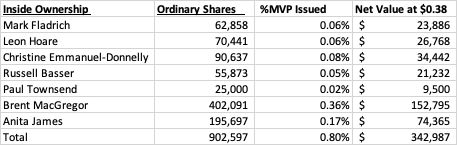

Recent Buying

Russell Basser

30 October 2025

Buying On Market 40,000 shares at average price $0.7056 ($28,227)

Mark Fladrich

30 September 2025

Buying on Market 62,858 shares at average price $0.7099 ($44,629)

Paul Townsend

22 September 2025

Buyiing on Market 25,000 shares at average price $0.6714 (16,785.31)

Management Bio’s

Mark Fladrich - Chair

Mark is an experienced leader with over 30 years of experience in the pharmaceutical industry, specialising in commercial, strategic, and operational roles across a broad range of therapeutic areas, including pain management.

Most recently, Mark served as Chief Commercial Officer at Grunenthal, a privately owned German company with a strong presence in Europe and Latin America. During his time at the company, he expanded Grunenthal’s commercial presence into the US in parallel with the relaunch of a non-opioid chronic pain management treatment.

Prior to this, Mark spent 23 years at AstraZeneca, holding various senior roles, including Vice President of Global Strategic Marketing, Country President roles in Germany, Australia and New Zealand and Regional Head of Southern and Western Europe.

Mark has also held leadership roles at Allergan and Faulding Pharmaceuticals in Australia.

Currently, Mark is the Chair of QBiotics, an Australian life sciences company, the Chair of the Strategic Advisory Board for Atacana, a global pharmaceutical and biotech industry consulting firm and serves as a Board Observer and Strategic Advisor at HealthMatch, a Sydney based digital startup who have developed a patient centric platform for clinical trial recruitment.

Leon Hoare - Non-Executive Director

Leon is an accomplished commercial leader with expertise across multiple Life Science sectors. He is currently the Managing Director of Lohmann & Rauscher, Australia & New Zealand (ANZ), a private EU based medical device company.

Previously, Leon was Managing Director of Smith & Nephew (S&N) ANZ, one of S&N’s largest global subsidiaries outside the USA. He served as President of S&N’s Asia Pacific Advanced Wound Management (AWM) business for 5 years and was a member of the Global Executive Management for the AWM Division (as one of three Regional Presidents).

In his 24 years with S&N, he also held roles in marketing, divisional and general management.

Leon’s career has also included a senior role at Bristol-Myers Squibb, and as Vice-Chair of the board of Australia’s peak medical device industry body, Medical Technology Association of Australia. Leon is also the Chair of MDI’s Human Resources Committee.

Public company directorships in the past 3 years:

Polynovo Limited since 27 January 2016

Christine Emmanuel-Donnelly Non-Executive Director

Christine is an experienced IP and business development professional having 35 years’ experience locally and internationally.

Christine is a former Executive Manager of Business Development and Commercial at the CSIRO, where she led the management of CSIRO’s IP team and IP portfolio for 14 years and managed the CSIRO equity portfolio for over 5 years.

Prior to this role, Christine was in-house IP Counsel for Unilever in the UK and practised as a patent and trademark attorney for Wilson Gunn (UK), Davies Collison Cave and Griffith Hack in Melbourne.

Christine is also currently chairwoman of Impedimed Ltd and non-executive director of Polynovo Ltd, Pikcha Holdings Ltd, trading as Seminal. She was previously on the Board of the Institute of Patent & Trademarks Attorneys of Australia for 13 years.

Public company directorships in the past 3 years:

Polynovo Limited since 13 May 2020

Impedimed Limited since 2023

Russell Basser Non-Executive Director

Russell is a qualified physician, with over 30 years of international medical and biopharmaceutical experience. He has worked as a medical oncologist in Melbourne prior to joining CSL in 2001.

During his 21 years at CSL, Russell held multiple global executive roles, including Head of Global Clinical Development, Chief Medical Officer and Senior VP of Research and Development for CSL Seqirus. He has substantial expertise in international drug and vaccine development and spent several years based in the USA.

Russell currently serves as a non-executive director on the Boards of Starpharma Holdings Limited and Doherty Clinical Trials. He has previously served on the Board of the ANZ Breast Cancer Trials Group and the Hadassah Australia Medical Research Collaboration.

Paul Townsend - Non-Executive Director

Paul is an experienced global finance executive with a strong commercial focus and reputation of delivering results across diverse industries, including manufacturing, resources, consumer products and academia.

Paul has substantial ASX CFO experience at organisations including Nufarm, Asaleo Care, and Pacific Hydro, as well as Monash University, bringing a wealth of knowledge to MDI.

His extensive track record includes business turnarounds, new venture start-ups, mergers and acquisitions across local and global markets, navigating equity and debt capital markets and implementing changes necessary to deliver strong earnings growth, robust cash flow, and balance sheet optimisation.

Paul’s strategic mindset and leadership have consistently enabled successful business outcomes and the generation of long-term value. Paul has a Bachelor of Business (Accounting), FCA and GAICD.

Brent MacGregor - Chief Executive Officer

Brent joined MDI as Chief Executive Officer in November 2020.

Previously, Brent was the Senior VP Commercial Operations for Seqirus, from its inception in 2015 until 2020. He has also held roles as Head of North America for Novartis Vaccines and Diagnostics and Managing Director ANZ, Managing Director Japan, VP Global Marketing, and Global Head Strategic Planning for Sanofi Pasteur.

