Consensus community valuation

- Dividend payout ratio to increase from 40% in FY23 to grow towards 70% by 2026. Management says this is due to the need for acquisitional growth flattening. This is a change from the previous approach by management. However, maybe a more realistic expectation of where the business will get to and a better allocation of investor capital for maximum return.

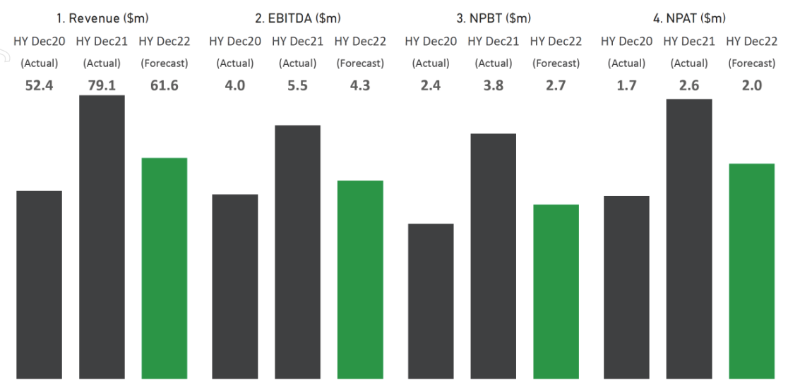

- H1FY23 outlook:

- Revenue looks like it will be significantly down from H1FY22. I didn't expect this. New structured products are a stated reason for the revenue drop, this was at Sequoia's election due to volatility of equity markets and interest rate uncertainty. This is affecting the "Equity Market" division.

- Abnormal item of remediation will affect the H1FY23 result.

- Company now has a $15m loan from ANZ, "on positive terms" which is available for acquisitions only. This is a positive outcome due to the low share price that would have made scrip highly dilutionary which the company is aware of. Management continuing to show they will allocate capital in a very focused and considered way.

- Morrison business continuing to increase market share in FY23.

- CEO states buyback has been slow on purpose to conserve cash for acquisition.

- CEO stated that SEQ is sometimes accused of doing too much. In his view this is wrong as the company's strategy is to provide as many services as possible to financial planners and accountants.

Overall, a negative outlook for the 1HFY23 results. Not so much expected so the company will have to be on watch as a result, do not buy more shares as a result.

Interesting re ASX dropping blockchain replacement to CHESS.

Morrisons (SEQ) I believe invested to prepare so hopefully can get a rebate as indicated below:

Per AFR

ASX is considering providing rebates to customers who have invested in building the replacement CHESS project.

ASX managing director Helen Lofthouse again apologised for the disruption, saying that the company is cognisant of the work customers have done on the project.

“One of the approaches you’ve seen us use when there are issues for our customers is we absolutely have gone through rebate processes from time to time to address customer issues.

“That’s certainly an approach that we’ve used in the past in this kind of situation.”

This has to be the most frustrating buyback, they start buying back at $0.57 but the share price falls a further 10% and they stop buying back shares despite using less than 7% of the facility. Do they see value in their own shares or not?

Reporting on the struggles of the financial advice industry - The profit struggles of financial advice licensees laid bare - Financial Newswire. I know for a fact that many publicly listed companies are trading at lower than private market multiples making the typical rollup strategy untenable.

Sequoia has been in a trading halt for the last couple of days pending an acquisition announcement. This morning they announced they were acquiring three business, including Sharecafe, which I'm sure some of us have used as an ideas generator/validator. These businesses will fall under Sequoia's Direct division. The release gives a decent explanation of each business and interestingly it spends some time talking to the credentials of the key personnel who are staying on with Sequoia, including Tim McGowan who will now head up the Direct division.

The price seems reasonable without being outstanding. It is largely script based though and is perhaps a little disappointing as the CEO made a point of saying right up until recently they weren't interested in diluting shareholders in acquisitions at the current share price. The share price hasn't really moved on the news and I would say that's a lot more reflective of what we're seeing more broadly in the market - compared to last year - where it now recognises both the opportunity and the risk that comes with acquisitions.

Overall I think it's a nice little announcement in line with their overall strategy for both organic and acquisitive growth, that gets them that little bit closer to their FY25 $400m revenue target.

[Held]

Overview:

Sequoia Financial Group provides products and services for ASFL holders, accountants and financial advisors. The company is split into four divisions:

- Wealth - Wealth advisor business, providing licensee services to financial advisors.

- Professional Services - Provides back office/admin type services for accountants and financial planners. For example, access to legal documents or SMSF administration on their behalf.

- Equity Markets - ASX clearing for 55 ASFLs. Morrisons is the main business in this segment. Trades for higher values with average orders of around $100k. Ie not for day traders/Selfwealth type clients but professionals and high net worth individuals. Competitors are Openmarkets and Finclear.

- Direct - News type business, seminars and newsletters.

CEO is an ex-financial advisor. Very passionate about non-conflicted advice. Sequoia does not sell any financial products (such as funds) to clients they only provide services to the financial advice industry. SEQ has been growing rapidly in recent years with CEO’s plan to continue this growth through organic means and acquisitions of businesses at 4-7x PE using the cashflows of the business. The four different segments of the business create the ability to cross sell all the different products that SEQ produces.

The value proposition of SEQ is that they are the "picks and shovels" for financial services industry. They provide products that enable financial planners and accountants to be able to provide advice services at a cheaper price or saves them time.

Main Thesis:

- CEO that thinks as a capital allocator, has experience in the field and has high insider ownership of the company. Therefore, strongly aligned with shareholders. The CEO talks about being the tortoise not the hare, compounding returns over time. Management is looking to take the operating cashflows of the business to buy cheap businesses that are earnings accretive to further increase the growth of the business.

