Top member reports

No meetings

Consensus community valuation

The consensus valuation is for members only and has been removed from this chart. Click for membership options.

No value forecast available for this company

Content is delayed by one month. Upgrade your membership to unlock all content. Click for membership options.

#Half Review

stale

The Good

- Operating expenses remain flat.(Slight increase in admin costs over the last couple of quarters)

The Not So Good:

- No growth in ARR and Revenue QoQ. Revenue for H1 is down on H2FY23.

- SaaS revenue is not growing as a portion of total revenue. Sitting at 52% for H1FY24 which is the same as what it was in H1FY23.

- Only $2.5m in cash available at the end of the quarter. (After $1m placement with Maptek). There is an additional $2m in an undrawn loan facility, but this does not leave much room before another placement may be looking necessary. Q4 has typically been the strongest quarter for cash flows which may assist slightly.

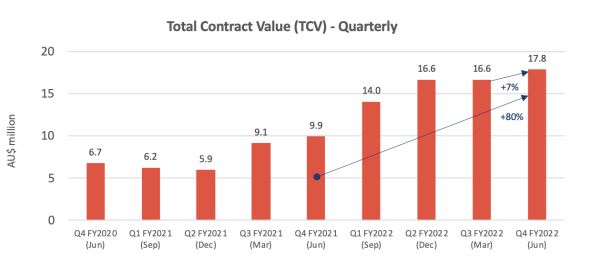

- TCV dropped from $17.7m to $16m which shows forward contracts are not replacing delivered work. Not included as a chart in the Q2 update.

Watch Status:

- Downgraded further due to stagnation of wins and low cash position

Valuation Status:

- Shifted weighting from bull case leading to decrease in valuation

What To Watch:

- Strategic review ongoing without any substantial updates. Likely leading to a whole business sale? Maptek is currently a substantial holder and would be the most logical acquirer.

- New global sales leader appointed in October 23 leading to a “considerably strengthened” pipeline for H2. (No announcements to date in Q3)

- New sales role to assist in expanding into adjacent markets (No announcements to date in Q3)

- Partnership with Asset Assurance Monitoring in the U.S to distribute dams and tailings solution.

- Reduction in investing spend. This has the potential to impact improvements in software and ongoing development.

- Release of update to JORC code. Likely not until the end of 24. Reported as "immanent"

- Migration of clients across to new Resource Disclosure modules started with Newmont Mining. Newmont migration to be completed by April / May.

Read More

#Quarterly Review

stale

The Good

- ARR continues to improve and is up 5.3% QoQ to $7.9m

- Second platform added for Roy Hill with TCV of $2m

The Not So Good:

- Cash position is in a precarious position even after the capital raise which has led to a strategic review to identify the best structure for access to capital. This is due to an increase in negative operational cashflow for the quarter along with $863k of investing expenses.

- Roy Hill was the only material contract awarded during the quarter.

- TCV remains steady at $17.7m

What Status:

What To Watch:

- Product release process should help onboard the current projects in progress: Anglo American, Arcelor Mittal and Eramet. Completion of implementation milestones should assist in improving revenues after a decrease in Q1

- Maptek continues to build a position with $1m placement at premium to share price. This has increased their holding to 17.7% with a further 12 months standstill agreement.

Read More

#Quarterly Review

stale

The Good

- Quarterly revenue at $4.0m up from $3.4m the prior quarter. Revenue has tended to be lumpy from quarter to quarter, so it is likely that this may not be as high in Q1FY24. Revenue for FY23 is also up 28% on FY22 which indicates although K2F has had some issues with cash burn, they still are maintaining a reasonable growth rate.

- Free Cash Flow positive for the quarter with $400k added to cash reserves. This leaves a cash balance of $4.4m (along with the working capital facility of $2m). Cash reserves have been an issue for K2F in the past, however with the improving quarterly cash flow position, this may be enough to reach a position where no further capital raises are required. Note. K2F has been in this position before, but then cash receipts quickly fell away in the following quarter.

- No significant changes in operating expenses, however staff costs are rising again.

