Overall Comment

Adding to position again due to the large margin of safety. The results were down on FY21 as expected due to lockdowns and cycling effects. The NTA of $3.72 per a share (mostly backed by freehold property) provides a nice margin of safety. The dividend continues to provide a strong yield, though I believe it is at its sustainable limit so wouldn't be surprised if this drops next FY. The market seems to price HVN as though the operating business will struggle to be profitable in the future or the property is worthless, effectively you get one of these for near free valuation at the current share price. The company everyone seems to love to hate (or is that just Gerry Harvey? Fair enough in that case...) continues to execute with sustainable growth and provide a more than acceptable return to shareholders through dividends.

General Notes

- Financial notes:

- Revenues:

- Products to customers - $2.8bn

- From franchisees - $1.3bn

- Other items - $397m

- Net debt to equity = 10.31%

- NPAT = $811m including property revaluations for comparison, excluding AASB16 net impact and net property revaluation profit was $673m.

- Freehold property portfolio of $3.74bn, 95 properties in Australia, 26 overseas or as Australian joint ventures.

- NTA = $3.72

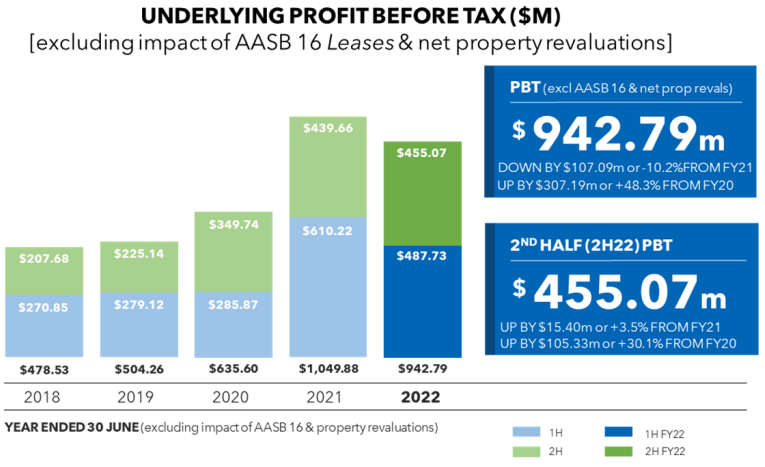

- To compare to FY19 for the COVID cycle, NPAT not including revaluations in FY19 was $386m compared to FY22 of $673m. On that basis profit is up 74%. These figures also don't include AASB16 impacts so are comparable. Total system sales of $9.56bn in FY22 compared to $7.65bn in FY19, a 26.5% increase. If these results continue the business has hit a point of operating leverage. Underlying PBT results below for the last 5 FYs.

- Footprint:

- 195 franchised complexes in Australia with 544 franchisees

- 109 overseas company operated stores.

Positives

- Overall, a decent result, nothing glaringly negative.

- Dividend of 17.5c, giving a total FY dividend of 37.5c fully franked. At a share price of $4.17 this is a yield of 9% or 12.8% gross yield.

- International segment continues to grow strongly, FY19 PBT was $129m now up to $232m and increase of 80%. The overseas segment now creates 25% of PBT (excluding revaluations). Given Australia has 195 complexes there is still significant growth for this segment into the future. 4 new stores overseas expected in FY23 and 10 new stores in FY24.

Negatives

- Looking at the cash flows the high dividend doesn't seem sustainable (or able to grow), partly funded by debt potentially. Not significantly over a sustainable level especially considering increase in inventory but reaching the limit of what is available.

- Gerry Harvey continues to make public comments throughout the year that turn off younger customers from entering Harvey Norman stores.

Has the thesis been broken?

- No, adding again to make a full position. This is a value play/trade. I believe HVN is significantly undervalued at the current price. There is a large margin of safety from the profitability and NTA backing (backed by the large property portfolio). The dividend yield also helps. The company is more diverse than on first thought given the multiple geographies and property holdings the company has.

Valuation

- Conservative valuation based on:

- 10% discount on property value = $3.366bn

- Using an underlying profit of $500m (ie no profit growth and removing property segment profits) and 8 times multiple = $4.0bn

- Total valuation = $7.376 bn.

- Valuation per share = $5.88

What are you expecting and what do you need to see over the next reporting season or generally into the future?

- Thesis only requires continued results around current levels of profitability. Some pull back is expected cycling off the COVID and higher interest rate impacts. Housing build completions seems still to be at higher than previous levels so I think this helps HVN and JB Hifi, will have to wait and see on that....

- Continue to expand the overseas business.