Top member reports

Straws

Sort by:

Recent

Content is delayed by one month. Upgrade your membership to unlock all content. Click for membership options.

#Financials

stale

They absolutely smashed the financials for FY21.

- Total revenue of $86.2M, up 41% on FY20 (The market cap is $100M you have got to be joking... That is 1x sales for the Price to sales experts)

- NPAT of $8M (that is a P/E ratio of 12 which now starting to make sense as the company has shown profitability & revenue growth in the last 2 financial years)

- Total sales of 31,275 units of electric motorcycles/mopeds, delivered for FY21, up 33% on FY20.

- International sales made up 29,945 units. That is close to 100% you will ever get haha. Clearly they are focusing on growth in China :D Let's underestimate demand in Europe.

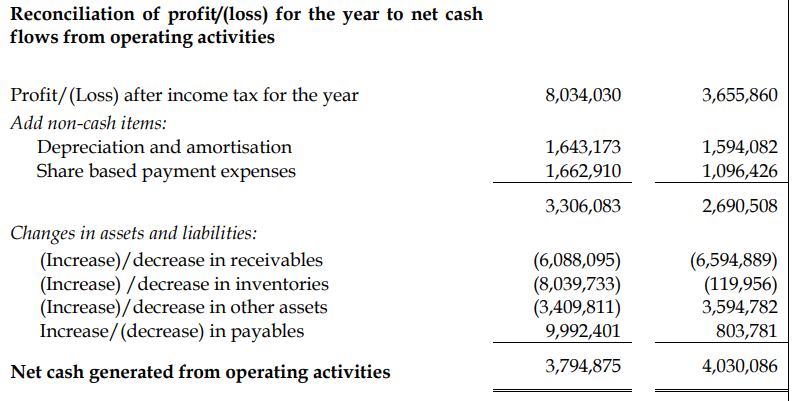

- During production, they generated positive operating cash flows using the indirect method. Unlike the direct method, you are going from Profits to Operating cash flows much like in US GAAP instead of IFRS. My hunch is that they are planning to list in US markets.

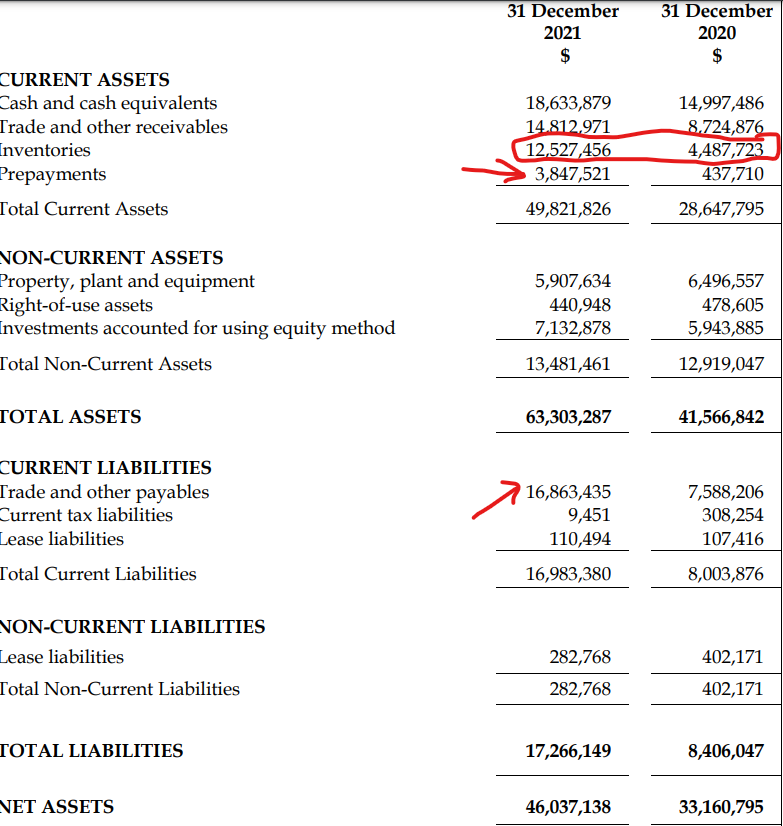

- They have $13M worth of inventory now while growing at 41% of sales. That is incredible for a manufacturing company. Prepayments also went up; where customers are paying cash to Vmoto before the delivery of the product/service. In this case, it is a product, not a service as it is an e-scooter/bike.

- Trade & Other payment liabilities went up and I do not know why, it is the one negative thing in the balance sheet. Especially when we are talking about current liabilities.

I am still stumped as to why the equity value of the business remains at $100M... They pretty much did everything an investor would want.