to make them look like low-cost gold producers when their gold mines that do NOT produce more copper than gold are NOT low cost:

- Mt Rawdon (Qld): September quarter AISC - and FY25 YTD AISC: A$2,918/oz

- Mungari (WA): September quarter and FYTD AISC: A$2,674/oz

- Red Lake (in Canada): September quarter and FYTD AISC: A$2,267/oz.

However, with NEGATIVE AISC of A$(1,815) and A$(1,629) for Northparkes and Ernest Henry respectively, due to copper production profits being deducted from gold production costs, Evolution's GROUP AISC ends up making them look like low cost gold producers who can make statements like this:

"On track to deliver guidance of 710,000 - 780,000 ounces of gold and 70,000 - 80,000 tonnes of copper at an AISC of A$1,475 - A$1,575 per ounce."

I've mentioned 5 of their mines there, but they have a sixth one, and it is by far their best gold mine: Cowal, a world-class open pit gold mine located 350km west of Sydney in NSW and operated by Evolution since July 2015. Cowal produced 83,245 ounces of gold in the September quarter (or 333 Koz annualised) at an AISC of A$1,581/oz. Even their lowest cost gold mine and best asset, Cowal, which is damn fine gold mine, no doubt, has costs that are slightly higher than their guidance range for their Group AISC, so hopefully this all explains why many people, including me, see this method of deducting copper profits off gold costs - using the byproduct credits method - to SIGNIFICANTLY lower a company's GROUP costs in terms of gold production, to muddy the waters somewhat and make it hard to do apples v. apples comparisons between EVN and other gold producers. It's easy enough to forgive when a company produces a relatively small amount of copper or other byproducts, but EVN is produces a LOT of copper:

17,561 tonnes of copper in 3 months is more than a "byproduct" of gold production.

"Deceptive" is a strong word, so I won't use it.

So, that's one thing I do not like about EVN - the way they calculate their gold production costs. The other thing is that they do have debt, but they have been reducing that debt at a good clip:

Source (the above AISC numbers and charts/tables): EVN-September-2024-Quarterly-Report.PDF:

So, here's what I DO like (now) about EVN, and why I've bought back in the past week:

- I'm now bullish on both gold AND copper and EVN produce both;

- Rising prices: The gold price keeps making new record highs and the copper outlook and sentiment around copper has certainly improved now;

- Red Lake no longer a basket case: EVN's one asset outside of Australia, Red Lake in Ontario, Canada, seems to be finally coming good: Red Lake produced 37,319 ounces of gold and generated record quarterly operating and net mine cash flow of $67 million and $27 million respectively in the September quarter;

- Jake Klein is probably still Australia's second best gold industry deal maker in terms of buying good assets at good prices when sentiment around gold is poor/weak and then selling EVN's least-best assets for good prices when gold sentiment is strong - Jake used to be #2 behind Bill Beament, but Bill is at DVP now, and doesn't own any producing gold mines (although Develop does have mining services contracts with two Aussie gold miners), so I would say Raleigh Finlayson at Genesis has now taken over that mantle as Aussie Gold's best deal maker and empire builder, although it's still early days at Genesis (GMD) - but I also include in my assesment what Raleigh managed to achieve at Saracen (through to the merger with NST back when Bill Beament ran NST) which was very impressive, so it's now Raleigh at #1 and Jake at #2 - IMO;

- A "major" Aussie gold miner: With US-listed Newmont Corporation - the world's largest gold mining company - acquiring Australia's largest (at the time) gold miner Newcrest Mining last year - Evolution Mining (EVN) has moved up from being Australia's third largest gold producer to now being Australia's second largest gold producer (still behind Northern Star Resources - NST) - and that's just their gold - not even looking at their copper production, which is becoming significant these days - and Australia's best gold producers do have a global reputation for lean operations, i.e. low costs, and superior management - so when money is moving into gold in terms of producers rather than physical bullion, EVN will be in the mix, so will get bought by global fundies and other investors looking for that gold and/or gold/copper exposure;

- Exploration success: They're finding more gold and copper - see their announcement from yesterday: ‘Exploration Success Continues to Unlock Growth Potential across the Portfolio.’ which is important because their existing mines are finite - they don't last forever. During the September quarter the Group spent $12 million on exploration. Ongoing discovery drilling continued at Northparkes, Cowal, Mungari and Ernest Henry, drilling commenced at the Cloncurry North earn-in joint venture and fieldwork was completed on the Lake St Joseph and October greenfields projects in Ontario, Canada; and

- Minimal Hedging: Evolution will continue to benefit from a rising gold price with minimal exposure to gold hedging at 85,000oz over the next two years at A$3,220 per ounce. There is no copper hedging in place.

Here's their September quarter production numbers and cashflow:

That bottom right number is significant - they had just over $1 Billion of total liquidity at Sept 30th, so they're well positioned, despite having some debt. Jake may indulge in some M&A however I would only expect him to do that with distressed assets at firesale prices when we're up here - with A$ gold just topping $4,000/ounce. He's not one to overpay for assets generally speaking - Red Lake being an exception to that rule.

Here's where we're at today with the Aussie and US$ gold prices:

A$ gold prices on the left, and US$ gold prices on the right.

And below we can see that EVN has been lagging behind NST for most of the past year in share price appreciation terms, but they've been catching up lately:

I've added the physical gold bullion GOLD ETF (which is really an ETP - an exchange traded product rather than an exchange traded fund) there for comparison. NST has been ahead of physical gold (i.e. GOLD) all year, however EVN has been underperforming relative to (physical) GOLD since mid-January up until the past few weeks when EVN have spiked up.

The ASX 200 Total Return (or Accumulation) Index (XJO) has produced a circa 18% return over the past 12 months, less than half of what EVN and NST have done in terms of share price appreciation alone.

Both EVN and NST are up over +40% over the past year, with good reason. The gold price has done most of the heavy lifting for them, and now we're seeing improved sentiment around copper impact EVN positively in addition to the improved sentiment around gold miners - i.e. investors now looking more to gaining exposure to gold through miners who own large amounts of gold that is mostly still underground rather than from investing in gold bullion through physical gold bars or gold bullion ETFs/ETPs.

Precious metals seems to be a good place to be at this point, as long as you have decent management and decent assets, located in decent locations.

And in EVN's case, being a gold/copper miner, with two copper/gold mines and another four gold mines, plus some development projects, the improved copper sentiment is turbocharging their recovery.

And that's why I'm raising my target price for EVN today, and disclosing that I'm back on the J. Klein train.

