Consensus community valuation

I notice Gerry Harvey is in the news again, this time with his innovative new method of reducing shrinkage before Christmas.

$HVN reported a YTD Trading Update today.

Australian franchisee sales down 13.9% on a LFL basis.

Unaudited operating PBT down 49.1% (before non-controlling interests and exclding AASB16 and property revals) again highlighting the strong negative operating leverage in this sector.

SP up almost 5% on the announcement of the share buy-back.

(Seems to be faring significantly worse than my pick $NCK, albeit with a longer period reported into FY24.)

Disc: Not held. I hold $NCK in RL

Now. 28/6/2023 report PBT: $670Mill ( $60.90m = 670 / 11 months )

30/6/2022 reported PBT: $1.140Bill ( $95m = 1140 / 12 months) monthly approx $95m vs $60.9m (158% change)

so reported PBT: has halved vs 12 months so discretionary retail shopping dived ..

Is HVN a buy? circa $3.30 see what the RBA presents in July, first Tuesday meeting..

So the share price has reflected this fall in PBT .. see what happens when HVN report on Thursday 31/8/2023

Checking comparible disclosure:

June 2022 . PBT $1.140Bill

Microsoft Word - PRESS RELEASE_30 June 2022_FINAL FOR RELEASE 310822 (markitdigital.com)

Further back dated below: Reported PBT $522.67Mill

Announced Feb 28th 2022

Microsoft Word - PRESS RELEASE_31 December 2022_FINAL FOR RELEASE 280223.docx (markitdigital.com)

Adding to the info from @Dominator HVN seems to have cracked the Asian secret and been successful where many Aus companies have failed. Should they execute on growing their store foot print in Malaysia from 28 to 80 through 2028 they will continue to reward holders with a steady growing dividend. The 3 slides below summarise key info regarding their Malaysian expansion. This much maligned and dismissed business continues to succeed and grow when a lot of so called “experts” had written this dinosaur off. Currently, returning over 9% with a significant payout ratio buffer it’s not hard to see this dividend return at the current share price being well into double figures by the end of the decade.

Overall Comment

Adding to position again due to the large margin of safety. The results were down on FY21 as expected due to lockdowns and cycling effects. The NTA of $3.72 per a share (mostly backed by freehold property) provides a nice margin of safety. The dividend continues to provide a strong yield, though I believe it is at its sustainable limit so wouldn't be surprised if this drops next FY. The market seems to price HVN as though the operating business will struggle to be profitable in the future or the property is worthless, effectively you get one of these for near free valuation at the current share price. The company everyone seems to love to hate (or is that just Gerry Harvey? Fair enough in that case...) continues to execute with sustainable growth and provide a more than acceptable return to shareholders through dividends.

General Notes

- Financial notes:

- Revenues:

- Products to customers - $2.8bn

- From franchisees - $1.3bn

- Other items - $397m

- Net debt to equity = 10.31%

- NPAT = $811m including property revaluations for comparison, excluding AASB16 net impact and net property revaluation profit was $673m.

- Freehold property portfolio of $3.74bn, 95 properties in Australia, 26 overseas or as Australian joint ventures.

- NTA = $3.72

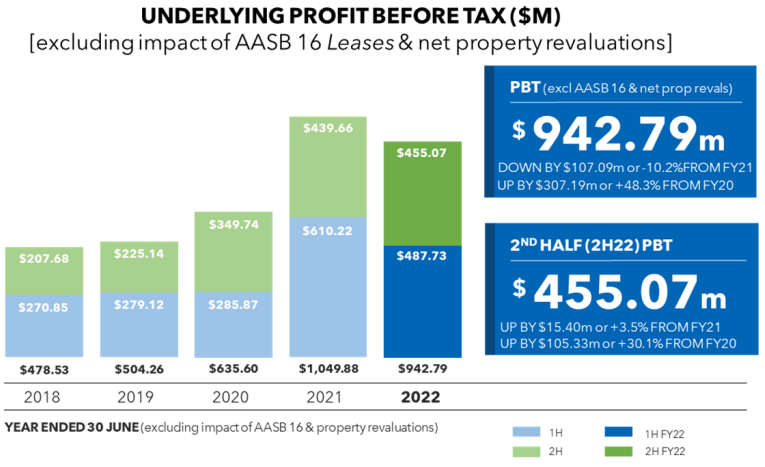

- To compare to FY19 for the COVID cycle, NPAT not including revaluations in FY19 was $386m compared to FY22 of $673m. On that basis profit is up 74%. These figures also don't include AASB16 impacts so are comparable. Total system sales of $9.56bn in FY22 compared to $7.65bn in FY19, a 26.5% increase. If these results continue the business has hit a point of operating leverage. Underlying PBT results below for the last 5 FYs.

- Footprint:

- 195 franchised complexes in Australia with 544 franchisees

- 109 overseas company operated stores.

Positives

- Overall, a decent result, nothing glaringly negative.

- Dividend of 17.5c, giving a total FY dividend of 37.5c fully franked. At a share price of $4.17 this is a yield of 9% or 12.8% gross yield.

- International segment continues to grow strongly, FY19 PBT was $129m now up to $232m and increase of 80%. The overseas segment now creates 25% of PBT (excluding revaluations). Given Australia has 195 complexes there is still significant growth for this segment into the future. 4 new stores overseas expected in FY23 and 10 new stores in FY24.

Negatives

- Looking at the cash flows the high dividend doesn't seem sustainable (or able to grow), partly funded by debt potentially. Not significantly over a sustainable level especially considering increase in inventory but reaching the limit of what is available.

- Gerry Harvey continues to make public comments throughout the year that turn off younger customers from entering Harvey Norman stores.

Has the thesis been broken?

- No, adding again to make a full position. This is a value play/trade. I believe HVN is significantly undervalued at the current price. There is a large margin of safety from the profitability and NTA backing (backed by the large property portfolio). The dividend yield also helps. The company is more diverse than on first thought given the multiple geographies and property holdings the company has.

Valuation

- Conservative valuation based on:

- 10% discount on property value = $3.366bn

- Using an underlying profit of $500m (ie no profit growth and removing property segment profits) and 8 times multiple = $4.0bn

- Total valuation = $7.376 bn.

- Valuation per share = $5.88

What are you expecting and what do you need to see over the next reporting season or generally into the future?

- Thesis only requires continued results around current levels of profitability. Some pull back is expected cycling off the COVID and higher interest rate impacts. Housing build completions seems still to be at higher than previous levels so I think this helps HVN and JB Hifi, will have to wait and see on that....

- Continue to expand the overseas business.