Top member reports

Straws

Sort by:

Recent

Content is delayed by one month. Upgrade your membership to unlock all content. Click for membership options.

#CEO Interview

stale

A pot stock that continues to remain unprofitable, and whose share price has dropped ~90% from its peak?

Not something that would capture your attention, but I thought Paul made some interesting points in today's interview:

- A lot of 'hot money' flowed into the sector during the easy money days circa 2020. This led to over-investment, over-supply and irrational competitor behaviour. But this is slowly being washed out, and Paul hinted that there would likely be some consolidation in the space

- Indeed, they picked up a ~$100m facility for $20m, and are currently using only <15% of capacity

- The regulatory lead time to get proper approvals is a period of years -- which gives them a bit of a head start to any would-be new entrants

- Adoption rates have grown significantly in Australia -- from 1% of adult population to 4% in a few years.

- Australia represents 90% of their business, but over the next ~5 years or so, he thinks 90% will come from Europe.

- Costs have been held steady for a couple years and the business is very close to cash flow positive. They will lose their R&D rebate soon (as they are now too big to be eligible) but as volumes grow they expect to scale into profitability

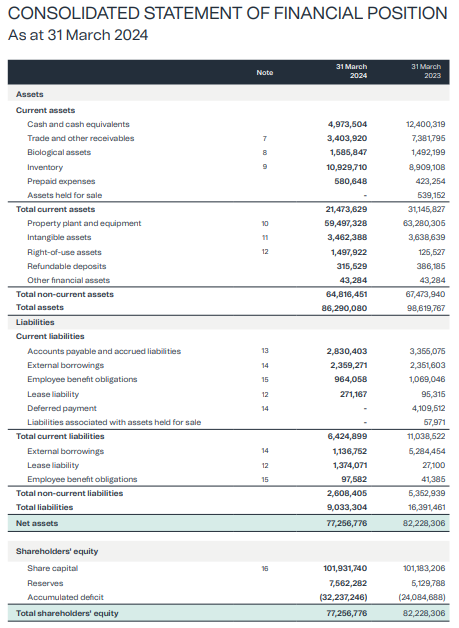

- The company's market cap is presently $30m and the enterprise value slightly less at ~$28.6m -- but the net asset position is $77m:

- Even if you write off ALL the inventory, forget about any accounts receivable and intangible assets, and even if you halve the value of land & buildings, you still have a NTA per share of ~10c per share (ie the current share price)

- Of course, they are losing ~$7m per year on a statutory basis, so at a 50% margin they'll need to see a sales increase of at least 60% to be in the black (all else being equal)

- This wasn't discussed during the call, but last year they spent $6.3m on R&D, which seems like a lot (especially on top of almost $8m in G&A and Sales costs). I get that they argue product consistency and quality are paramount, but still.. On the plus side, it feels like a lot of money could be saved on that front (potentially) if they needed to.

- I think there's genuine and growing legitimacy to the sector, and we will likely see a maturation of the industry in the years ahead. LGP do seem well placed to capitalize on this trend, but shares really seemed priced for disaster -- perhaps a hangover form the previous irrational exuberance in the sector? And, as Paul mentioned, expectations for another raise.

- There's a deep value case to be made here so long as you think they can sustain reasonable sales growth while keeping costs contained.