12-Feb-2025: Update:

EVN-Record-H1-FY25-Financial-Performance.PDF

Plus: FY25 Half Year Results Presentation.PDF

Plus: Appendix 4D and FY25 Half Year Financial Report.PDF

Plus: Evolution-Mining-Executive-Leadership-Update.PDF

Two months ago, I highlighted here that EVN were in a solid uptrend:

Well, that has certainly continued, and today's report hasn't done that uptrend any harm at all:

Disclosure: I hold EVN in my SMSF, having bought back in last year. I had previously gone cold on the company because of the increased exposure to copper through their production of more copper than gold (by value) at two of their mines (Ernest Henry and Northparkes), however I'm now more comfortable with that dual exposure to both copper and gold.

Here's some of the highlights from todays first half report:

I note they are using a gold price there (in note 5 above) of A$3,300/oz and the gold price today was over A$4,600/oz, so EVN are being conservative here, and there is clearly plenty of further upside potential in this guidance.

I have typed up a straw today with more info on today's report from EVN. Lots to like.

Above: The only metric that was below the previous half was gearing, i.e. they have reduced their debt, so every single metric improved.

I love the way they break down their costs by minesite (below). Ernest Henry and Northparkes had NEGATIVE AISC (All In Sustaining Costs per ounce of gold produced) due to their copper byproducts, which, as I have previously stated here, distorts their Group AISC number (which is $1,475 to $1,575 per ounce - all amounts are in Australian dollars) and makes them look like low cost gold producers when the reality is that 3 out of 6 of their mines (being Mungari, Red Lake and Mt Rawdon, the bottom three below) have high costs, and in Mt Rawdon's case, VERY high costs ($3,000 to $3,500/ounce).

Cowal is EVN's BEST gold mine by a country mile, and they have reasonable costs of $1,700 to $1,770/ounce, but EVN's overall group cost guidance for all the gold they expect to produce in FY25 is even LOWER than Cowal, even though their other three gold mines (Mungari, Red Lake and Mt Rawdon) have HIGHER costs. The group AISC (costs) are distorted by those negative AISC (costs) at their two copper/gold mines where they use all of the profits from those mines' copper production to offset the gold production costs from those two mines and end up with negative costs because they make more profit from that copper than it costs them to produce the gold from those two mines.

Below is something I'd like to see ALL gold producers (and other miners) do, break down their costs in percentage terms so analysts and us mug punters can see how much underlying price movements in these imputs (electricity, labout, diesel, reagents, etc) might affect EVN's costs. They also show there (below, right) how copper and gold price movements - and volumes produced - affect their cash flows and their costs.

It's a pretty comprehensive report in terms of both what they've achieved and their guidance.

Disc: Holding.

I have raised my PT today; My new 12 month price target for EVN of $7.40, so by end of Feb, 2026.

If copper demand and sentiment increases - as well as gold, they could easily go higher than that.

June 4th, 2025: Updating Price Target

Raising my PT for EVN as they're already over $2 higher than my previous one - or they were yesterday - they dropped -26 cents today. They may have a couple of goes before pushing through $10, but I reckon high $9's, like $9.87 should be a nice target in the short to medium term. It will all depend on the gold price of course. And the copper price as well for EVN as they do produce a lot of copper as well as gold.

I listened to an excellent podcast this evening hosted by Matthew Kidman called SUCCESS and more interesting STUFF, and this episode (#52) was titled: "Jake Klein: The West is ill-prepared for what lies ahead and the gold price reflects this" - well worth a listen for the history of the company (Evolution Mining) and to understand Jake's MO as the company founder and Executive Chairman - soon to be non-executive Chairman (from July 1st) - here's the link to that.

Still holding EVN in my SMSF. It's been a good ride so far!

December 9th, 2025: Updating Price Target (Again):

Raising my PT for EVN once again as they've blown through all of my previous ones.

$14 sounds like a plan.

Still good. Jake Klein now non-executive Chair instead of Executive Chair. Still well run. Still Gold + Copper.

I'm still holding them in my SMSF (4.5% weighting based on their $11.75 closing price yesterday and the market value of my EVN position as a percentage of the total market value of all of my positions across all of my real money portfolios).

Feb 11th, 2026: Raising Price Target (Again):

Raising my PT for EVN once again as they've blown through all of my previous ones.

Bumping my PT up to $17.75 now. EVN reported today, and they reported very well.

Their SP made a new all-time-high of $16.30 today before closing just 2 cents shy of that @ $16.28, being up +8.68% on the day:

It's been a good 12 months for EVN shareholders (I hold them in my SMSF).

$6 to over $16.

Have a look at these results (from today for H1 of FY2026, i.e. the 6 month period that ended 31 Dec 2025):

Note that while it shows positive figures for AISC (costs, 4%) and Gearing (74%) and Net debt (72%), those are all improvements, not increases, so compared to the p.c.p. (H1 of FY25) EVN had 4% lower costs (AISC), 74% lower gearing, and 72% lower net debt in H1 of FY26.

Their gold costs (All-In Sustaining Costs or AISC) is/are now below $1,500/oz, which is industry leading in terms of being the lowest cost producer on the ASX, and while I know they use copper byproduct credits to achieve that low AISC for their gold production, it's still impressive that they were already the lowest in the industry and they managed to reduce those costs even further while other goldies' costs are rising.

Their net debt on December 31st had reduced to just $362 million, down from $1,293 million ($1.3 billion) one year before (31-Dec-24). $362 million not a lot of debt at all for an ASX50 company with a market capitalisation of over $30 Billion.

They should be in a net cash (zero net debt) position by late Feb (this month) or early March (next month) based on their average monthly debt reduction of $155 million over that six month period (they reduced their debt by $931 million during the half) and the gold price being higher now as well.

Lots of records set in the half:

Disc: Held. Current weighting: 5.37%, now my third largest gold producer position, with only BC8 (5.85%) and CYL (5.76%) being larger.

I hold positions in three other non-gold-producing companies that are larger than my EVN position (GNG, LYL and ARB). So EVN is currently the 6th largest position of the 27 companies I hold overall across my 4 real money portfolios (although EVN is not held by me here on SM). I only hold EVN in my SMSF.

11-Feb-2026: EVN-FY26-Half-Year-Financial-Results-and-Interim-Dividend.PDF

See also: EVN-Growth-Projects-Approved-to-Deliver-Higher-Returns.PDF

Plus (also released today): EVN-Unlocking-value-at-Northparkes-for-Evolution-and-Triple-Flag.PDF

As expected, not engaging in M&A in a high gold price environment (not buying anything), but instead being focused on keeping costs controlled and printing cash. And LOTS of cash. Evolution is Australia's second largest gold miner (behind NST) and they're making plenty of hay while the sun is shining.

