Consensus community valuation

19/02/2026

For full explanation of assumptions see my straw “1H FY26 Results”

Looking forward I am now expecting FY26 NPAT to be higher than current consensus of $40 million. Over the last 4 years (on average) the first half contributed 66% of the earnings, while the second half contributed 34% of the earnings. With group revenue up 13.5% on pcp in first seven weeks of 2H26 and I expect NPAT in 2H FY26 will be similar proportionately to previous years, ie 34% of the full year earnings, or approx $14.6 million. This puts FY26 NPAT in the ball park of $43 million and EPS at 55 cps (up 8% on consensus).

Over the l last 5 years UNI has traded on a PE between 10 and 27, with a midpoint of 18. Working on 18 times estimated FY26 EPS of 55 cps, that puts UNI on a valuation of $9.90.

Using McNiven’s Valuation formula assuming equity of $2.10 per share (calculated from 1H26 financial report), ROE of 26.2% (based on FY26 EPS of 55 cps), 30% of earnings reinvested, fully franked dividends and a required annual return of 10% (ROI), I get a valuation of $9.80.

Jarden analysts said today that net profit beat consensus expectations by about 7% and have a price target of $10.69. https://www.fool.com.au/2026/02/19/universal-store-trading-higher-as-profits-beat-expectations/

I’m going to increase my valuation from $9 to $10 per share and would be looking to add shares under $8.50 and start lightening off above $11.50 per share.

23/10/2025

For a few years now I think Universal Stores have been one of the best performing retailers on the ASX. All the metrics have been improving and I don’t see that changing in FY2026 as management continue with their store rollout.

The Perfect Stranger stores have been a standout and the revenues have been growing exponentially in the early roll out stages. They now have 19 PS stores and are planning another 5 to 7 in FY26.

The FY26 year started strong with Like-for-like sales up strongly across all stores.

FY2025 ROE was 24% and could be c. 29% in FY2026. The business is debt free with $17 million cash on hand. It has strong free cash flow.

Analysts are forecasting c.16% earnings growth going forward and a consensus price target of $10. Forecasts are for FY26 EPS of 51 cps. At a valuation of $9 that puts UNI on a forward PE of 17.6x. Currently the stock is trading on a multiple of 19.5 times FY25 earnings.

Using McNiven’s Formula and assuming forward ROE at 29% and a minimum annual return of 10%, I get a valuation $9.30. It could be worth paying up a little for a business with strong metrics that continue to improve!

Given the outstanding performance of UNI when many retailers are struggling at the moment, I’m going to lift my valuation to $9.00. At the current price of $8.75 it’s a HOLD for me.

Held IRL

19/09/2025 - Valuation $8.80, Current share price $8.77

It’s been over 12 months since I’ve reworked my valuation for Universal Store Holdings (UNI). Now with a market cap of $650 million, UNI has been a solid performer since we added shares IRL two years ago.

UNI reported another great result for FY2025:

- Group sales of $333.3 million, +15.5% versus prior corresponding period (“pcp”):

- Universal Store (“US”) sales of $280.9 million (+15.0% vs pcp), like-for-like (“LFL”) sales +13.0%

- Perfect Stranger (“PS”) sales of $25.5 million (+83.1% vs pcp), LFL sales +25.5%

- CTC sales of $40.1 million (-9.8% vs pcp), DTC LFL sales +2.9%1

Gross profit margins +100 basis points vs pcp, to 61.1%

Underlying earnings before interest and tax (“EBIT”)2 of $54.6 million, +15.9% vs pcp

Underlying net profit after tax (“NPAT”) 2 of $34.8 million, +15.2 % vs pcp

Statutory NPAT of $23.3 million (-32.3% vs pcp) includes H1 FY25 $13.6 million CTC impairment charge

Underlying earnings per share (“EPS”) of 45.4 cents per share (“cps”)3, +14.6% vs pcp

16.5 cps fully franked final dividend declared, taking full year dividends to 38.5 cps (+8.5% vs pcp

Underlying cash flow from operations4 of $98.0 million, +23.3% vs pcp

111 physical store locations as at 30 June 2025, comprising 84 Universal Store, 19 Perfect Stranger and 8 THRILLS stores

Earnings, margins and ROE have all improved on last year.