Brent is also a board member of Dynavax, a Hepatitis B vaccine company.

Brent has a BA in Political Science/Economics from Carleton University, Ottawa Canada, MA in Political Economy from Reading University, UK and an MBA from Kellogg – Northwestern University, Evanston IL USA.

Anita James - Chief Financial Officer

Anita joined MDI in May 2022 as Chief Financial Officer, bringing extensive senior finance and commercial experience in ASX listed environments.

Prior to joining MDI Anita worked at Pact Group Holdings Ltd, as General Manager Finance and Investor Relations, and other ASX listed companies in the mining and resources sector, including 12 years with the multi-national mining services Company Orica Ltd.

[Courtesy of Claude]

Short story: this got massively over hyped, now it is written off. But sales continue to quietly increase.

The market cap, as low as it is ($46 million), actually understates how low the valuation is. MVP holds around 40% of it's market cap ($18.7 million) in cash.

The big question is when they start showing real profitability? My take: they were free cashflow positive for the most recent 9 months. This is only likely to improve as revenue continues to increase going forward

3 things give me confidence:

1. The consistent revenue growth over time

2. The very cheap share price. Almost no success is "baked in"

3. The quality and uniqueness of the product, plus the lack of competition

[Sorry for the spam posts re this company. Can't help myself. I promise to shut up now. For a while. Maybe]

Could this perennial underperformer finally be starting to deliver? It certainly looks possible.

Genuine cashflow positivity. Sales improving both in Australia and Europe

Even after the 35% jump in the share price on Friday, this is still cheap. Market cap $57 million, but they have $18 million cash and no debt. EV/revenue is not much over one.

Paediatric approval (age>6) in Europe is about to happen and will almost certainly boost sales.

This quarter's figures would have looked even better if "respiratory" revenue (basically asthma spacers etc) hadn't dropped (it seems to bounce around quite a bit). So the performance of the core product was even better than it looks at first glance.

My take: the product has always been good, that's what prompted me to invest in the first place. Management was overly optimistic and tried to do too much all at once. MVP has struggled and underperformed for years. Maybe management have finally found a path forward

I have a small, deeply underwater position that I have held for some time. Almost tempted to add more.

Some Background - Why Am I Even Bothering?

(Perhaps against my better judgement and experience) last year I initiated a small position in $MVP (of Green Whistle fame), given some indications that good growth continues in Australia, and the impending European pediatric indication (August 2025 HPRA extension approval for children > 6 years) bodes well for growth in Europe, given that having a combined adult and pediatric indication increases the likelihood of adoption in emergency rooms and ambulances/paramedics (Evidenced by one NHS Trust already).

Having struggled through the pandemic for obvious reasons, having abandoned its attempt to enter the US (legacy of historical reputational overhang of toxicity in previous high-dose, anaesthsia applications in the 1960s and 1970s), having upgraded management and board with more internationally credentialled people (bye bye DW), a number of historical negative flags have been taken down, and so I now hold an initial 1% position (RL) having avoided the business for the last 8-9 years.

I'm still not convinced it is a good move, and will await a couple more quarterly reports before deciding to add or drop. That's because I need to see if Australian momentum can be sustained, and if UK/Europe usage ticks up. If that happens, then the business could start to look attractive. It is currently on an undemanding FY26 revenue multiple of 0.8x.

Today's report is not bad. I'm not going to get too excited about positive operating cashflow for the half, as there is varaibility from period to period, and we need to see Europe come to the party and start driving stronger growth than the somewhat anaemic +10%, given low current adoption. At the first sign that this is happening, I'll add.

Their Highlights

• Positive cashflow from operating activities for FY26 half year.

• Penthrox revenue up $2.3 million.

• Penthrox volume growth of 26% in the Australian hospital segment.

• Penthrox PBS Prescriber Bag eligibility extended to Nurse Practitioners in Australia.

• European in-market Penthrox volume growth of 10%.

• MAGPIE paediatric study published in Injury.

• Approvals for the Penthrox paediatric label in Europe progressing to plan.

• Cash balance at 31 December 2025 of $16.9 million.

My Analysis

Here's my usual 4C trend analysis over the last 8Q.

Costs were well controlled, albeit receipts weaker than trend, driven by softer revenue in the last Q.

The 8Q trend indicates that the business is moving into overall cash generation, and so the question is can we see uplift in Europe over the coming years?

There's good volume growth in Australian hospitals to provide a robust revenue base, and the extension to Nurse Practitioners in Australia, while unlikely to be material, add some support. (There are about 2,250 nurse practitioners in Australia, a tiny part of the c/ 138,000 registered clincal prescribers. But they could be an important first line users in remote and regional areas.) Rather than being major news in its own right, it is part of a continued pattern of wider adoption of the product.

Conclusion

An OK result, neither thesis confirming nor destroying. I am prepared to monitor while holding a small position over the next few quarters, unless the capital is called away elsewhere (which is entirely possible!)

Disc: Held (RL 1%, but low on conviction list)

This is one that I got terribly wrong. I sold out at least a year ago for a big loss but glad I got out when I did.

They have a great product in Oz and should have been able to make it work internationally. Execution and capital management have been abysmal and it doesn't seem to be getting any better.

Another example of an Australia health company that cannot turn a great product into a viable business. So disappointing. This slide tells you all you need to know:

good luck to anyone still holding !