Their copper production isn't doing them any harm either.

Disclosure: Held. (in my SMSF).

Click anywhere on that image (or here) to watch this interview of Jake Klein by Peter Ker. Jake was the founder of EVN and its Executive Chairman until earlier this year when he transitioned to being the company's non-executive Chairman.

Always worth listening to what Jake has to say if you're interested in gold mining, and/or the rise of China - particularly as it relates to mining and resources in general.

Disclosure: I hold EVN (4.5% weighting).

29th October 2025: The latest MoM podcast is a deep dive by JD into the history of Evolution Mining and how Jake Klein created the company through opportunistic M&A at the start and grew it to become Australia's second largest gold miner, behind NST.

Click anywhere on those images above (or here) to go to their home page and access any of those podcasts.

To go straight to today's one about EVN, click on the image below.

Source: https://www.youtube.com/watch?v=Smoli3gxry0

Disclosure: I hold EVN. 5.3% weighting.

13th August 2025: Not so unlucky for EVN - Pretty Good Numbers, Eh!?!

Source: EVN-Record-FY25-Financial-Performance-and-Final-Dividend.PDF [above and below]

Bear77 Comment: This is what a large Australian gold producer with good management can achieve when the gold price is high and they make excellent capital allocation decisions; mostly through NOT making any acquisitions at high gold prices. One of the best things that Jake and Lawrie did in FY25 was nothing - in terms of M&A - they just made a LOT of hay while the sun was shining - and they didn't spend money except on further exploration of their own tenements and expansions of their own mills.

Jake Klein in August 2018 (7 years ago):

Klein told delegates at Diggers & Dealers that Evolution's modus operandi was building a business that would profit during the good times and the bad times.

"This means a strong focus and discipline on upgrading the asset base by selling lower quality assets in the upturn and acquiring higher quality assets in the downturn," he said.

"It also requires having the courage to swim against the tide - when things are at their darkest for the sector is when you should be growing and when everything seems too good to be true, then maybe it's time to sell assets."

Source: https://www.miningnews.net/precious-metals/news/1344129/gold-companies-scalable-klein

---

In other words, be smart, and engage in counter-cyclical M&A - if you engage in it at all.

---

This year (Feb 2025):

Good deals don’t come along often, particularly in resources. More often, pro-cyclical M&A results in value destruction as peak-cycle commodity prices revert. Cyclicality is an absolute certainty in commodity pricing, and acquired assets are often the subject of massive impairments as soon as the cycle turns – for example Rio Tinto and Alcan.

General exceptions to the rule have been:

- The purchase of Tier-1 assets from motivated sellers requiring urgent balance sheet repair - for example Evolution’s purchase of Ernest Henry from Glencore. To quote Evolution’s Jake Klein, “if you are looking to be successful in M&A don’t find assets, find sellers.”

- The opportunistic purchase of unwanted smaller assets from major producers. Particularly those who have recently completed a major acquisition (e.g. Newmont / Newcrest). Historically, buying assets off major mining companies has been a great strategy for juniors, particularly when assets shake loose as part of a broader consolidation.

Source: https://www.livewiremarkets.com/wires/gold-deal-of-the-decade [Matthew Fist of Firetrail Investments on the opportunity with Greatland Gold, now Greatland Resources, ASX: GGP)

I have also heard Jake asked in interviews this year about M&A and he said the time to buy things is when there are motivated sellers and he doesn't see too many of those around at these gold prices; so the thing to do currently is print cash and bank profits, and reward shareholders.

Jake has taken a step back now from Executive Chair to Non-Executive Chairman of EVN (from July 1st), however Laurie and Jake have always sung from the same hymn sheet, so I don't expect any radical departures from EVN in terms of strategy, especially M&A strategy.

See also: FY25 Full Year Results Presentation

See also: D&D 2025 | Evolution Mining - Lawrie Conway, Managing Director & Chief Executive Officer [Presentation, August 2025]

The market likes EVN's results today (why wouldn't they?!) - however there are some goldies who are up even more than EVN are:

Disclosure: Of the goldies on that list above, I currently hold just two - EVN & GMD - but I also hold others who are not on that list (which is just the top quarter of my Aussie Gold Sector Watchlist in order of share price performance today).

Show Notes:

Our special guest is one of Australia’s most influential mining leaders, Jake Klein, Executive Chair of Evolution Mining.

In this jam packed Finding the Front 50thepisode Jake provides valuable lessons and observations in gold, China and importantly, the future of Australia's mining sector.

A seriously insightful discussion, Jake opens up on his:

- early days in Cape Town and arriving in Australia with $1,000 in his pocket, the major influence of his first job at Macquarie Group,

- views on early China and leading the largest foreign gold miner in China Sino Gold to a $2.2B exit,

- insights into the founding of Lynas Rare Earths Ltd where he was a long term Non-Exec Director,

- his journey over 15 years and the steps to build Evolution into a gold powerhouse - M&A, gold assets (inc. Mt Rawdon, its mine life to now becoming a Pumped Hydro Project for Qld energy), costs, people, gold price and

- the challenges facing the future of the Australian mining sector including the major influence of China.

For those who love mining or are involved in the industry, opportunities like this don’t come along often.

--- end of show notes ---

Source: https://www.youtube.com/watch?v=WYloLJZimJE

Disc: I hold EVN in my SMSF.

03-April-2025: Mungari-Expansion-Project-Commences-Commissioning.PDF

Excerpt:

3 April 2025: Mungari Expansion Project commences commissioning

Evolution Mining Limited (ASX: EVN) is pleased to advise that commissioning of the expanded Mungari mill has commenced, with the project team handing over to the operations team. Commissioning is set to continue through the June quarter.

The project expands the Mungari process plant capacity from 2 million tonnes per annum to 4.2 million tonnes per annum. The mill expansion project has been delivered nine months ahead of the original schedule with the current estimated final cost of $228 million, now 9% under the original $250 million budget. This is an outstanding achievement by the project team.

Completion of the project enables the extension of Mungari’s mine life to at least 2038 and supports the operation’s anticipated transition to an average annual production rate of ~200,000 ounces in the coming years. This represents a 50% increase on current production rates of approximately 135,000 ounces.