26/08/2024 - Valuation $6.50, Current share price $7.00

Universal Stores reported a strong FY2024 due to a better than expected second half. Statutory EPS was 44.7 cps, beating guidance and up 45% on last year. Underlying EPS was 39.6 cps, calculated from underlying NPAT and the weighted average shares outstanding during the period (76.3M FY24 vs. 73.6M FY23).

Here are the Highlights:

• Group sales of $288.5 million, +9.7% versus prior corresponding period (“pcp”), reflecting strong trading performance, with increasing momentum throughout the financial year

• Gross profit margins +110 basis points versus pcp, to 60.1%

• Underlying EBIT of $47.1 million, +16.6% versus pcp

• Statutory net profit after tax (“NPAT”) of $34.3 million (+45.3% vs pcp)

• Underlying earnings per share (“EPS”) of 39.6 cents per share (“cps”)

• 35.5 cps fully franked dividend determined (final dividend of 19.0 cps)

• Net cash of $14.3 million as at 30 June 20243

• 102 physical store locations as at 30 June 2024, comprising 80 Universal Store sites, 14 Perfect Stranger sites, and 8 THRILLS stores

The FY25 Trading update & outlook also looks very positive as seen in the sales performance during the first seven weeks of FY25:

• US sales up +15.3%, with LFL growth up +12.5%, cycling -9.0% last year

• PS sales up +89.9%, with LFL growth up +24.2%, cycling +4.9%

• CTC’s sales in the DTC channels up +13.3%, with LFL up +22.4%, cycling +4.1%

Looking ahead management expects a further four to six Universal Store sites in FY25, plus four to six new Perfect Stranger stores as well as one to three new THRILLS stores.

The Group will continue to enhance gross margins by ensuring fresh and appealing stock, while introducing new brands and products to engage its customers. Prioritising CODB reduction through optimised productivity continues to be a focus. Additionally, investment in new stores and technology upgrades will further support long-term sustainable growth.

Summary

I like what management have been doing with the business and they seem to be ahead of the game when it comes enhancing value through brand positioning and store roll outs. The Perfect Stranger brand is showing exceptional growth.

Universal Store’s customers are a younger demographic and seem to be less affected by higher interest rates and mortgage payments. It is one retailer that is still growing in spite of the pressures on household budgets.

It would seem at this early stage that Universal Stores is in for a year of high single digit EPS growth with forward ROE over 24%.

Valuation

Using McNivens Formula and assuming the following: shareholder equity of $2.00 per share (up from $1.78 at 30/06/23), forward ROE 24%, 20% of earnings reinvested at 24%, 80% of earnings paid out as fully franked dividends (currently 5%, or 7.2% gross yield), and requiring a 12% annual return I get a valuation of $6.50.

At the current share price of $7.00 you could expect an annual return of over 11% providing the business can maintain an ROE of 24% from here.

Held IRL (2.2%)

23/07/2024

While most analysts have set a PT for Universal Stores at close to $6.50 (@Remorhaz‘s post https://strawman.com/member/forums/topic/9390?post=27623#post-27623), I’m not quite as enthusiastic. I like to leave a good margin of safety with retailers because consumer demand and sentiment can change quickly. Universal Stores is also a new kid on the block (excuse the pun)!

Universal Stores doesn’t have a long history of PE ratios to go on, so I would prefer to look at ROE stability and base my valuation on that. I expect FY24 ROE to be close to 22%. The business seems to be maintaining ROE at around this level over the last 4 years.

Modified from Commsec chart

If UNI can maintain ROE at 22%, and at a share price of $5.70 I think the business could return investors almost 12% per year going forward based on McNiven’s Formula. I am expecting this to come as a 7% grossed up yield (includes franking credits), and 5% growth. This is likely a bit conservative, but I prefer to be a bit conservative when building a position in a retailer to allow for the unexpected.

Held IRL (1.9%)

20/03/2024

Following a strong 1H24 result, and a promising trading update for the first seven weeks of 2H24, the share price has increased from $4.00 to $5.24 (up 31%). My previous valuation for Universal Store Holdings (UNI) in January this year was $4.40. Has the share price got ahead of itself, or has the business outlook materially improved to justify a higher valuation?

For 1H24 sales were up 8.5%, gross profit margins increased +80 points to 59.7%, and NPAT was up 16.7% pcp to $20.7 million, and adjusted earnings per share 26.6 cps. They held net cash of $27 million. A nice fully franked 16.5 cps dividend was declared (3.5% yield, 5% gross) up 18% pcp, and that’s for the first half only!