23 Half Year Results - Results

MVP announced it's half year results last week, at a high level revenue up 45% to 13.9 and a net profit of 2,658. However this was only due to a refund from the termination of the China contract. Taking out that revenue and impairment net profit sits at -8,864 which is an 8% increase on the PCP.

Overall, mixed results. Not the growth required in the pain management and a surprise 80% growth in the respiratory business. After listening to their announcement below is my take on the good, bad and progress based on my watch list.

The good

- Increasing prices in December for Australia resulting in higher gross margins

- Gross profit margin increased to 71% from 67.9%

- 29% Growth in UK and Ireland with the current distributor even with a deferred shipment in UK. Revenue is only recognised when shipment is made so this will flow into the FY results.

- Positive feedback from all customers, CEO mentioned he has never heard a negative thing about the product

- Re-launched in Canada with a new partner

- 80% growth in respiratory and expected double digit growth in US moving forward

The bad

- 24% growth in France is well behind the > 50% they needed to achieve 110k units. Current run rate is at 60k units which is the same run rate presented for Jun-22 quarter. Effectively meaning no growth from June quarter.

- Negative growth in pain management units in Australia by 6k

- Expenses increased by 16% on PCP and 27% on the last half.

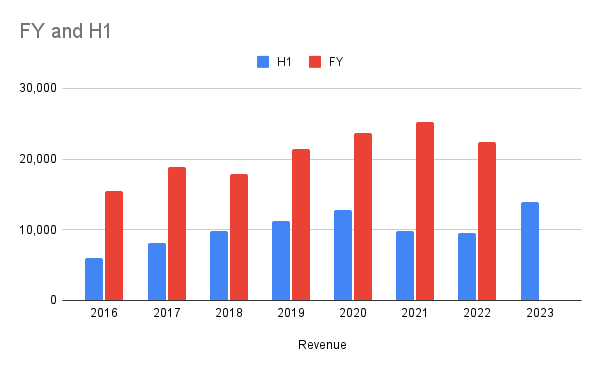

H1 / FY Total Revenue

Good growth in revenue, slightly beating H120

The split based on franchise

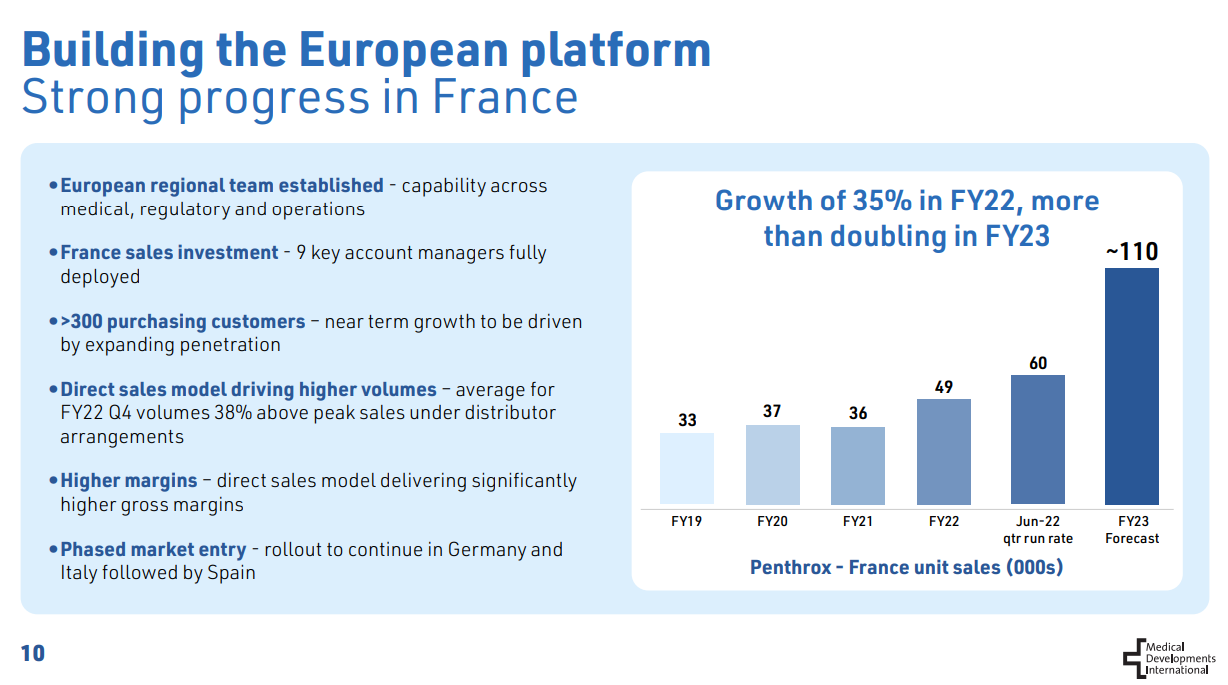

Continued penetration of Penthrox in France

At FY22, MVP were targeting ~110k units sold in France. Currently they are tracking on a run rate of 60k units. Well short of expectations.

Management have expressed multiple reasons which include

- Retaining / Recruiting: MVP uses a contract sales organisation in France. They are seeing issues retaining staff as they are going to companies which are offering permanent roles.