Onsite commemorations of the successful completion of construction and start of commissioning are being held onsite today which secures the long-term future of Mungari Operations in the Goldfields regions, Western Australia.

Managing Director and Chief Executive Officer, Lawrie Conway said:

“Today we celebrate the operational handover of a construction project that has been executed safely, efficiently, ahead of the original schedule and under the original budget. This incredible achievement would not have been possible without the collective efforts of our employees, contracting partners including GR Engineering Services Limited (ASX: GNG), NRW Holdings Limited (ASX: NWH), MLG Oz Limited (ASX: MLG) and local stakeholders, for which I am very thankful. It’s a proud moment for all of us and an important milestone for the Mungari Operation, which will now transition back to a major cash contributor for Evolution.

“I am delighted that the Hon. David Michael MLA, Minister for Mines and Petroleum and Goldfields-Esperance, and Ms Ali Kent MLA, Member for Kalgoorlie are both able to join us today to celebrate this significant achievement.”

--- end of excerpt ---

Disclosure: I hold EVN in my SMSF, and I hold GNG and NWH both here on SM and also in my real life portfolios (NWH in both my RL portfolios, and GNG only in the larger one outside of my SMSF because GNG is an ex-ASX300 company and I can only hold ASX300 companies in my SMSF).

It is a real credit to GNG, who were awarded the $153 million contract to expand the Mungari Mill back in late September 2023 (see here: https://www.gres.com.au/news/article/29092023-120/epc-contract-mungari-future-growth-project-process-plant.aspx), and have now completed the project and handed it back to EVN for commissioning approx. 9% UNDER the original budget and 9 MONTHS ahead of the original schedule. Another feather in their cap.

GNG remain the "go to" company for gold mills here in Australia, both greenfields builds (new mills) and brownfields expansions (as in this case, expanding the existing mill from 2 mtpa to 4.2 mtpa). Outside of Australia, fellow Perth-HQ'd engineering company Lycopodium (LYL, who I also hold) win most of those contracts, particularly work in West Africa and other higher risk areas of the world, however GNG are still winning most of the local contracts for this sort of stuff.

Combining the two (GNG + LYL) into a single company would make heaps of sense, but each of them has very high insider ownership - around one third of each company is owned by their management, board members, company founders and their families - so I see that as a high hurdle to get over, as neither company's management would likely be too keen on giving up control of their company to the other company's management team. It could happen, but it would be a tricky deal to negotiate I reckon.

In the meantime both GNG and LYL are doing well by themselves, and I hold both, including here where LYL is my largest position. LYL is also by far my largest position IRL. I do often load up on GNG, but currently I only have about $50K in GNG (over $200K in LYL) because GNG look like they are close to fully valued to me up at $2.90 to $3/share, until they land some more large contracts, whereas LYL look significantly undervalued at below $11/share. They're both going to keep growing and performing well IMO, especially if the gold price stays up around these high levels or rises further, but LYL has greater near and mid term upside from here based on their current share price, IMO.

Both are very good at what they do.

And EVN is a decent company to consider if you want some copper exposure along with your gold exposure. Leaving aside their copper (and they produce quite a bit of copper, particularly from Northparkes and Ernest Henry), their gold production alone makes Evolution Mining (EVN) the second largest Australian gold producer, behind NST.

Below are some images of EVN's Mangari mill:

Further Reading: https://www.abc.net.au/news/2023-06-05/evolution-mining-approves-250-million-expansion-of-mungari-mill/102440912 [05-June-2023]

04-March-2025: EVN released an update concerning their best asset (by a country mile) Cowal in rural NSW on Friday arvo:

28/02/2025: 2:04 pm: Final-regulatory-approval-received-to-extend-Cowal-Operation-to-2042.PDF

Excerpt:

Cowal Gold Operations (Cowal) Open Pit Continuation (OPC) has received Federal Government approval pursuant to the Environment Protection and Biodiversity Conservation Act 1999 (‘EPBC Act’).

This approval marks the final regulatory step required for the continuation of open pit mining following the previously granted NSW State Development Consent in December 2024. It allows for the expansion of open pit mining at Cowal, including the mining of three adjacent ore bodies. The approval is valid to 28 February 2050, reinforcing long-term operational stability.

As all regulatory approvals for the OPC have now been received, approval from the Evolution Board is expected to be sought during the June 2025 quarter.

Managing Director and Chief Executive Officer, Lawrie Conway said: “It is extremely pleasing to receive the final regulatory approval to continue open pit operations at our Cowal Gold Operations. This project has been subject to a robust approvals process, at both a State and Federal level, and we acknowledge the constructive engagement and rigorous input across government to reach this positive outcome. Cowal possesses a significant mineral endowment that will sustain our operations for decades to come and provide lasting benefits for our stakeholders and continue the significant returns generated to date for our shareholders.”

--- end of excerpt ---

Good news for Cowal and EVN.

Disc: Holding, in my SMSF.

Map Source: https://evolutionmining.com.au/cowal/

https://evolutionmining.com.au/storage/2025/01/FY24-Fact-sheet-Cowal.pdf

Water management is key to this one, otherwise it's a gold mine, literally.

Lake Cowal pictured in flood, with the Cowal gold mine next to it, in the NSW Central West. (Supplied: Brad Shephard)

Lake Cowal gold mine expansion approved by federal government

https://www.abc.net.au/news/2025-02-28/lake-cowal-gold-mine-expansion-approved-by-federal-government/104995690 [28-Feb-2025]

In short:

The federal government has approved the Cowal Gold Mine's expansion project in the NSW Central West.

The plans include expanding the mine's main open cut pit, digging three new pits, and extending the lifespan to 2042.

What's next?

Evolution Mining will make a final decision on the project at its board meeting later this year.

ABC Story [28-Feb-2025, link above]:

One of New South Wales' largest gold mines has been given federal approval to expand further into the state's biggest inland lake in the Central West.

Evolution Mining sought approval to extend its main open cut pit further into Lake Cowal, dig three new pits, and lengthen its life span until 2042.

The company estimated the expansion would inject more than $900 million into the state's economy over its lifetime, and produce about 1.6 million ounces of gold, and 1.5 million ounces of silver.

The NSW government signed off on the project in December.

The state government estimated the three new open cut pits would result in an additional $56 million in royalties, and employ a further 64 full-time-equivalent roles during construction.

Evolution Mining's managing director and CEO Lawrie Conway said in a statement that securing federal consent was "extremely pleasing".

"This approval reinforces our original vision for Cowal as a long-life asset that can continue for decades to come," he said.

