Discl: Held IRL and in SM

SUMMARY

- Progressing nicely on all trial fronts - going as best and as fast as can be it would seem

- The key thing I am watching is funding: 30 June 25 cash balance is $10.5m, with $4.8m of grant funding to come + FY25 R&D Tax Incentive of ~$2.0m, so total funding of ~$17.3m is available - at $3.0m operational burn, this is 5.8 quarters of funding, which should take EMV to sometime 2QFY2027 - that feels reasonable, particularly given how relentless EMV has and will continue to be with the grant opportunities

OPERATIONAL UPDATE

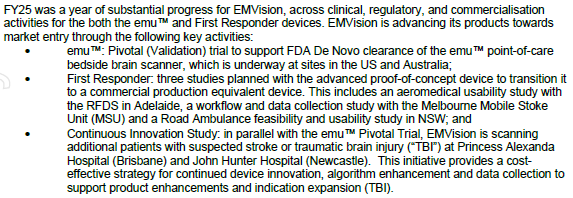

Nothing exciting or new about the EMV trading update as all the news has already been announced prior - this is a good summary of where things are at:

This was interesting as it provides context to understanding the US Defence market for Portable Field Scanners which was mentioned in an earlier announcement.

FINANCIALS

- Excluding the $0.98m 1st payment from the $5.0m Industry Growth Program Grant announced in June, EMV burned $3.05m this quarter

- Only change worth noting was that R&D expenses fell to $0.8m, a sharp drop from the previous 2 quarter’s spend of $1.2m each in 2Q and 3Q, respectively. This is consistent with Scott saying that R&D expenses will fall as they focus on trials.

Summary

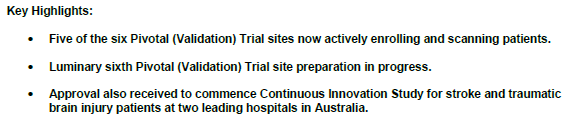

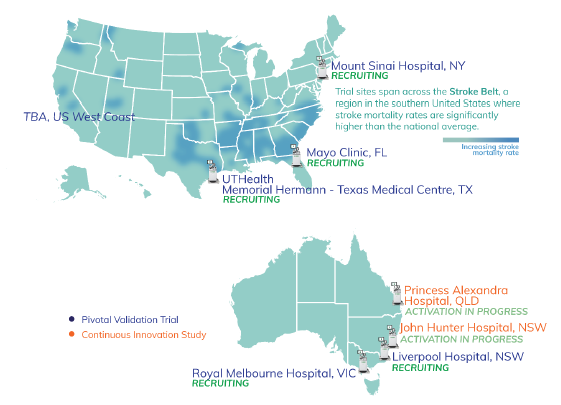

- Pivotal (Validation) Trial is moving steadily - all sites are luminary, high volume comprehensive stroke centres

- Continuous Innovation Trail is good front end loading for the indication expansion into traumatic brain injury

- All are occurring at major stroke centres - nice map to show where trials are occurring, which in the US, are also likely to be where commercial activities will be focused on per, as Scott indicated in the SM interview

Continuous Innovation Study

In parallel to the Pivotal Trial, EMV is implementing a cost-effective strategy for continued device innovation, algorithm enhancement and data to support indication expansion for traumatic brain injury

Ethics approval received to commence scanning patients with suspected stroke or traumatic brain injury at Princess Alexandra Hospital BNE and John Hunter Hospital NTL - both sites are high volume Comprehensive Stroke and Level 1 Trauma Centres.

Nice award! To put this in perspective:

- At 31 Mar 2025, EMV had available funding of $12.6m, so this increases available funding to $17.6m, with the $5m to be progressively dispensed quarterly

- Actual cash outflow, excluding Grants and Incentives, in FY2025 to 31 Mar 2025 was $8.8m

- There thus appears to be funding for roughly 18M, which should get EMV past FDA approval, I suspect

I still expect a capital raise but the grant removes the immediate need for that, pushing the timing of any raise nearer to commercial launch. Am very OK with that prospect as EMV has been very careful in its funding approach.

Next week’s SM chat with Scott is timely to get a better sense of how it is thinking about funding.

