Consensus community valuation

Up 20% today, so a bit of excitement it seems.

The investor day was in person so I missed out but the 51% stake in VIZ for $1.4m and announcement of up to a 10% on market buyback look to be good uses of the rather large cash pile they had building up (~$30m).

The expansion into offering insurance via the “VIZ Tradie Pass” is on brand and strategy as previously guided by management so I can see why investor like it. It shows the TAM expansion strategy is for growth is happening. The company has call and put options to acquire the remained over four tranches based on EBITDA margin targets.

It’s good to see a board use a buy back when the company is clearly under valued buy the market. I expect as owner operators they will use this facility only to extent it remains undervalued.

In terms of the Investor day presentation the improvements in MAA from the Feb update was encouraging:

Compared to 24 Feb presentation:

They have a lot of platform offerings to expand into:

If anyone was able to make the investor day I would love to hear feedback.

Disc: I own RL

Initial Base Valuation (17/3/26) - $1.39

Following an initial thesis for investment I have now had some time to put some numbers around value, already being comfortable that my initial buy in for a starter position at 80c was likely well below value, still I needed to confirm with numbers.

To do so I am simply looking at FY26 expected results from a few angles. Firstly as a PE multiple then as a P/FCF multiple, in both cases the range of 25 to 35 (ie 30 average), which for a capital light company with high bottom line growth due to operating leverage and high margins is relatively conservative given it has only recently tipped into profit so these multiples will drop rapidly with minimal top line growth.

Valuation Result:

NPAT Projection for PE value:

FCF Projection for P/FCF value:

Notes on assumptions:

- EBITDA for FY26 assumes ROU asset depreciation is removed along with other depreciation and amortisation, which is how it is reported and should aligh to the method used for the target FY26 EBITDA. However, for the historical figures I include this cost in EBITDA which is why depreciation and amortisation shown in FY26 is higher than prior years when I am assuming it’s the same.

- I have assumed no tax payable due to the below note from the FY26 annual report which shows deferred tax assets from losses and R&D tax credits. From this there is at least $10.5m in future tax payable that can be offset, plus R&D credits from FY25 and forward years, so it will be many years before HPG is paying tax. The value of these tax assets is thus indirectly included through a higher NPAT and FCF used to calculate value.

Page 92, FY25 Annual Report:

Comment

The FY26 targets the company has stated are reasonable if you assume H2 growth to be in line with H1, which I am comfortable with. The flow through impact to NPAT is that a modest 8.2-9.4% growth in the top line may result in a 52-138% growth in the bottom line YOY. The PE range at the current price of 77c would be 18-29 on the FY26 target with an expectation of mid to high double digit NPAT growth in FY27 – so very cheap.

From a cash perspective, almost 30% of the market cap is held in cash. The last two halves generated $8.7m in FCF in total, so the current run rate of cash generation would put the IV of the company at under a FCF multiple of 10. My FCF for FY26 in the valuation is probably too conservative, but it’s where the numbers landed assuming flat Depreciation and Ammortisation as well as spend on PPE and Intangibles. I suspect the cash generating gap between these will open up more this year and going forward.

I have kept the forecast to near term because the company business model transition and expansion is still working through the reported numbers, making a projectable set of numbers even more difficult than normal. Hence the short term valuation view is simply to ensure the current price is well supported with plenty of upside potential, which I feel it is.

As a result I have topped up today, but it still remains a relatively small position and may continue to add even given plenty of other good value options.