"This project has been through a robust approvals process … and we acknowledge the constructive engagement and rigorous input across government, together with all our stakeholders, to reach this positive outcome."

A local environmental group has previously raised concerns that the expansion could threaten the lake's bird breeding seasons.

Lake Cowal is a known breeding ground for waterbirds such as the straw-necked ibis. (Supplied Mal Carnegie)

Part of the mine currently covers 132 hectares of the lake's 13,500-hectare size.

The approval means that would expand the mine's operations to about 500 hectares of the lake's footprint.

The disturbance area includes land classified as key fish habitat, and important habitat for migratory bird species.

The company also proposed to extend a protective wall that separates the mine and the lake to more than 6 kilometres in length.

Lake Cowal operations general manager Joe Mammen said in a statement the company would address all environmental requirements attached to the consent.

"We are committed to meeting all approval conditions, including biodiversity protection measures, environmental offsets, and ongoing compliance reporting," he said.

"We look forward to seeing the strong socio-economic benefits it will bring to the Central West region."

A spokesperson for the federal Department of Climate Change, Energy, the Environment and Water said it approved the extension with "strict" conditions to protect important habitats for threatened and migratory species.

The company will make a final decision on the expansion project at its board meeting later this year.

--- ends ---

Bear77 comment: This final approval for Evolution's Cowal gold mine extension is interesting because Cowal is west of Newmont's Cadia gold mine, which is just a hop, skip and a jump away from Regis Resources' (RRL's) McPhillamys Gold Project (see map, below left), which had received "final" development approval before the project got scuttled by Tanya Plibersek, the Federal Minister for the Environment and Water, who made a controversial decision last year that the planned McPhillamys TSF (tailings storage facility, a.k.a. tailings dam) could not be built in the location it had been planned to be built, due to indigenous cultural heritage concerns. According to Regis, the TSF could not be relocated so that decision by Plibersek effectively blocked McPhillamys from proceeding - I understand Regis are in the process of challenging that decision through the courts.

Source: Slide 18 of Cowal site visit presentation 20 June 2024

Here's that Map a bit larger:

My take on this is that it is becoming increasingly hard to get greenfields (new) projects going in eastern Australia, or in NSW more specifically, but much easier to get approvals to expand existing operations.

If you like both gold and copper at this point in time, EVN mine both through a bunch of mines, with two of those (Northparkes and Ernest Henry) producing more copper than gold (in dollar value terms). Cowal is their best gold mine in terms of ounces of gold produced p.a. and lowest costs without using copper byproduct credits.

EVN is the second largest gold producing company on the ASX that is headquartered here in Australia with the ASX as their primary listing, behind Northern Star Resources (NST). So I'm not counting Newmont (NEM.asx) because Newmont is a US company who bought Australia's largest gold miner (at the time), Newcrest Mining, a couple of years back, and while NEM can be traded here on the ASX, those are CDIs for their US shares; Newmont's primary listing is on the New York stock exchange. So I do not include Newmont as an Australian gold mining company, because they aren't.

Just for clarity, EVN do produce a lot of copper, however even if you ignored all of their copper and ONLY looked at their gold production, they would STILL be Australia's second largest gold producer, behind NST.

Disclosure: Holding both EVN & NST (in my SMSF). [and NST here also]

EVN are within spitting distance of their all-time high SP of $6.43 which was set within the past fortnight (on Feb 20th). Below, right, is their 10 year chart:

12-Feb-2025: EVN-Record-H1-FY25-Financial-Performance.PDF

Plus: FY25 Half Year Results Presentation.PDF

Plus: Appendix 4D and FY25 Half Year Financial Report.PDF

Plus: Evolution-Mining-Executive-Leadership-Update.PDF

Two months ago, I highlighted here that EVN were in a solid uptrend:

Well, that has certainly continued, and today's report hasn't done that uptrend any harm at all:

Disclosure: I hold EVN in my SMSF, having bought back in last year. I had previously gone cold on the company because of the increased exposure to copper through their production of more copper than gold (by value) at two of their mines (Ernest Henry and Northparkes), however I'm now more comfortable with that dual exposure - to both copper and gold.

Here's some of today's highlights:

I note they are using a gold price there (in note 5 above) of A$3,300/oz and the gold price today was over A$4,600/oz, so EVN are being conservative here, and there is clearly plenty of further upside potential in this guidance.

And here (below) are some of the more important slides from their presentation today:

Above: The only metric that was below the previous half was gearing, i.e. they have reduced their debt, so every single metric improved.

I love the way they break down their costs by minesite (below). Ernest Henry and Northparkes had NEGATIVE AISC (All In Sustaining Costs per ounce of gold produced) due to copper byproducts, which, as I have previously stated here, distorts their Group AISC number (which is $1,475 to $1,575 per ounce - all amounts are in Australian dollars) and makes them look like low cost gold producers when the reality is that 3 out of 6 of their mines (being Mungari, Red Lake and Mt Rawdon, the bottom three below) have high costs, and in Mt Rawdon's case, VERY high costs ($3,000 to $3,500/ounce).

Cowal is EVN's BEST gold mine by a country mile, and they have reasonable costs of $1,700 to $1,770/ounce, but EVN's overall group cost guidance for all the gold they expect to produce in FY25 is even LOWER than Cowal, even though their other three gold mines (Mungari, Red Lake and Mt Rawdon) have HIGHER costs. The group AISC (costs) are distorted by those negative AISC (costs) at their two copper/gold mines where they use all of the profits from those mines' copper production to offset the gold production costs from those two mines and end up with negative costs because they make more profit from that copper than it costs them to produce the gold from those two mines.

Below is something I'd like to see ALL gold producers (and other miners) do, break down their costs in percentage terms so analysts and us mug punters can see how much underlying price movements in these inputs (electricity, labout, diesel, reagents, etc) might affect EVN's costs. They also show there (below, right) how copper and gold price movements - and volumes produced - affect their cash flows and their costs.

It's a pretty comprehensive report in terms of both what they've achieved and their guidance.

Disc: Holding.

10 December 2024: Regulatory approval granted to extend Cowal Operations to 2042

Evolution Mining Limited (ASX: EVN) (Evolution) has been advised that the NSW Department of Planning, Housing and Infrastructure has reached a determination on the Cowal Gold Operations (Cowal) Open Pit Continuation (OPC) with approval received and Development Consent granted.

This Development Consent is for the continuation of open pit mining with extension of the E42 pit and subsequent development of three new open pits, and continuation of ore processing at a rate of up to 9.8 Mtpa. The mining lease extends to 2045.

