Consensus community valuation

A pot stock that continues to remain unprofitable, and whose share price has dropped ~90% from its peak?

Not something that would capture your attention, but I thought Paul made some interesting points in today's interview:

- A lot of 'hot money' flowed into the sector during the easy money days circa 2020. This led to over-investment, over-supply and irrational competitor behaviour. But this is slowly being washed out, and Paul hinted that there would likely be some consolidation in the space

- Indeed, they picked up a ~$100m facility for $20m, and are currently using only <15% of capacity

- The regulatory lead time to get proper approvals is a period of years -- which gives them a bit of a head start to any would-be new entrants

- Adoption rates have grown significantly in Australia -- from 1% of adult population to 4% in a few years.

- Australia represents 90% of their business, but over the next ~5 years or so, he thinks 90% will come from Europe.

- Costs have been held steady for a couple years and the business is very close to cash flow positive. They will lose their R&D rebate soon (as they are now too big to be eligible) but as volumes grow they expect to scale into profitability

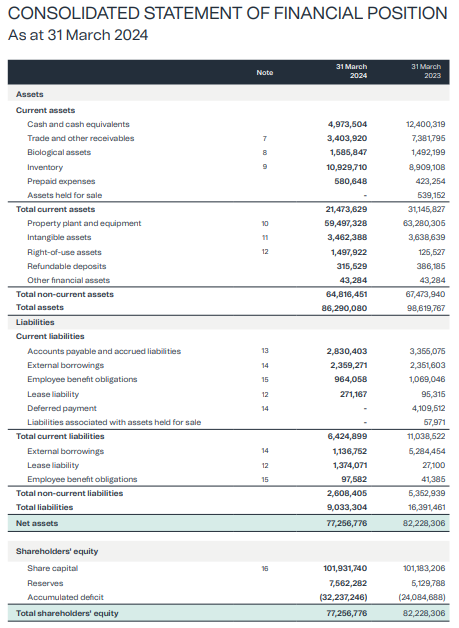

- The company's market cap is presently $30m and the enterprise value slightly less at ~$28.6m -- but the net asset position is $77m:

- Even if you write off ALL the inventory, forget about any accounts receivable and intangible assets, and even if you halve the value of land & buildings, you still have a NTA per share of ~10c per share (ie the current share price)

- Of course, they are losing ~$7m per year on a statutory basis, so at a 50% margin they'll need to see a sales increase of at least 60% to be in the black (all else being equal)

- This wasn't discussed during the call, but last year they spent $6.3m on R&D, which seems like a lot (especially on top of almost $8m in G&A and Sales costs). I get that they argue product consistency and quality are paramount, but still.. On the plus side, it feels like a lot of money could be saved on that front (potentially) if they needed to.

- I think there's genuine and growing legitimacy to the sector, and we will likely see a maturation of the industry in the years ahead. LGP do seem well placed to capitalize on this trend, but shares really seemed priced for disaster -- perhaps a hangover form the previous irrational exuberance in the sector? And, as Paul mentioned, expectations for another raise.

- There's a deep value case to be made here so long as you think they can sustain reasonable sales growth while keeping costs contained.

Cannabis clinics are driving the increase in cannabis flower sales in Australia.

The model is clinic like Alternaleaf provide a telehealth consultation for $59 no referal needed.

Access is very easy if you have one of these conditions:

Leafio is their distributor which has a number of suppliers one of which is Little Green Pharma. LGP run about 1/4 of their sales through these clinics who take a 30%+ commission.

Alternaleaf recently had the Therapeutic Goods Administration (TGA) launch court proceedings against the sponsor’s parent company for breaching the Therapeutic Goods Act for advertising on The Dolphins jersey who were forced to tape then remove the logo.

Alternaleaf is owned by Montu which is a private company. Corporate records show Montu earned $96 million in revenue in Australia last financial year – an annual increase of 471 per cent.

The TGA, "Alleged that Montu and Alternaleaf unlawfully advertised medicinal cannabis using terms including ‘medical cannabis’ and ‘plant medicine’ to promote the Alternaleaf online clinic, which enabled patients to purchase prescription-only medicines after completing an online consultation process."

Some of these cannabis clinics have been set up to purely capitalise on on the boom in regulated cannabis flower sales and don't have an interest in genuinely promoting the medicinal benefits. There is some unconventional promotion by these companies which is drawing the ire of the TGA. PlantMed have sponsered an event called Buds & Bowls a Brisbane event that included DJ sets, lawn bowls and a tent in which patients could vaporise their medicines.

