Overview Comment:

Cash from operations looks good while profitability down. Extra costs throughout the half due to the ordering of new compute and cost of 3rd party compute appear to be temporary issues. Revenues and order book continue to grow as expected so the growth narrative is still there.

General notes:

- A wild swing in the share price throughout the day. Started at $1.80 and closing at $2.44. Price down 4.3% for the day.

- $12.2 of capex in the half (for new compute).

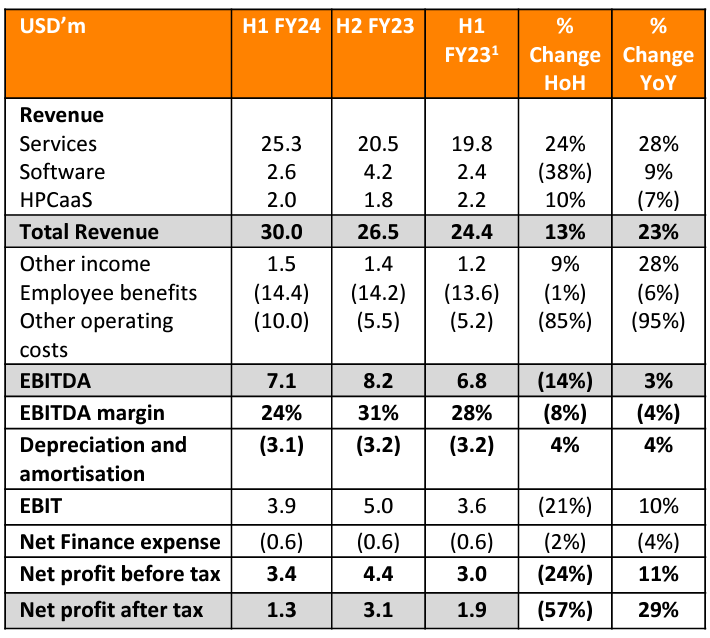

- Financial figures half by half:

Positives:

- Strong revenue growth to $30m. Up 24% HoH or 28% PcP. MP-FWI imaging is gaining momentum and key driver of revenue growth. Record high half for revenue for the company.

- Order book as of end 1HFY24 $40.6m. Up 45% from FY23 end.

- Operating cash flow of $6.2m and expected to strengthen further in H2.

- New compute expected to be available by late April, at this point compute power would have doubled.

- The significant cost of third-party compute compared to DUG's own compute shows their relative efficiency and justification of their business model to complete the compute themselves.

Negatives:

- Still do not have enough compute to meet demand. Started using external compute. This reduced profitability due to the additional cost. Debt levels have increased due to asset financing of new computers.

- Profitability down HoH and PcP.

- HPCaaS still not looking like it will take off as a product.

- New graph showing client relationship length and value. Negative is it showed one client provides around 20% of revenues.

- Cost of construction for Geraldton HPC campus significantly higher than expected.

Has the thesis been broken?

- No, as long as revenue continues to grow and temporary costs such as 3rd party compute can be removed due to DUG getting on top of the compute demand of orders.

Valuation:

- Unchanged at around $2.40-2.50.

What are you expecting and what do you need to see over the next reporting season or generally into the future?

- New compute is able to meet the demand of customers and remove unnecessary extra costs associated with this. I expect higher profitability into the future as a result.

- Start to pay down financing debts as expanded compute meets demand.

- Still watching the CFO revolving door from the past.

- Order book continues to grow. Even after compute starts to meet demand.

- Share price has been on a run. I think it is fairly valued for the growth at $2.40-2.50. Maybe consider trimming at prices above $2.75 unless there is news which justifies a higher valuation.

Note: USD used for all figures except share price.

- New "Multi-Parameter Full Waveform Inversion" (MP-FWI) product had US$11mil of new project awards in the last quarter.

- New project announced. "DUG Nomad" which is a mobile supercomputer installed inside a shipping container. Using the DUG Cool immersion system, the mobile contain can be deployed anywhere for "edge solutions" such as defence, mining and education.

- Generally high tendering activity continues, good outlook.

- Still constrained by computer power and expecting new computers in December.

Trading notes after AGM.

- MD Matt Lamont has sold 2.5mil shares (in wife's name), he still owns around 24 mil shares.

- Wilson asset management has sold down their position to under 5%.

Image from presentation of "DUG Nomad":

Overview Comment:

Very positive results for DUG. Order book is looking very strong already for FY24 so hopefully results can continue to improve from here. Seems like a step change has occurred driven by oil and gas exploration.