Managing Director and Chief Executive Officer, Lawrie Conway, said, “The approval received today is an important milestone for Cowal and our stakeholders. Since acquiring Cowal in 2015, the operation has been a cornerstone asset for Evolution delivering material cash flows and high rates of returns, which will now enable its continuation to at least 2042.

“The extension of operations allows continued contributions to the local and national economies through employment, community advancement, payment of taxes and royalties.

“We acknowledge and thank the NSW Government for their continued support of Evolution and the thorough and rigorous approval process undertaken.”

--- end of excerpt ---

Market Like!

Disclosure: I hold EVN in my SMSF where it is currently my largest position.

I was planning to sell half after Trump won the US presidential election recently based on my bullishness for copper waning in terms of 2025 at least, however I had a change of mind after NST made the $5 Billion bid for De Grey (DEG), as I think EVN could garner more interest from prospective investors and traders in light of that M&A, even though Jake has recently said (on an MoM poddy) that Evolution is not looking to be buying anything at current levels and is focused on making profits right now.

Leaving aside all of the copper EVN produce from Northparkes and Ernest Henry, EVN are still Australia's second largest gold producer, behind Northern Star (NST). And Cowal is by far their best gold mining operation - it's the gift that keeps on giving - now permitted through to 2045 with this announcement claiming they have enough ore to keep it running through until at least 2042, so for at least another 17 years.

And Cowal is here in Australia, in NSW, just a stone's throw from Regis' McPhillamys gold project, which got the rug pulled out from under them in August this year (2024) when Federal Environment and Water Minister Tanya Plibersek made a declaration of protection over part of the approved McPhillamys gold project site to protect a significant Aboriginal heritage site near Blayney, in central west NSW, from being destroyed to build a tailings dam for the gold project.

This came only days after the NSW Supreme Court of Appeal upheld an appeal against the development approval for the Bowdens silver mine project near Mudgee a little north of Cowal and McPhillamys on the basis that the the state's Independent Planning Commission (NSW IPC) failed to consider the impacts of a transmission line when it granted the approval in 2023.

The locals were more concerned with the lead that Bowdens would produce as a byproduct of silver production, so were protesting against the "Bowdens Lead Mine" even though the mine would have been a signifcant silver mine that also produced some lead.

While it might be true that getting approval to build new mines in NSW is a damn sight harder than it used to be, getting approval to expand an existing mine that is already producing seems to be a lot more straightforward.

Below, EVN's Cowal gold mine, now set to keep producing gold until at least 2042:

17-Jan-2024: I hold EVN in my SMSF, but nowhere else, so not here on Strawman.com. I wasn't planning to take part in their SPP, which formed part of the CR for their recent acquisition of 80% of the Northparkes Copper-Gold Mine from CMOC Group Limited, but a few things have changed now. [I'm still not planning to participate despite those changes]

[03-Sep-2024: Note: Not holding EVN now, anywhere]

Firstly - there's this: Extension-of-Share-Purchase-Plan.PDF released on Thursday 11th Jan (last Thursday) which advises that the closing date for the SPP that was announced on 5 December 2023 will be extended from its original closing date of 16 January 2024 (yesterday) to 5.00pm on Tuesday 30 January 2024.

Eligible shareholders participating in the SPP will be able to purchase shares at the lower of:

- A$3.80 per Share, being the same price paid by institutional investors under the Placement announced on 5 December 2023; and

- a 2.5% discount to the 5-day volume-weighted average price of Shares traded on the ASX up to, and including, the revised SPP Closing Date (30 January 2024) (rounded to the nearest cent).

Which is a good thing for EVN shareholders participating in the SPP because they're now likely to be paying a good deal less than $3.80 for those shares now due to today's announcements:

Wednesday 17 January 2024:

Firstly: December-2023-Quarterly-Report-EVN.PDF

Secondly: Exploration-Success-Continues-at-Cowal-and-Ernest-Henry.PDF

The first one did the damage. EVN closed down -65 cps at $3.10, so down -17.33% today.

The market was in no mood for bad news - here's the sector movements today:

Gold sector down -5.27% - that's a BIG move. EVN's selloff would have contributed to that for sure because they are the third largest constituent of that gold sector. They should be the second largest after NST, but the sector still has NEM in it, Newmont Corporation, even though they are listed in the USA and are not an Australian company. Because Newcrest (formerly NCM) WERE Australia's largest gold producer, and Newcrest shareholders were paid in Newmont (NEM) shares when Newmont acquired Newcrest last year, they've (S&P have) decided to keep those NEM CDIs in the Australian gold index.

EVN was the worst of a bad bunch today...

The fact that the majority of our goldies closed substantially lower than the four physical gold ETFs (see above) is a clear sign of seriously negative sentiment across the sector today.

Pantoro (PNR) released the following update last week (on the 8th): December-2023-Quarter-Production-Update-PNR.PDF

And their SP fell -7.55% on the day and then another -6.12% the following day.

Today they released this at 9:33am: Underground-Development-to-Commence-at-Scotia.PDF

And their SP fell another -6.25%. Those that follow PNR (and that would be a small group, because they're a small goldie) were clearly expecting or at least hoping for better, or more, and dumped them when they didn't get what they wanted from those updates. Pantoro finished CY 2023 @ 5.7 cps and they're now (in the middle of January) some -21% lower at 4.5 cps. I have held them in one of my real money portfolios previously and do occasionally have a small trade in them with some loose change here - because of the lack of brokerage fees.

After the market closed, at 4:54pm, they lodged this: Addendum---Underground-Development-to-Commence-at-Scotia.PDF

Meanwhile Evolution Mining (EVN), one of our gold majors, closed at $4.14/share on December 4th, the day before they announced the Northparkes transaction and capital raising, and today they closed at $3.10, which is -25% lower.

Some details from today's update:

- Evolution’s Chief Operating Officer (COO), Bob Fulker has decided to leave the Company to pursue other opportunities. Mr Fulker will finish at the end of March. A search to identify an appropriate replacement is underway.

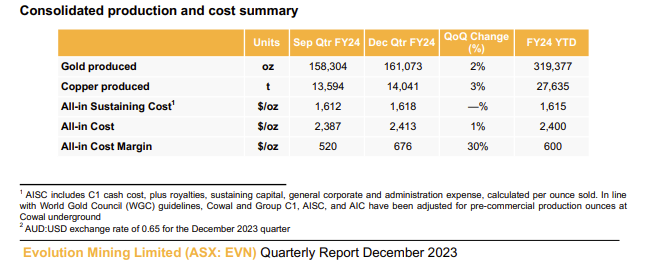

- Gold production for the quarter was 161,073 ounces at an All-in Sustaining Cost (AISC) of $1,618 per ounce (US$1,052/oz) compared to the previous quarter which was very similar:

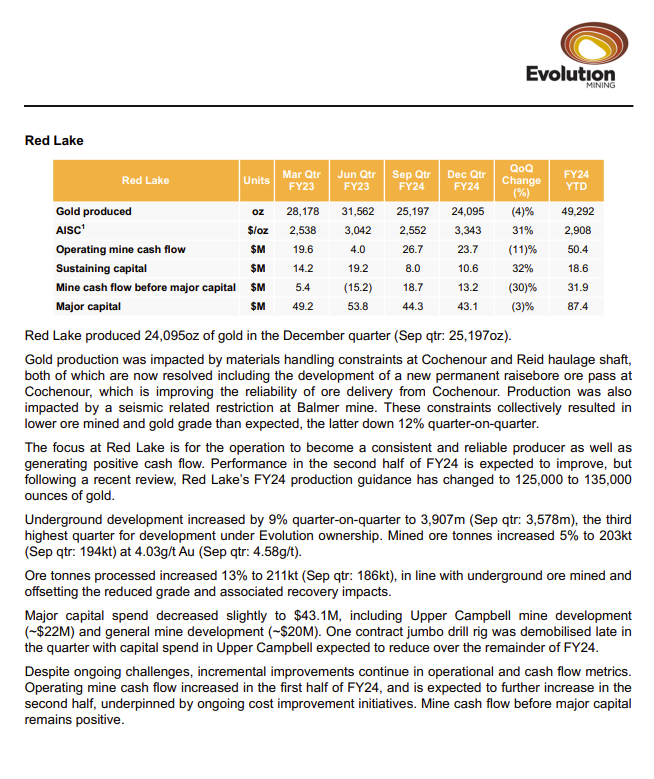

- Despite some positives elsewhere, the market is probably focusing more on the continuing basket case that is Red Lake:

- Evolution Mining's Red Lake underground gold mine in north-western Ontario (Canada) is their only gold mine located outside of Australia (they have 4 gold or copper/gold mines here in Australia - Cowal, Ernest Henry, Mungari and Mt Rawdon, plus their 80% of Northparkes in NSW as well), and Red Lake is certainly their problem child. The update (see above) shows that for the December quarter, their production at Red Lake (gold produced) fell by -4%, their AISC (costs) rose by +31% from A$2,552 to A$3,343/ounce (above the gold price, so Red Lake is losing money), cashflow decreased by -11%, and sustaining capital (which is included in that AISC) increased by +32%. I've included the whole page (above) on Red Lake from today's quarterly report, for some context. That is one acquisition that Jake Klein made that has NOT worked out as planned. Not yet anyway.

Appendix 1 contains their December 2023 quarter and their FYTD (financial-year-to-date) production and cost summaries. Below is page 14, which is the second page of Appendix 1. Page 13 was the production breakdown. Page 14 (below) is the cost breakdown for the December quarter:

The full report can be read here: December-2023-Quarterly-Report-EVN.PDF

You can see there how wide the range is across their minesites for their costs - both AISC and AIC. Their AISC ranges from negative (A$5,677)/ounce at Northparkes up to positive A$3,343/ounce at Red Lake. It is only because of those byproduct credits for copper from Ernest Henry and Northparkes, which both produce far more copper than gold, that EVN manages to get their Group AISC down to A$1,618/ounce. All of their mines also produce Silver, but the silver production is not particularly material, as shown on page 13 (reproduced below).

Cowal, EVN's flagship copper/silver mine in NSW which produces around 45% of all of EVN's annual gold production, is clearly their best asset. Cowal has an AISC of just $1,226/oz after silver byproduct credits and it's a high quality gold mine for sure. And I'm sure Ernest Henry and Northparkes are great copper mines too, that also produce some gold. But looking across the suite of mines that EVN operate, the quality varies greatly, as do the costs.

Source: https://evolutionmining.com.au/cowal/

Cowal is an excellent mine that is expanding with heaps more gold there at good grades, but I believe the market isn't entirely comfortable with how some of EVN's other assets are travelling.

I'm not adding to the EVN position in my super or selling any - it's a long term holding in what was Australia's third largest gold producer when I bought that position a few years ago (@ $2.83/share) - they are now Australia's second largest goldie after Newcrest got taken out by Newmont last year.

But I don't intend to buy any EVN in any of my other portfolios, including the virtual one I have here. Other goldies like NST and GMD look heaps better to me at this point.

------------------

03-Sep-2024: Update: I sold out of EVN earlier this year after deciding I wanted more pure gold exposure rather than gold/copper which you get with EVN with Ernest Henry and Northparkes both being copper mines that also produce gold but being regarded by EVN as gold mines that have a negative ASIC because of the copper "byproduct credits" reducing the cost of gold production to a negative number. When you have your cost of gold being negative because of copper production, i.e. it cost you LESS than nothing to mine the gold, then clearly those are copper mines that also produce gold and should not be regarded as gold mines that also produce copper, but it's legal, and they're doing it. I just find it very misleading in terms of trying to make cost comparisons across the gold industry and including EVN, so I tend to exclude EVN from my gold sector universe now because it's just too hard.

The main problem for me is that if you REMOVE the copper production entirely, EVN is NOT a low cost gold producer. They are ONLY a low cost gold producer because they use their copper sales to reduce their gold production costs.

That said, for people who want exposure to gold AND copper, EVN would likely be a good option to consider. I just don't want that copper exposure right now - I may later, but not now.

EVN's latest report was apparently very good, and the market liked it, especially their bullish outlook, but I'm not interested in them now, so I haven't looked at it in any detail. Their SP closed at $3.81 on the day before they reported (August 13th) and they've traded as high as $4.40 and closed as high as $4.36 during the following fortnight, but they closed at $4.11 yesterday. So a bit of a reality check perhaps.

Their share price may well be driven as much by copper prices and sentiment than gold prices and sentiment now.

[not held]

10-August-2023: Today: Jake Klein joins us to Share the Evolution of the $8b Gold Major - YouTube

Their Show Notes:

"We’re at the end of 3 big days at Diggers, and we’ve got a great interview to share. Please bear with our lower-than-usual production standards because the value of this one is phenomenal."

"Jake Klein, the executive chair of Evolution Mining (EVN), one of Australia’s largest gold miners, came on Money of Mine to share his thoughts with us. We had a great chat about gold, copper, M&A, previous acquisitions, and a bunch more."

"We hope the Money Miners enjoy the discussion!"

Source: https://www.youtube.com/@Moneyofmine

CHAPTERS

0:00 Preview

0:29 Introduction

2:26 Interview with Jake Klein

24:09 Wrap-up

You can click on the time stamp to the left of the "Chapter" title above to go straight to that point.

DISCLAIMER

All Money of Mine episodes are for informational purposes only and may contain forward-looking statements that may not eventuate. The co-hosts are not financial advisers and any views expressed are their opinion only. Please do your own research before making any investment decision or alternatively seek advice from a registered financial professional.

---

I hold EVN shares. They are Australia's third largest ASX-listed gold miner, and after NCM is delisted from the ASX later this year (after the completion of US-based-Newmont's acquisition of Newcrest) - Evolution (EVN) will become Australia's SECOND largest ASX-listed gold miner. Jake Klein is one of the highest profile "thought leaders" in the Aussie gold sector, and is always worth listening to - I feel the same about Bill Beament but Bill is out of gold now and into mining services, although I believe Bill's new company (DVP) will end up owning some mines themselves as well, a business model that could end up being similar to MinRes' (MIN's) business model. I don't think Jake Klein is going anywhere - he's definitely still a gold-bug!

In this interview with the MoM podcast boys at "Diggers" (or D&D) in Kalgoorlie today, Jake discusses Evolution (of course) but also why he's bullish on gold and the gold price from here. This interview was recorded after Jake's D&D Presentation, which by all acoounts was very well received.

EVN also released its Quarterly yesterday.

the headline results are fine:

Production is up a bit (both for gold and copper) and cash flow has improved

Brilliantly, AISC reduced massively. But....

The future of EVN rests on Red Lake, and things there are continuing to go from bad to worse. The only reason the headline figures are any good is because of this:

The AISC from Ernest Henry has created a weirdo -$3748.

I think in a previous post @Bear77 explained the reasoning behind this which has to do with the contract with Glencore for copper sold, when EVN bought the mine. Anyhoo, it is a big masking agent for Red Lake which is not going to plan.

In the report though, there are good reasons why it isn't going to plan just now, but will improve shortly:

And even though this is apparently, entirely normal, expected and nothing to see here:

So, heads have rolled. There have been many quarters of disappointment regarding Red Lake

I have now lost faith in EVN. I think that "the great white hope" of Red Oak is not going to eventuate and will be selling out completely tomorrow.

Bit sad, after nearly 20 years or so of holding EVN from a penny stock.

But..never fall in love with a stock, and always re-assess in the light of new evidence.

05-Sep-2021: This is really a reply to Barney's Business Model/Strategy Straw for EVN. If you like Minelab, they are owned by Codan (CDA) - have a look at their share price graph. I own Codan shares and Evolution Mining Shares. I also own a few other gold stocks, and some gold ETFs, so you could say I'm bullish on gold longer term. However, you have to realise that gold producers are a leveraged play on gold. When the gold price is rising, most quality listed gold producer's share prices will rise by MORE than the gold price rises, and when the gold price falls, particularly if it is in a downtrend, the share prices of most gold producers will fall FURTHER than the gold price in percentage terms. When you invest in a gold producing company, you are investing in what they own (which is primarily gold, albeit most still underground or in pits or in ore stockpiles) and the company's ability to deliver shareholder returns in the form of profits, dividends, and share price increases. Gold companies are generally valued with a good discount off the gold that they own that is still underground, because there is risk associated with them being able to efficiently extract that gold (including getting it to their plant and processing it through their plant) and then sell it while the gold price remains accomodative.

Also, with a lower gold price, lower grades of gold - in terms of ounces per tonne of ore (dirt/rock/whatever it's in) - may not be economic to dig up and process - the cost might be higher than what they will get when they sell the gold - but a higher gold price means that lower grades become worth processing, even though they are going to be costlier to process. For example a company might have an AISC (all-in sustaining cost) for their gold production of $1,200/ounce, however if the gold price rises to A$2,800 (Perth Mint gold price is currently around A$2,450/ounce), the same company might be able to mine additional lower grade ore that might cost $1,500 or $1,800/ounce to process and still make heaps of money. A higher gold price can means that a company can include more of their ore as minable gold. They use a cut-off grade for calculating what they've got, and the higher the gold price, generally the lower the cut-off grade can be.

So what that means is that without anything else happening other than the gold price rising, a gold producing company can get a double positive, in that the gold they were going to mine anyway becomes worth more, and they may also be able to mine and process additional gold that they already know they have but that was previously not economical (cost-effective) to mine.

The same effect works in reverse when the gold price falls substantially. They may have to raise the cut-off grade to remain profitable which may mean they now have less minable gold - i.e. less gold that is cost-effective to mine.

All that said, Evolution Mining is the third largest ASX-listed gold producer (behind Newcrest and Northern Star), and they currently have the best portfolio of mines I think, certainly the cheapest AISC (costs) of the three. Also there have been two star performers in terms of superstar gold company managers in Australia in the past 10 years and Jake Klein at Evolution is one of those. The other is Bill Beament who used to run Northern Star (NST) but has now left to run Venturex (VXR) who are currently focussed on base metals (not precious metals like gold). Jake and Bill have excellent track records of very smart dealmaking, mostly buying quality yet underperforming assets during the gold-price-lows, then turning those assets around and working them hard and smart, and also offloading assets when the gold price is high and prices of gold mines are even higher. With Bill stepping away from the gold industry for the time being, that leaves Jake (at EVN) as the #1 smartest gold mine manager in Australia - in the opinion of most industry participants I would imagine.

If you're going to buy a gold producer, buy them when the share price is at the lower end of their range - and EVN is back to near March 2020 (COVID-19 crash) lows. Also buy a quality gold producer that makes money and has very smart management - and EVN ticks those boxes also.

On page 12 of their recent FY21 Full Year Results presentation, they stated that they have low leverage at less than 0.5x and modest gearing at 15% (net debt to equity ratio) plus no material debt repayments until 2026, followed by some material repayments due in 2029 and 2032. Their average debt maturity is 7 years. I'm not worried about their debt. They also have a lot of cash and a lot of cashflow.

But Barney, if you want to go look for gold yourself, you can't beat a Minelab gold detector, they are the best in the world!