- Growth in revenues and profitability appears consistent and likely to continue moving forward.

- The company's share price has good upward momentum (and unchanged during current market ups and downs).

- The diversity of revenue sources and high friction costs of moving to competitors

- Company appears undervalued at current earnings. If SEQ is able to achieve or even make it halfway to the compound growth goals management have set out, there is a high upside potential. The growth doesn't appear to be priced in.

- Sum of all parts of the company, appear undervalued. Morrisons, for example, has competitors that are less profitable but valued higher than what SEQ share price implies.

- Advisors are leaving the big banks and conflicted firms. Independent financial advice after the Royal Commission is the way forward for the industry. SEQ is perfectly positioned for this pivot.

- A company that can be held for a long time as management has a clear path to create long term compounding returns.

General Notes:

- There is normally seasonality to the earnings of the company. There is a tendency that bills are paid near the end of the financial year.

- Management’s goal is to increase revenue to $400 million by the end of FY2024.

- Key goals of board and management:

- While they are in the advice industry, profitability doesn't appear to be clearly linked to funds under management as they are the licensor for advisors. FUM could affect Morrisons business.

- Company reports "Operating Profits"/EBITDA. This is a reasonable figure to see the underlying profitability of the company year to year.

- Wealth division doesn't lock financial planners in with high upfront or exit fees. CEO states they don't want planners that don't want to be with them.

- CEO keen to take questions and hear from shareholders during AGM presentation.

- 15% growth expectation of management doesn't include acquisitions.

- FY22 will be the first year of the family office business, a new segment for the business.

Positives:

- CEO talks about Warren Buffett, obviously a big fan and looks to allocate capital in the same way.

- Strongly cash flow positive. This cash flows facilitates the purchases of business at low PEs (4-7x) which will compound growth into the future.

- Consistent revenue growth over the last 5 years from $23 mil in FY16 to $116 mil in FY21.

- A good likelihood of their being a shortage of advisors in the future due to current change in the industry.

- Advisors that are licenced through SEQ are not conflicted trying to sell products from SEQ.

- Strong ability to cross sell the different products across the different units of the business. For example, the advisors licenced under the wealth division can be sold the services offered by the professional services division.

- Consistent share price momentum since May 20. Steady bottom left to top right movement. The share register is very tight with only 600-700 shareholders.

- CEO owns approximately 9% of the shares of the company. Is very aligned with shareholders and has experience in running businesses (he sold his previous financial advice business).

- CEO has made recent on-market purchases.

- Company appears to have hit a point of operating leverage with increasing revenues resulting in larger increases in profitability.

- Net cash position. However, can't use all cash and cash equivalents to calculate enterprise value as a large portion of the funds are client’s funds not for company use. Additionally, company must have $7.5 mil available, a requirement for the Morrisons business.

- Company report states non-cash return on equity for all divisions was above objective of 15% in FY21.

- Stock on HIN (Equities division) in FY21 went from $1.5 billion to $4 billion.

- While revenues and profitability increased strongly over the past year head office costs are flat.

Negatives/Risks:

- Key man risk with CEO. Seems to be the driving force. However, high ownership lowers this risk.

- As the company continues to buy businesses it becomes too bloated with all these consolidated small companies. What may have worked as a small company might not work well in a large group. Need to monitor how integration works.

- Low liquidity. Average around $15K a day and a low number of transactions. Shareholders around 600-700.

- Financial planner numbers under the Sequoia licence don't increase. There is currently an exodus in the industry of planners (generally conflicted planners).

- This is a low gross margin business. Though improving with increasing revenues.

Valuation Metrics:

For valuation see valuation straw.

- Can’t use basic cash figure for EV calculations. Need to take out client cash that can’t be used by the business.

- Operating EBITDA is very similar to operating cash flow.

- Info for ratios using FY21 figures:

- Share price = 68c

- Market cap = $89.89 mil

- Cash = $13.3 mil (not counting client cash)

- EV = 89.89-13.3 = 76.59

- "Operating profit" / EBITDA = $11.5 mil

- NPAT = $5.55 M

- EBIT = $8.1 M

- Operating Cash flow = $15.5 M

- Equity = $41.1 M

- Ratios:

- PE = 89.89/5.55 = 16.2

- EV/E = 76.59/5.55 = 13.8

- EV/EBIT = 76.59/8.1 = 9.5

- EV/FCF = 76.59/15.5 = 4.9

- EV/EBITDA = 76.59/11.5 = 6.66

- ROE = 5.55/41.1 = 13.5%

- ROE (non-cash company measure) = 5.55/27.8 = 19.96%

- NTA per share = 10.4c

- P/B = 89.89/41.1 = 2.2

How I expect this will play out:

- SEQ will keep growing at a minimum of 15% with greater growth to come from acquisitions or outperformance of expectations.

- With the stable growth trajectory and great capital allocation focus of the CEO, I will be looking at SEQ as a long-term holding stock due to the potential for compounding returns.

- How profits will increase in the future:

- Acquisitions that are made using the cash flows off the business.

- More financial planners use Sequoia as licensees.

- Greater trading volumes for Morrisons.

- General move by consumers towards non-conflicted advice.

- Increase the number of docs they create through their professional services division.

When to get out:

- Management heavily reduces the revenue/profit expectations.

- Revenue or profit growth stops.

- CEO selling sizeable portion of shares.

- High valuation ($2+) = trim.

Management Medium Term targets from their September Presentation. They have lowered the 2024 goal from 1200 to 1000 advisers recently, but are ahead 2021 target.

If this is what success looks like, then SEQ could easily have a market capitalisation over $400 M in 3-4 years. I would be happy if they get to $250 M by 2024.