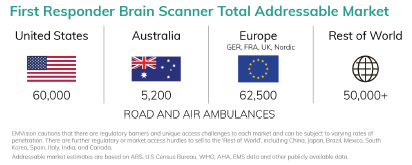

On a separate note, this was a good summary of the TAM for the First Responder Unit. I don’t think its new, but its the first time I have taken notice of it!

Discl: Held IRL and in SM

Nothing newsworthy as all of the business updates have been previously announced

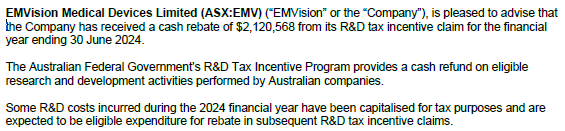

- A good cash flow quarter as $2.1m FY24 R&D Tax Rebate was received this quarter which reduced the cash outflow to a low $1.07m

- Cash burn would have been $3.2m excluding the Tax Rebate, about the same as 2QFY25, so no concerns

- The $12.6m cash on hand + $0.8m Stroke Alliance Grant, $13.4m will last ~13M ie Mar-April 2026, at the current burn rate

Announcement says “remains well funded” but there has been no announcement of any funding plans for the latter part of CY2026 thus far. Management has a good track record of proactively paving the way forward, so I do expect news on this front should be forthcoming soon. Would be significantly more comfortable once this funding issue is decisively sorted.

Both a capital raise, particularly as FDA approval for emu becomes imminent would be a distinct possibility, or short term debt for 1-2 years to provide funding coverage for the commercialisation startup, would make sense.

Discl: Held IRL and in SM

In these turbulent times, happy to take whatever positive news is on offer by any of my companies! 2 positive things out of this:

- emu Pivotal Trials continue to chug along nicely

- It absolutely can't hurt, from the perspectives of (1) the product (2) company reputation and (2) trial integrity, when one of your US trial sites is THE Mayo Clinic ..

Discl: Held IRL and in SM

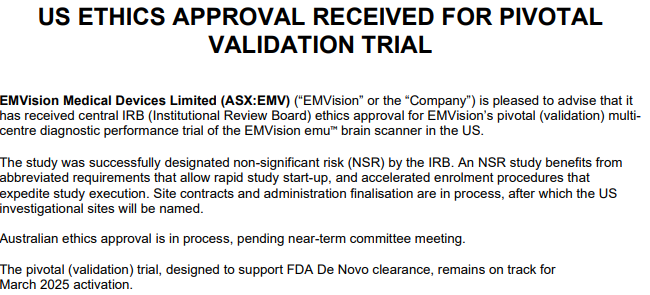

Another on-track tick obtained to keep the trials moving forward. Things are happening quickly, and very much on the right track!

Discl: Held IRL and in SM

Not unexpected - this was 1 of 2 sources of funding that EMV flagged for FY2025. But good to have it locked in regardless.

Probably adds a quarter of funding more to the 9.7 quarters of funding as of end-Sep 2024.

Discl: Held IRL and in SM

There were some interesting slides in the EMV FY2024 slide pack. No new news as EMV has communicated clearly and regularly to the market but there were a few background/context slides which was interesting to note.

Discl: Held IRL and in SM

The Stroke Indication was always front-and-centre

Seeing “Traumatic Brain Injury” as a second indication for the first time since I started deep-diving EMV

Also seeing the introduction of “Time Sensitive Medical Emergencies” for the first time - makes good sense and probably provides an indication of EMV’s direction and focus areas in the longer term

The step improvement in size and mobility illustrates how game changing EMV’s products will be in improving the diagnosis and treatment options

Don’t recall seeing a TAM slide like this before, so this was really useful

No target sale price for First Responder yet, so size of the TAM is unclear, but the significantly higher number of potential units surprised me somewhat

Nice summary of the pre-validation clinical results - that is seriously impressive accuracy

Nice summary of what’s ahead

End CY2025 Market Entry target is key from a funding standpoint - if that holds, and assuming no additional funding is obtained, EMV should have consumed ~55% of available cash at 30 Sep 2024 to get to that point (5 quarters vs ~9.4 quarters available funding)

First Responder timeline

Amen, but I would have liked to have seen a line or 2 to confirm “we have available cash to see us through to market entry”!

NEURODIAGNOSTIC ALGORITHMS DELIVER EXCELLENT RESULTS IN EMVIEW STUDY

My medical expertise goes as far as applying a band aid on a small cut wound, but this looked like good news in the stroke detection capabilities of Emu.

The absolute Sensitivity (correct diagnosis)/Specificity (negative diagnosis) looked really good in absolute terms in the highlights. What blew me away though was how good those results are relative to the current Gold standard CT scans, in absolute terms AND given the size and mobility of the device.

Entering the Validation Trial is another milestone which adds to the good EMV track record of defining and meeting milestones.

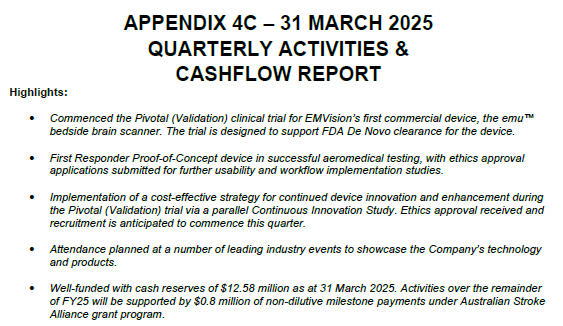

I do have an emerging concern about cash reserves though from the last Appendix 4C.

- Cash balance last Quarter was $16.8m, and secured funding from various agencies ends this current Quarter, with $0.8m due, with the reserves funding ~9.8 quarters.

- Excluding receipts from Govt Grants/Other Funding, EMV burns between $2.3m and $3.5m per quarter in the last 5 quarters.

- The $4m needed to fund the validation trial should be completely manageable, as it will already have been planned for and will likely be BAU, not incremental cost.

But without additional funding clearly lined up to replace the end of the existing formal funding, things do start to feel tighter ... not a huge cause of concern yet, but one which I am watching very closely.

Held IRL and in SM

Back to a “normal” Quarter after the spike in spend in R&D Expenses in 4QFY2024 - combination of R&D expenses and Staff Costs have reverted back to normal quarterly levels.

At the current cash burn rate, there is funding for 9.7 quarters or 2 years and a bit.

Keeping a close eye on the funding situation as the ASA funding is down to the last $0.8m, expected in 2QFY25, and the FY24 R&D Tax Incentive claim. Not an immediate cause of concern given that FDA approval is going to plan, but need to keep a closer watch on this from hereon.

Disc: Held IRL and in SM

------

OPERATIONAL HIGHLIGHTS SUMMARY

‘EMView’ multi-centre pre-validation trial recruitment complete, enrolling over 300 participants. Stage 3 trial results anticipated in November.

277 suspected stroke patients provided valuable data for EMV’s “blood or not” and “ischemia or not” AI algorithms

EMVision continues validation trial preparations after positive FDA engagement.

The study design was confirmed as a multi-centre, prospective, consecutive, paired diagnosis, diagnostic performance study that is anticipated to enrol up to 300 suspected stroke patients at a minimum 5 stroke centres including a minimum 3 based in the United States.

Transformative ultra-light weight First Responder Proof-of-Concept brain scanner device unveiled. Preparations for road and air study well advanced.

- Ultra-light weight (<12kgs), non-ionising, non-invasive device that can be easily operated by trained healthcare professionals and is designed for cost-effectiveness, to enable rapid stroke and stroke sub-type diagnosis at the point-of-care.

- Represents an opportunity to fundamentally transform stroke and thereafter traumatic brain injury (TBI) outcomes, for all patients, regardless of their location.

- Intended to enable much earlier diagnosis and therefore much earlier triage, transfer or treatment decisions, which in acute stroke and TBI is proven to lead to improved patient outcomes.

- Delivery of the First Responder PoC device satisfied the "Ambulance Device Fabrication" milestone under the Company's Project Agreement with the Australian Stroke Alliance (ASA), which is funded by the Commonwealth of Australia's Medical Research Future Fund (MRFF), resulting in a $600,000 non-dilutive milestone payment during the quarter.

- Comparative initial bench tests have been conducted with the First Responder PoC device and emu™ bedside scanners.

- Pleasingly, the First Responder PoC device is demonstrating at a minimum equivalent sensing performance in these initial tests

Well-funded with cash reserves of $16.85 million. Activities over the next few months will be supported by further non-dilutive funding from the Company’s FY24 R&D Tax Incentive claim, currently being finalised, and the Australian Stroke Alliance grant program.

$1.72m cash outflow within normal quarterly cash outflow ranges

9.78 quarters of funding available

EMVision’s activities over the next few months will be supported by further non-dilutive funding from its FY24 R&D Tax Incentive claim, currently being finalised, and the ASA grant program. The final ASA milestone payments are due on achievement of telemedicine and road/air integration activities ($400,000) and commencement of pilot studies of the first responder device targeted for first quarter CY 2025 ($400,000).

EMV announced the following milestones today:

- reached its recruitment target for Stage 3 of its multi-site clinical trial of 30 haemorrhagic stroke patients, rapid achievement of this target is attributed to the continued positive engagement and goodwill at the investigational sites as well as the introduction of several recruitment accelerating initiatives under Stage 3

- Company’s FDA pre-submission package has been delivered and is under FDA review prior to a consultation meeting in the coming months

- In parallel, activities to initiate the Validation clinical trial are well under way, including protocol finalisation, CRO appointment and engagement of luminary investigational sites.

Continues the steady progress achieved thus far!

Discl: Held IRL and in SM

Interim Stage 2 Analysis Confirms Hyperacute and Acute Ischaemic Stroke Detection Capabilities

Stage 2 data confirms positive AI algorithm performance to help answer the “clot or not” question. This comes off the back of earlier positive news of the AI detecting "blood or not".

Key clinical question of “ischaemia or not” (“clot or not”) - current non-contrast computed tomography NCCT scans shows a limited sensitivity to detecting acute ischaemia

Other tests are required for patients with suspected ischemic stroke to confirm diagnosis - advanced imaging modalities such as CT Angiogram, CT Perfusion or MRI are often used to confirm the presence of ischaemia (‘clot or not’) and determine a patient’s eligibility for thrombectomy (clot retrieval).

Depending on the neuro-diagnosis, and treatment capabilities of the hospital to perform urgent intervention, a time critical decision is whether to transfer the patient to a comprehensive stroke centre, or not.

Continues the good progress and news on Stage 2 Trials.

Discl: Held IRL and SM

SUMMARY

- EMV has been making good progress on all fronts - trials, pre-FDA submission, First Responder System proof-of-concept

- Remains well funded following Keysight Investment with $21.35m cash reserves, $2.6m remaining grant funding ontop of this

- No concerns - it feels like there is good project cadence on the several fronts that EMV is focused on

Summary of Highlights - Most Already Announced Previously

- Strategic $15.28m investment from Keysight Technologies

- Stage 2 clinical trial insights confirm stroke diagnostic and clinical viability

- Time from start of scan data acquisition to removal of the device was 5.5 minutes (range from 4.2 to 14.6 minutes), confirming the emu device seamlessly fits into acute stroke workflows, in time sensitive situations

- Preparations well advanced for a pre-submission meeting with the FDA

- To clarify and confirm the points remaining to finalise the Validation Trial package

- Pre-submission package is well-advanced for near-term submission

- Validation Trial designed will be finalise aligned to the FDA’s expectations to ensure the trial will deliver the clinical data critical to the emu’s De Novo market clearance application

- First Responder System on track

- Progressing well, leading to the near-term assembly of the proof-of-concept unit

- Ethics approval received for healthy human volunteer testing

- $21.35m cash reserves as at 31 Mar 2024 - nothing extraordinary

- $2.65m of funding is remaining from the 3 Grant Programs below

Another positive announcement which the market seems to have liked. While the quantum of the funding release is only $0.6m, it is EMV's continuation of a stellar track record of meeting milestone obligations that is the key positive here.

Discl: Held IRL and in SM

Not much to write home about, a good thing! Things look like they are progressing nicely to plan on all fronts of the trials, algorithm analysis, Gen 2 prototype build and cash reserves. Good to see the showcasing going international and generating interest and leads.