- Hospital Staff Shortages: Staff shortages in hospitals have made it harder to get the right decision makers on-board to add the green whistle to the hospital

- Bed Closures

- Budget Constraints

At a high level I get the sense that for pain management, they have to invest a lot of time in education. As this is a new product to majority of French hospitals there is effort in education to promote the benefits - ease of use and quick pain relief. I would imagine after time this education will reduce as this becomes the standard of care.

Market entry planning for Germany, Italy & Spain

Not much news on this apart from the next market they would target would be Germany sometime in FY24.

With the cash bleed at the moment, it does make sense to focus on growing and learning from France before spending more in entering another market.

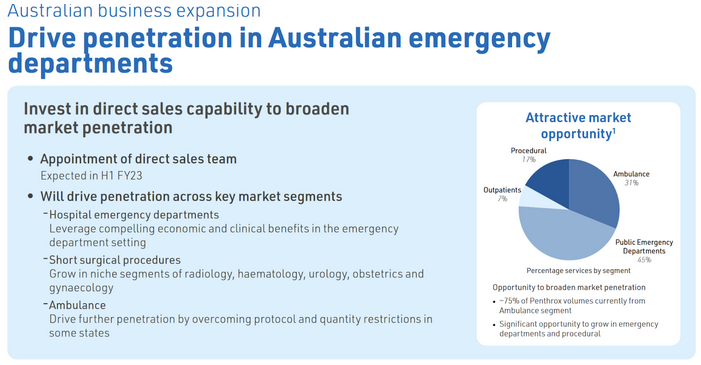

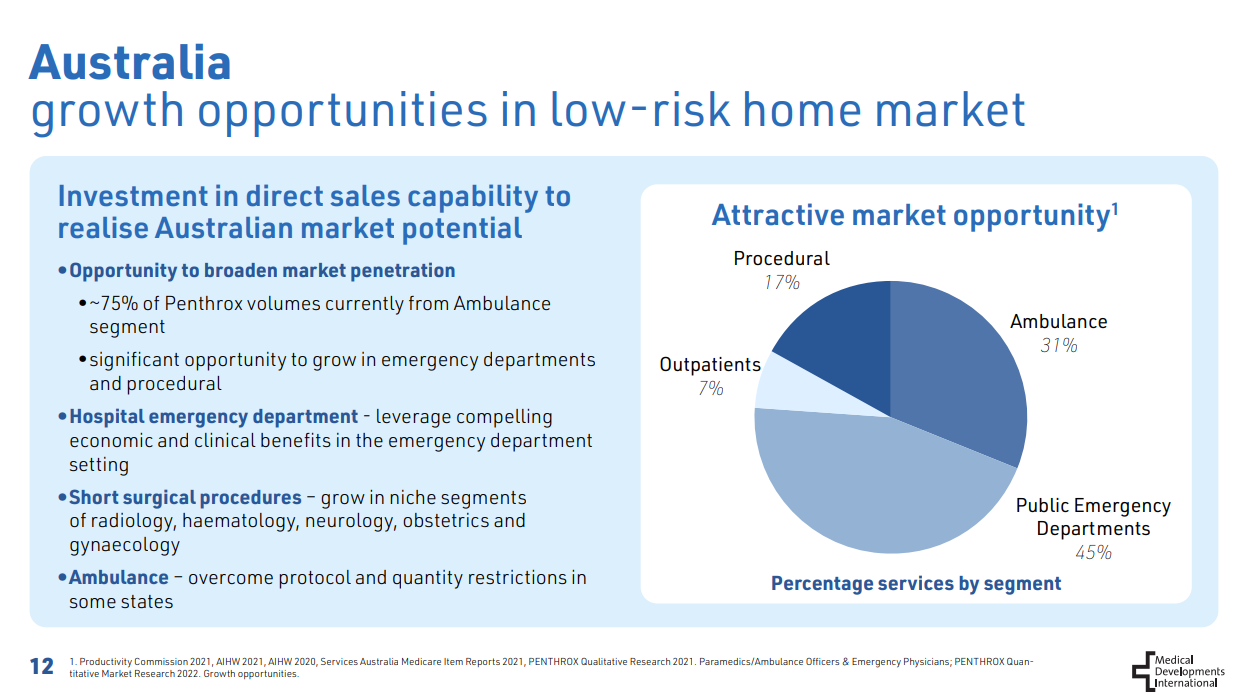

Direct in-market sales capability in Australia

Slight decrease in Australia units sold in the pain management section. However promising that they have on-boarded 2 ED's in Australia since October. Interestingly the indication in Australia is wider than anywhere else in the world. Overall not much of an improvement here with the direct sales team so expecting more.

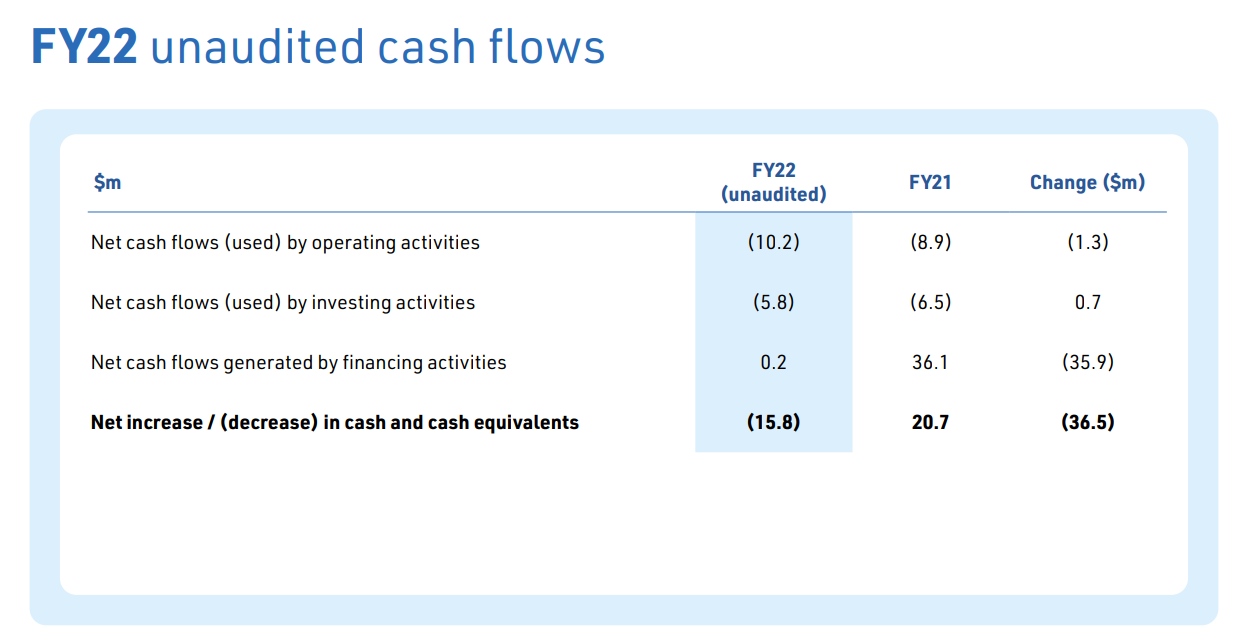

Cash Burn

MVP cash position is now 37m, free cash flow for this half was -11,604. Management still expect break-even / cash-flow positive in FY25.

For the US trials, they are currently assessing a funding plan. Currently the group has no planned capital investment activities and plans to seek partner or third party funding.

23 Half Year Results - Watch list

MVP announced it's half year results will be on Feb 24th. Thought I would do a straw on items I'll be looking out for in those results. All my watching is on the pain management side of the business (The Green Whistle) as I believe that is where the greatest opportunity lies (not in respiratory).

Progress to their strategic priorities in FY23

From the FY22 report, below are the strategic priorities for FY23

- Continue penetration of Penthrox in France

- Market entry planning for Germany, Italy & Spain

- Investment in direct in-market sales capability in Australia to drive penetration of Penthrox in hospital ED and the ambulance segment

- Further investment in platform capability to support growth

Continued penetration of Penthrox in France

France has a population size of roughly 65 million, as of FY22, MVP had 720 units sold per million population in France. This compares to 11,577 units per million population in Australia. There is considerable growth opportunity available, as part of this strategy management is expecting to sell circa 110k units in FY23, more than doubling FY22 sales (49k) but well short of the penetration of Australia.

Market entry planning for Germany, Italy & Spain

I’m not expecting too much here as the word “planning”. However there is opportunity for MVP in these markets. The population of these four is ~260 million, taking out France of ~65 million there leaves 195 million in the remaining 3 markets.

With Australia’s benchmark of 11,577 units per million population If these 3 markets get to that then that would be an extra 2.25 million units sold per year.

Direct in-market sales capability in Australia

MVP have now hired a direct sales team after taking the distribution rights back from Mundipharma in December 2020. I'll be watching to see how this translates to sales and turning around the recent decline in sales, two ways it might:

- Lock downs & Sell Through Over: The decline can be attributed to lock downs and Mundipharama selling through it's stock levels so hopefully they can get the levels back to FY20.

- Penetration in Emergency Departments: Secondly, MVP have said they want to target emergency departments. Currently the ambulance segment makes up around 75% of AU sales, roughly 223k units based on FY22 sales of 298k units. MVP believes the ambulance segment makes up roughly 31% of the market opportunity however there is 45% opportunity in Public ED departments.

Cash Burn

Cash burn, currently MVP has roughly 50m in cash. Management have expressed that they believe they will be cash flow positive in FY25 and the recent capital raise will get them to 2025 (with the options exercised). Study costs for the US trials will be around 12m.

China Exit

Lastly, my two cents on the recent decision to cease planned trials in China. I think this is a good idea to allow the company to focus on growth in existing markets. China is a very difficult market to get into with Medical Devices, not only is the registration time for foreign companies longer with the China FDA but China has a 2025 made in China vision (Article 104). Although I’m not certain article 104 would apply to MVP, if it does, manufacturing would have to be set up in the country which adds its own costs and risks.

The real potential here is the drug methoxyflurane and its penetration into the US and Europe.

A quick primer on the product:

Methoxyflurane provides rapid short-term analgesia using a portable inhaler device. Its primary role is in acute trauma but it might also be used for brief procedures such as wound dressing or for patient transport. It is a non-opioid alternative to morphine and is easier to use than nitrous oxide.

Methoxyflurane is a volatile anaesthetic originally used in the 1960s until it was found to be nephrotoxic at anaesthetic doses (typically 40–60 mL). Since the 1970s it has been used in Australia in lower doses for acute analgesia (up to 6 mL), largely by paramedic services.

Methoxyflurane is supplied with an inhaler device (Penthrox inhaler), which patients use to self-administer. It can be used by conscious haemodynamically stable patients, under supervision.