General notes:

- NPAT = $4.9m. Slightly below what I hoped but inline with my valuation. However, cash flow was stronger than NPAT.

- Order book at $27.9m. About the same as what it was at during Dec 22. However, in July 23 $18.6m of work was signed.

- Op cash flow seemed very strong but not sure if this was a result of timing?

- Outlook for oil and gas remains strong according to the company.

- Making a $7m investment in the install of new hardware in Houston to support new services projects (this will be asset financed).

Positives:

- Revenue = $50.9m up 51% and 70% in services division.

- My "FCF" = $7.6m.

- Strong operating leverage. Employee and other expenses only rose by $5.6m while revenue grew by about $17.2m.

- July order of work worth $18.6m is a strong start to FY24.

- Turnaround in services is due to expansion into new markets and commercialisations of DUG's "multi-parameter FWI imaging".

- Net cash of $5.2m. Very positive that the company is no longer in debt. Additionally $7.1m cash was received i August due to repayment of a loan funded share plan.

- Market liked the results up 10%.

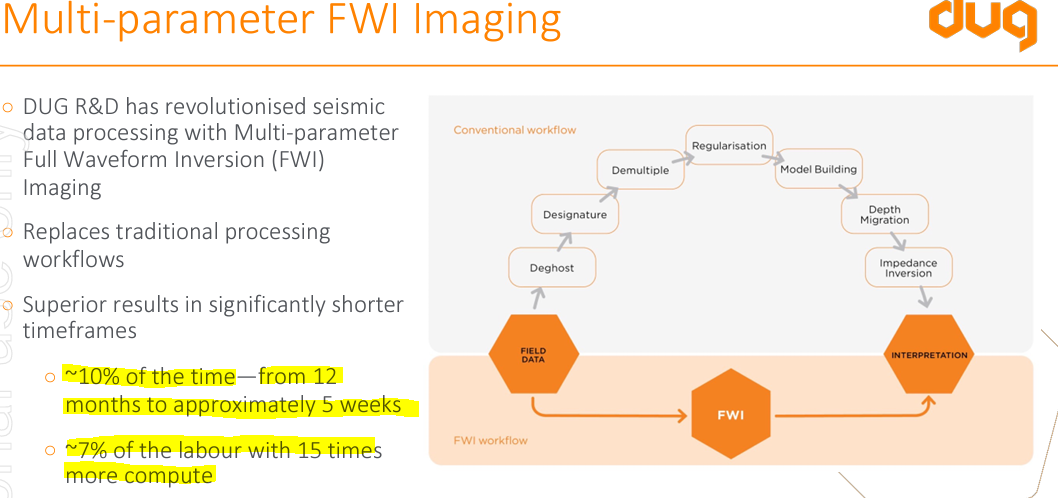

- Given some numbers in the presentation the FWI product appears to be a leap in magnitude type better product. It can replace traditional processing of imaging of seismic data. The improvement for customers shown below in presentation:

- Multiple examples provided by the company in their presentation of the significant value proposition they provide to their customers. See bottom of post for copied quotes.

Negatives:

- HPCaaS only up 2% to $4.0m of revenue. Clearly not a focus anymore for growth. No sign of the graph of monthly sales again.

Has the thesis been broken?

- No, opposite, all seems to be going well. Starting to see DUG make some real progress and becoming a valuable resource for its customers. Examples of order of magnitude improvements such as FWI will help adoption. Lots of investment in increasing computer side indicators expected growth in compute time which directly relates to revenue, especially given the just in time format of their computer setups.

- Worried about valuation here but all depends on what happens with profitability. The order book as been a very rough guide as to the revenue over the next 6-month period over the previous year. As of end of July this figure is indicting a large improvement in revenue potentially. Given the operating leverage that has appeared in this year's results if things go well DUG will probably look cheap, if not expensive. Adding to position very cautiously.

What are you expecting and what do you need to see over the next reporting season or generally into the future?

- It is clear oil and gas through FWI imaging is a key driver for revenue growth for the business. If oil and gas explorations slows DUG will be impacted.

- If DUG continues to grow revenues rapidly it will be through the continued expansion of FWI.

- Revenues to be above FY23. Order book at the end of FY23 $27.9m with $18.6m added to that in July. Order book as of June 30 22 was only $22.2m.

- Watch the order book numbers. Does it continue to grow?

- Share price has been on a run. All news has been generally positive in recent times. Watch out if some bad news hits, I would expect a pull back.

NOTE: All values in USD unless otherwise specified.

Value proposition quotes in company presentation: