Top member reports

Straws

Sort by:

Recent

Content is delayed by one month. Upgrade your membership to unlock all content. Click for membership options.

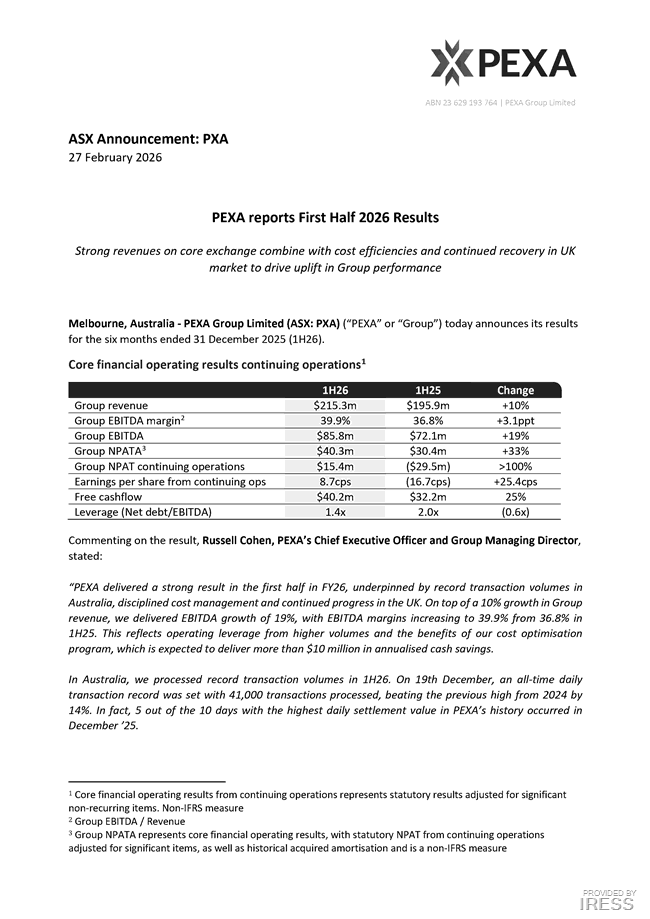

#1HFY26 Results

PXA has finally delivered a decent result (numbers below). No dividend but PXA has reduced leverage from 2x Net debt/EBITDA to 1.4x.

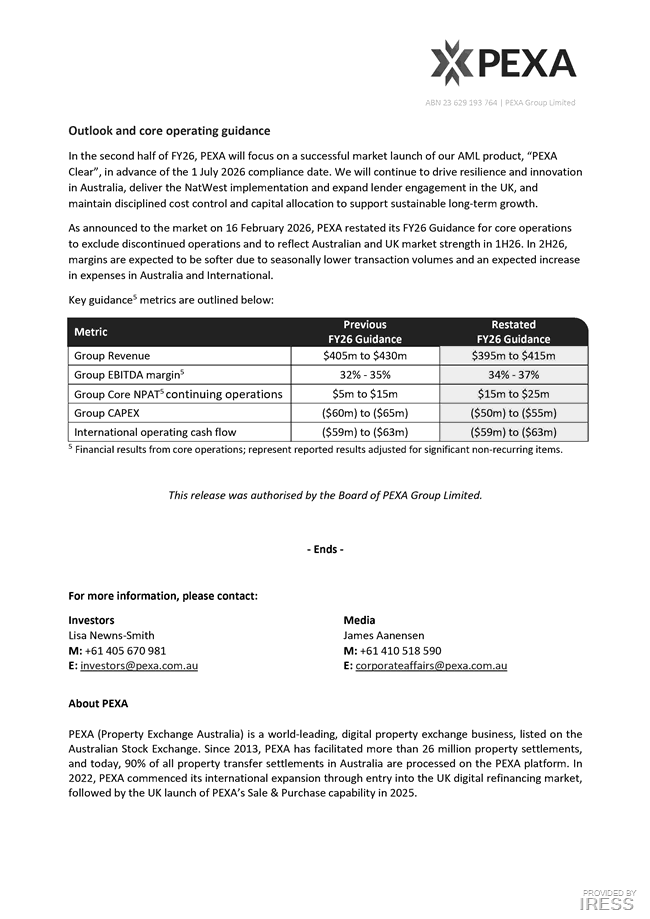

Revenue guidance for FY26 has been lowered but EBITDA margins have been revised up with higher underlying NPAT.

Market presently likes the result and guidance with shares up 7.69%.