Pain relief begins after 6–8 breaths and continues for several minutes after stopping inhalation. Continuous use of methoxyflurane 3 mL provides analgesia for up to 25 minutes; a second 3 mL dose can be administered if required for up to 1 hour's analgesia. No more than 6 mL should be given in 1 day.

(from NPS.org.au)

From a medical perspective I see it as

- Safe (difficult to OD with minimal side effects)

- Effective

- Probably quite limited in its potential applicability

- Don’t have to be as worried about people stealing it as not typically abused

For over 10 years MVP have been probing its applicability into different settings and beyond prehospital it hasn’t really found decent traction.

This isn’t surprising to me as soon as you have IV access you likely have better / more familiar / cheaper options for acute analgesia. Essentially as a rule of thumb just assume anywhere an IV is likely to be in situ methoxyflurane isn’t going to be your first choice or even second choice (or your third choice if I’m honest) and this is in a country where it has been used for 30+ years.

If I had to say where I say applicability reducing dislocations in ED and prehospital minor trauma.

Therefore the company should focus on EDs and prehospital. Everything else is marginal at best and likely a waste of time and money. It could easily replace most nitrous oxide use in EDs and for quick pain relief and minor short procedures is a great option.

The reason I have become interested is management have been doing a lot of things that I like to see recently:

- Become more focused. Appears they have realized the value lies in the penthrox product so have ceased marginal business activities like a vet segment and an experiment in continuous flow manufacturing. These were unnecessary unprofitable distractions.

- Phase 3 clinical trial in US is actually approved and underway meaning a product launch in 2026 is a real possibility. The outcome of the trial, unlike many pharma trials is almost assuredly positive given its long history of clinical use in Australia and preexisting safety data.

- The company is well capitalized with $50mil in the bank which should get it through the trial and to US product launch.

- European expansion / distribution has been insourced and beginning to show real traction.

- There is strong insider alignment with ongoing insider buying and participation in capital raise and mostly at much higher prices.

Why now?

Losses have been exacerbated by a blowout in employee wages as they hire to begin direct sales at the same time as revenue falls on account of the previous distributor winding down stock. That will likely begin to work itself out this year with accelerating revenue growth. As the business metrics turn around I expect the share price will follow.

Price Catalysts

- Revenue acceleration

- Some sort of underlying profitability inflection once trial costs are excluded

- Phase 3 trial conclusion expected 2025: We basically already know the outcome but will still be a big day.

Downside

- $50mm in cash currently and $130mm MC suspect downside could be as low as $40mm so SP of ~$0.50

Upside

- More difficult but with growth in European segment and phase 3 US trial completion I can’t imagine a MC of less than $500mm due to the market size. Should equate to a share price of $5-6

I’m basically discounting the respiratory business as it appears only marginally profitable and if it were up to me I would look to sell it off.

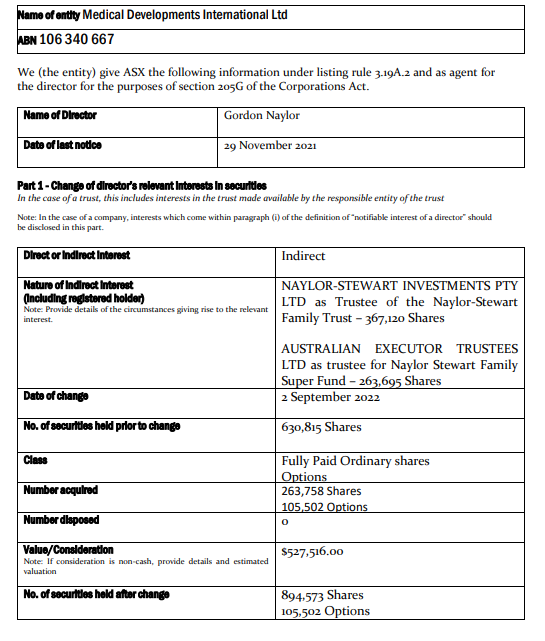

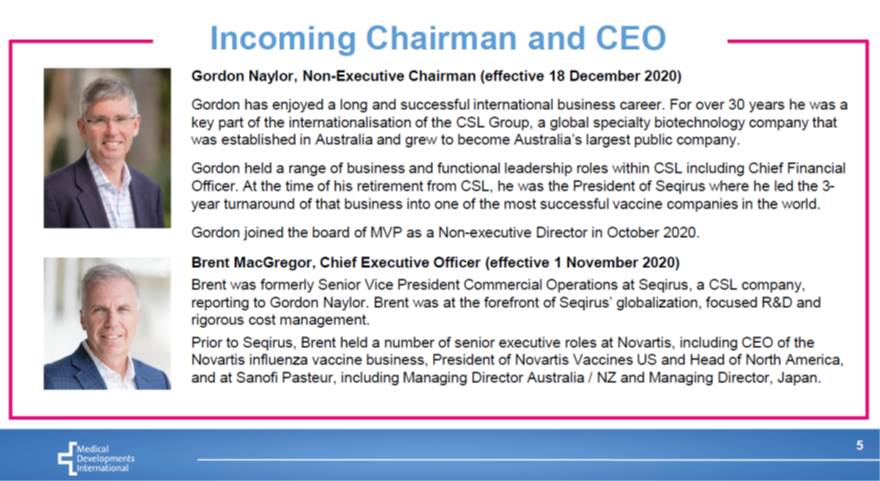

Gordon Naylor has doubled down *again* with MVP, buying up a further half a million in the most recent capital raise at ~$2 per share. This takes him to a total of ~1m shares/options, worth around $2m. I note that the first entry point was a $1m of shares when he first joint MVP, at a price of around $6 per share. So he would be heavily under water, and continues to buy up more.

While Gordon bought his shares when he started, Brent McGregor took a small pay and a large incentive based scheme. He has ~2m options that kick in at $8, $9, $10 and $11 per share, each 25% based on 1/2/3/4 years of service. So the long term view still remains in tack while insiders keep buying up.

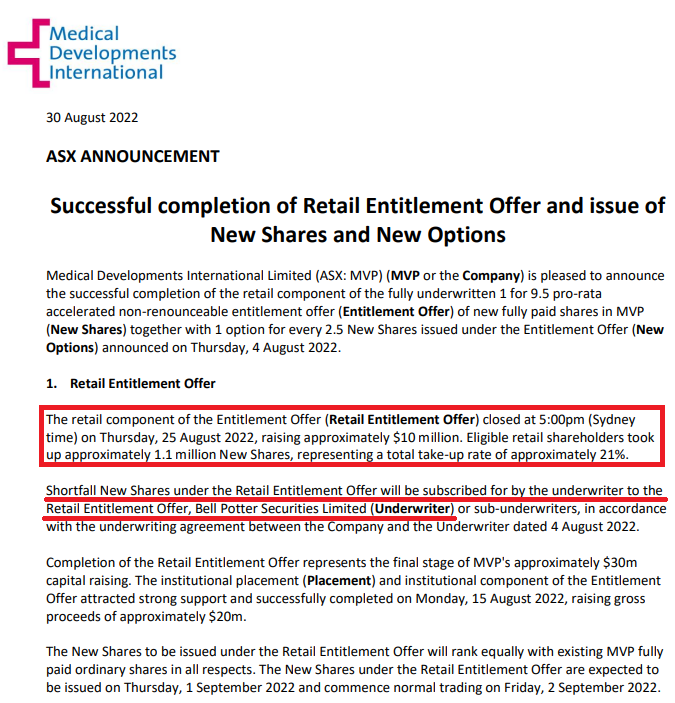

The retail entitlement offer closed, with only 21% take up. That is not surprising considering the shares have been trading at a discount to the offer, currently sitting around 12%. Why take up the offer when you can just go on the market and buy the shares?

That means that Bell Potter will need to underwrite ~$20m. And they are not going to want to be left holding the bag. So they are going to want to sell those shares over time no doubt. Which means, there could be further downward pressure on MVP. This is obviously exacerbated by the recent result which was not fantastic (Europe grew slower than expected, etc).

In terms of cash flow for MVP however, I think they will have enough cash to fund the expansion for some time. We shouldn't need to worry about further dilution unless there is a massive failure in the FDA approval process requiring an expanded clinical trial, or massive failure in the European scale-up requiring more SG&A without the incoming cash flow.

Howdy Strawfolks,,

The fourth stock in my Strawman Portfolio to start with is MVP. Now I am clearly a bag holder in real life and have lost money watching things unfold of late, but I believe the fundamentals and the investment thesis remains in place. If you wish to see my full analysis it is on another platform that remains nameless.

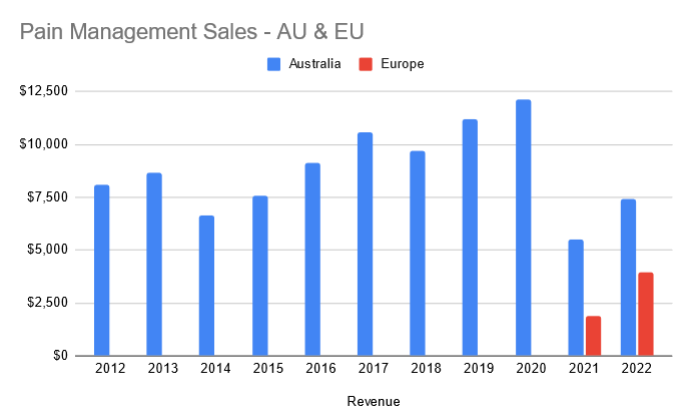

Penthrox European Sales

Penthrox is a great product and has been expanding it's sales. Even in the most recent FY22, it was +29% revenue which seems OK. But most of that is driven through European sales as Australia is largely a saturated market. The problem is that the distribution has severely been lacking over time, and this has been insourced to MVP now. So they are burning cash today to set up new sales teams, get new distribution/approvals in place in France etc, but the revenue will come later. And because Penthrox is a 2-year shelf life, it's actually got a decent recurring revenue once contracts with the likes of ambulances and hospitals are in place. But for now, they burn cash. And still, the European sales growth has been slower (35%) than expected. But there is a long runway and they just need to keep investing in this area.