Aggressive advertising tactics employed by parts of the industry have also attracted scrutiny from psychiatrists, who are concerned that products containing THC are being inappropriately prescribed to young patients at risk of psychosis. There is a risk that these clinics, which are on the boundary of illegality, will be shut down/regulated. This would affect some sales for Little Green Pharma and more importantly have a broad negative impact on the industry.

Sharing some thoughts on a company called Little Green Pharma (LGP) that I have been following for a few years and have recently started buying IRL and here on Strawman.

In a nutshell this is a deep value play.

LGP is a medicinal cannabis business. There was furious excitement for medicinal cannabis companies in 2021 when share prices peaked. Since then market sentiment has fallen and the share price for these companies is in the dog house. Most of these companies are loss making. We are now in a period of consolidation for this sector. When market sentiment is poor like it is in the cannabis sector the baby can get thrown out with the bathwater.

The industry is a strange mix of “health and wellness” companies, biotech’s rolling the dice on specific applications for humans and in some cases animals, the cannabidiol (CBD) sleep bros and traditional dry flower growers/producers for medicinal purposes. Majority are private companies in Australia.

According to data from Australia’s Therapeutic Goods Administration (TGA) medical cannabis approvals for new patients through an Authorized Prescriber have continued to grow in 2023. From January to June 2023, the aggregate of all new patients reported was 307,846 compared to 137,111 new patients from January to June 2022 and 30,662 from the same period in 2021.

The Australian Government Office of Drug Control lists 44 entities who are approved manufacturers and suppliers of medicinal cannabis products. Most of these are private companies. Of the handful of public companies I can't find any that are profitable. LGP have said they are cash flow positive in March excluding their R&D rebate. I think their business is at an inflection point and no one is looking.

In my opinion medicinal cannabis flower sales are growing because there is a transition from illicit sales to prescription sales. This is a reflection of the softening regulation occurring in all markets which makes the logistics of transport, storage, accounting and access of cannabis easier. As the public perception of cannabis becomes less negative it use is moving into new areas such as elderly people with terminal cancer.

LGP was the first company in Australia to grow medicinal cannabis for domestic use. Their main facility is in WA. In 2021 LGP acquired one of Europe’s largest medicinal cannabis cultivation and manufacturing facilities in Denmark for $21m from Canopy Growth. This was at a significant discount to the asset value.

Majority of sales are in Australia. LGP had record quarterly revenue of $7.3 million, up 34% on previous quarter.

Flower sales were up 57% on the previous quarter and are growing strongly. LGP has strong branding and a good product. Australian sales were up 27% from the prior quarter predominately due to the introduction of CherryCo flower. See this review (https://www.youtube.com/watch?v=ZrtqEhzbIR4)

European sales are choppy. On 1 April 2024 cannabis was legalised in Germany with its removal from the Narcotics List and there are early signs of strong patient uptake. LGP’s Danish facility is two hours from the German border and in an excellent position to capitalise on likely improved medicinal cannabis access pathways. LGP was one of two companies supplying a French medicinal cannabis pilot which ended on 27 March 2024. They will have early access to this market. LGP also sell to UK and have just started selling to Poland and Switzerland.

Also the US Drug Enforcement Administration have just confirmed they will recommend reclassifying cannabis from Schedule I to Schedule III. The news has resulted in a re-rating of North American cannabis companies with the MJ ETF and the MSOS ETF both increasing by over 25%. This sector re-rating is expected to flow through to other cannabis companies including LGP given the historical mirroring of the North American markets. The proposed rescheduling would remove s280E taxes which tax cannabis operators at their gross margin level (versus net income) and generate potential momentum for other pro-cannabis legislation at the federal level and increased institutional interest in US cannabis stocks.

The US cannabis companies are the biggest. Most seem to be loss making.

Here is a snap shot of the largest by revenue Curaleaf Holdings (CURL):

Revenue $1.3b

Operating income $43m (noted almost half a billion dollars for Selling and Administration expenses!)

Net income $-280m!! (after tax, impairment of goodwill, interest on debt)

Haemorrhaging cash big time. A lot of consolidation is happening/ gonna happen.

LGP finished FY24 with a positive operating cashflow of $0.5 million. This included a $5m research and development rebate. The month of March being operating cashflow positive in its own right without the R&D rebate.

Management and employees own about 20% of the company so strongly incentivised.

LGP’s net tangible assets are significantly above it’s enterprise value. This means that the value the market has given LGP as a business (about $40m) is less than the value of it’s assets (about $80m)! In other words the share price is deeply discounted. This company has been priced to fail but the market is wrong in my opinion.

Thesis: significantly undervalued company at a profitability inflection point driven by a transition of cannabis flower sales from illicit to prescription

Risks:

The cannabis sector is still bloated and full of loss making companies many of which will fail

This is a commodity business to some degree with a rapidly shifting regulatory framework