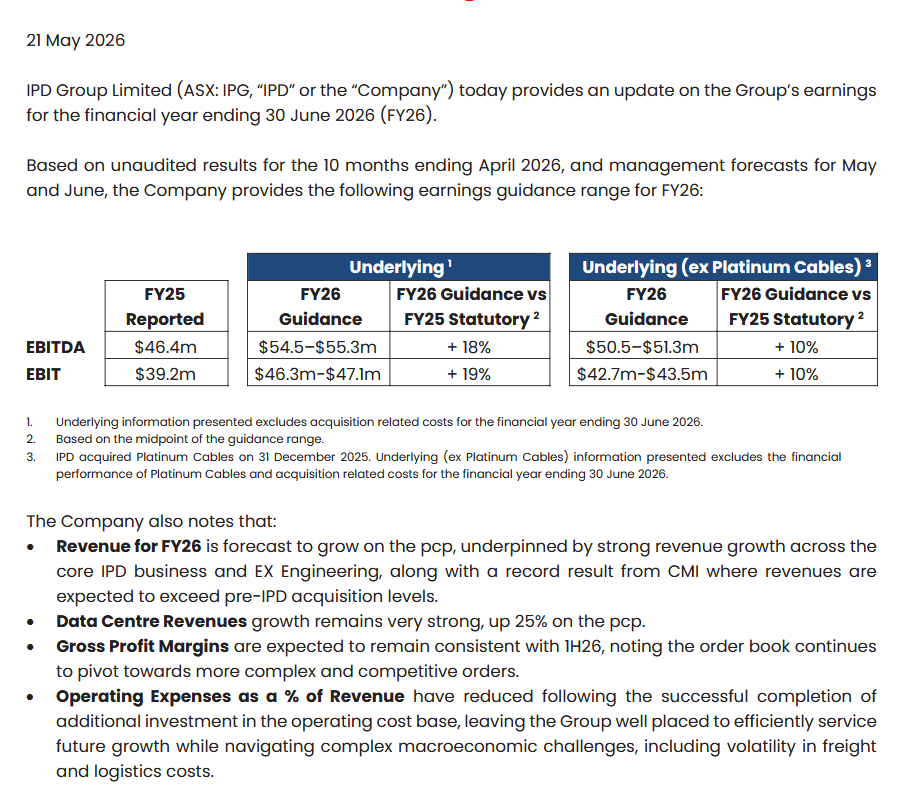

IPD Group put out what looks like solid guidance

But the news sent the shares down 12% from around $6 to $560.

I'll leave the others to decide whether this fall was justified.. Results below.

[held]

Bell special if you need to find the source of the recent price declines

[held]

Looks good on preopen

[Held]

Bell Potter report downloaded from Factiva. Price target 5.75

Screen capture of one page

[held]

Full text from behind the paywall of the Weekend Australian.

Interesting article that highlights the valuation gap of the CMI sale vs the book value of CMI from Excelsior but not getting any answers why this has happened.

Excelsior’s valuation perplexity - 16dec23

[held]

IPD Group is undergoing a capital raising.

Funds raised: $65m

Extra shares: 16.5m

Synergies: Expected but not included

Because I don't have time, hopefully someone can do an exact valuation. If you are inclined go to fightfinance for the methodology after clicking the answers.

Roughly we should expect a market cap from 364m to 429m and SOI of 103m shares.

Some important slides that will help

But I'm sure the market will try and drag this below $4.

As I already topped up at the recent lows, I think I have enough shares already - not sure if I take up the rights issue.

[held]

Good to see Mirabooka Investments still holding IPG amid the volatility

Even though the holding has risen, I noticed they did sell recently to rebalance the portfolio.

Aug 2023:

Sept 2023:

IPD group moves into the top 10 along with some heavy hitters such as James Hardie, Hub24, Breville and Carsales. Literally a minnow in the ocean. So I don't blame Mirabooka for selling a bit..

Mirabooka investments is an LIC under code ASX:MIR.

[held]

In case no one noticed, IPD group got an upgrade from Bell Potter. Target price increase of 38% to $5.50.

Explains the share price going up 5% today to $4.80

See below for the estimates. Will definitely pin this to the wall and see if these estimates can be achieved

[held]

IPD Group acquires EX engineering, a firm specialising in custom equipment used in hazard areas and achieving another prospectus objective.

Apart from leveraging/selling this expertise in the eastern states, there are not much details on synergies.

Not much detail on financials of EX engineering as they are private but after briefly going through their website it seems like a good fit.

10.2m with 9.2 in cash and 1m in shares so not much dilution. Plus an earnout provision based on normalised ebitda for a total of 11.4m if I am reading correctly but there is no details on trigger conditions for the earnout (I assume there would be - correct me if I'm wrong). So that is total earnout of 1.2m? Just great when announcements like this make us stretch our brain cells!

Normalised ebitda currently 2.5m.

More details to be revealed on 25h August.

[held]

Upgraded FY23 Guidance

Seems solid with EBIT around 30-40% growth. Perhaps fairly priced on retrospective PE basis and why it sold off today.

IPD Group Limited (ASX: IPG, “IPD” or the “Company”) today provides guidance on the Group’s full year earnings for the financial year ending 30 June 2023 (FY23).

The Company expects earnings to exceed the FY22 Full Year results due to the continued strong operating performance as previously announced on the 24 February 2023.

[held]

Not many acquisitions as claimed by many from what I can see. Unless I have missed something.

As comparison, look at Swoop holdings - 13 acquisitions.

[held]

Further adding to recent straws which NewbieHK has already summed up.

On the acquisition front, IPD had already rejected a few potential opportunities and are being selective.

Probably this is what the market may have also been nervous about judging by the price action in the last few weeks..

[held]

Financial FY22 results announced and generally a beat against prospectus forecasts. Including a dividend which I was predicting when I first bought about a few months ago as they were already making net profit after tax before.

The only concerns which probably contributed to the selloff today:

- Some disruptions in back office operations from the Sri Lanka economic crisis. IPD are mitigating this by bringing some functions over to Manila

- Guidance not provided until Nov 2022 due to supply chain uncertainty.

Adding as a straw since I can't additional valuations as myself on top of the one I added for Shaw and Partners

IPD Group Price Target Raised 19% to A$2.15/Share by Bell Potter

Bell potter also named this as one of their top picks for FY23

Maybe no longer under the radar :(

Held

Upgraded profit guidance and background.

IPD Group supplies products for the electrical and power industry. Lately they have been expanding into supplying components for charging stations of EVs.

And profitable after tax.

Only listed last year. Very much under the radar at 140m market cap.

Unfortunately hard to find any shares on sale due to the amount of shares available.

[Held]