Six new stores opened, three of these were Perfect Stranger stores which are doing exceptionally well.

The Universal Store (US) has performed OK in a challenging half for retailers, but sales were down 1.4%. The absolute standout for UNI has been the Perfect Stranger (PS) stores. Sales growth has been exceptional.1H24 sales were $6.6 million, up 59.7% pcp. There are currently 11 PS stores, and there are plans to open another 4 - 8 stores in 2H24.

UNI have experienced uplift in sales in US (4.5%) and PS stores (56.5%) for the first seven weeks of 2H24. CTC sales are down 0.5%.

Consensus is for FY2024 NPAT of $28.46 million, or $7.76 million NPAT generated in 2H24 (27% of full year sales). This equates to $0.37 per share.

Consensus is for FY2024 NPAT of $28.46 million, or $7.76 million NPAT generated in 2H24 (27% of full year sales). This equates to $0.37 per share.

Valuation

Shareholder equity has increased to $151.3 million at 31st December 2023, or $1.97 per share. Consensus NPAT is $0.37 per share, and therefore ROE should be c. 19% this year. Assuming further rollout of the high performing Perfect Stranger stores, we could see ROE lifting to +20%. This is inline with analyst consensus and historical ROE over the past 3 years:

Source: Commsec

Using McNiven’s formula assuming Equity of $1.97 per share, ROE of 20%, 30% of Earnings reinvested, 70% of earnings paid out as fully franked dividends, and requiring an annual return of 12%, I get a valuation of $4.93, say $5.00. At a 11% required return the valuation would be $5.54. At $5.00 that puts UNI on a PE of 13.5, which is at the lower end of PE over the last 3 years.

Held IRL (1.4%)

January 2024

Universal Stores passes all my investment filters and I added some IRL on a dip in October 2023. Over the next few years I am expecting double digit earnings growth due to continued store rollouts and a forward ROE of over 20% (providing we see a soft landing in the economy). It has a very healthy balance sheet and holds more cash ($21 million) than it has debt ($15 million). I expect it will pay a 5% fully franked dividend in FY24 at a 70% payout ratio.

Like Lovisa, the Universal Store attracts a younger demographic seeking the latest fashion wear.

On a forward PE of 13x (FY24) and a PEG ratio (PE/earnings growth) of 1.2, the share price still looks reasonable at $4.40 (providing double digit earnings growth continues).

Using McNiven’s formula Universal Stores could return investors over 12% per year based on the current share price of $4.40. For an 11% return you could pay up to $5.00 per share. For a better margin of safety, I’d prefer to add shares at around $4.00, or better still wait until the next trading update and reassess expected FY24 earnings.

Held IRL (1.2%)

I was very pleased with the Universal Stores 1H26 results today. The highlights of the announcement and CEO Alice Barbery’s comments are included at the end.

Universal Stores has performed better than I was expecting prior to the results with 1H26 NPAT of $28.3 million (Underlying up 22% pcp).

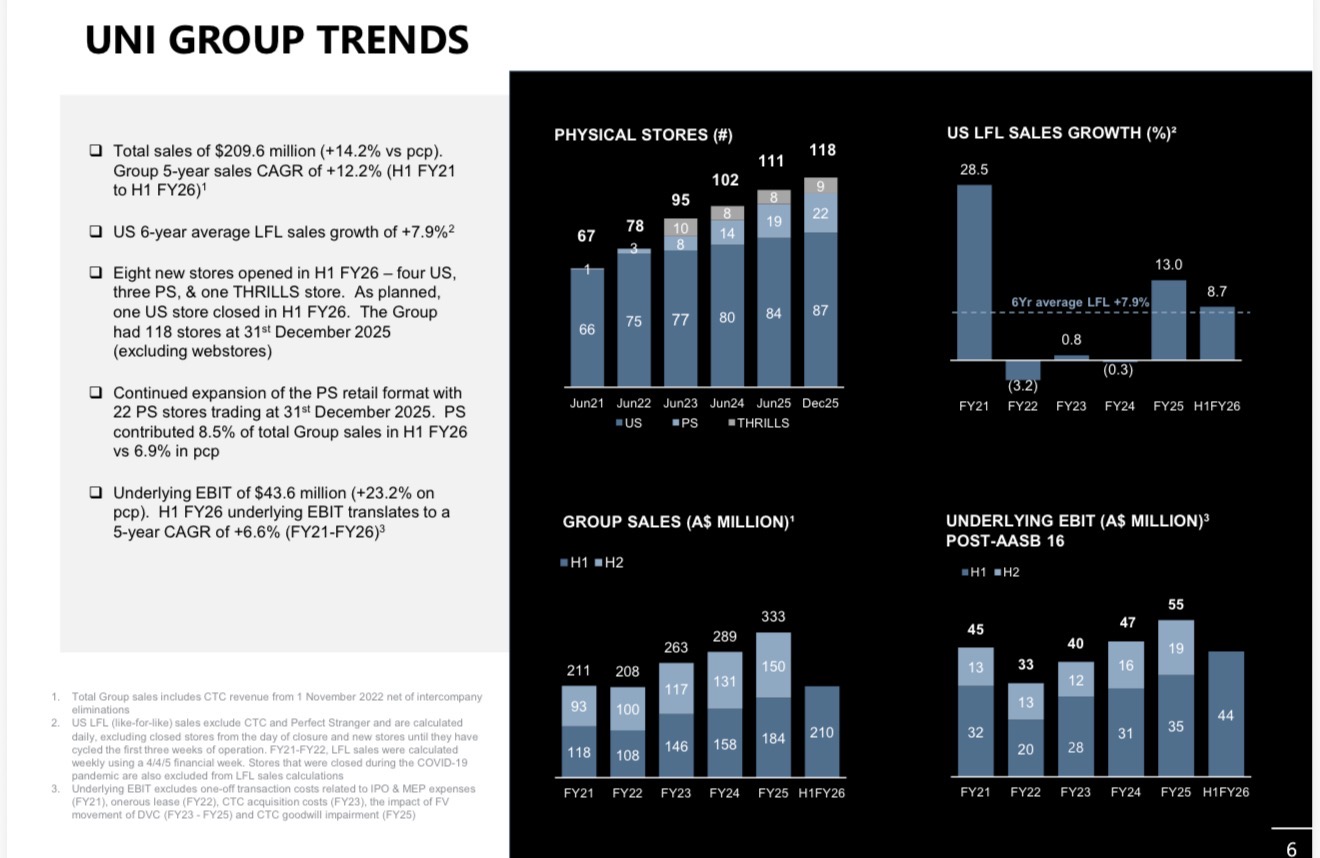

Group new store rollout is on track to achieve previous market guidance of 11 to 17 in FY26. Eight stores opened in H1 FY26 with five stores confirmed for H2 FY26 – four PS and one US store.

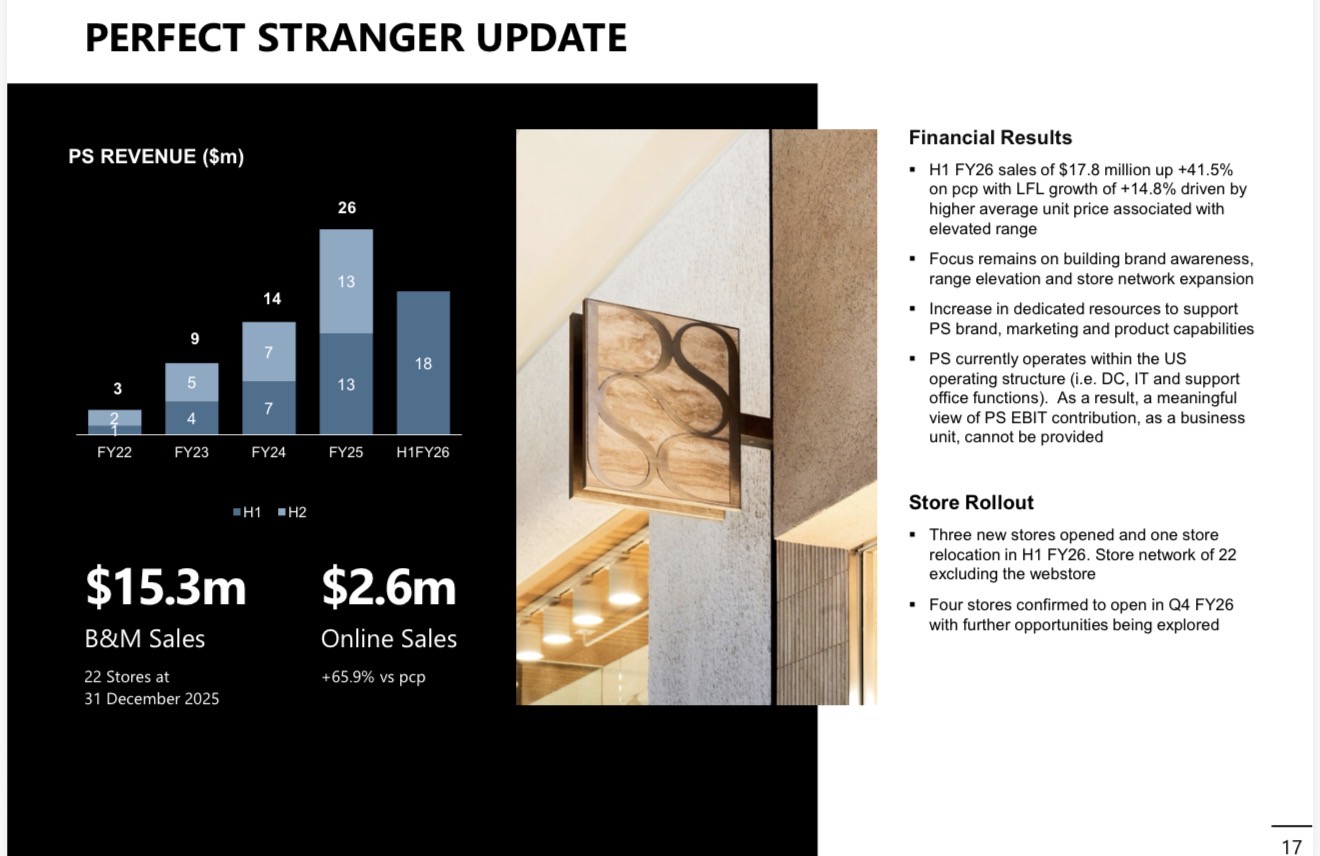

The Perfect Stranger stores have been an outstanding success and are contributing strongly to accelerated earnings growth and to improving gross margins. FY26 should see PS revenue 12 times higher than in FY22. With 4 new PS stores planned in Q4 FY26, PS with its outstanding metrics will become a larger contributor to group earnings going forward.

Currently PS contributes only 8% to group sales. However management are focusing on the higher margin labels with 4 out of the 5 stores proposed in Q4 FY26 will be PS.

Looking forward I am now expecting FY26 NPAT to be higher than the current consensus of $40 million. Over the last 4 years (on average) the first half contributed 66% of the earnings, while the second half contributed 34% of the earnings. With group revenue up 13.5% on pcp in first seven weeks of 2H26 and I expect NPAT in 2H FY26 will be similar proportionately to previous years, ie 34% of the full year earnings, or approx $14.6 million. This puts FY26 NPAT in the ball park of $43 million and EPS at 55 cps (up 8% on consensus).

Valuation

Over the l last 5 years UNI has traded on a PE between 10 and 27, with a midpoint of 18. Working on 18 times estimated FY26 EPS of 55 cps, that puts UNI on a valuation of $9.90.

Using McNiven’s Valuation formula assuming equity of $2.10 per share (calculated from 1H26 financial report), ROE of 26.2% (based on FY26 EPS of 55 cps), 30% of earnings reinvested, fully franked dividends and a required annual return of 10% (ROI), I get a valuation of $9.80.

Jarden analysts said today that net profit beat consensus expectations by about 7% and have a price target of $10.69. https://www.fool.com.au/2026/02/19/universal-store-trading-higher-as-profits-beat-expectations/

I’m going to increase my valuation to $10 per share and would be looking to add shares under $8.50 and start lightening off above $11.50 per share

Held IRL (3%)

H1 FY26 Highlights:https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-03058294-2A1654439&v=undefined

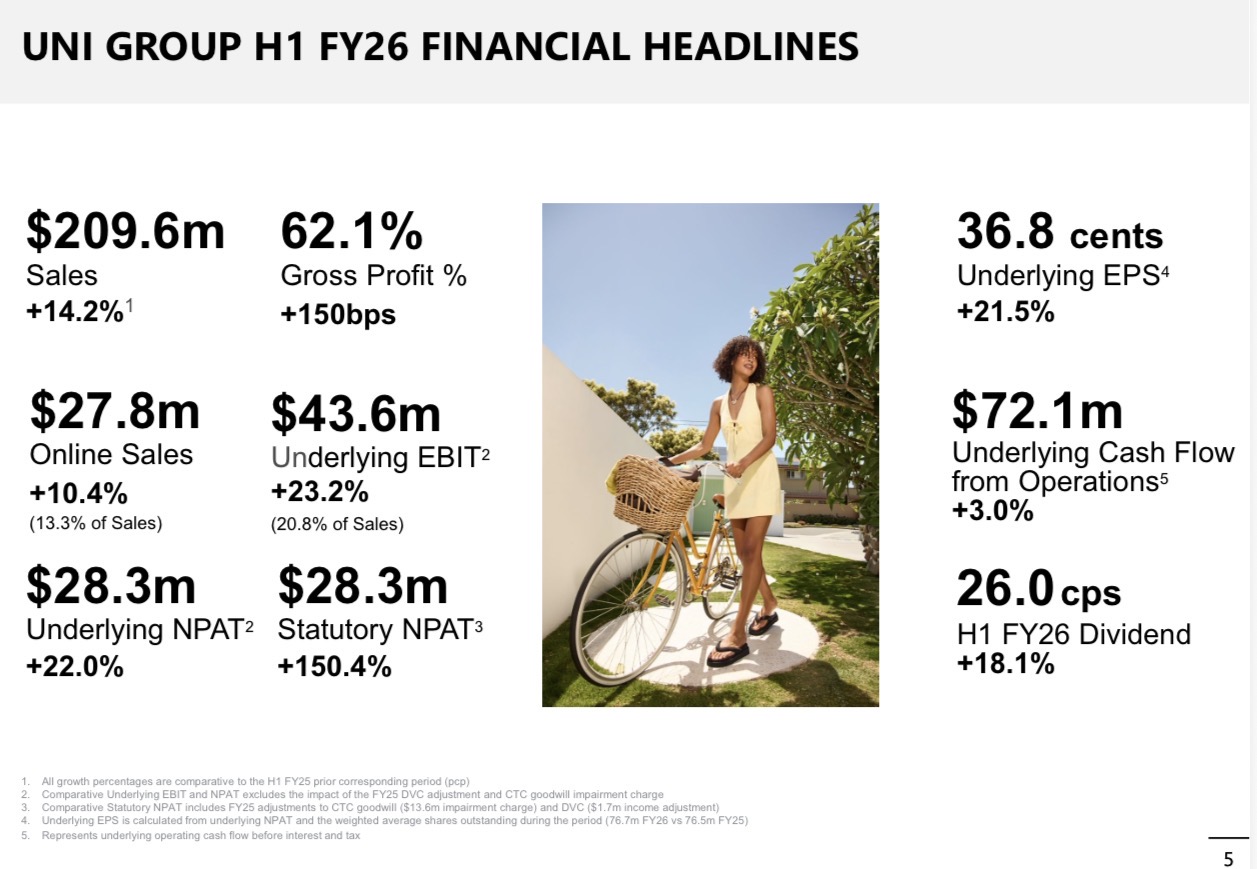

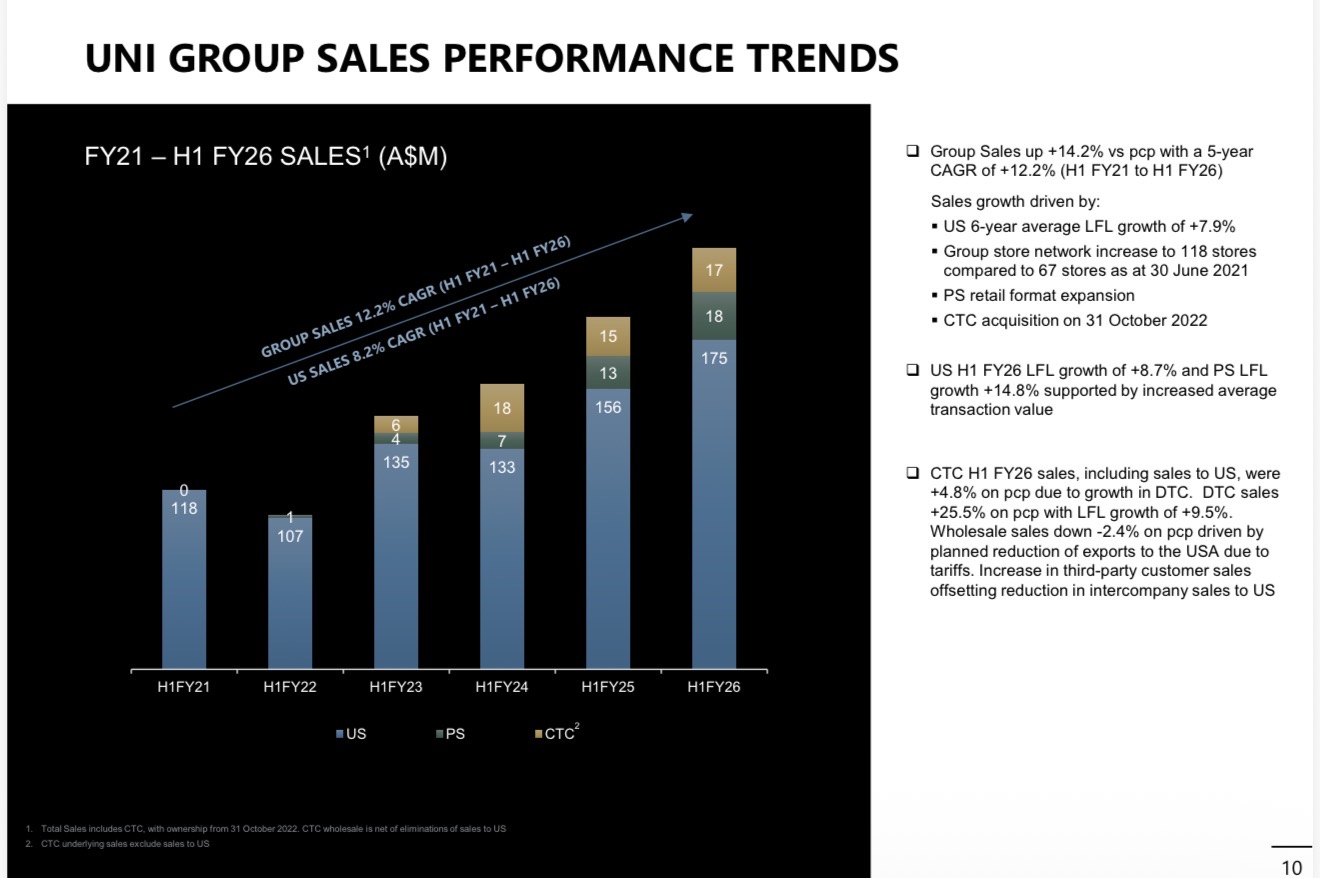

- Group sales of $209.6 million, +14.2% versus prior corresponding period (“pcp”):

- Universal Store (“US”) sales of $174.8 million (+11.9% vs pcp), like-for-like (“LFL”) sales +8.7%

- Perfect Stranger (“PS”) sales of $17.8 million (+41.5% vs pcp), LFL sales +14.8%

- CTC sales of $23.2 million (+4.8% vs pcp), DTC LFL sales +9.5%

- Gross profit margins +150 basis points vs pcp, to 62.1%

- Underlying earnings before interest and tax (“EBIT”)2 of $43.6 million, +23.2% vs pcp

- Underlying net profit after tax (“NPAT”) 2 of $28.3 million, +22.0 % vs pcp

- Statutory NPAT of $28.3 million (+150.4% vs pcp)

- Underlying earnings per share (“EPS”) of 36.8 cents per share (“cps”)3, +21.5% vs pcp

- Fully franked interim dividend of 26.0 cps determined, +18.1% vs pcp

- Net cash of $38.4 million as at 31 December 20254

- 118 physical store locations as at 31 December 2025, comprising 87 Universal Stores, 22 Perfect Stranger and 9 THRILLS stores

Commenting on the H1 FY26 results, Group CEO, Alice Barbery said: “The Group delivered a solid first half result, with robust sales growth and gross margin expansion. This growth reflects the team’s continued excellence in providing our customers with on-trend products for their occasions, a service-oriented experience and engaging communication. We note that the youth fashion customer remains discerning, choosing to spend on quality, on-trend clothing from brands they love. The Group continues to focus on cost discipline as we build our team and system capability to support our future growth.

CTC (THRILLS) performance

CTC H1 FY26 total sales of $23.2 million was +4.8% above pcp. This increase was driven by direct to customer (“DTC”) channel growth of +25.5% partially offset by a -2.4% decrease in the wholesale channel.

The Retail strategy is progressing with improvements in store execution, product curation and fast to market mindset. Brand and product positioning has been aligned with historical brand values. The decline in wholesale sales was driven by planned reductions to USA exports due to increased tariffs. Increase in third-party customer sales has offset a reduction in intercompany sales to US. Collectively, the CTC brands

(THRILLS and Worship) represented ~9% of US format sales versus ~12% in pcp.

CTC H1 FY26 gross margin of 46.8% was 150 basis points above pcp due to a higher retail sales mix and improved price management.

One new store opened in H1 FY26 resulting in a CTC network of nine stores as at 31 December 2025, excluding the webstore.

FY26 trading update & outlook: weeks 27 to 34 (H2 FY26 to date)

Group FY26 to date6 DTC sales are up +13.5% on pcp and broken down below:

- US total sales growth of +11.4%, LFL sales +7.1% (cycling +22.5%)

- PS total sales growth of +39.0%, LFL sales +4.9% (cycling +38.8%)

- CTC total sales growth of +14.6%, LFL sales -10.2% (cycling +37.8%)

THRILLS retail stores continued to deliver a strong performance with LFL growth of +18.0%. Online sales were -31.7% with reduced promotional and clearance activity.

Group new store rollout is on track to achieve previous market guidance of 11 to 17 in FY26. Eight stores opened in H1 FY26 with five stores confirmed for H2 FY26 – four PS and one US store. Management continues to pursue additional new store opportunities being prudent to ensure long-term profitability.

Management notes the increase in interest rates and the strengthening AUD/USD exchange rate. The Group maintains a disciplined approach to hedging foreign currency risk and product pricing. Management expects continued volatility in CTC wholesale sales as H2 FY25 USA sales are cycled. The CTC wholesale channel represents less than 5% of Group sales, net of intercompany eliminations.

Universal Stores (UNI) reported a strong 1H24 result today sending the share price up 15%. Sales were up, gross profit margins up, NPAT up 16.7% pcp, net cash of $27 million, 6 new stores opened (3 Perfect Stranger which are doing exceptionally well). Nice fully franked dividend declared yielding 3.5% (5% including franking credits) for this half only! :) They generally plough back c.30% of their earnings back into growth and that’s likely to be on a ROE upwards of 20%.

I tuned into the end of the webinar during question time (following the Lovisa call) and I was blown away by the enthusiasm of these two young women leading the Universal team. They really have their heads around the business, their passion and smiles were infectious, and the business culture at Universal seems to be really positive. I am pleased I invested when the market was negative on their prospects.

CEO Alice Barberry, and CFO Renee Jones at the results webinar this morning (22/02/2024)

Commenting on the results, Alice said:

“The results in the half demonstrate our resilience and ability to manage our business as macro-economic conditions fluctuate. Our team has successfully managed margins, inventory, and operating costs to deliver earnings growth in a difficult and subdued consumer spending environment. Our growth ambitions for Universal Store remain unchanged, as does our long-term strategy.

I am also pleased with the progress we continue to make in developing our emerging retail concepts – Perfect Stranger and THRILLS. These brands and retail formats are continuously improving their offerings and adding the capabilities necessary to successfully scale and deliver attractive financial performance over the years ahead."

Here are the highlights from the Announcement:

• Group sales of $158.0 million, +8.5% versus prior corresponding period (“pcp”), primarily reflecting added CTC contribution

- Universal Store (US) sales of $133.2m (-1.4% vs pcp), LFL sales -5.4%2

- Perfect Stranger sales of $6.6 million (+59.7% vs pcp)

- CTC sales of $25.3m (+4.2% proforma vs pcp)

• Gross profit margins +80 basis points versus pcp, to 59.7%

• Underlying EBIT of $30.8 million, +8.1% versus pcp4

• Statutory net profit after tax (“NPAT”) of $20.7 million (+16.7% versus pcp)

• Adjusted earnings per share (“EPS”) of 26.6 cents per share (“cps”)

• Net cash of $27.4 million as at 31 December 2023

• 6 new stores opened during H1 FY24; 3 Perfect Stranger (“PS”), 2 Universal Stores (“US”) & 1 THRILLS store, bringing total Group stores to 100 (excl. webstores)

• Interim FY24 dividend of 16.5cps declared (up from 14.0cps in prior year).

-ENDS-

More later with another crack at the valuation.

Disc: Held IRL (1.2%)