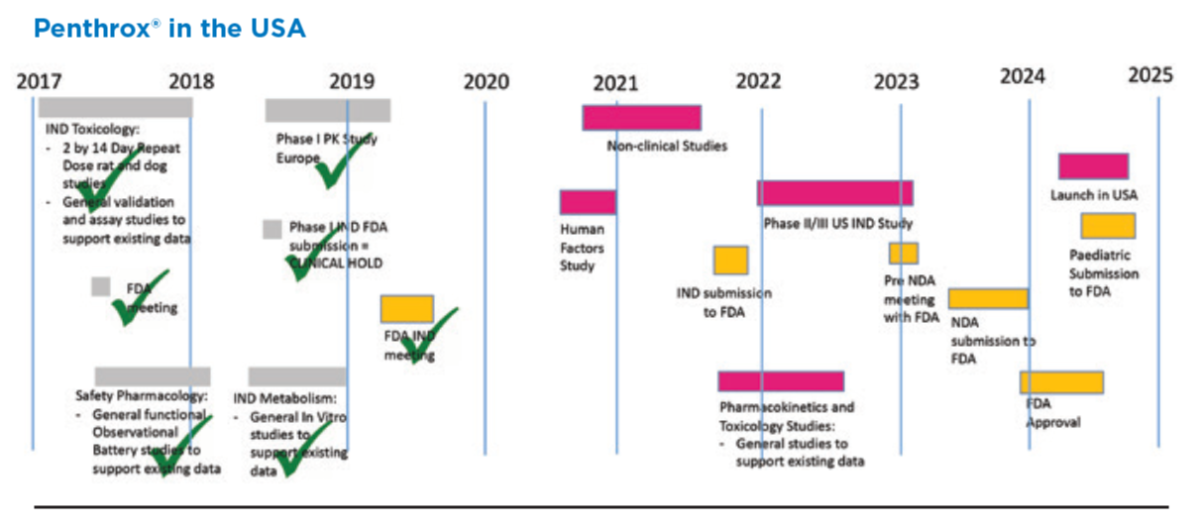

US-FDA Approval

The big fish of course is US-FDA. They recently secured the Phase 3 clinical trial approval, which should cost around $12m. It's a very small clinical trial because they get approval for most of the data they already have - that's a huge win. So now they are planning for the trials and results to be done in the coming years, and by FY25/26 they should be ready for approval and then distribution (all going well). If the SAM for the US is +$250m per year, as once mooted and prior to the expansion of use applications, then a rule of thumb for value is 3xSAM=$750m. That's the price that medical devices get bought out for. So this is a big part of the investment thesis. Note the picture below is 1 year old and there was a delay, but you can see the timeframe is for 2025 basically.

Expanded Applications

I am not sure how substantial this is, but the team at MVP think it is very important to expand the SAM by looking at further applications. This could include for example the use of Penthrox in day care surgery etc.

New Management

I have been fortunate enough to talk with Gordon and Brent, and I back their plans. They have a lot of experience with their work in Seqiris, and have a good team around them. Plus, they have performance rights that kick in at $11 per share, and they have bought substantial shares and taken low salaries. So they have huge skin in the game.

Risks? Cash burn.

The main risk is that they continue to burn cash to try and step-up their expansions. Or they don't get the FDA approval I suppose. But right now they have a cap raise at $2 which aint great for shareholders, but if the additional $30m gets them to scale up their European sales quicker, it should be worthwhile.

Placement at $2 then a proposed Retail SPP

Passing the hat around!!

Endo International plc to distribute Penthrox in Canada

- Release Date: 10/05/22 15:35

- Summary: MVP signs new Penthrox licensing agreement in Canada

- Price Sensitive: Yes

I thinking the share markets were bearish in May 2022..So MVP could get some momentum going forward..

25th July 2018: USA Update from MVP

Some may view this as a temporary setback, but MVP has fallen 19% since the 24th (the day before that announcement) from $5.85 to finish today (July 30th, 6 days later) at $4.74, after making a new year low today of $4.69.

It's been a bad year for MVP. They were trading as high as $8 during the first 3 months of 2018, and 4 months later they're 40% below those levels. Their trading update on the 14th May resulted in a 25% share price fall over 4 trading days:

14th May Trading Update from MVP

It makes me wonder how Penthrox, a self-medicating strong-pain-relieving drug widely used in Australia since the '70s, and now used extensively in over 15 countries worldwide, with very few adverse side-effects associated with short-term use (i.e. when used as intended) could concern the FDA this much. It's almost like the conspiracy theorists who contend that the FDA is run by US "Big Pharma" stooges to protect their own - might not be miles away from the truth...

I had a bad motorcycle accident 2 days before my 21st birthday and I sucked that green whistle dry - & had just started on a second one (after a lively argument with the ambos) when they got me to the local regional hospital. Ahh, the memories... 31 years ago - seems like yesterday. Even if I was mildly allergic to methoxyflurane (as I am to pethidine), I would still have used it - I was in that much pain. It works! I was actually pretty cheerful when we arrived at Bunbury Hospital.

Due to the risk of organ (especially kidney) toxicity, methoxyflurane (Penthrox) is contraindicated in patients with pre-existing kidney disease or diabetes mellitus, and is not recommended to be administered in conjunction with tetracyclines or other potentially nephrotoxic or enzyme-inducing drugs.

It's not always possible to fully screen patients in emergency situations (like in ambulances after accidents) for all of those conditions and existing medications.

The max recommended dose is 6 ml per day or 15 ml per week because of the risk of cumulative dose-related nephrotoxicity, and the inhaler should not be used on consecutive days. When used this way (as indicated), very few adverse side-effects have been observed.

The USA already has major issues with the illegal trade and use of Oxycodone ("Oxy") and other opioids and strong analgesics. Perhaps they're concerned with their own ability to control another one.

29-Oct-2018: SP now $4.40. More pain to come?