Disc: I own RL

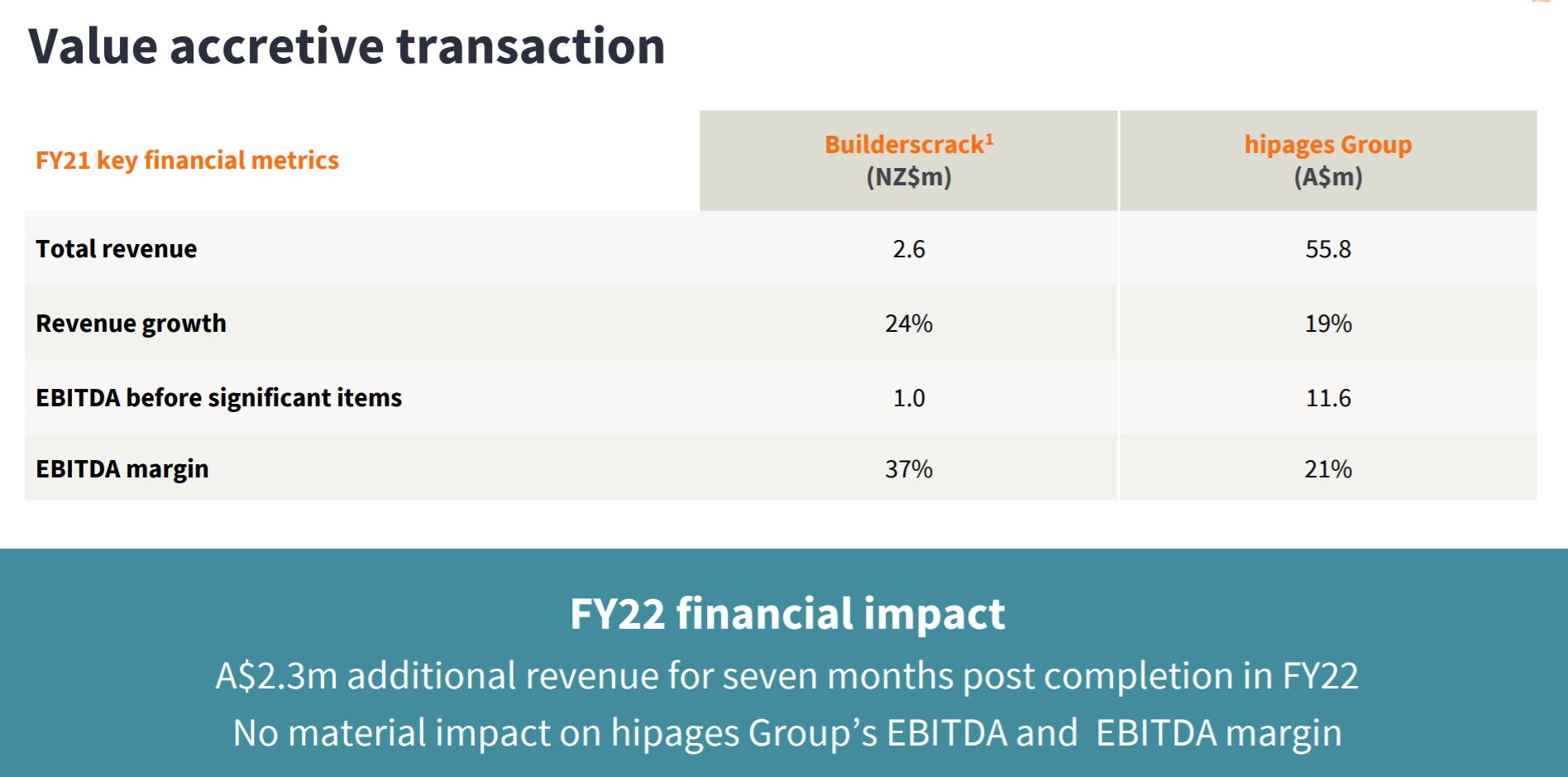

- Hipage spends $11.8m in cash and equity to acquire similar NZ tradie marketplace (builderscrack)

- It has 4000 active tradies

- more than 95000 jobs per year

- FY21 Revenue = 2.6m (NZ$)

- FY22 expected Revenue for 7 months post acquisition = $2.3 ( if we annualize that equates to $3.9m, i.e 50% growth)

- CEO and CFO said that there will be an investment for the initial couple of years - importantly it gives them exposure to NZ market where they can go and sell other hipage's products like tradicore

- HPG is also currently in process of developing payment solution

- The acquisition increases TAM for total business