- ARR $7.5m and TCV $17.7m are both slightly higher than I was forecasting in an earlier straw. (After quarter end a new contract with Roy Hill puts these figures now closer to $7.8m and $19.7m)

The Not So Good:

- Material contract signings are quite infrequent with only 2 announced in Q4FY23 and none in Q3

What Status: Turning

What To Watch:

- Mineral Resources & ArcelorMittal contracts were announced in November so these contracts should be live in Q1FY24.

- Time to implement Eramet & Roy Hill contracts

- The 12 month standstill agreement with Maptek expired in April. Given the current weakness in K2F’s share price, Maptek may look to continue to build a position in the company. (Carried over from the previous quarter - No indication of this yet)

- Further details on Maptek collaborations / integrations

Read More

#Quarterly Review

stale

The Good

- Revenue for Q3 improved over previous quarters to $3.4m.

- Staff expenses have largely levelled out after previous spikes.

The Not So Good:

- Total Contract Value has taken a hit for the first down and is down on the previous quarter. This indicates that as K2F is delivering on projects and services, they are not replacing this with new work along with no new major contract wins announced this quarter.

- ARR is flat for the quarter but up 35% over the pcp.

- Cash balance of $4m provides ~ 1 yr runway (including investing expenses) which given funds were raised only 12 months ago, additional capital could be hard to come by. Operating cash burn continues to improve, however cash receipts have been lumpy over previous quarters.

What To Watch:

- Product costs are significantly up on previous quarters. This along with the increase in invoices raised over the quarter of $3.6m may indicate a rise in cash receipts for Q4. This will likely still be down on the $5.4m in Q4FY22.

- So far the land and expand strategy execution is questionable as there haven’t been many significant additions across the existing customer base.

- BHP ground disturbance & Rio Ground Disturbance have gone live. These were announced in May 22 & Nov 22 respectively. So in the future I need to factor in 6-9 months of implementation time before ARR goes live.

- The 12 month standstill agreement with Maptek expired in April. Given the current weakness in K2F’s share price, Maptek may look to continue to build a position in the company.

Read More

#Quarterly Update

stale

The Good

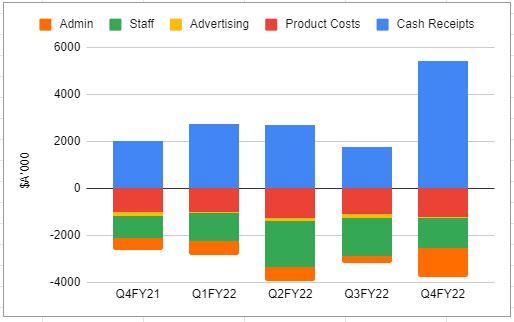

- Cash flow positive quarter of $1.7m. This was driven by a significant increase in cash receipts for Q4 at $5.4m. Timing of cash receipts are likely to be lumpy going forward given some of the commentary around operational cash flow, this positive quarter along with the increase in invoices raised for the quarter means that going forward cash burn is likely to be reduced. With $8.2m of cash available, it is looking like there shouldn’t be any need for capital raises for ongoing business operations.

- BHP is now a customer. Given the extent of BHPs operations, there is an opportunity to sell other products and extend the use of the Ground Disturbance Software

- No significant change in product costs as ARR continues to grow, hints that there is potential there for operating leverage as further deals continue to be signed.

The Not So Good:

- ARR is up ~ $800k to $6m. On first glance this number is decent being the largest increase by value in the last 2 years, however this looks to consist of two contracts: The 1 Year BHP contract for $620k and $145k for Asarco. The rate of contracts signed has slowed over the last year which can be seen in the ongoing total contract value. I had expected that potentially the Maptek investment may lead to a burst of new contracts, but this may require a bit more time given the deal is only recent and the end of the financial year.

What To Watch:

- Cash receipts next quarter. I expect this to be down on the current quarter and more inline with the invoiced value of $3.8m

- Cost control looks to remain an ongoing focus with staff costs coming down, however this has been offset by a large increase in admin and corporate costs.

- Further updates on the fraud in overseas operations. No news in this update.

- Rate of contract wins amongst both existing and new customers. If this remains low it will be a sign to review investment thesis.

Read More

#Fraud incident

stale

Sucks to be them.

How does anyone think $745k won't be missed in a company that booked $4.6m revenue and had a cash balance of $3.6m in 1H FY22. It undermines all of their accounts.

[Not held]

Read More